William_Potter/iStock via Getty Images

Thankfully, 2022 is coming to an end as the both the broader stock market as well as the bond market have turned in negative performances. The bond market itself turned in its worst annual performance, and that is usually a safe haven for investors looking to plant money.

The only thing that made money this year was really CASH.

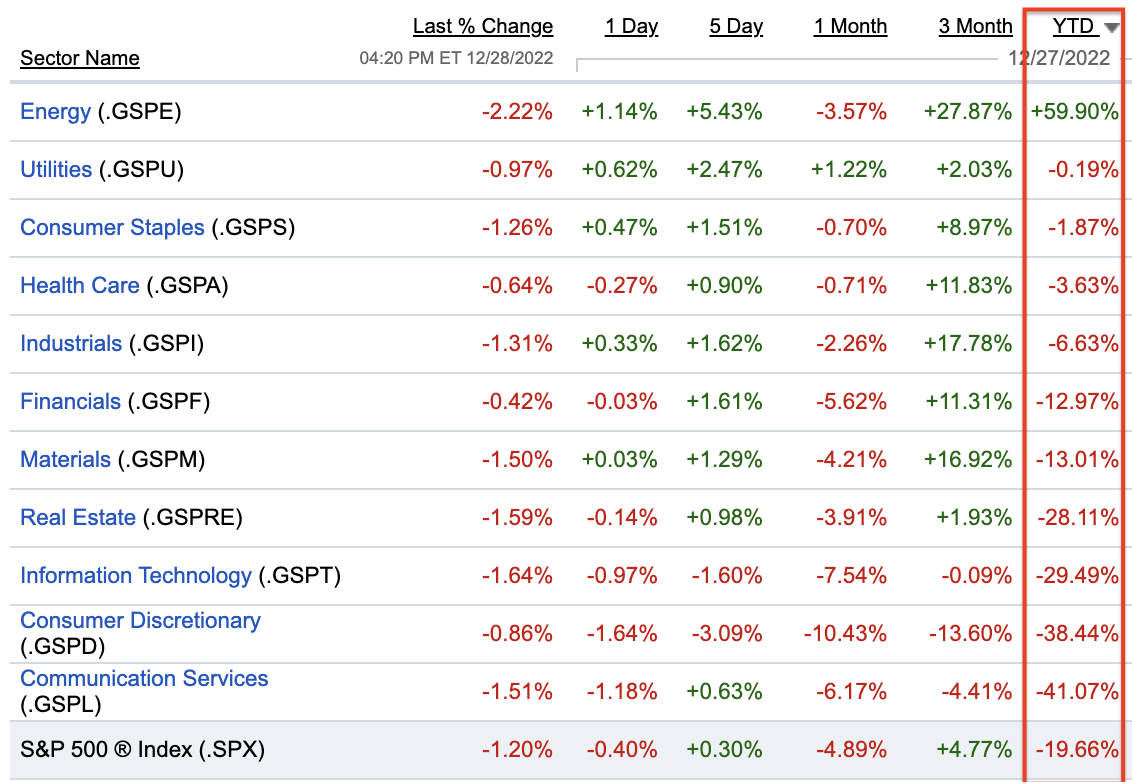

There are some sectors like energy and some healthcare stocks that did perform well in 2022, so not everything was bad I should say. But, from a sector wide performance, only energy ended in the green.

Here is a look at Year to Date performance by all 11 S&P sectors.

Fidelity

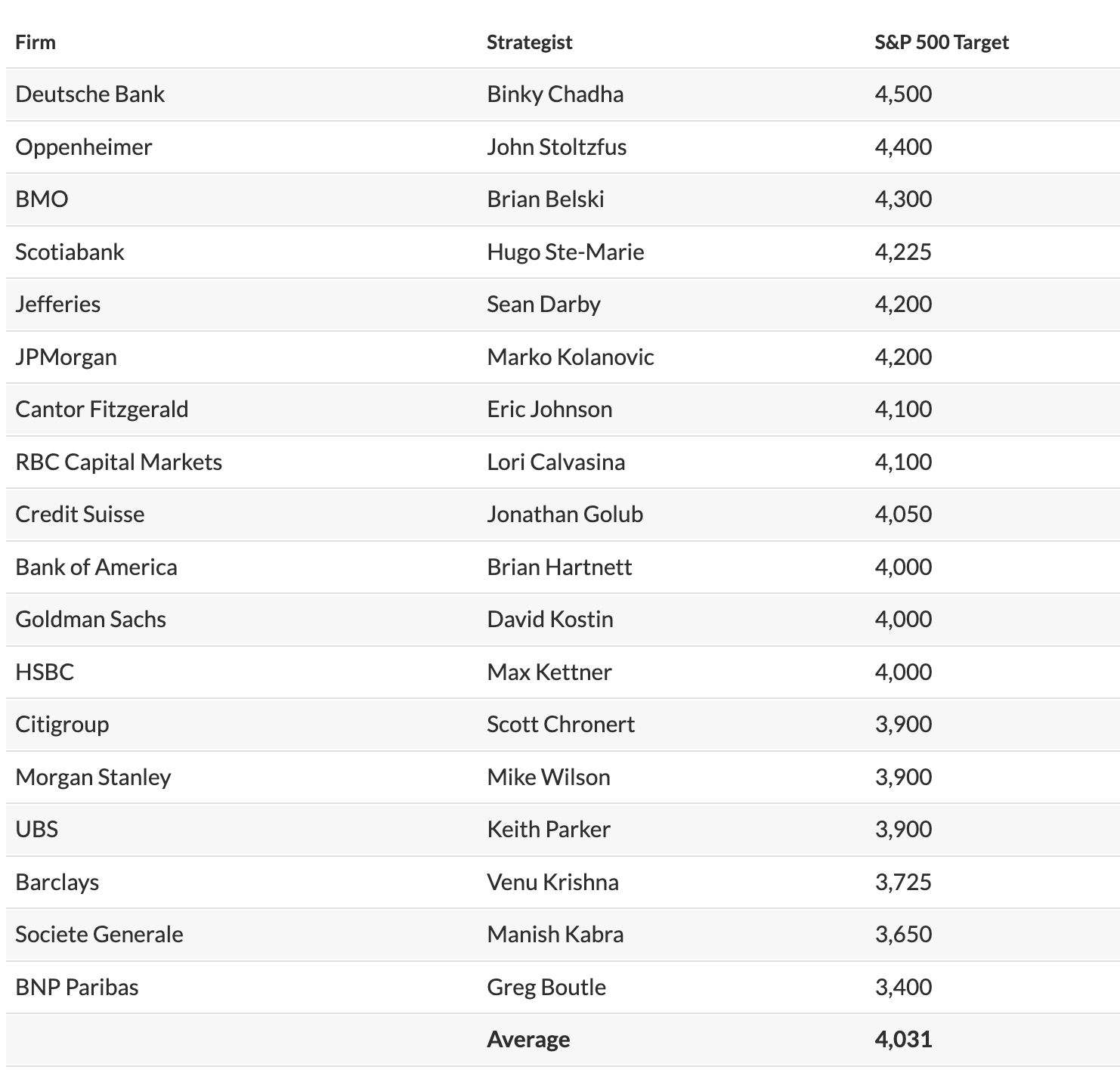

Analysts expect a lot of the same to start the new year, as inflation remains high and the Fed seems dead set on continuing to hike rates in order to bring inflation back down to their 2% target.

The back half of 2023 is where economists believe we could see some turnaround, which is evidenced in these S&P 500 price targets, which for the most part believe we will squeak out some gains when it is all set and done.

Marketwatch

The average price target comes in at $4,031, which is roughly 6.5% higher from where we closed as of this writing.

The goal for me when investing is to continue to add to high-quality positions at cheap valuations. Some of these names may continue to fall into 2023, but long-term I am confident in all of these companies to make for a great investment.

With that being said, let’s briefly look at all 10 of these Dividend Stocks for 2023.

Dividend Stock #1 – Johnson & Johnson (JNJ)

Johnson & Johnson is a Dividend King operating out of the health care sector. I recently published an article that was trending for a number of days on Seeking Alpha covering this very stock.

Johnson & Johnson: Time To Buy Before The Split

Late last year, the company announced they would be splitting up the business, the consumer health segment would spinoff into its own business, called Kenvue, and the Pharmaceutical and MedTech segments would remain together.

The consumer Health sector has many well known brands that are ALWAYS in demand regardless of the economic backdrop. Brands include:

-

Tylenol

-

Motrin

-

Zyrtec

-

Band Aid

-

Listerine

-

And MANY more

The spin off is expected to take place in Q4 2023. This spinoff will allow for a greater focus on the faster growing Pharmaceutical and Medical Devices segments, but how the dividend plays out will be interesting nonetheless.

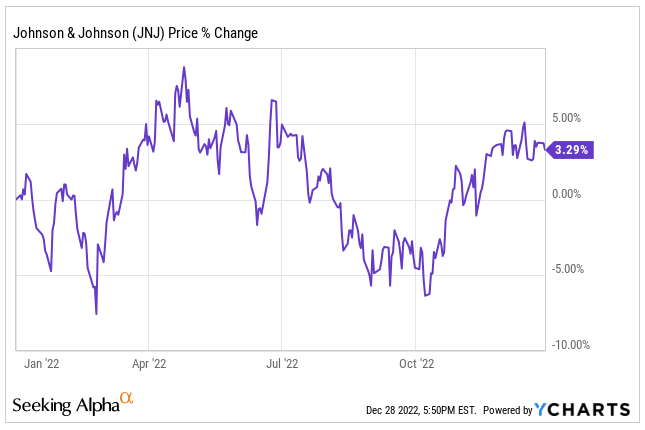

JNJ is going to be among the safest stocks on the list today, which is why I thought it was worthy of the number 1 position. Over the last 10 years, the total return between JNJ and the S&P 500 is almost identical, separated by less than 2 percentage points.

On the year, shares of JNJ are up 3.3%.

ycharts

As I mentioned at the start, JNJ is Dividend Royalty being a Dividend King for increasing their dividend for 50+ consecutive years. In fact, JNJ with their latest increase has now hiked their dividend for 60 consecutive years.

The company currently has a dividend yield of 2.6%.

In terms of valuation, JNJ rarely trades at a discount, but right now they do trade at a slight discount to their recent 5yr history. Shares of JNJ trade at a forward earnings multiple of 17x, compared to a 5yr avg of 17.8x.

Fast Graphs

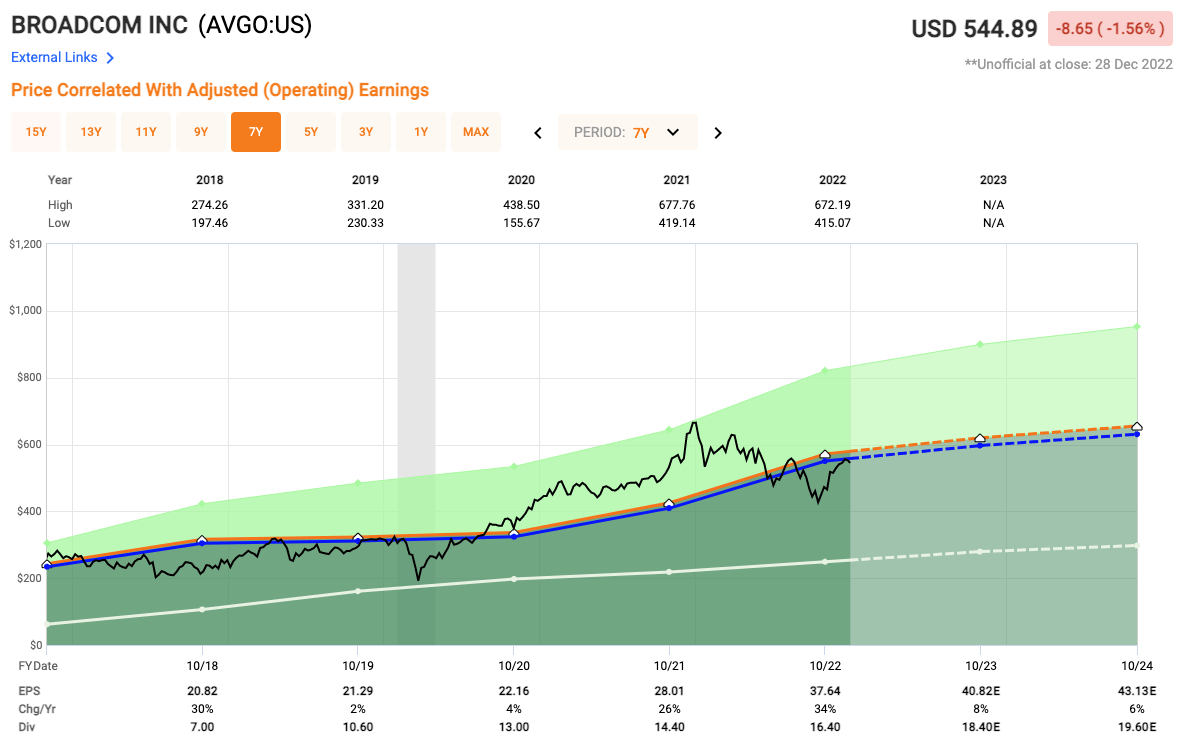

Dividend Stock #2 – Broadcom (AVGO)

This next stock could seem a little weird given the state of the semiconductor industry, but that is one of the very reasons I made it. The sector has been severely punished in 2022, but I believe companies within this space that have diversified product lines and strong free cash flow represent a great opportunity.

Broadcom has their hands in a lot of different sectors from broadband to data center, from cybersecurity to wireless connectivity and much more.

The company has also expanded into software and services in recent years, and is in the process of acquiring the cloud computing company VMware (VMW) for $61B. The deal is still in motion and has been approved by VMware shareholders, and it is expected to create plenty of synergies.

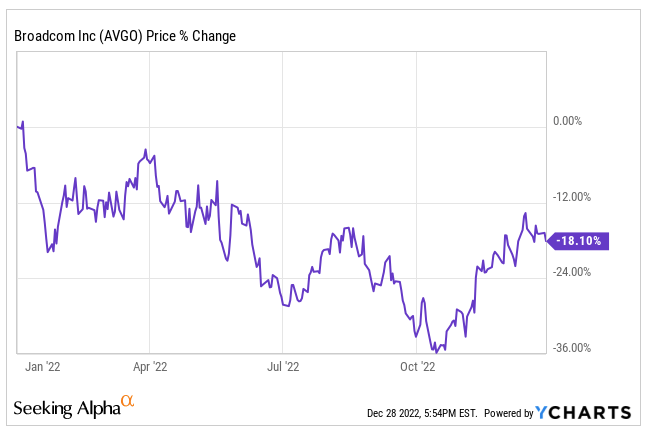

On the year, shares of Broadcom have fallen 18% making the valuation look very intriguing.

ycharts

In terms of the dividend, the company has a 3.2% dividend yield and a dividend that has increased for 11 consecutive years. The company has a 5yr DGR of 32%. The company recently hiked their dividend another 12%.

With Broadcom you get GROWTH potential, a solid Yield, and strong dividend growth. Shares of AVGO currently trade at just 13.7x next year’s earnings, and over the past 5 years they have traded closer to 14.6x.

Fast Graphs

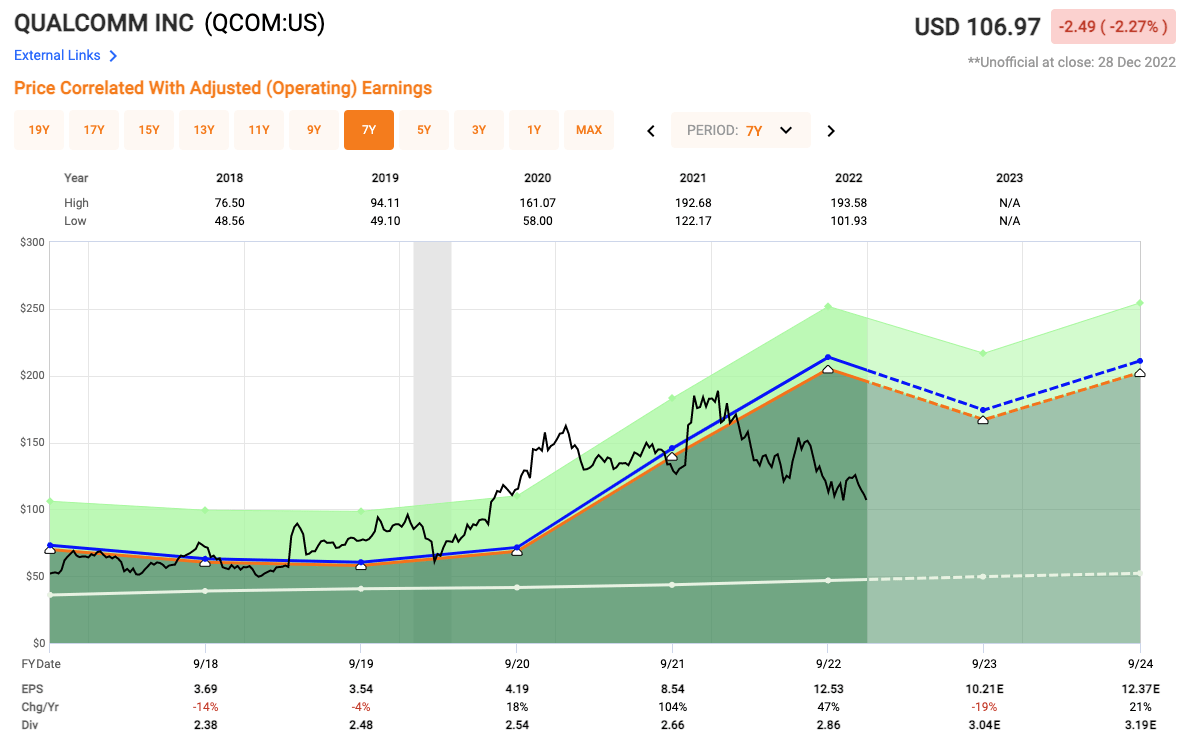

Dividend Stock #3 – Qualcomm (QCOM)

Let’s stick with the semiconductor space and highlight another well diversified company in Qualcomm. Qualcomm currently has a market cap of $123 billion.

They have products that reach a number of different areas including:

-

Mobile Phones

-

Computers

-

VR and AR

-

Automotive (which is a big growth driver for the company)

-

Wearables

-

Wireless

-

IoT

-

Smart Home

-

5G

The company has had many differences with Apple (AAPL) over the years, as the two companies have sued one another on multiple occasions, but even after all of that, Apple to this day is still using QCOM products which speaks to the power and advanced technology that QCOM products offer, especially with their popular snapdragon chip.

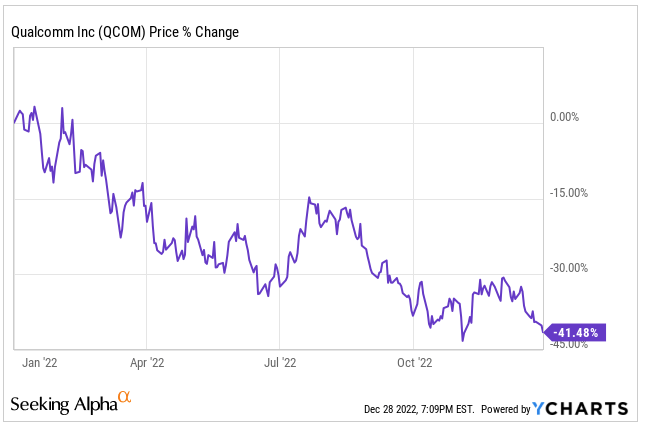

QCOM shares on the year, like many in the semiconductor space are down roughly 40%, representing a GREAT opportunity to get into this blue-chip company at a great valuation.

ycharts

Shares currently trade at just 10.5x next year’s earnings compared to their 5yr avg of 17x, that is 35% below their historical norms.

Fast Graphs

Shares of QCOM yield a dividend of 2.5% and the company has been increasing the dividend for 19 consecutive years with a 5yr DGR of 6%.

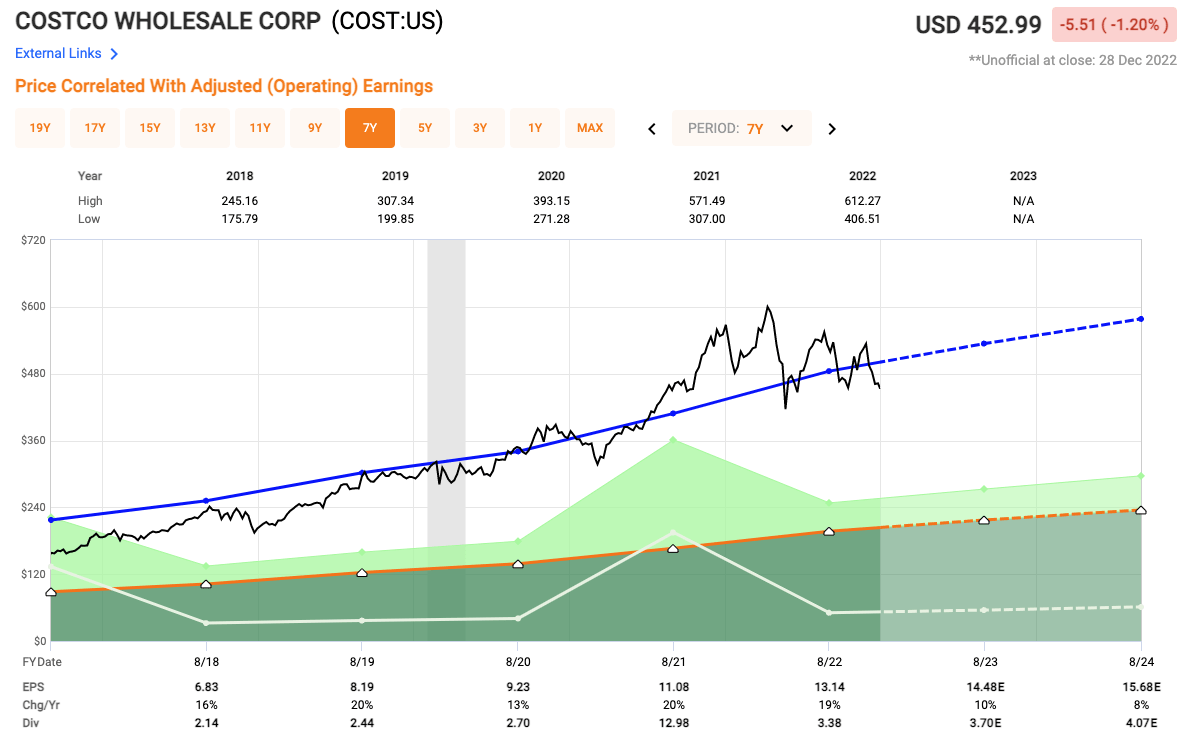

Dividend Stock #4 – Costco Wholesale (COST)

Costco has become more and more popular for consumers over the years, as many, including myself that have a Costco membership, have turned to Costco for their regular grocery needs. Costco’s market share in the grocery space continues to grow as they trial only Walmart (WMT) and Kroger (KR).

Costco currently has a market cap of $203 Billion.

The company is able to share their products at low prices, but they receive membership revenues from a loyal customer base with a high renewal percentage rate above 90%.

In addition, Costco maintains a fortress balance sheet with an A+ credit rating.

On the year, shares of COST are down 20%.

ycharts

Costco currently trades at a forward P/E multiple of 31.3x, which is below their 5yr avg of 37x. The stock should hold up ok if we do drop into a recession, as consumers will be looking to save money by shopping at a low cost leader like Costco for their everyday essentials.

Fast Graphs

As you can see from the fast graph chart above, the blue line represents the 5yr avg PE, and for much of the year, Costco had been trading well above it reaching a multiple of 48x in the spring, but valuations have since sunk with the pullback in the stock.

Costco has a low dividend yield of just 0.7% but they have increased the dividend at a 12.5% clip over the past 5 years and they have increased the dividend for 18 consecutive years, inching themselves closer to Dividend Aristocrat status.

Dividend Stock #5 – Altria Group (MO)

This next stock is a little more controversial for some people, as Altria Group is a tobacco company selling products such as cigarettes, cigars, marijuana products, smokeless and heated products as well.

The company understands the downtrend in cigarettes, which is why they have done a nice job over the years diversifying their portfolio of products. Their timing and valuation calculations have not been all that great, as they have had a few failed acquisitions or investments, but no one bats 1.000.

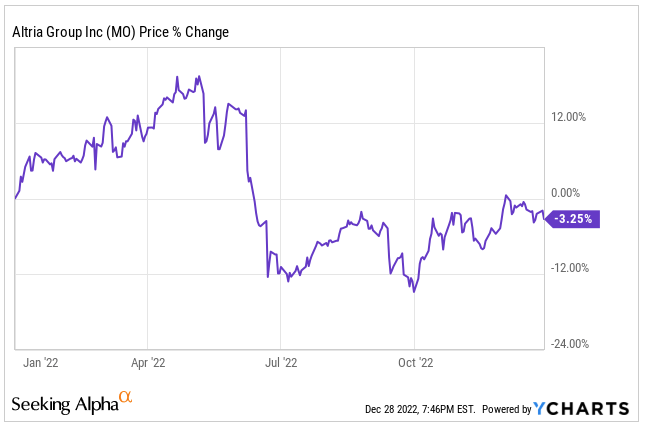

Altria currently has a market cap of $83 Billion and shares are down only 3% on the year.

ycharts

Altria has been a common stock found in many dividend portfolios over the years, especially those looking for higher yields. They have a large yield and in terms of total returns, they have performed well for investors over the decades.

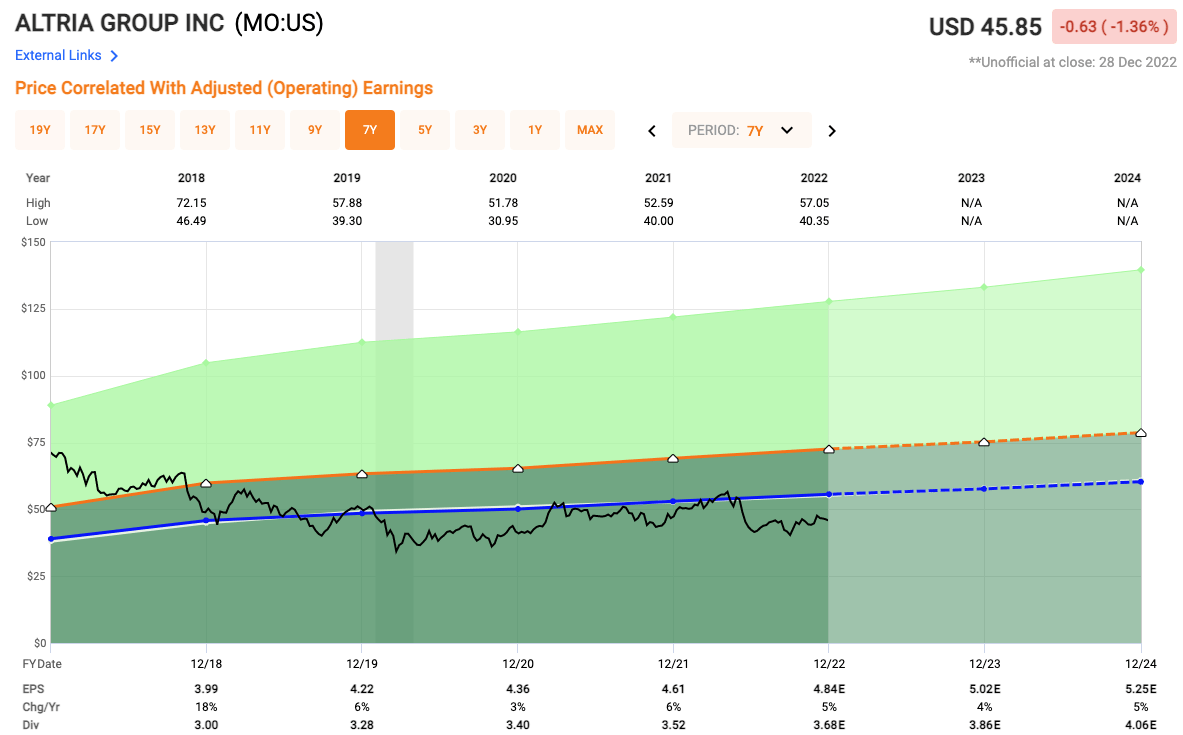

Given that, you can still get shares of Altria at a multiple of just 9x next year’s earnings. Over the past 5yrs, Altria shares have traded closer to 11.5x.

Fast Graphs

Buying shares today would also earn you a very high dividend yield of 8.1%.

Dividend Stock #6 – Bristol-Myers Squibb (BMY)

Bristol-Myers Squibb is a pharmaceutical company with a market cap of $161 Billion. The company has a great portfolio of products that are in high demand, plus they have a strong pipeline.

A few years back, BMY acquired Celgene for roughly $74 billion, which further expanded an already strong portfolio. The acquisition was not well received at first, but the diversification, innovation, and synergies it is adding today is beginning to pay dividends for the company, and investors are beginning to take notice.

Bristol-Myers happens to be the best performing stock on this list in 2022, as shares of BMY are up 15% on the year.

ycharts

Currently, shares of BMY have a dividend yield of 3.1%, and that dividend has grown at an average annual clip of 7% over the past 5 years. The company has increased the dividend for 14 consecutive years now.

Even with the share price growth we have seen in ’22, shares of BMY still trade at just 9x next year’s earnings and over the past 5 years, they have traded at an average of 12x, so plenty of growth left just to get back to average.

Fast Graphs

Dividend Stock #7 – Verizon Communications (VZ)

Verizon Communications is one of the largest companies within the telecommunications sector, battling it out with the likes of AT&T and the fast growing T-Mobile.

The telecommunications sector has seen fierce competition this year with all three major wireless carriers competing for respective customers.

Growth has slowed in the sector, but much of that was due to the explosion we saw in 2020. However, VZ executes much better than the likes of AT&T which has had numerous poor acquisitions that has led to mountains of debt.

5G rollout continues to be pricey for the telecom companies, which is one reason I like American Tower (AMT), which is a cell tower REIT that is in my Top 10 REITs for 2023 (look for this article next week).

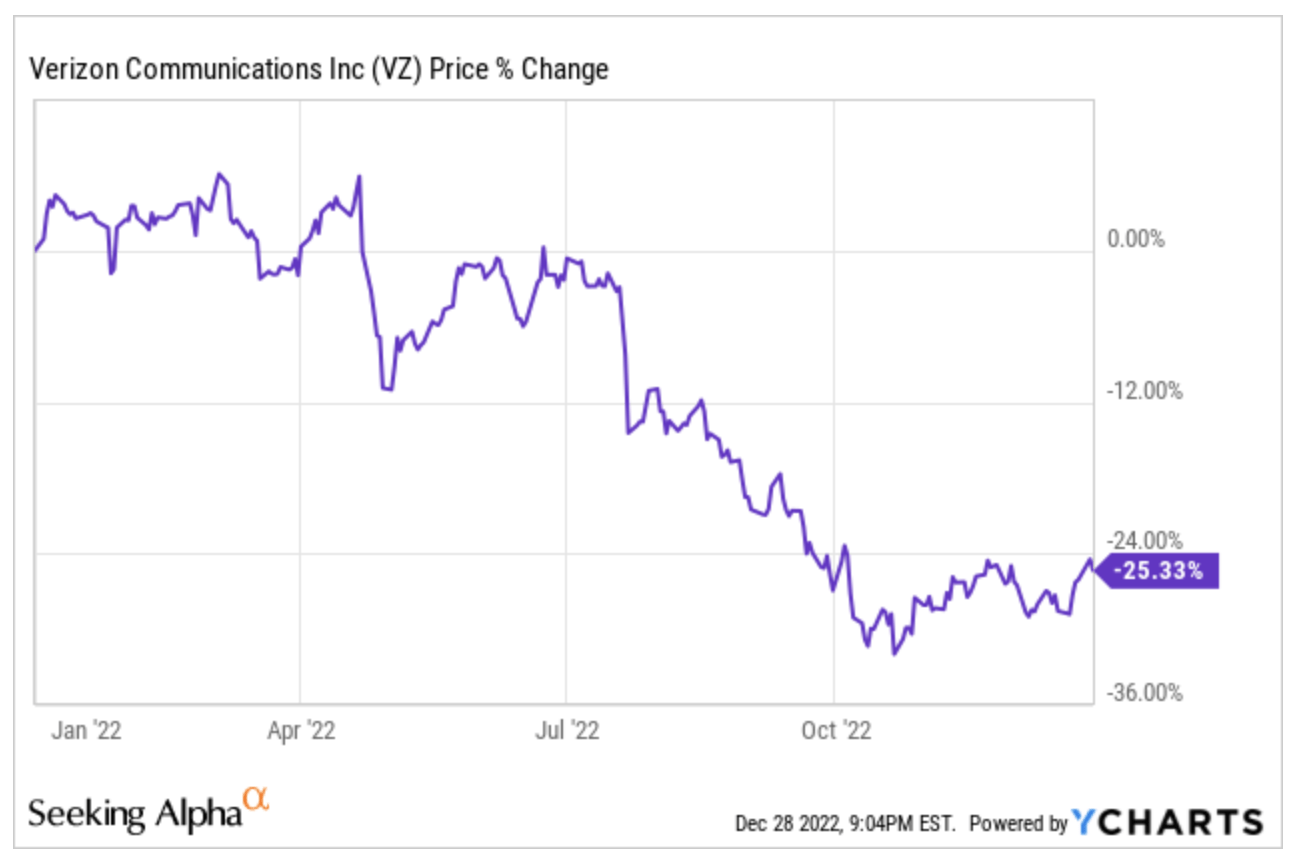

On the year, shares of VZ are down 25%.

ycharts

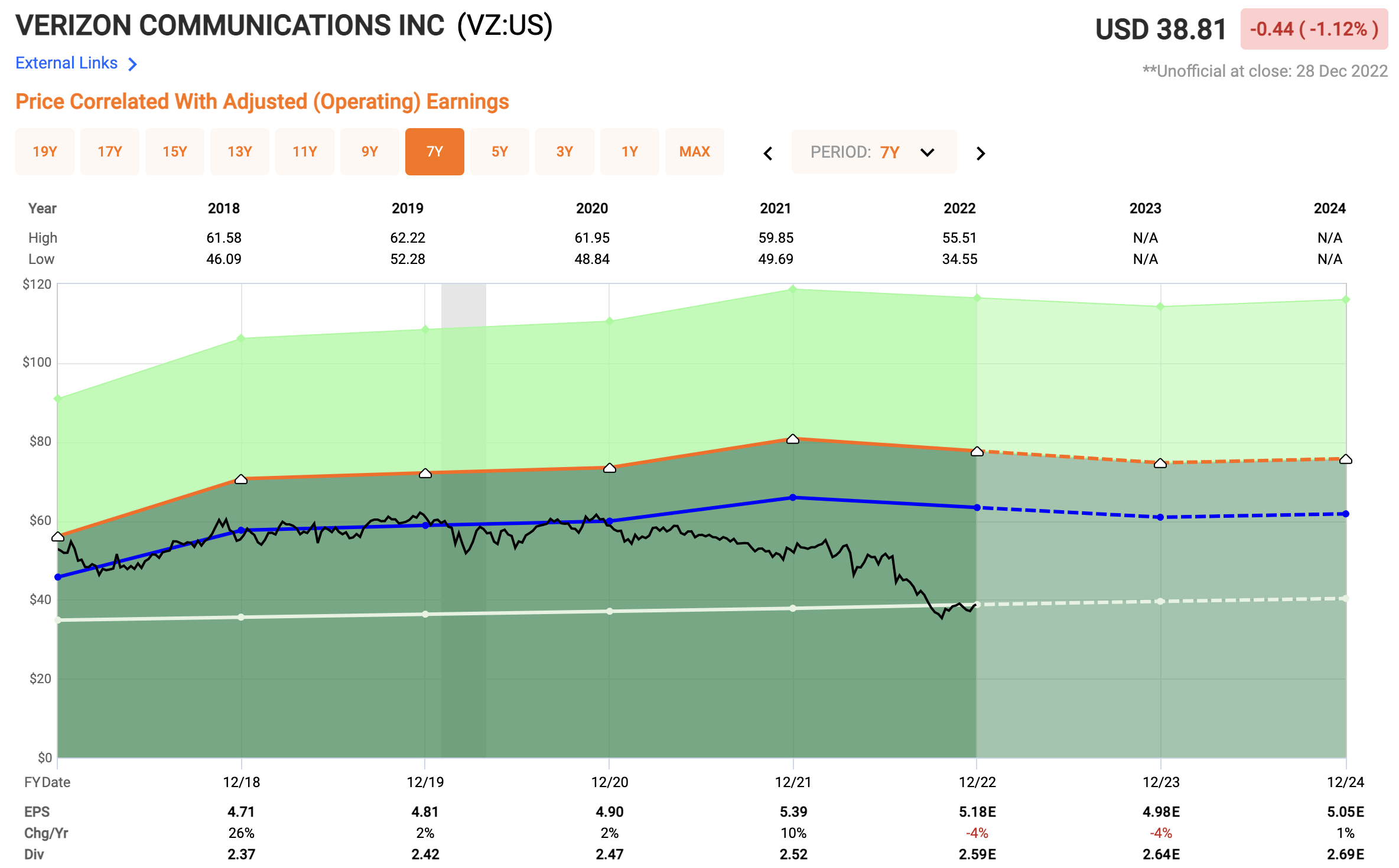

When it comes to VZ, a lot of the downside has been priced in to the share price already and Verizon shares now find themselves trading at just 7.5x next year’s earnings, which is an historically low valuation.

Fast Graphs

In terms of the dividend, the company pays an annual dividend of $2.61 per share which equates to a high-yield of 7%. Verizon has increased their dividend for 16 years and counting.

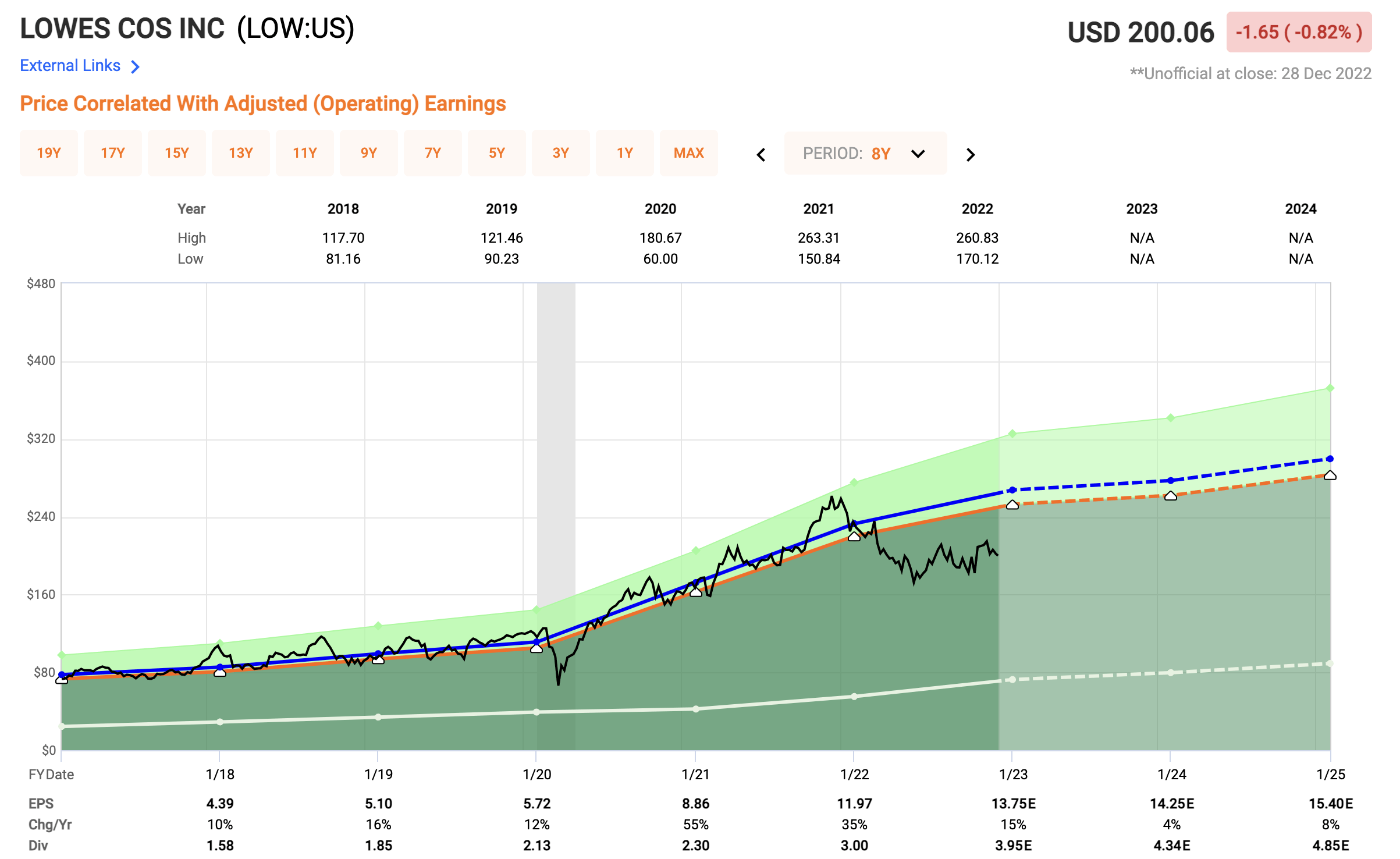

Dividend Stock #8 – Lowe’s Companies (LOW)

Lowe’s Companies happens to be one of my favorite stocks on the list. I have owned Lowe’s for a number of years, but sold out of the position at the end of 2021 due to valuation and concerns about the housing market in ’22. That move proved to be correct, but I am dying to get back into the position.

However, I am trying to be patient as the real estate sector continues to see some near-term headwinds, but the cheap valuation for this great dividend paying stock is making it tough to hold off.

Lowe’s currently has a market cap of $122 Billion, making it the 2nd largest home improvement retailer behind HD who has a market cap of $326 billion.

There is still plenty of separation between the two home improvement retailers. HD is largely considered the gold standard when it comes to operating efficiency, and that has allowed them to separate themselves as the clear leader in the space.

However, back in July of 2018, Lowe’s hired CEO Marvin Ellison, and I have written about it a number of times, but he is a big reason for the position I had built in the stock. When you look into his background, you see loads of amazing experience within retail and home improvement.

-

He spent roughly 15 years over at Target (TGT)

-

12 years in a senior leadership role at HD

-

CEO stint at JC Penny

That Home Depot role is what got me excited because he knew exactly what made HD so successful over the years and he has brought that over to Lowe’s.

On the year, shares of LOW are down 22%.

ycharts

Lowe’s is trading at an insanely low valuation, however, there are still plenty of headwinds in the real estate sector to know, but for long term investors looking for a GREAT dividend stock, look no further than Lowe’s.

Lowe’s currently trades at just 14x next year’s earnings compared to a 5yr avg of 19.5x.

Fast Graphs

In addition to the low valuation, Lowe’s also pays a dividend that yields 2.1% and has been growing its dividend for 61 CONSECUTIVE years, making them a Dividend King. Not only has the company been increasing the dividend, but they have been increasing it at a strong clip. The 5yr DGR is 21%. The past 2 years has seen dividend hikes of 31% and 33% respectively.

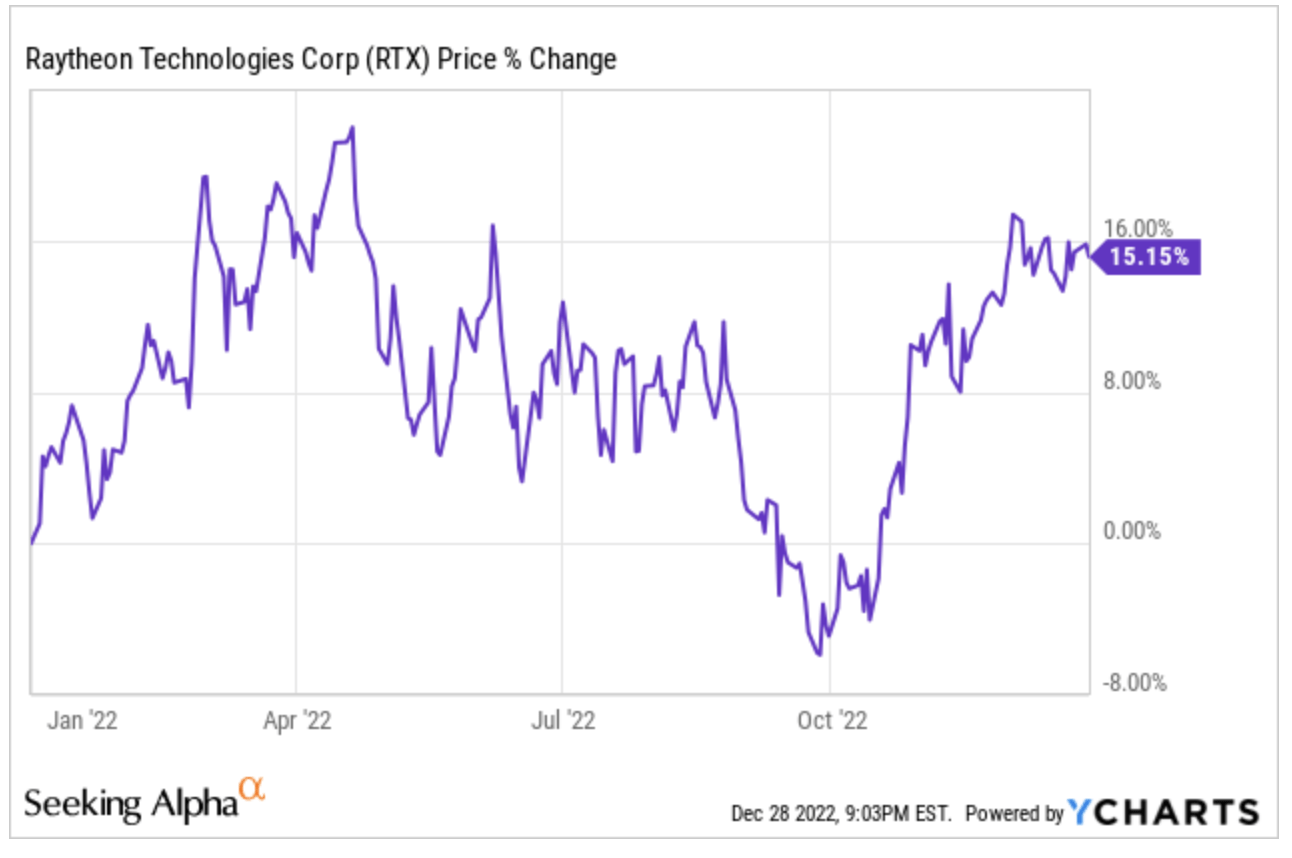

Dividend Stock #9 – Raytheon Technologies (RTX)

Next, let’s move into the Defense sector with Raytheon Technologies. Raytheon is the largest defense contractor on the market today with a market cap of $146 Billion.

Lockheed Martin (LMT) and Boeing (BA) are the next largest with market caps of $126 billion and $110 billion respectively.

On the year, shares of Raytheon have far outperformed the market as they are up 15%, making them the 2nd best performing stock on this list in 2022.

ycharts

Reasons to be optimistic going into 2023 begins with the global tensions that remain with the Ukraine/Russia war as well as growing tensions with China. Nations around the world, including the US, are looking to bolster their military, which provides a tailwind for this defense contractor.

Raytheon continues to secure new contracts that end up playing out over a number of years. The company recently secured a $619 Million contract with the US Navy for modifications to their F-35 jets. In addition, they were awarded a $1.2 billion contract to supply additional Surface to Air Missile systems to Ukraine.

These contracts continue to fund not only a safe dividend but a growing dividend. RTX shares currently yield a dividend of 2.2%. That dividend has been growing now for 29 consecutive years.

Even with the year RTX shares have seen, shares still trade at just 19x next year’s earnings compared to a 5yr avg of 27x.

Fast Graphs

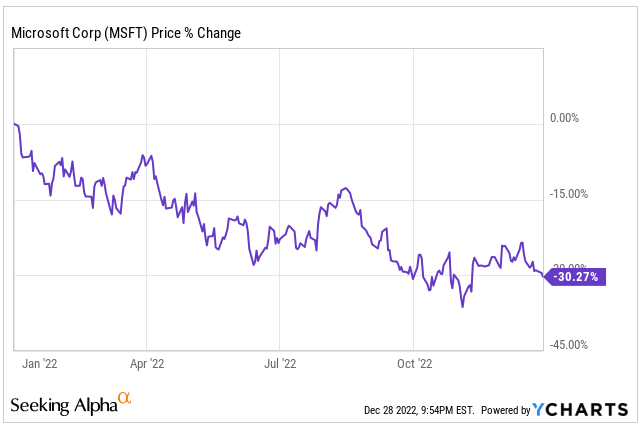

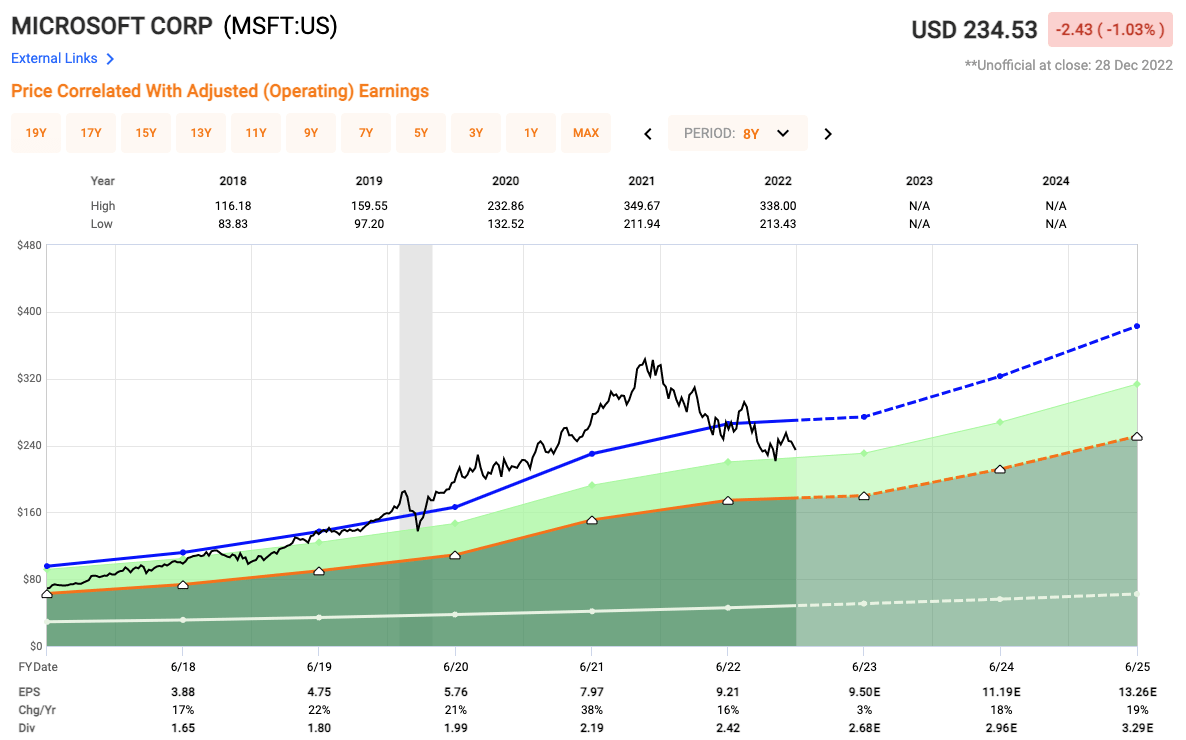

Dividend Stock #10 – Microsoft (MSFT)

The FINAL stock in my list of 10, is by far the most popular, and that is Microsoft. Microsoft currently has a market cap of 1.8 Trillion.

Big Tech stocks have been under siege in 2022, as the popular Invesco QQQ (QQQ) ETF has fallen over 35% and MSFT shares have fallen 30%.

ycharts

Valuations across the board skyrocketed in 2021, and 2022 has been the year of correction. We have seen a slowdown in spending and now we are also beginning to see layoffs in the tech field. MSFT being one of those companies announcing layoffs in recent months as a way to cut costs and improve margin.

When it comes to MSFT, they have a very diversified portfolio of products, a dominant cloud offering, and in addition to all that, they have a very strong management team. The company’s cloud offering Azure, is the second largest of all the cloud competition, trailing on Amazon’s (AMZN) AWS.

Microsoft is also looking to expand their gaming segment with the announced acquisition of Activision Blizzard, which is still under review by regulators.

This company is loaded, they still have massive revenues, strong cash flows all which will continue to fund their growing dividend.

After the year that MSFT has had, shares are now looking quite reasonable for long-term minded investor. Remember 2023 is still going to have plenty of headwinds but the key to remember is that the stock market is forward thinking. It does not trade based off what’s happening today, its trades off what it believes will happen in the next 6-9 months typically.

As such, right now you can pick up shares of Microsoft at just 21x next year’s earnings which is quite low for a company of MSFT’s stature considering they tend to trade closer to 29x.

Fast Graphs

In terms of the Dividend, MSFT pays a low yield and is more viewed as icing on the cake. MSFT currently has a dividend yield of just 1.2%, but it has been growing at a 10% clip the past 5 years and it has grown for 20 consecutive years making them well on track to become a Dividend Aristocrat soon.

Investor Takeaway

2023 will begin like 2022 is ending, under pressure, but it will be especially important for long-term minded investors to perform their due diligence ahead of time, so they develop a list of stocks they have on their watchlist for when the time is right.

All of these stocks are currently trading at great valuations, but given the market conditions, I think we could see some lower lows set in real soon, so my goal is to dollar cost average into these positions over time.

Let me know down in the comments section below which of these dividend stocks you prefer.

Be the first to comment