Khanchit Khirisutchalual

Investment Thesis

The Trade Desk (NASDAQ:TTD) has always been a crowd favorite and carried a valuation in excess of its peer group. In hindsight, this valuation premium was justified, as the Trade Desk succeeded in taking market share away from its peers, both big and small.

The question investors now have to attempt to answer is whether looking ahead The Trade Desk is the best place to deploy capital into. Or whether there are better opportunities elsewhere.

What’s Happening in the Market?

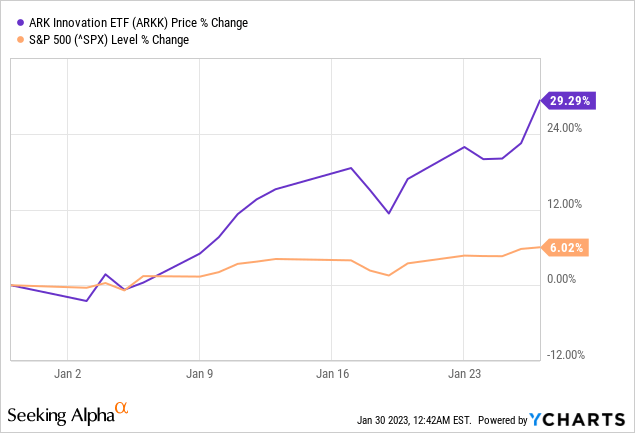

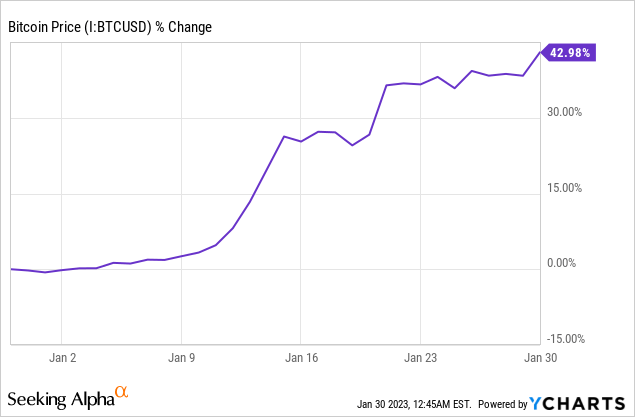

So far 2023 has seen unprofitable companies sizzle back. Hard. Risk appetite for ”concept stocks” is back. Above I’ve used the ARK Innovation ETF (ARKK) to echo this sentiment, but you can look elsewhere too. Perhaps Bitcoin (BTC-USD)?

I believe that since this area of the market was the first to implode in February 2021, this could be the first pocket of the market to stage a comeback. After all, it has been two brutal years for investors in that sector. And two years is a long time.

Going forward, in 2023, investors are going to be backing with their capital (and minds) exciting concept companies with attractive opportunities. Companies that were crushed in the past two years as investors stowed away their capital in areas that were perceived to be ”safe” investments.

And this leads me neatly to my next point.

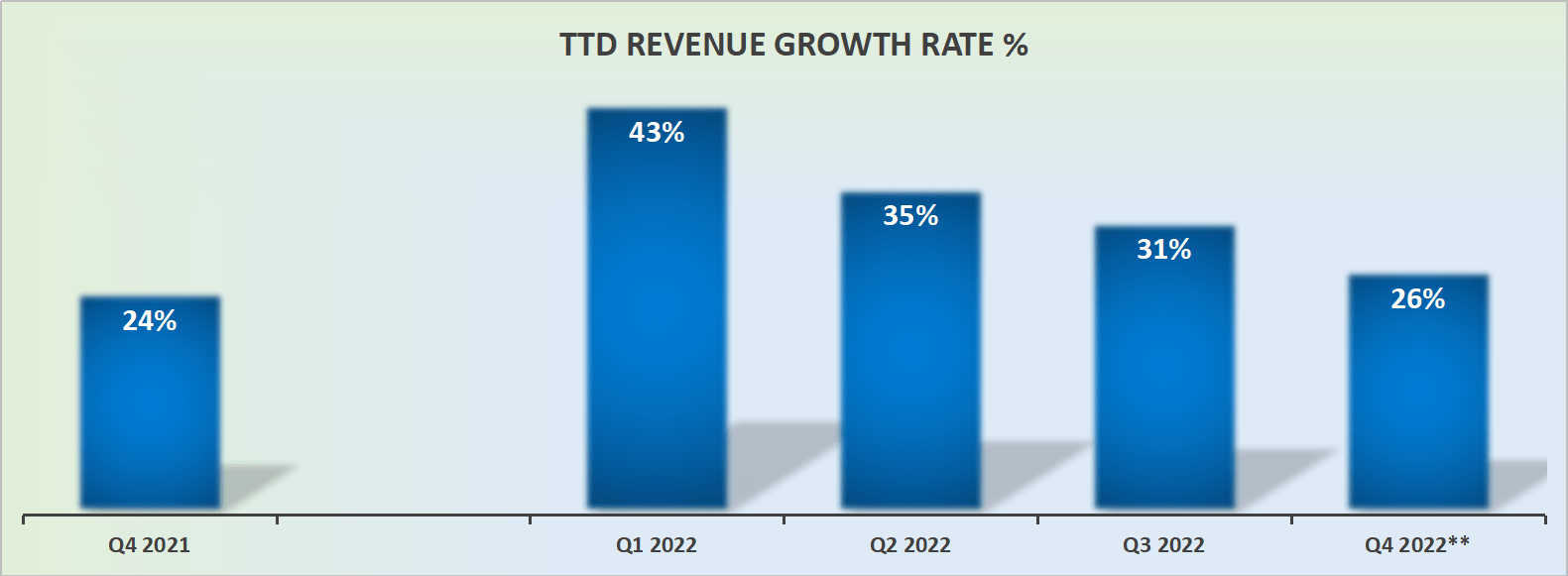

Is TTD Still a High-Growth Company?

Author’s work

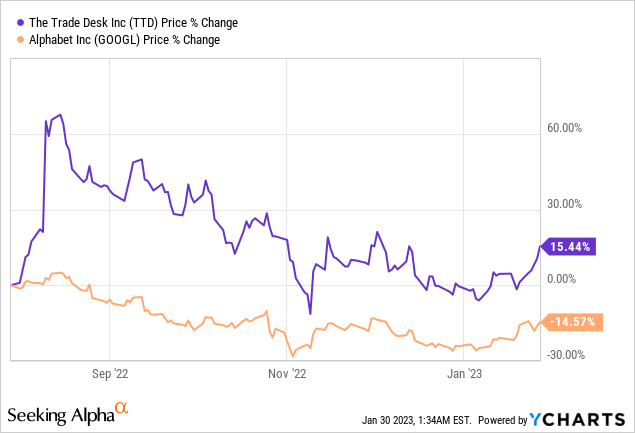

The Trade Desk has always been rewarded by investors for being a disruptive adtech player. Despite my concerns about its valuation, the fact of the matter is this: The Trade Desk was always more expensive than its peers because it has consistently positively surprised investors with its strong growth rates.

Even when many of its peers were struggling in 2022, somehow TTD was able to both take market share from Alphabet (GOOGL)(GOOG) and positively delight its shareholders.

Was TTD Too Bullish?

SEC Filing, Jeff Green package

Now we get into a contentious question.

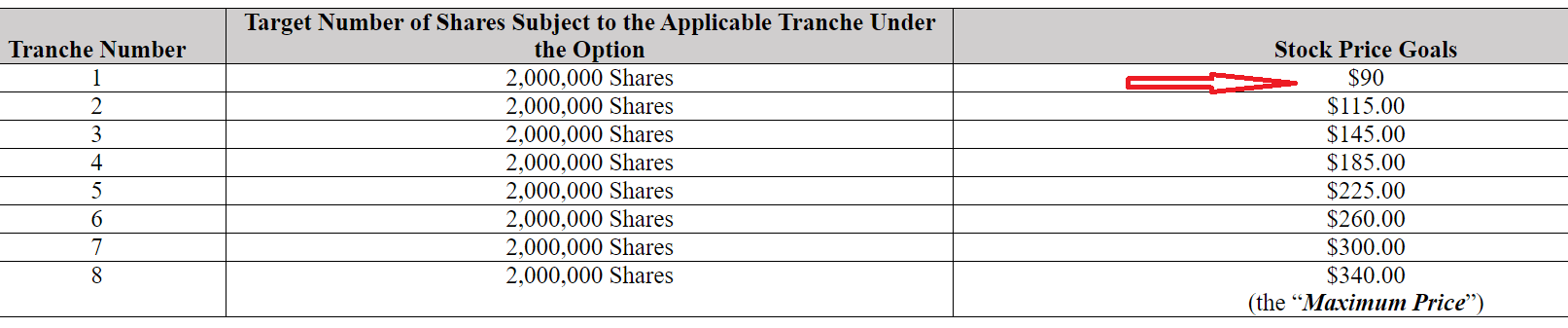

What we see above is The Trade Desk’s CEO Jeff Green’s package. You see that his compensation package is directly tied to the share price. If the share price gets to $90 there are 2 million shares coming his way. And with each further increment in the share price, there are another 2 million shares coming.

On the one hand, I don’t believe that this positively aligns Green with shareholders. For example, Mark Leonard from Constellation Software (OTCPK:CNSWF) has never diluted shareholders to compensate either himself or his management team and shareholders have benefited tremendously over time. And I don’t need to remind you about Warren Buffett either.

On yet the other hand, here’s another way to look at this. For example, Warner Bros. Discovery’s (WBD) CEO has built notoriety for his huge stock-based compensation and the stock has gone absolutely nowhere, even when Discovery was a standalone company.

I can highlight other examples from the Liberty groups, and you’ll see the same thrust. Huge stock-based compensation, but shareholders not faring well.

On yet the other hand, there’s another way to look at this. Unless The Trade Desk gets its shares price to $340 over the next eight years, this is all a moot point.

All this being said, recall when The Trade Desk’s board awarded this compensation package, The Trade Desk had been a crowd favorite among investors and analysts. Since October 2021, a lot has happened, as you know.

So, with this in mind, what should investors think about?

Is TTD Cheaply Valued?

Ultimately, I believe whether or not Jeff Green gets all or most of his stock compensation package comes down to the question of whether there’s still a disconnect between TTD’s future prospects and its valuation.

According to my estimates, The Trade Desk is priced at around 40x forward earnings.

And if while acknowledging that the Trade Desk has always traded at a premium to its peers, I have to question whether there’s not a significant amount of vulnerability in its share price.

Can TTD grow its bottom line quickly enough over the next 2-3 years to support this type of valuation? I’m not fully convinced.

The Bottom Line

At the start of the analysis, I turned our focus to the fact that many pockets of the market got crushed in 2021. Many companies within adtech were sold off by 50% or 60%, sometimes even 80%. But The Trade Desk navigated this whole period unscathed.

And while I believe there’s a significant amount of justification for why The Trade Desk didn’t sell off, I don’t necessarily agree that The Trade Desk is the most compelling space in the market for investors looking for an opportunity with a positive risk-reward.

Be the first to comment