DNY59

In this cycle Fed monetary policy has been conducted poorly and has been under attack. The Fed has been pressured from the start by progressives to delay its tightening, even in the face of inflation. While economists and monetary experts have been critical of the Fed for waiting so long to hike rates, that’s the path the Fed took.

Once the Fed got on the right hiking plan, it had a way to go to bring interest rates up in line with inflation, as it had fallen behind by an unprecedented margin. The Fed escalated its policy, raising rates relatively sharply. In the wake of those sharp increases markets have become concerned that the Fed may have raised rates too rapidly, risking recession.

However, rate levels compared to the pace of inflation do not suggest that the Federal Reserve has even made policy restrictive let alone too restrictive. Still, the argument about adequacy, the inadequacy, or of the excessive nature of Fed policy swirls about.

Summers: a critic, not an advisor

What is new is that Fed critic Larry Summers suddenly is abandoning his criticism that the Fed is too slow and needs to hike rates rapidly. Instead, he takes the position that the Fed should, at this meeting, be totally neutral and not provide any guidance at all about what it sees for the future and should instead let the economy itself develop and clarify what policy measures are needed. Summers has been quite a vocal critic of the Fed and his backing-off is a significant event for Fed policymaking – even though there’s no evidence that the Fed has been greatly influenced by Mr. Summers in the past. Summers had also been very critical of the Fed raising rates and urged it not to raise rates in December of 2018 in the last cycle when the Fed went ahead and hiked rates anyway. That proved to be a rate hike that was at least ‘one too many,’ as the Fed then had to begin dismantling rate hikes later in 2019.

I don’t know what has caused Mr. Summers to change his mind about his advice to the Fed but the table below is instructive in looking at what’s in play regarding Fed policy.

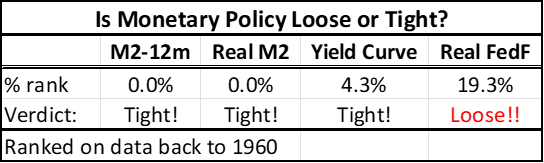

Mixed and contrary policy signals (Haver Analytics and FAO Economics)

This table evaluates four different metrics that are often used to assess Fed policy. It ranks each measure on data back to 1960. It shows that the simple 12-month growth rate in the nominal money supply has never been weaker. Similarly, if we make the calculation for the real money stock for M2 adjusted for PCE headline inflation, the 12-month growth rate in the real money stock is the weakest that we have seen as well. To evaluate the yield curve on such a long timeline we have to use the securities that are available over that horizon. The yield curve measure in the table is the difference between the 10-year Treasury note yield and the three-year note yield. What we see is that yield curve measure has been lower (in this case it means more inverted) only about 4% of the time. However, if we assess Fed policy by looking at real interest rates, the real fed funds rate (nominal fed funds less the 12-month pace in the PCE headline), we find that the real fed funds rate has been lower only about 19% of the time. The Real funds rate shows that monetary policy is still quite stimulative.

This is in line with the old Summers criticism; it says that the Fed still has more work to do in raising rates. However, Larry Summers has gotten off that bandwagon and he’s on a new one. Does that mean that he’s been looking at money growth and that is more impressed with the weakness in money growth rates? I don’t know…

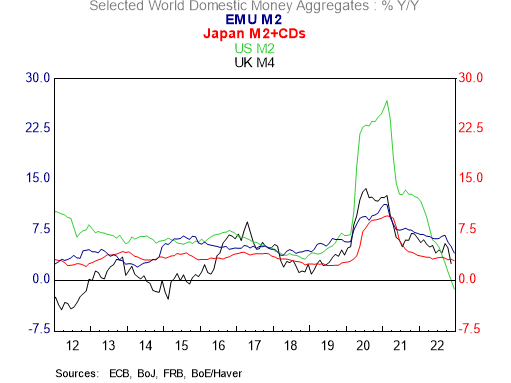

Global Money Supplies Soar and Dip (Haver Analytics and FAO Economics)

A Global Boom-Bust Cycle

When we look globally, we find that there has been the same sort of monetary boom bust abroad that we have seen in the US. The US cycle has been the most outlandish. Still, there are the same boom-bust forces generated in the EU, the UK and to a lesser extent in Japan. There is a burst of stimulus followed by a pull-back and the two sets of forces are so close together that their impacts intermingle, complicating any analysis. That doesn’t help us evaluate the impact of US monetary policy. It just alerts us to a global magnification of the risks.

What to focus on?

Should the Fed be looking at the real interest rate or should it be looking at the money growth effect? Depending on which scheme is used to evaluate the relative tightness of monetary policy, different answers are obtained. In fact, the market measure of looking at the yield curve seems to conclude that policy has been so tight that recession is coming, something that economists have been batting around as a possibility.

Is it conceivable that the US could transition from the strongest money growth in 60 years to the weakest money growth in 60 years over a period of just one-and one-half years, and avoid recession? Maybe it can, but I don’t see how.

The most interesting schism is between the money signal and the real interest rate signal.

- Money growth rates, earlier in this cycle, boomed at the strongest growth rates that we’ve seen since 1960. Nine of the strongest year-over-year growth rates (monthly) were posted in that cycle whereas now money supply growth is declining and it’s the first outright contraction in the 12-month change in the money stock in over 60 years. Money growth has gone from being super stimulative to being contractionary in a way that is without precedent.

- By comparison real interest rates are in ‘nowhere land.’ Real interest rates, in the stimulative part of the cycle, show the 13 lowest real fed funds rates since the 1960s (all deeply negative real Fed funds rates). This emphasizes and reinforces the news from money growth that finds a great deal of stimulus from monetary policy in this cycle as Covid struck. However, after that, there’s a divergence in the money growth Vs real rate analyses and signals. Real interest rates continue to give a signal that monetary policy is still benign and stimulative while money growth signals speak to an unprecedented contractionary force developing.

- This is a significant difference between the signals from money growth and real interest rates. Money growth rates may well be signaling a recession. However, real interest rates; Real rates had been at unprecedented lower levels earlier in the cycle, but have only risen to a point such that real interest rates since 1960 have been higher 80% of the time, hardly painting the picture of a tight monetary policy that could cause a recession.

What is the Fed to do? If you are confused about the state of monetary policy, it is because you are paying attention!

This is a clear dilemma and a split in the signals about what Fed monetary policy is doing right now. Clearly, it’s good to look at both of these metrics, both at money growth and at real interest rates. It’s good to be informed about what the monetary signals are. However, once informed, we are not well-advised about what to do. At this point, Summers’ advice seems best. Given the confusing and contrary signals about the tightness in monetary policy the Federal Reserve should stop giving forward guidance and should wait to see what’s going to develop after delivering its expected 25bp hike.

What the Fed can and can’t do…

Since the Fed is not offering any new projections at this meeting, avoiding any new guidance should not be difficult. But is the Fed prepared to do that? And if the market sees the Fed stop saying that it plans further rate hikes, will markets take that as a signal that the Fed funds rate is at its peak? Markets already are rallying in the New Year and that rally has loosened underlying financial conditions ahead of the Fed moving. On further thought there is probably nothing the Fed can do or say in the way of change that markets will not interpret to have more meaning than what the Fed intends. That’s show business and monetary policy. Some things are simply beyond control.

Be the first to comment