MF3d/E+ via Getty Images

Russia’s invasion of Ukraine has triggered plans by many oil and natural gas importing countries to curtail Russian imports and transition to what may be perceived as more reliable, less unsavory sources of supply while accelerating their transitions to green energy – opening the door for the U.S. to re-emerge as the world’s dominant oil and gas provider.

Reducing dependency on Russian energy will be onerous, particularly for Europe, which imports about 30% of its natural gas and 25% of its oil from Russia. So far, the U.S. and some EU countries have curtailed imports of Russian crude oil and if more countries follow suit, there will be strains in the global markets to adjust to accommodate a reconfiguration of the 5 million Bbl/d (barrels per day) of waterborne exports from Russia. Indeed, Russia’s oil tanker exports are being offered at a significant discount of roughly $30/Bbl to Brent, indicating that new buyers aren’t fully absorbing the demand lost in the boycott.

Recent releases from the U.S. Strategic Petroleum Reserve (SPR) (30 million Bbl) and from international partners (30 million Bbl) provide minimal relief. Potential deals – if they could even be reached – with Iran (1 million to 1.5 million Bbl/d) and Venezuela (less than 1 million Bbl/d) would still not be enough to fill the void. If anything, the recently announced historic SPR release (1 million Bbl/d for six months) suggests that these deals are unlikely to be completed soon and emergency responses are needed to meet demand.

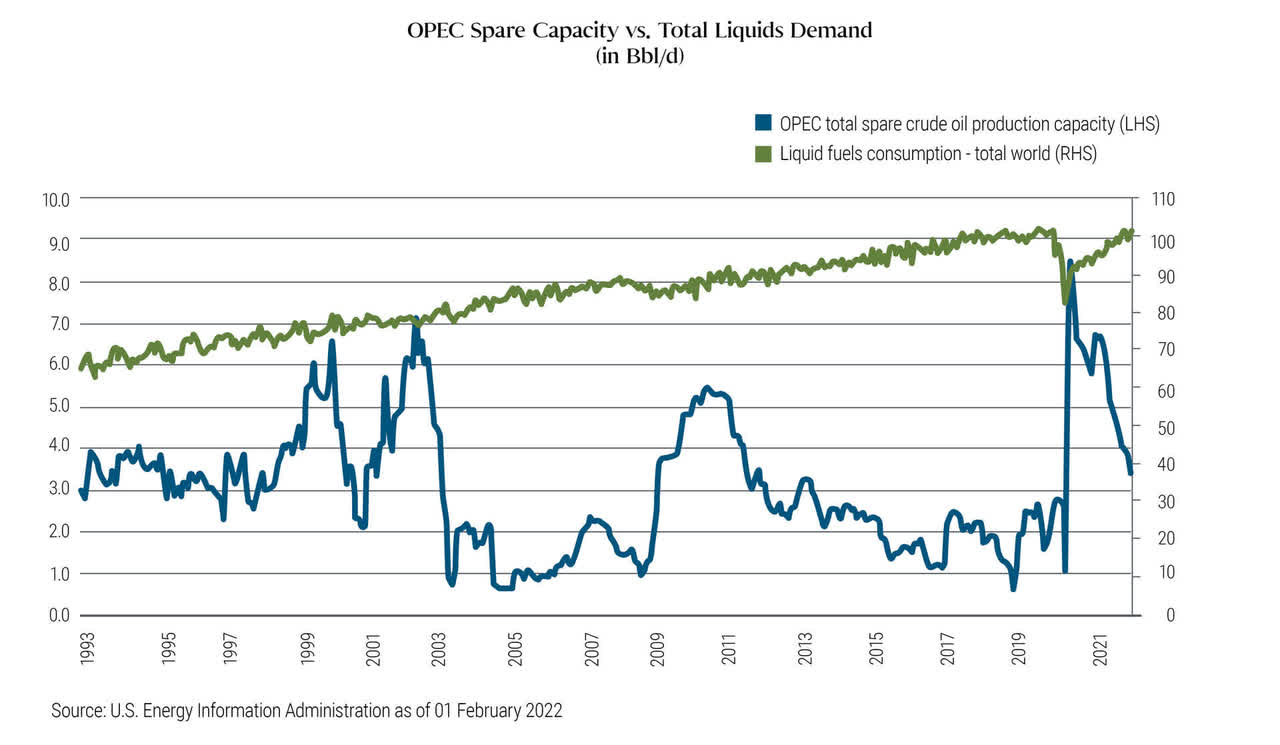

The war in Ukraine comes at a particularly vulnerable time of tight inventory and a low backlog of oil wells, with little room for disruption. According to the U.S. Energy Information Agency, prior to Russian sanctions, OPEC+ excess capacity stood at only 3%-3.5%, or roughly 3-3.5 Bbl/d, down from about 8% to 9% in 2002. However, from recent discussions with energy officials in the Middle East, true spare capacity could be even lower at just 2.5%.

We believe OPEC+ will likely stick to its current plan and not increase output further, despite higher oil prices. This is because if the cartel decided to bring more volumes online, the investment community might react to the prospect of little-to-no spare capacity by sending oil prices even higher. Moreover, Russia is the joint chair of OPEC+, leaving it unclear whether it will be able to fulfill its share of the cartel’s production.

U.S. shale oil production positioned to regain dominance

The U.S shale industry – which produces both crude oil and natural gas – is well-positioned to increase production in the lower 48 states, but it will take time. During the last few years, energy producers curbed spending on new wells, following two mini U.S. shale boom and bust cycles, the latest causing roughly $55 billion of defaults. Responding to shareholder demands for strong investment returns, producers pivoted from a focus on production growth (“drill baby drill”) to one of capital discipline – maintaining modest leverage metrics and consistent cash returns on volume growth of just 0% to 5%.

As a result, exploration and production (E&P) operators face shortages in oil rigs (utilization is approaching 90%), frac fleets[i] (which are completely sold out), and labor. E&P executives have indicated they could deploy more capital and maintain high profitability levels – thanks to improvements in drilling and completion technology – but estimate it will take them up to 12 months to increase current production volumes. In our view, the U.S. Shale “3.0 model” (e.g., spending within cash flow) of reliable production volumes and consistent cash returns could make U.S. energy attractive to countries overseas over the medium- to long-term.

Rising oil prices set to accelerate green energy investments

Along with the growth in U.S. shale production, we expect recent geopolitical events and consequent rise in oil and gas prices to accelerate investments in green energy. As green energy becomes a larger component of the overall global supply, traditional U.S. oil and gas will likely remain a dependable baseload power source in the overall market.

Investment implications

The global energy shortage and consequent elevated price levels seem likely to persist in the medium term, sparking a resurgence in U.S. shale oil and natural gas production. Yet, history has shown that energy investing is fraught with risks and bouts of elevated volatility. A new COVID-19-related global lockdown or a Fed overshoot in the current hiking cycle could start a global recession, diminishing demand and prices for hydrocarbons. We approach this sector carefully by leveraging deep expertise across the entire energy value chain and maintaining appropriate risk mitigation.

OPEC’s spare crude oil production capacity is only about 3% of the total demand

U.S. Energy Information Administration

[i] A fracturing (fracing) fleet is the equipment owned and operated by an oilfield service company that is used to extract natural gas liquids and oil through the earth through hydraulic fracturing.

Disclosures

All data and views are as of 01 February 2022 unless otherwise noted. Source: U.S. Energy Information Administration

Please note that this communication contains the opinions of the manager as of the date sent, and may not have been updated to reflect real-time market developments. All opinions are subject to change without notice.

All investments contain risk and may lose value. The energy sector is susceptible to adverse economic, environmental, or regulatory occurrences affecting that sector. Pipeline companies are subject to changes in the demand for and availability of products for gathering, transportation, processing or sale due to natural declines in reserves and production in the supply areas serviced by the companies’ facilities, sharp decreases in crude oil or natural gas prices that cause producers to curtail production or reduce capital spending for exploration activities, and environmental regulation.

The issuers referenced are examples of issuers PIMCO considers to be well known and that may fall into the stated sector. References to specific issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold securities of those issuers. PIMCO products and strategies may or may not include the securities of the issuers referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries, and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2022, PIMCO.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment