tracielouise

Just over a year ago, I wrote on Triple Flag (NYSE:TFPM), a mid-cap royalty/streaming company with a large portfolio of producing assets on several high-quality mines, including Northparkes, Fosterville, Buritica, and Cerro Lindo. In the article, I note that while the stock was reasonably valued, pullbacks below US$9.70 would provide much better buying opportunities vs. chasing the stock. Since the stock pulled back to these levels in December 2021, it has performed quite well and was one of the best-performing royalty/streaming stocks last year. In this update, we’ll take a closer look at the company following its recent Maverix (MMX) acquisition and try and discern whether it’s worth investing in at current prices.

Camino Rojo Oxides (MMX NSR Royalty) (Orla Mining Presentation)

Q3 Results

Triple Flag Precious Metals (“Triple Flag”) released its Q3 results in November, reporting quarterly sales of ~19,500 gold-equivalent ounces [GEOs], a 6% decline from the year-ago period. This was related to lower sales at Cerro Lindo (timing of streaming deliveries), lower production at Fosterville (lower grades and tonnes processed), lower production at Buritica (temporary blockade of mine), and fewer sales from Northparkes (shipment delayed to Q4 from Q3). On the positive side, Agnico Eagle (AEM) continues to have exploration success at Fosterville, Northparkes enjoyed record throughput with its ramp-up of the E26 Lift 1 North Cave ahead of schedule. Plus, Calibre’s (OTCQX:CXBMF) Eastern Borosi could see production in 2023 ahead of the previously planned schedule (environmental permits granted in October).

Triple Flag – Quarterly GEO Contribution by Mine (Company Filings, Author’s Chart)

While these are all positive developments, Triple Flag’s financial results were softer in Q3, with revenue at its lowest levels since 2020 ($33.8 million), impacted by one-time issues (delayed shipments at Cerro Lindo and Northparkes) and much weaker metals prices. Fortunately, Fosterville is expected to have a strong Q4 on deck with higher-grade stopes planned, Pumpkin Hollow’s restart and financing package has closed, and the environment for transacting on new royalties and streams has not been better for years, with Triple Flag in a nice position as it sits on $600+ million in liquidity. Its most recent activity was the addition of a GRR and gold/silver stream on a copper-zinc mine in South Africa and a 2.5% NSR royalty on the TB North Project in Ontario, Canada.

Triple Flag – Quarterly Revenue (Company Filings, Author’s Chart)

However, the major news of the past year was the company’s announcement that it would be acquiring Maverix Metals (MMX), one of the largest royalty/streaming companies in the junior space, on track to report sales of ~30,000 GEOs this year alone. This transaction is not only expected to give Triple Flag greater scale with sales of nearly 120,000 GEOs per annum in 2023 ($200+ million in revenue), but it also addresses two of the rare negative attributes about Triple Flag – its relatively low trading liquidity and concentrated shareholder base, and its relatively high concentration to its three top assets (Northparkes, RBPlat, and Cerro Lindo). Despite Maverix being a solid addition to the portfolio and arguably the most sought-after takeover target in the junior space, the company paid an attractive price for MMX (~1.0x P/NAV). Let’s take a closer look below:

Maverix Acquisition

Triple Flag announced in early November that it would be acquiring Maverix for $606 million in shares and cash or a 22% premium based on the 10-day volume-weighted average share prices of both companies. The deal is expected to provide for ~$7 million in pre-tax synergies on an annual basis, and it will bring together two very solid portfolios, with the deal addressing weaker points in both companies’ portfolios. In Triple Flag’s case, it has an impressive attributable production profile (90,000 GEOs). Still, its GEOs were quite concentrated in its top four assets, as was its NAV, and one of its top-4 contributors has seen its best years behind it (Fosterville). With the addition of Maverix’s portfolio, its top-4 assets will no longer contribute to nearly 60% of NAV, and its top asset will decline from ~30% to ~25% of total NAV.

The second benefit to Triple Flag is that while the company has a very productive portfolio with less than half the assets of its intermediate peers but a similar production profile, its portfolio did lack depth, with only a handful of key development assets set to contribute later this decade (depth is something that Maverix has in spades). The third benefit is that Elliott Investment Management had a massive stake in the stock, and this large stake contributed to lower liquidity (50-day average volume on the US Market of 12,000 shares traded as of November), which may have deterred some funds from owning the stock. However, post-acquisition, we should see a significant increase in liquidity, and Elliott’s stake will decline to near 65% vs. more than 80% previously. These are key benefits that make this transaction logical for TFPM.

In Maverix’s case, the company had a substantial royalty/streaming portfolio with ~150 total assets (14 paying assets), plus a very mature and diversified development pipeline concentrated in Tier-1 jurisdictions. However, with relatively low liquidity as well, a smaller scale than its intermediate peers, and some adverse developments over the past year (Omolon uncertainty, continued underperformance from Moss with ~$2,000/oz AISC, and a deteriorating security situation at Karma), the stock was having a difficult time re-rating despite several positive updates in its development portfolio. Fortunately, Triple Flag’s large production profile adds key diversification; the combined company will likely have much higher trading liquidity, and its significantly higher cash flow will allow it to transact more frequently and possibly do more significant deals similar to the royalty/streaming majors.

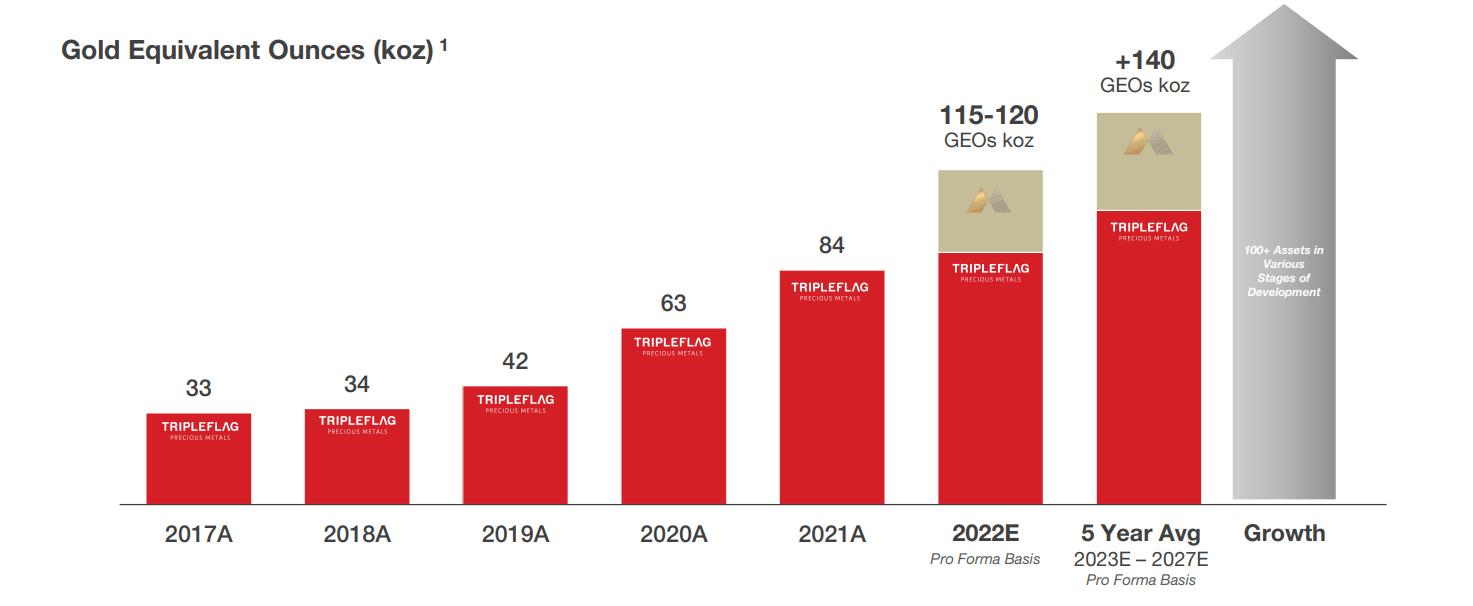

Triple Flag (Post-Deal) – Annual GEO Estimates (Company Presentation)

Looking at the below chart of Maverix’s attributable production, some Triple Flag investors might believe that they paid a rich price, especially with one of Maverix’s largest producing assets being Omolon Hub (Russia) and one of its best assets moving offline while Agnico works to optimize the operation for an eventual restart. However, the below attributable production profile displays a well-diversified company, and the chart does not do Maverix justice. This is because the Beta Hunt royalty asset will see a significant boost post-H2-2023 as Karora (OTCQX:KRRGF) ramps up mine production to 2.0+ million tonnes per annum. Additionally, while Hope Bay may not be contributing today, this could be a 3,000 GEO per annum asset held by the most aggressive driller sector-wide.

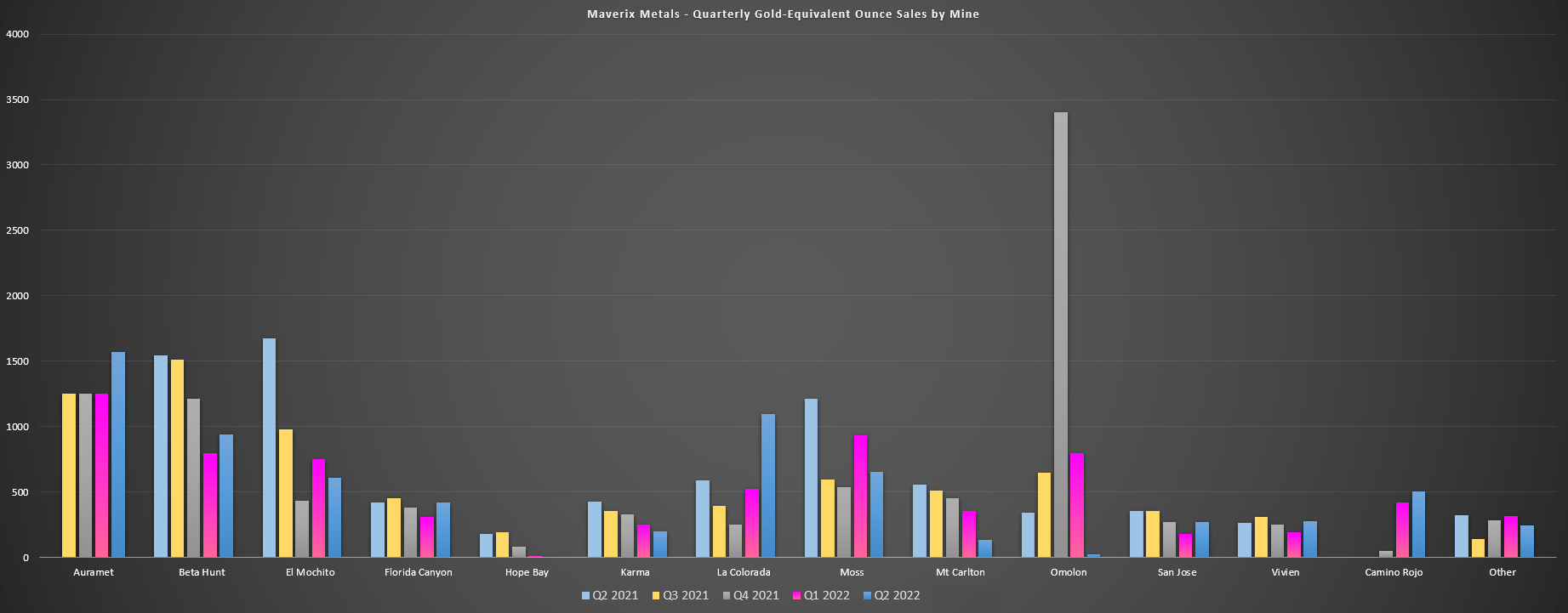

Maverix Quarterly GEO Sales (Company Filings, Author’s Chart)

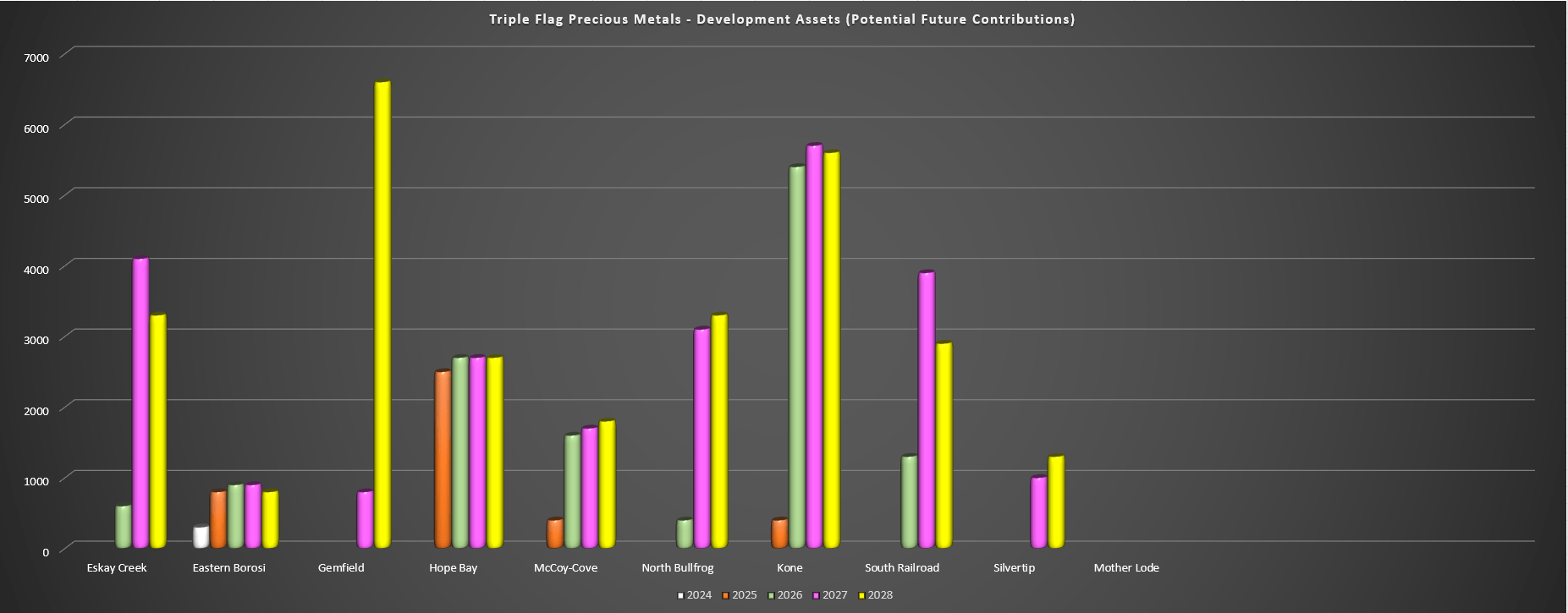

Outside of these two long-term positives, Maverix’s development portfolio is one of the best in the sector among junior/intermediate producers, with nearly a dozen solid royalty assets. Some examples are Mother Lode, North Bullfrog, Gemfields, McCoy-Cove, and South Railroad, all in Nevada, as well as Hope Bay in Nunavut, Silvertip and Eskay Creek in British Columbia, and Kone in Cote d’Ivoire. The below chart, which is conceptual and should not be relied upon given that these are rough estimates, shows what contributions from this development portfolio could look like (2024-2028). We can see that even if just 7/9 of these assets head into production by 2028, Triple Flag would see a 20,000+ GEO per annum boost on an incremental basis. In a best-case scenario, attributable GEOs could increase to closer to 30,000 per annum (2028 estimates).

Triple Flag/Maverix – Development Assets (Potential Future Contributions) (Company Filings, Author’s Chart & Estimates)

So, when combined with Eastern Borosi, which could begin contributing next year (Triple Flag’s portfolio), the ATO Phase II Expansion, and a Pumpkin Hollow restart at a higher contribution rate, there is a clear path to 150,000+ GEOs per annum even if Fosterville never returns to a 400,000+ ounce per annum production rate (one of Triple Flag’s key contributors that padded its growth from 2019-2022). In summary, I think Triple Flag got a solid deal for Maverix with its price paid, and it’s a bonus that the bulk of this development portfolio will offer new ounces coming from Tier-1 ranked jurisdictions.

So, how will the combined company look?

Combined Portfolio (MMX/TFPM) (Company Presentation)

As noted, the combined will have approximately 30 producing assets, nearly 230 total assets (closer to its other intermediate peers), and a very diversified portfolio with the bulk of production coming from Tier-1 jurisdictions (Canada, Australia, and several exceptional assets as contributors, including Hope Bay (assuming a restart), Beta Hunt, Northparkes, RBPlat, Cerro Lindo, Buritica, Young-Davidson, Fosterville, and La Colorada). So, while Triple Flag previously had the production profile to match its closest peers, it has received a nice depth addition, and it will see improved diversification with it no longer having one asset being a massive contributor (which can be a risk), similar to Cobre Panama and Salobo for the majors. Let’s dig into the valuation:

Valuation

After adjusting for shares to be issued in the Maverix deal (assuming the transaction closes), Triple Flag would trade at a market cap of approximately ~$2.81 billion at a share price of US$14.00. This places Triple Flag’s market cap ahead of peers like Sandstorm Gold (SAND) at ~$1.58 billion and Osisko Gold Royalties (OR) at ~$2.22 billion. In the case of Sandstorm Gold, the significant premium can be partially explained by Sandstorm’s ~$340 million in net debt minus investments in mining companies, or ~$190 million, once Sandstorm’s Antamina agreement closes with Horizon Copper. Hence, while TFPM might appear to trade at a significantly higher valuation than SAND, their valuations have less divergence from an enterprise value standpoint, with TFPM having a net cash position pre-MMX deal and a relatively small cash contribution.

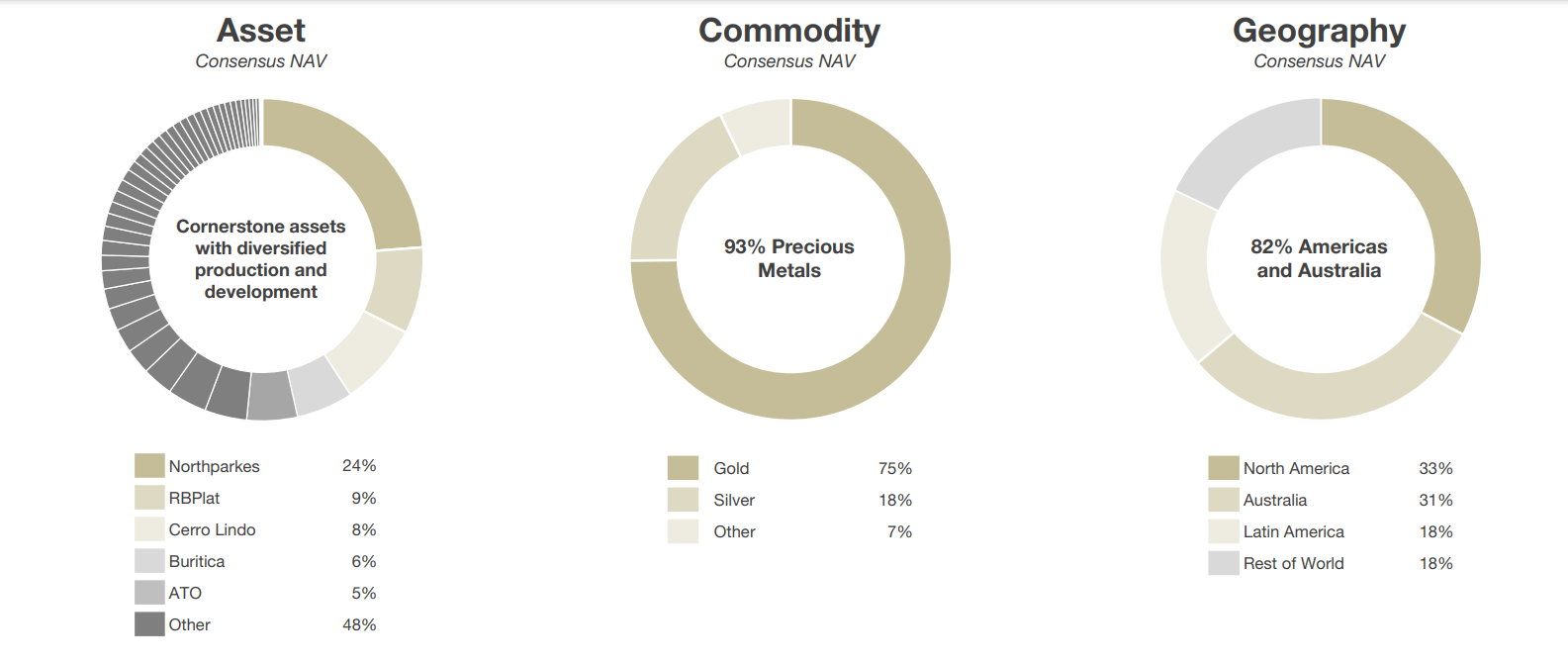

Triple Flag – Consensus NAV (Assets) & Commodity/Geography Split (Company Presentation)

Comparing the stocks from a size standpoint, Triple Flag will leap ahead of Osisko and Sandstorm in terms of attributable GEOs earned in 2023 (assuming the Maverix deal closes), and depending on how its development portfolio progresses, the three companies should remain neck and neck from a GEO standpoint in 2026 with Osisko and Sandstorm forecasting ~140,000 GEOs (2025/2026), and Triple Flag forecasting a 5-year average of 140,000+ GEOs (2023-2027). So, with similar production profiles, all companies having at least 20 producing assets (and over 200 total assets), and no company having more than 25% of estimated NAV tied to one asset, I would expect them to trade at similar P/NAV multiples.

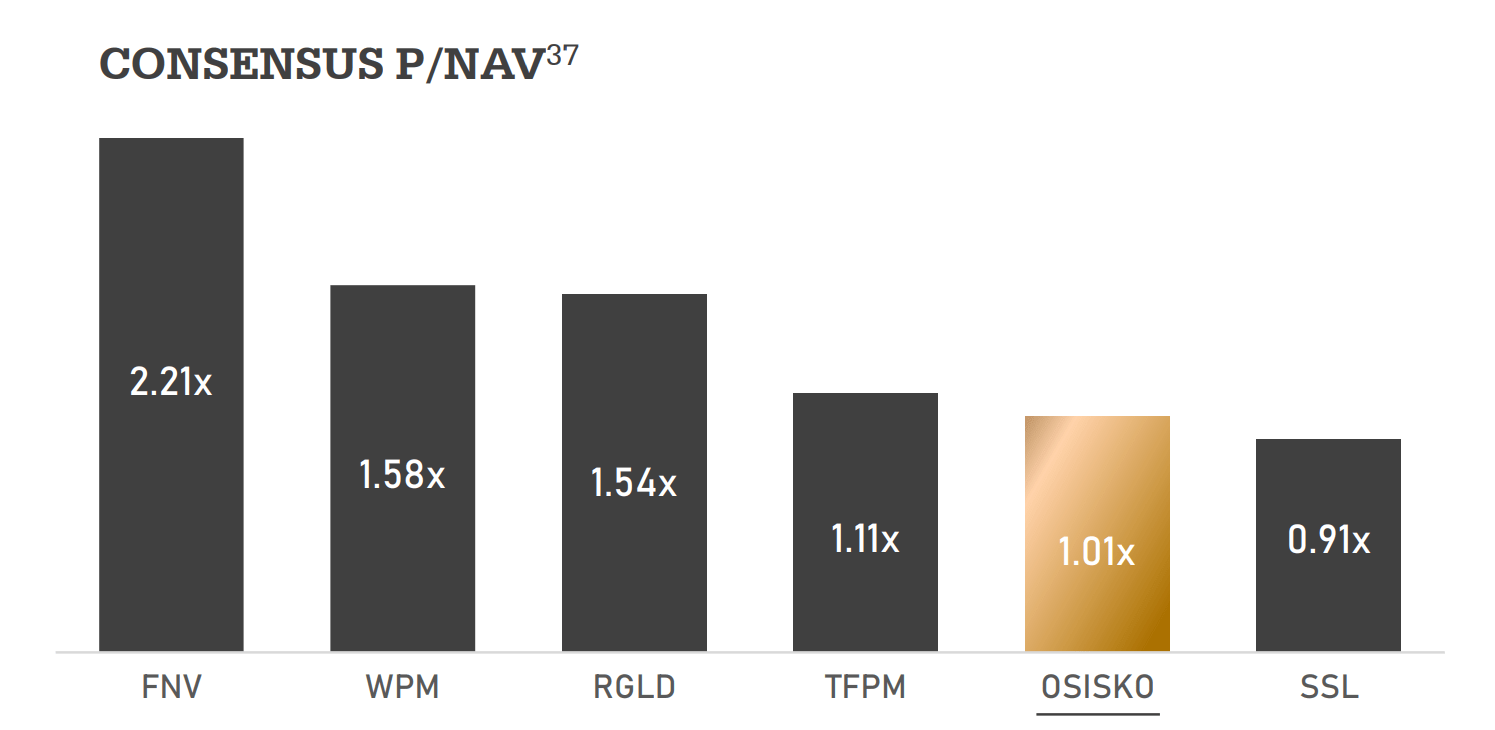

However, due to Sandstorm’s underperformance over the past few months and Osisko having a depressed multiple before its Osisko Development (ODV) de-consolidation and only beginning to play catch-up to reflect this, Triple Flag trades at the highest P/NAV multiple within the intermediate peer group of these three companies. One could argue that Triple Flag has its positive attributes vs. its peers. Still, a case can be made for Sandstorm and Osisko also having key positive attributes vs. Triple Flag, such as industry-leading diversification for Sandstorm and higher growth and an industry-leading jurisdictional profile for Osisko (~90% of GEOs from Tier-1 jurisdictions). So, while TFPM is cheap relative to the majors, I continue to see SAND and OR being more attractively valued here.

Consensus P/NAV Royalty/Streaming Companies (Osisko Gold Royalties Presentation)

Based on what I believe to be a fair P/NAV multiple of 1.50 to reflect Triple Flag’s improved diversification and depth in its portfolio following the Maverix deal, I see a fair value for the stock of ~$3.42 billion. This translates to a fair value of US$17.10 per share based on ~200 million outstanding shares, or a 22% upside from current levels. While this is a decent upside, and I would expect the company to continue to increase its NAV through new transactions given the favorable environment and ample liquidity, I generally prefer at least a 33% discount to fair value to justify starting new positions in mid-cap names. In the case of TFPM, this would require a dip below $11.50 per share.

TFPM 6-Month Chart (TC2000.com)

If we look at the technical picture above, TFPM has upper support at US$11.80 and an overbought zone at US$15.50, and the stock currently trades in the upper portion of this support/resistance range. This doesn’t mean that the stock can’t go higher. Still, with a reward/risk ratio of 0.70 to 1.0, which measures the potential upside to resistance vs. potential downside to support, I don’t see this as a low-risk buying opportunity. So, if the stock were to continue its outperformance and rally above US$15.80 before March (2% above the US$15.50 area overbought zone), I would view this as an opportunity to book some profits.

Summary

Triple Flag looks like it will close on an excellent acquisition announced last year, and I see this as a win-win for both companies. Maverix’s portfolio should be re-rated slightly higher in a larger portfolio, and Triple Flag will see significant depth additions to its portfolio and less concentration, with Northparkes, RBPlat, and Cerro Lindo previously being quite chunky contributions. In addition, trading liquidity should improve considerably, which was one thing that held back Nomad as well (Orion stake). Given this upgrade to the investment thesis, I continue to see Triple Flag as a solid buy-the-dip candidate. That said, I remain focused elsewhere currently and would need a larger correction to get interested in starting a position in TFPM.

Be the first to comment