RL Photography

Written by Sam Kovacs

Introduction

Investing can be made as complex as you want it to be.

Some “experts” like to make it seem very complicated, as they believe it will make people think they know what they’re talking about.

For instance, I could say that our dividend investing strategy is:

A valuation based approach which drives profits through exploiting time horizon arbitrage and mean reversion theory within a well defined investment world of companies with durable competitive advantages and favorable governance in regard to shareholders.

Of course, what I really mean is:

We focus on high quality dividend stocks. We buy low, sell high, and are happy to get paid to wait.

And you’ll never really see us using the former version, because we’re not in the business of confusing people. We’re in the business of taking the complex, and articulating it in easy to understand concepts.

We’ve talked about this idea of “buy low, sell high, get paid to wait” many times.

Let me expand on the “get paid to wait” bit.

Why are we happy to get paid to wait? Wouldn’t we rather buy the stocks which go from low to high in a couple weeks and repeat?

Well, maybe in an ideal world. But the world isn’t ideal. Sometimes opportunities you notice take time to be noticed and fully appreciated by others.

In the complicated version of our strategy above, I mention “time horizon arbitrage”. What this entails is that the market is pricing an asset in a certain way (cheap or expensive) because most of the market participants have a certain time horizon. If you have a different time horizon, you can profit from this inefficiency.

In the US, the vast majority of assets are managed by institutional investors. Professionals are running the show.

What is particular about professionals? They are investing in stocks on behalf of the true owners of the assets. They will be measured based on their performance. Not their 5, 10 or 20 year performance, but their quarterly and annual performance.

Did well? More assets for you. More assets, more fees. More fees, bigger bonus. Bigger bonus, bigger swimming pool than your neighbor.

Did badly? Less assets for you. Less assets, less fees. Less fees, no bonus. No bonus, no new swimming pool.

So the incentive is naturally skewed towards maximizing your returns over the next quarter or the next year.

Those are the two speeds the market operates on: one quarter & one year.

But no matter how old and wrinkled you are, I’m sure your time horizon goes beyond that.

If you are investing in dividend stocks to cover your retirement expenses, then your time horizon potentially goes beyond your death. You have no need for performance this quarter or this year, so you can easily give it up for stronger long term performance.

So when the markets make short term assumptions which alter the price of assets without changing much beyond one quarter or one year, opportunities arise to buy low. The reverse is also true, opportunities arise to sell high.

At any point in time, something in the market is undervalued and something in the market is overvalued. This has been true in every environment.

As the famous saying goes: “it’s not a stock market, it’s a market of stocks”.

In this article, I’ll highlight 5 contrarian high quality dividend growth stocks which are attractively priced because of short term market beliefs and assumptions.

The short version

Market participants are projecting that higher rates will hurt real estate companies: this has driven American Tower Corp. (AMT) down.

They believe that higher rates will lead to a recession. This recession will hurt discretionary spending such as on home improvement, driving down Lowe’s (LOW).

It will also make consumers fragile, which is holding back bank stocks such as Regions Financial (RF).

They believe that the strength of the dollar will persist forever, keeping Canadian stocks like Suncor (SU) down.

Finally, high inflation and weaker consumers will be a burden on transportation stocks such as United Parcel Service (UPS).

American Tower

American Tower Corporation has a wonderful business.

They buy land and cell towers, which they then rent out to multiple tenants. Returns from having one tenant are quite low, but then scale very quickly when the company has multiple tenants.

With the growth of 4G and 5G connectivity throughout the world, AMT has growth opportunities both domestically, as well as in Europe, Asia, and Africa where it has operations.

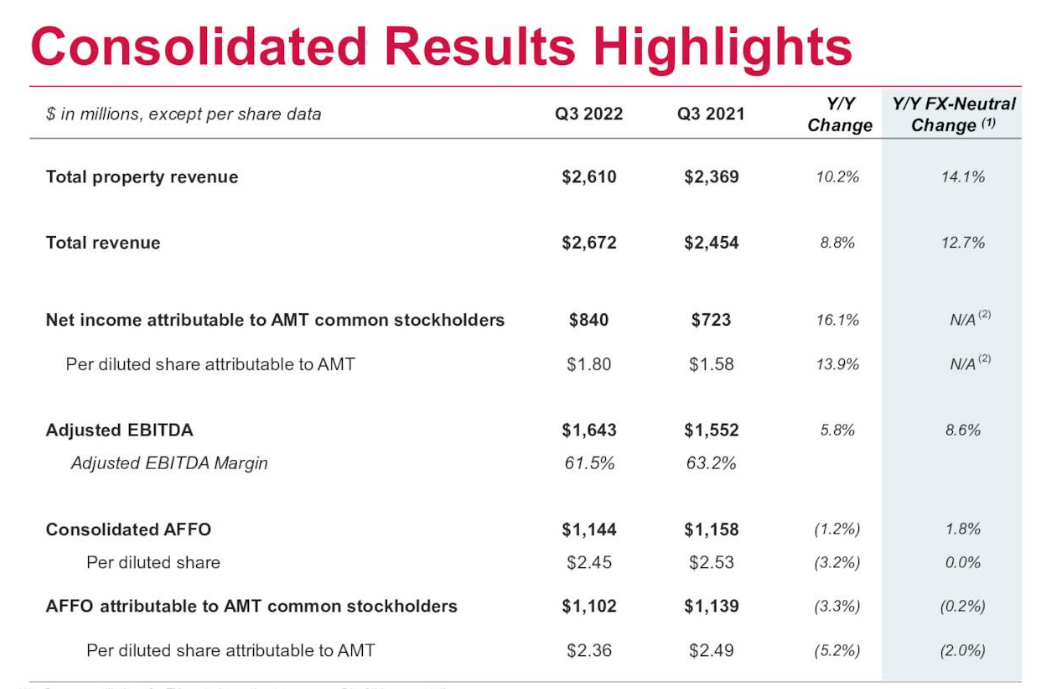

As you can see in the Q3 results, everything is going well, especially at the top line.

AMT Earnings Presentation

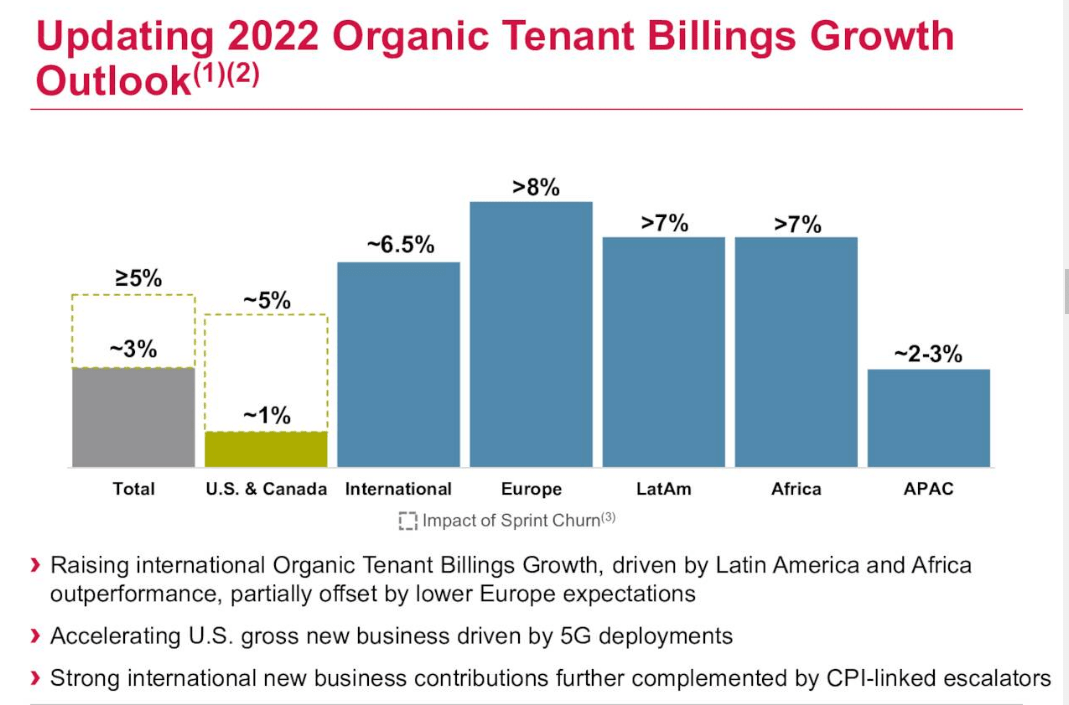

If you exclude the fact that they lost Sprint as a customer, which significantly impaired growth in the US, the company has been growing in every single market.

AMT Earnings Presentation

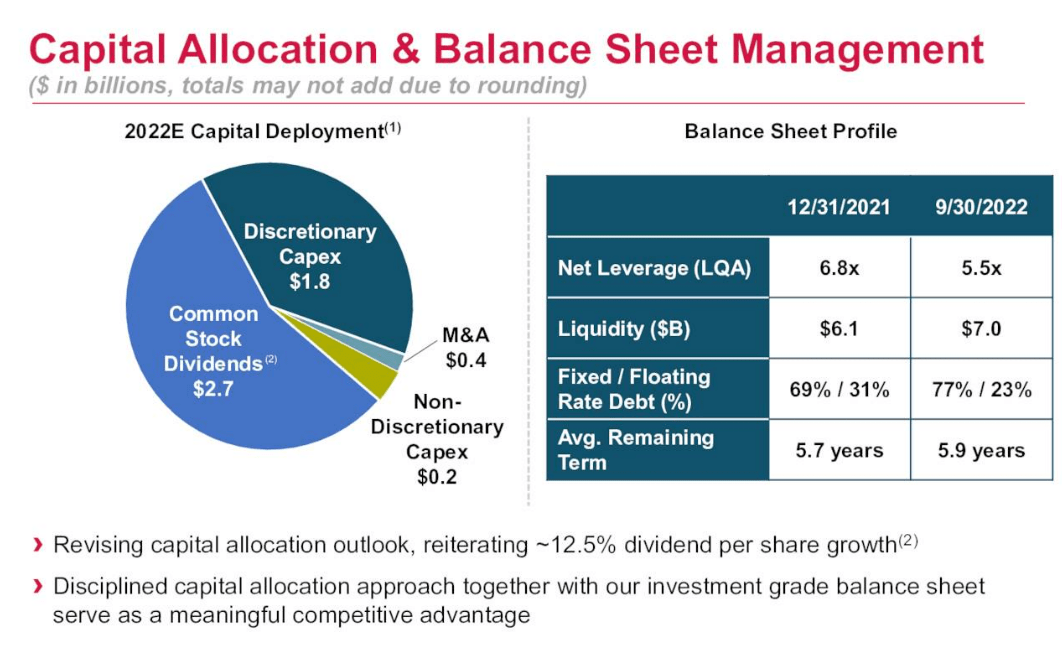

The company has improved its balance sheet significantly, reducing leverage, locking in more fixed rate date at longer maturities, and has increased liquidity.

AMT Earnings presentation

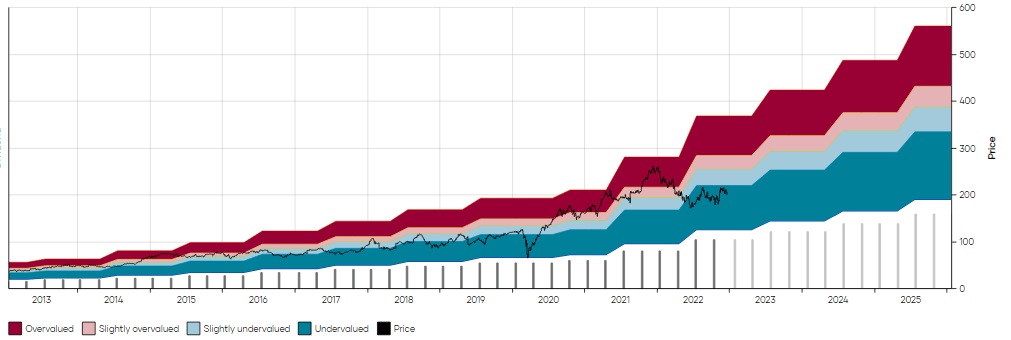

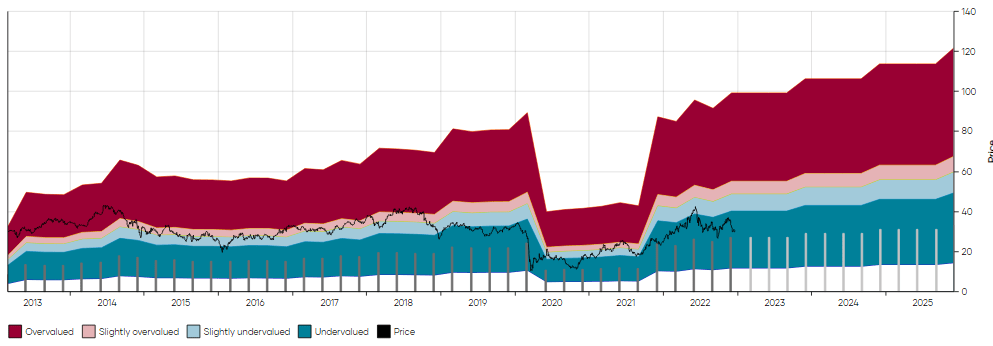

Yet shares are down.

Why?

Because the market fears that higher interest rates, mean lower spreads for real estate companies.

The fact that over 3 quarters of AMT’s debt is fixed, that the FX hits it takes are mostly from currency translation (and not conversions!) seem to be ignored, as it has been grouped in with other REITs.

Yet just this quarter, the dividend was once again increased by 6.1%.

AMT increases its dividend every quarter, as you can see on the MAD Chart below (click here for more on MAD Charts).

AMT MAD Chart (Dividend Freedom Tribe)

While the dividend has continued to grow as usual, as business has continued as usual, the stock price has become distanced from reality, presenting an opportunity to patient investors like us.

You can now get the stock at $205, which provides a yield of 2.9%.

If you invest $10,000 dollars in AMT today, and reinvest the dividends every year, then 10 years from now, assuming they can continue with their 12% dividend growth, you’d expect annual dividend income of $1,200, which equates a 12% yield on your original investment.

AMT Income simulation (Dividend Freedom Tribe)

This is particularly attractive, and means that while the market hates on AMT, we just need them to keep delivering as they have been.

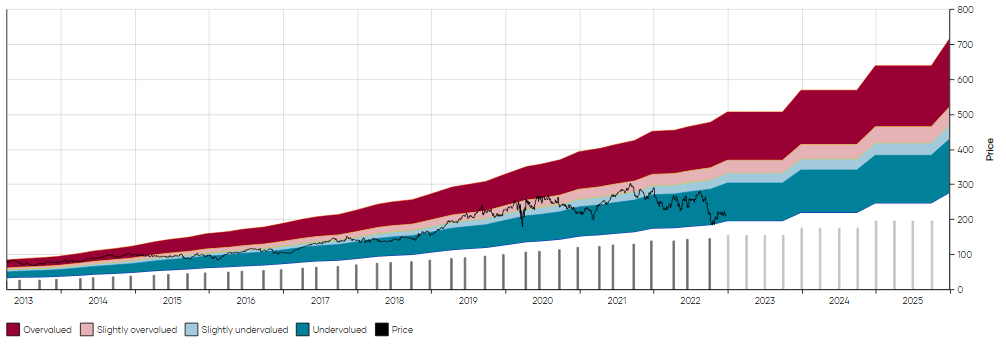

When the market changes its mind and reverts to its historically fair range of valuations, we can expect AMT to increase to $300-$310. This provides 50%+ upside from the current prices.

The market extrapolated rate increases to increased costs for REITs and punished AMT wrongly.

This will get corrected in time. In the meantime, get paid to wait.

Lowe’s

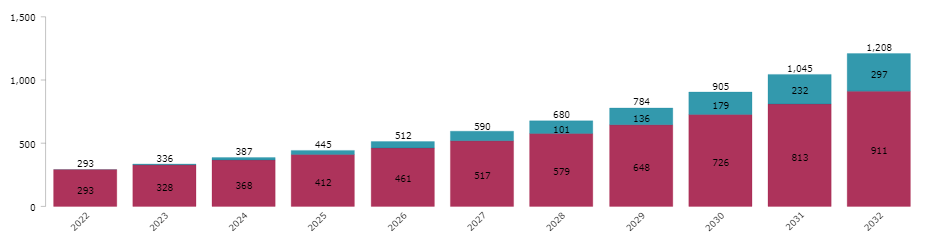

This is how the market assumption goes: Increasing rates means less people will get mortgages to buy houses, which means housing starts will go down, which means spending on home improvement spending goes down.

As Lowe’s pointed out on its investor day, retail home improvement rates can do well when home building slows and shows this telling example from the 1990s.

LOW Earnings Presentation

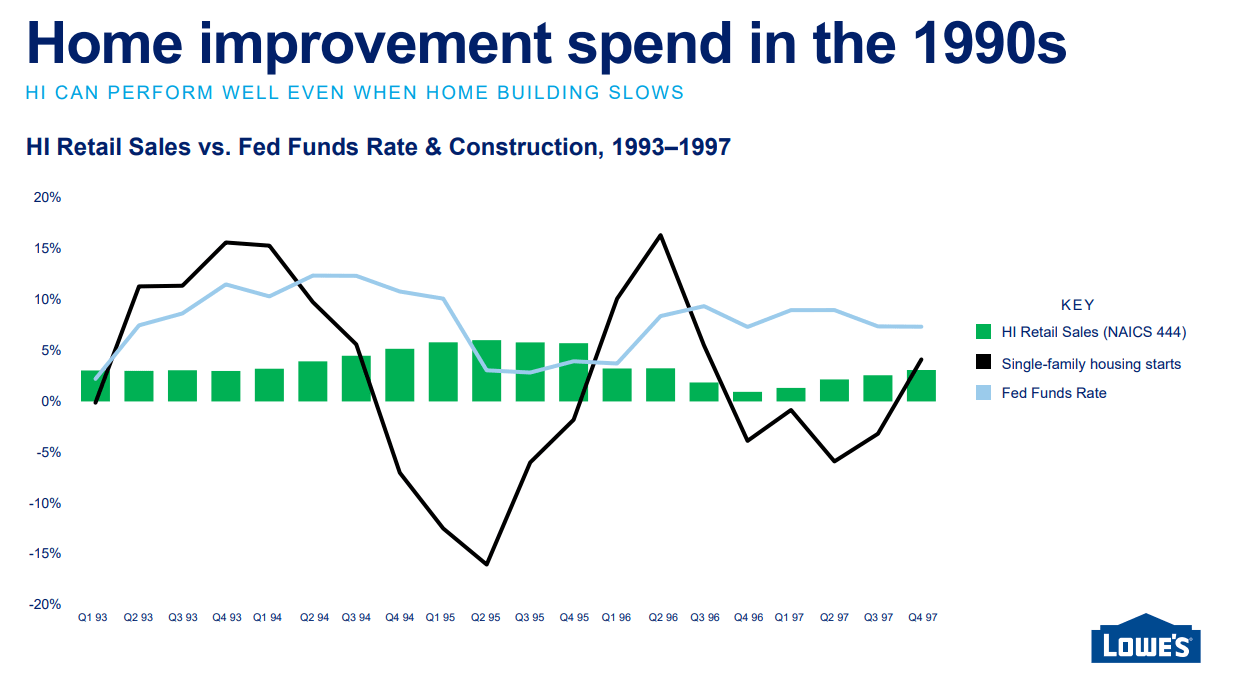

This is because the demand for home improvement is driven by different factors than demand driven by home building.

As you can see in the slide below, new home building depends on rates, and affordability. Neither are too appealing right now.

LOW Earnings Presentation

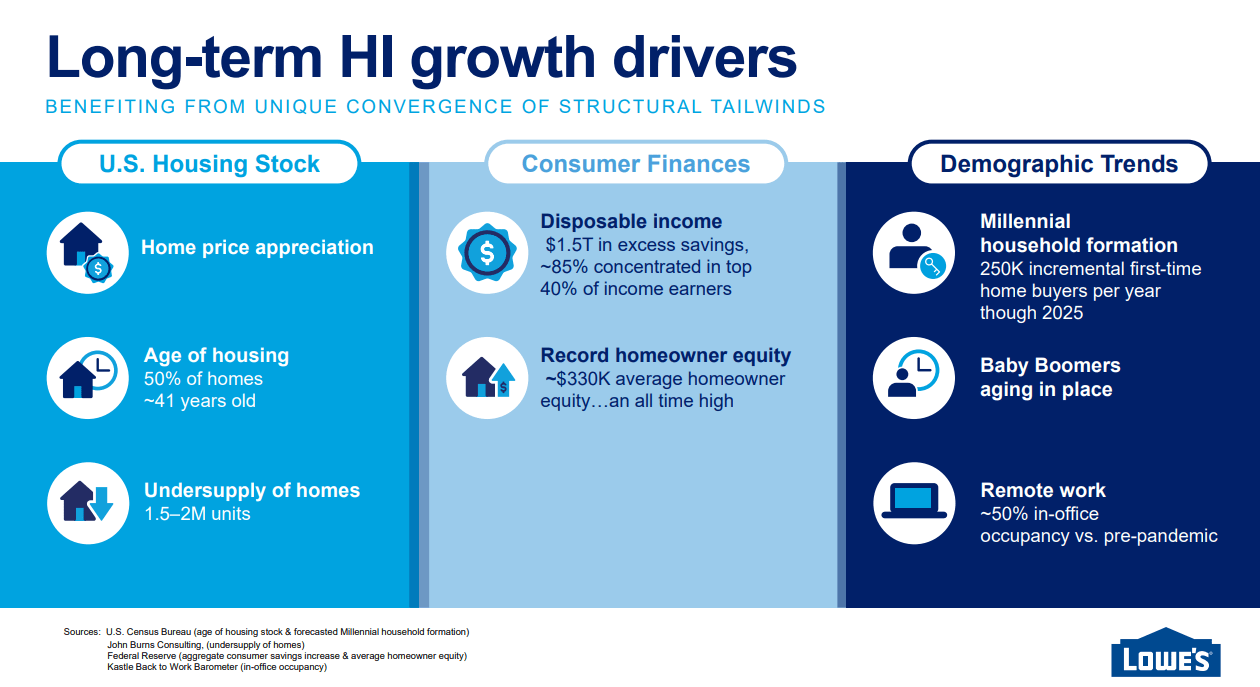

On the other hand, home improvement depends on appreciation of home price, age of housing stock, and disposable personal income.

LOW highlights that prices in the US have appreciated a lot in the past few years, the top 40% of income earners still have over $1Tn in excess savings, homeowner equity is at a record high, while houses continue to age in the US, with the average home being 41 years old.

LOW Earnings Presentation

It is no surprise then, that LOW is beating expectations.

75% of its business comes from DIY/retail sales, whereas 25% is exposed to professional clients.

This works well in the current environment, because home improvement is primarily driven by consumers, whereas home building is driven by the pros.

LOW beat earnings and is yielding 2.09% more than its historical median yield of 1.6%.

LOW MAD Chart (Dividend Freedom Tribe)

This isn’t the highest yield, but when you consider that LOW has grown its dividend at a 20% CAGR over the past decade, and increased it 30% last year, you get an idea of the potential.

Given that the company is still only paying 35% of its FCF as a dividend, it still has plenty of room to grow.

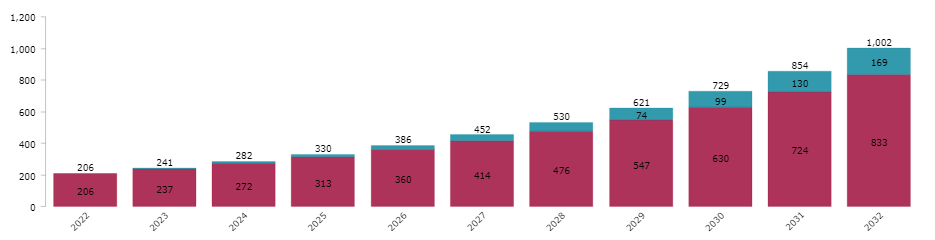

Let’s say LOW can continue growing at a 15% CAGR, which is conservative given the historical growth rates, then the income opportunity is still very attractive.

If you invest $10,0000 today in LOW, then 10 years from now, assuming the above rate of growth and annual dividend reinvestment, you could expect $1,002 in annual income, or 10% on your original investment.

LOW Income Simulation (Dividend Freedom Tribe)

This is very satisfactory and goes to show the income from a low yielding, but high growth stock, can compound to very attractive numbers.

Fair value for LOW is $260-$280, which offers 30% to 40% upside from the current prices.

Regions Financial

Financials were meant to be favored in the current period, as the increase in Feds fund rate should lead to better spreads on deposits for banks.

This has happened, and banks all over are reporting good results.

Regions Financial is one which is doing very well, yet the market is not recognizing this.

The market fear here is that a recession means that people will not be able to make mortgage payments, or auto loan payments, à la 2008.

But this isn’t 2008.

Who is at risk in the upcoming recession?

Not the blue collar workers, but the white collar workers.

Blue collar workers are usually considered the more fragile demographic, but the demand for workers in these jobs is at record highs, with many positions still unfilled.

Blue collar workers outnumber white collar workers 4 to 1.

White collar workers are losing their jobs and will continue to do so. We’ve seen this among tech companies, but the current recession is one which will be targeted at cutting the fat amongst middle management in jobs which did well during the pandemic.

The white collar workers are usually the higher income earners. As a group they still have LOTS of excess savings, as we mentioned in the section on LOW.

Therefore, even as they go redundant, they should have some security net which sees them through the time period between jobs.

The result is that we won’t see the delinquencies that the market expects.

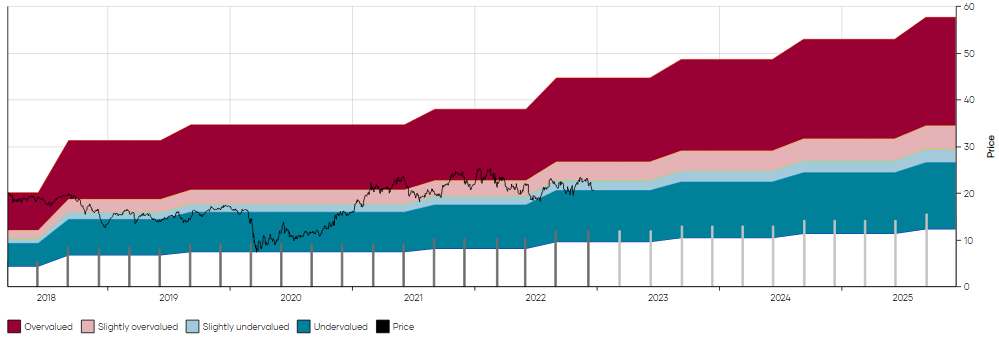

When it comes to RF, they had a record year both for top and bottom line.

RF Earnings Presentation

This allowed the company to increase their dividend by 17%, which is in line with the 5 year CAGR.

The bank still pays out only 35% of its earnings, which suggests it can continue to increase its dividend generously for the foreseeable future.

The bank currently yields 3.86%, which is somewhat above the 5 year median yield of 3.4%.

RF MAD Chart (Dividend Freedom Tribe)

Even at its median yield, I believe RF would be undervalued because of its superior shareholder friendliness.

Let’s say growth does taper over the next decade, and that RF can achieve 12% dividend growth instead.

Well the combination of a 3.8% yield and 12% growth is just explosive.

Once again, let’s simulate the income you’d receive each year for 10 years if you invest $10K today and reinvest dividends every year for the next decade.

RF Income Simulation (Dividend Freedom Tribe)

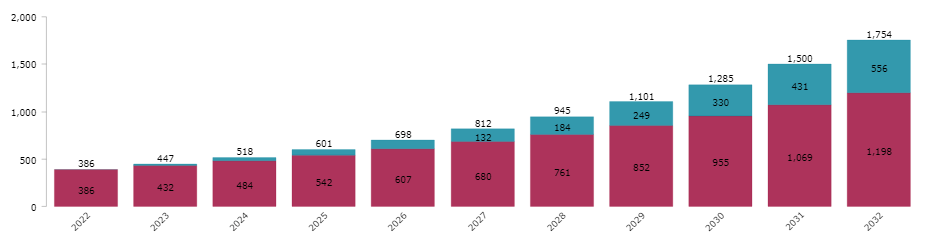

In year 10, you could explain income of $1,754, or an astounding 17.5% of your original investment.

Growth and yield together are always a fantastic combination, and they’re possible because RF is mispriced today.

Suncor

With higher rates in the US than in the EU, the UK, or Canada, it is natural that the demand for US dollars will increase, thus increasing the value of the dollar.

But this increase in value is temporary.

Yet it has been enough for investors to shun non-US based operations at the very time they should be spending their expensive dollars on cheap foreign currencies.

You can do this by investing in Canadian stocks which are listed on the NYSE, such as Suncor, one of Canada’s finest energy companies.

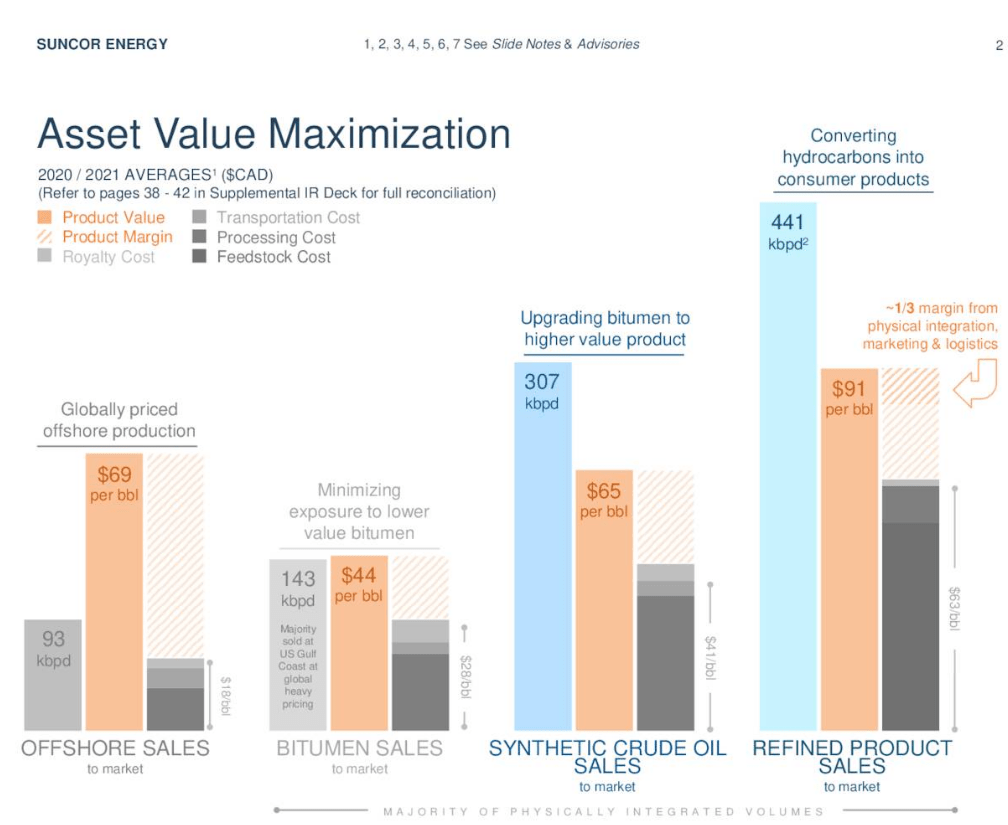

Suncor is vertically integrated which allows it to add a lot of value from the extraction of oil to the end customer product, as you can see in the slide below.

SU Earnings Presentation

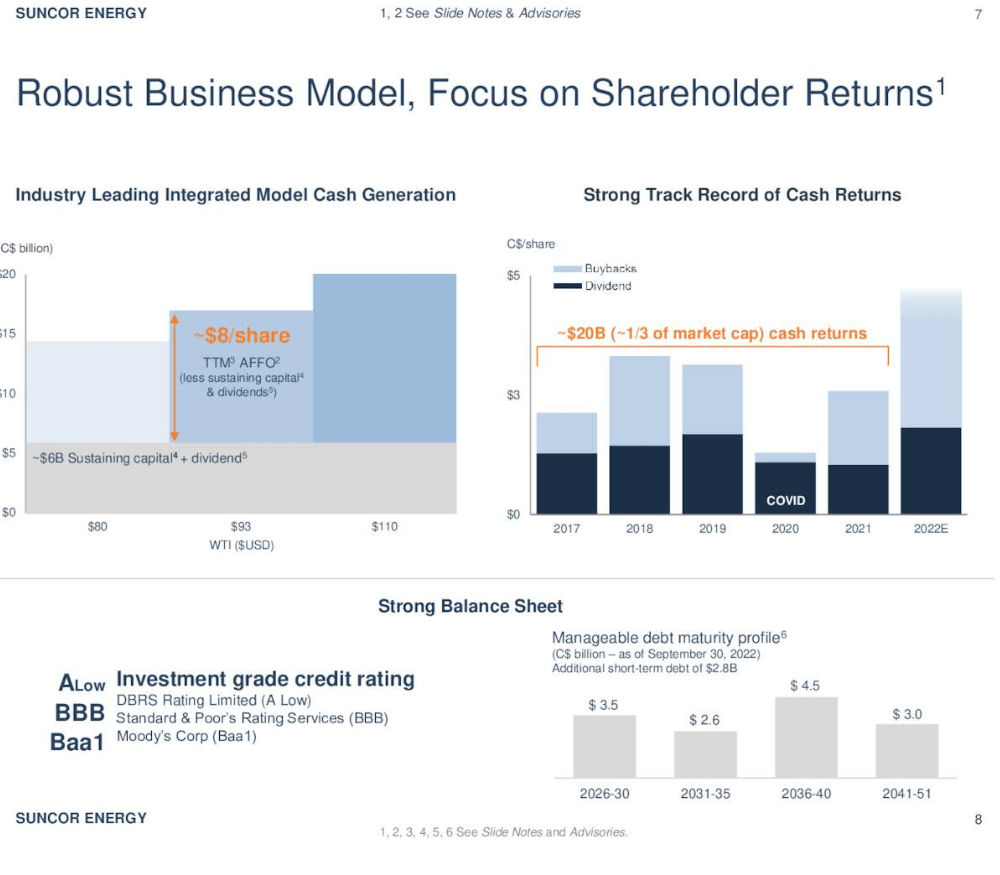

The company generates so much cash in the current environment, that it has an extra $8 per share of cash flow after the dividend and capex have been taken care of.

SU Earnings Presentation

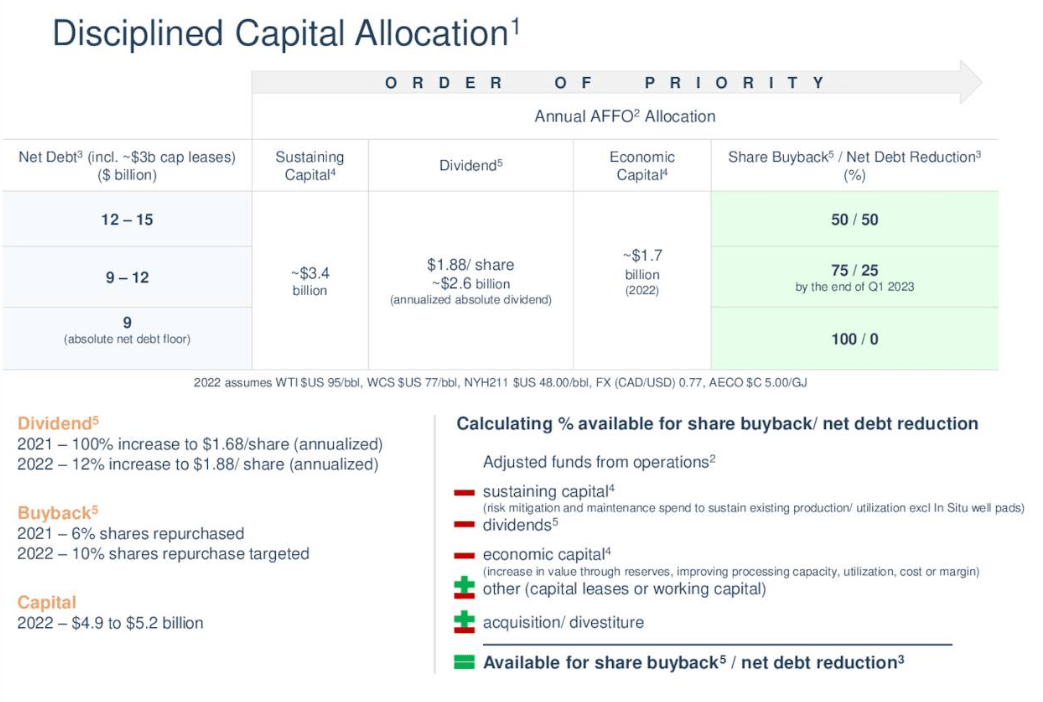

It goes without saying that this is a LOT of cash, which is getting returned to investors in the form of buybacks, and is being reinvested in the balance sheet in the form of net debt reduction.

SU Earnings Presentation

This year, SU has repurchased 10% of its shares, and increased its dividend by 12%.

It deserves to have increased in a similar fashion to US majors Exxon (XOM) and Chevron (CVX).

But it hasn’t, mostly because of the FX situation. A pity for the stock price, but a blessing for the dividend investor.

SU has a 10 year median yield of 3%, but it currently yields 5.1%.

SU MAD Chart (Dividend Freedom Tribe)

Let’s assume SU continues to grow its dividend at a 10% CAGR.

Not a crazy assumption given that it has grown at 11% per annum over the past decade, and given that management is reinvesting so much into debt reduction and share buybacks, that even more cash will be left over for dividends.

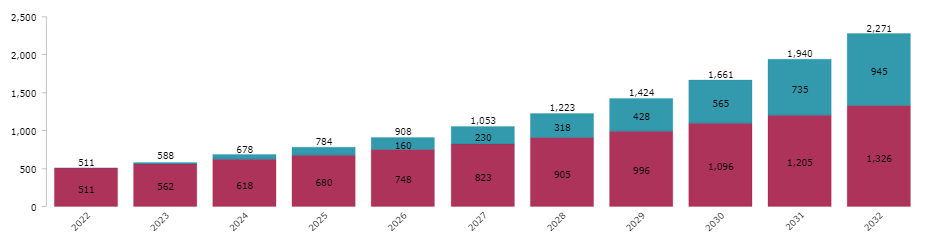

What does it look like if we invest $10K and reinvest dividends every year for 10 years?

Well, year 10, you could expect to receive $2,271 of annual income.

SU Income Simulation (Dividend Freedom Tribe)

That is 22.7% of your original investment, which is phenomenal.

When you see the power of compounding printed on a screen, you understand why we’re happy to get paid to wait.

When the market realizes its mistake, SU should be a $50 stock, which provides 66% upside from the current price.

United Parcel Service

The last pick is UPS.

Of course, it is easy to see how the market would project that everything would go wrong for UPS.

Higher energy costs. Higher inflation. Less discretionary spending. Surely this is bad for UPS.

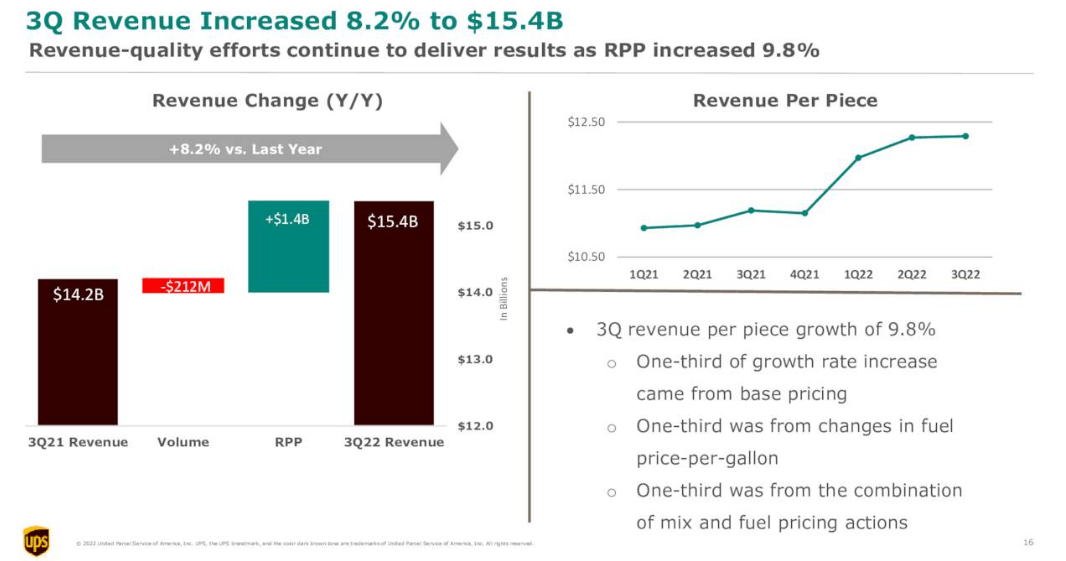

And yes, it is true, volume of parcels shipped declined by 1.4% year over year.

But revenue per piece is up 9.8% year over year, as UPS managed to pass on costs of inflation and then some.

UPS Earnings Presentation

So while volume is negatively impacting revenue, pricing is a big boost.

This shows that demand is still strong, and willing to pay the higher price.

If it wasn’t, both volume and pricing would have suffered.

The company continues to generate growth, good returns, and loads of cash, plenty to pay their growing dividend.

UPS Earnings Presentation

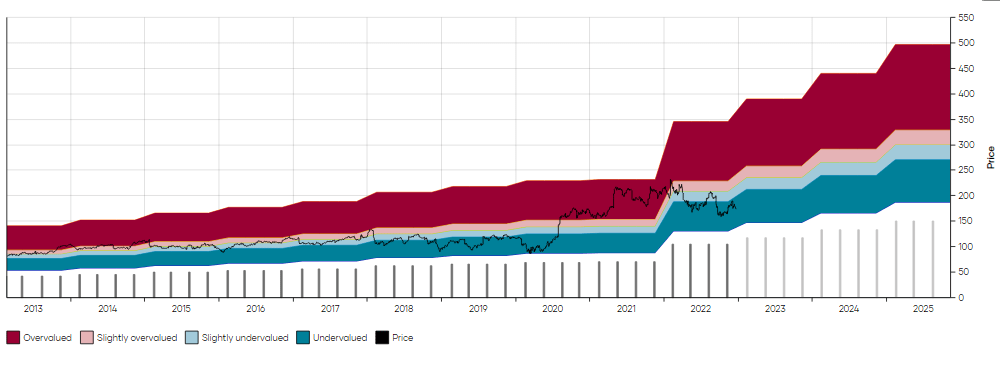

Yet the market doesn’t like UPS, and the share price has now made no progress since 2020, despite the company having grown a LOT in that time period.

The big bump in the dividend was only a reflection of the durable increase in business which started during the pandemic.

UPS MAD Chart (Dividend Freedom Tribe)

UPS now yields 3.45%, which is somewhat higher than the ten year median of 2.9%.

At this rate we don’t need aggressive double digit dividend growth.

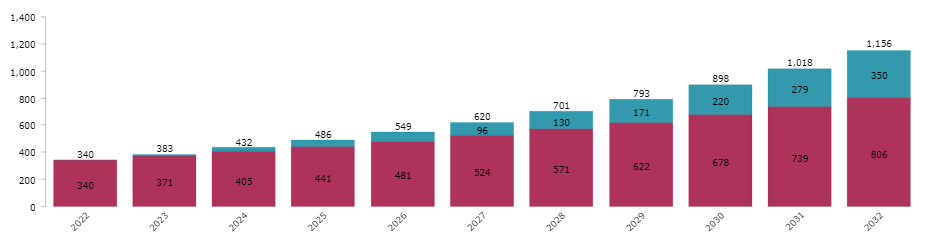

During the past 10 years, UPS has grown at an average rate of 10%. I believe they can maintain that growth rate throughout the next decade, but let’s project 9% for the sake of being conservative.

If you invest $10K today and reinvest dividends each year, then in 10 years, you’d expect to receive $1,156 in annual income.

UPS Income Simulation (Dividend Freedom Tribe)

This is once again a very attractive dividend profile, which makes us comfortable to wait until UPS returns to historical valuation levels.

When it does, I expect UPS to be a $230 to $250 stock, which provides 30% to 40% upside.

Conclusion

These stocks are top stocks to buy for 2023. Does that mean that the performance will be realized in 23? Not necessarily.

Sometimes things take years to play out. When they do, it happens quickly.

You might have to wait 3 months or 3 years for the price to get where you want it to be.

But if you’re building a healthy stream of growing dividend income which will see you through your retirement years, you can be patient with your performance.

This is our way at the Dividend Freedom Tribe: Buy low, sell high, get paid to wait.

Be the first to comment