Nickbeer/iStock via Getty Images

During this fortuitous time of a sharp rebound, we often have to dig deep in untouched corners of the market in order to find true bargains that have the potential for big gains. A rising tide lifts all boats – but acute stock-picking can deliver tremendous rewards.

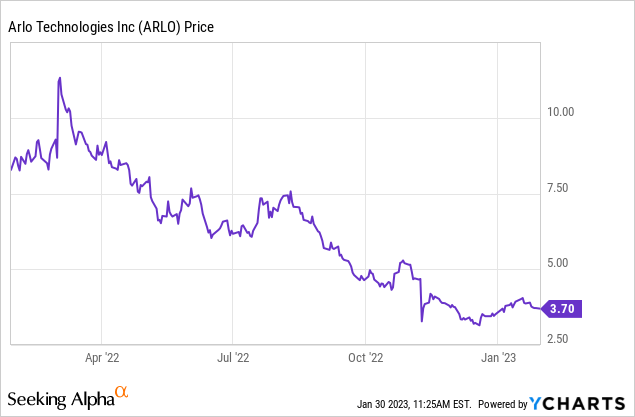

Arlo (NYSE:ARLO) is a small-cap stock worth watching. The maker of home security cameras is down nearly 60% over the past year, and this year’s rebound rally in small and mid-cap growth stocks has barely helped drive any resurgence in this stock, despite solid fundamentals. It’s a good time, in my view, for investors to re-assess the bullish thesis in this stock.

The bull case for Arlo

I remain bullish on Arlo and encourage you to hold it in your portfolio. In my view, many of Arlo’s merits have gone un-recognized. Yes, Arlo may today be a hardware vendor selling a fairly common product – but it’s the company’s rapidly growing base of subscribers that makes Arlo a stickier product and will drive margins in the long run.

Here is my full long-term bull case for Arlo:

- Best-in-class category leader. Arlo has been highly reviewed by major tech publications like CNET and PCMag and is considered one of the top home smart cameras. In addition to this, Arlo is one of the most prominent security companies to promote DIY installation, vs. other cameras that required expensive technicians for installation.

- Huge TAM. Arlo estimates the market for home security to currently stand at $53 billion, and it also expects this opportunity to grow to $78 billion by 2025. With less than ~$500 million in annual revenue, Arlo has plenty of room to expand and innovate in this space. Given as well that there is no clear leader in the home security camera market, Arlo has a chance to take the crown.

- Partnerships with some of the largest retailers in the country. Arlo products are sold through resellers like Best Buy (BBY), Costco (COST), Amazon (AMZN), and others. Arlo’s visibility to consumers is unmatched, and the company is well-positioned for retail sales growth ahead of the holiday season.

- Building a subscription base. Arlo is moving away from being a pure hardware products company. Paid subscriber accounts, reaching more than 1.6 million as of Arlo’s most recent quarter, are growing at faster than a 2x y/y clip. Arlo also notes that ~65% of new hardware customers sign up for Arlo Secure within six months.

- Profitability. Unlike many small-caps of its size, Arlo has hit pro forma operating profitability, or hovered very close to it, for several quarters in a row.

Valuation: a lot of it is sitting in cash

Let’s now zoom in on Arlo’s valuation. At current share prices near $4, Arlo trades at a market cap of just $326.5 million. Note as well that the company has a generous $125.3 million load of cash on its balance sheet. On a per-share basis, that works out to $1.42; in other words, roughly one-third of Arlo’s current market cap is already “instantly” valued in cash.

Arlo cash (Arlo Q3 earnings release)

Netting out this cash from Arlo’s market cap, we get to an enterprise value of $201.2 million.

For the current fiscal year FY23, meanwhile, Wall Street analysts expect Arlo to generate $484.0 million in revenue – representing flat 1% y/y growth, which I think is quite conservative given Arlo is currently growing at a mid-teens pace. Nevertheless, taking consensus at face value, we arrive at a valuation of just 0.4x EV/FY23 revenue for Arlo. In other words – Arlo is cheap enough to take a bet on.

Zooming in on services growth

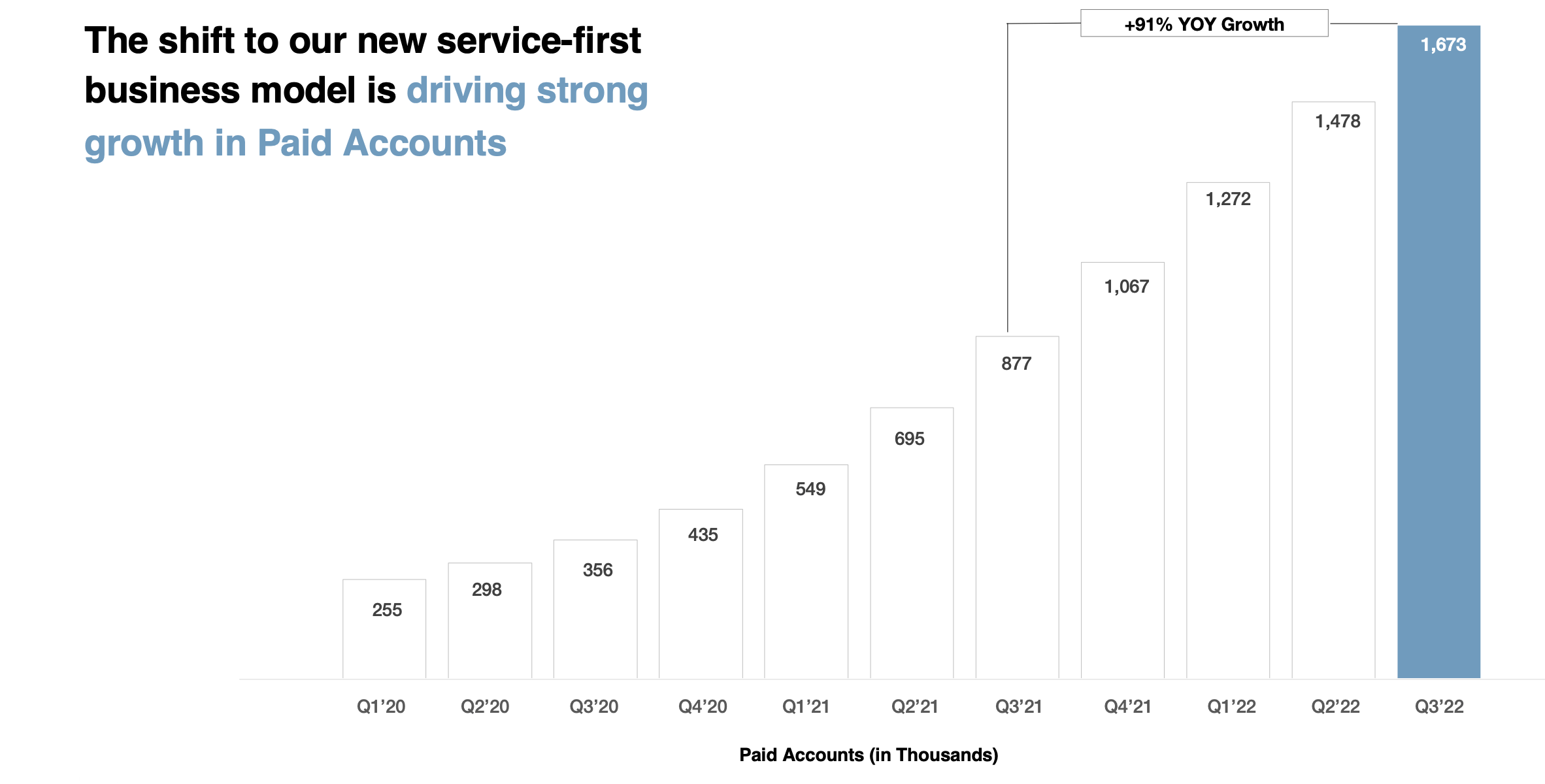

The core piece of the Arlo story that investors should focus on is how the company is building up its services/subscription base. In Arlo’s most recent quarter, the company added 195k net-new paid subscribers, growing its subscription base by 91% y/y to 1.67 million:

Arlo paid account growth (Arlo Q3 earnings deck)

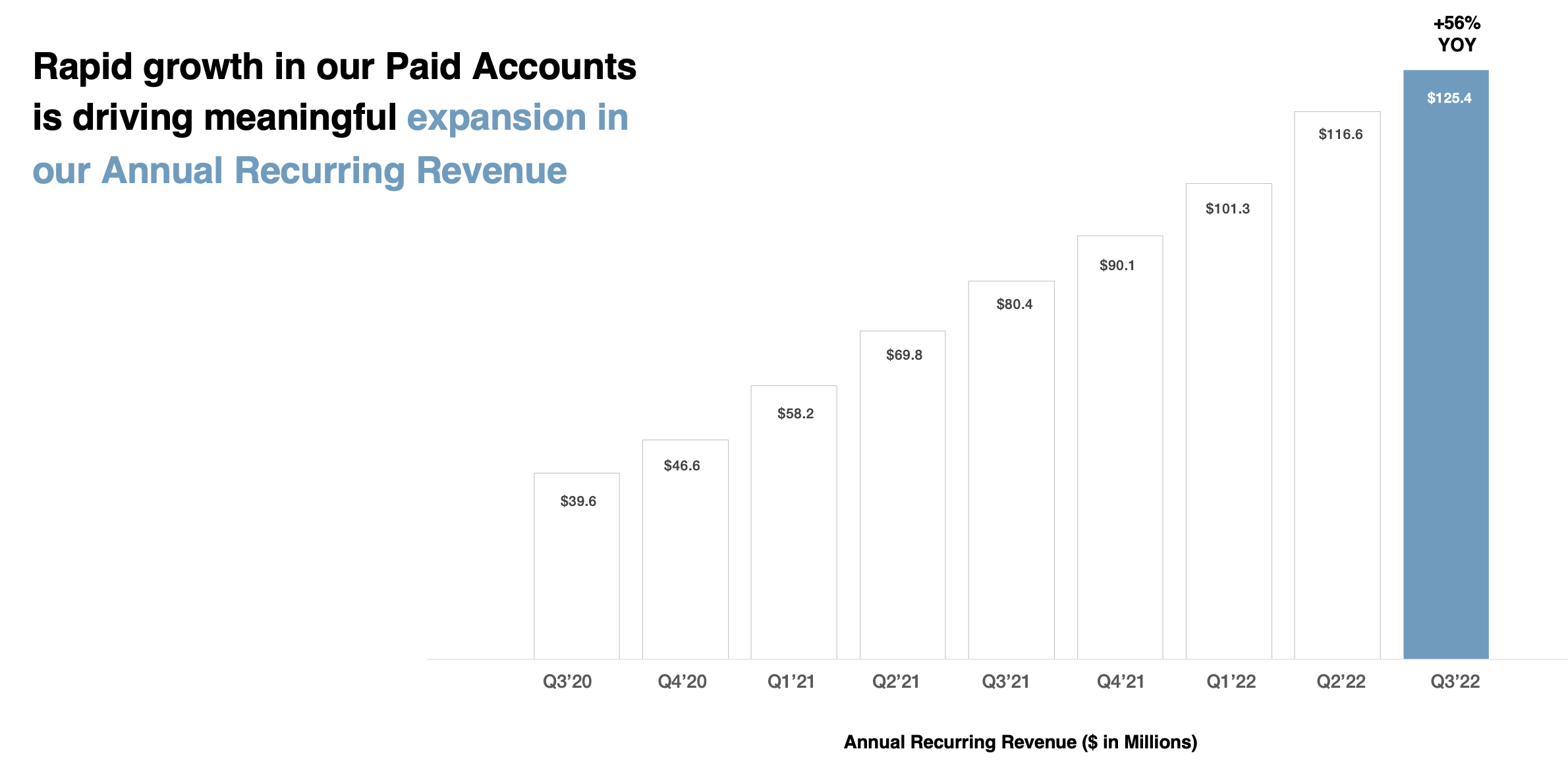

Similarly, ARR also grew 56% y/y to $125.4 million:

Arlo ARR growth (Arlo Q3 earnings deck)

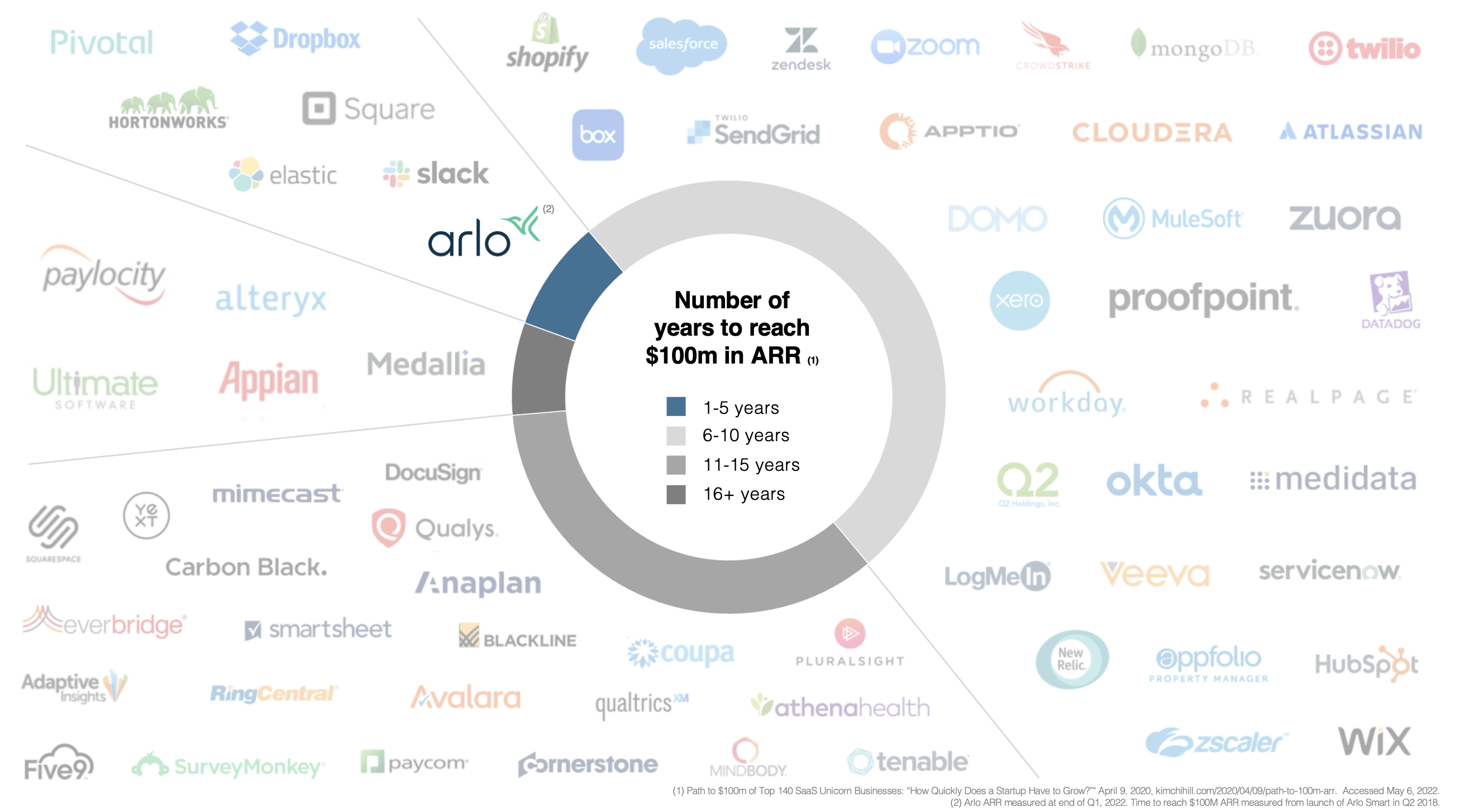

The company only crossed the $100 million ARR mark early last year. Management presented an interesting chart below, showcasing that very few consumer/internet or software companies reached the $100 million ARR mark as quickly as Arlo did:

Arlo ARR buildup comparison (Arlo Q3 earnings deck)

Now, of course, it would be prudent to expect some near-term moderation in terms of growth rates. The company noted that it does expect macro pressures to have an impact on its business, notably via channel partners who may be trying to offload inventory (and may not replenish as quickly as in the past). Per CEO Matthew McRae’s remarks on the Q3 earnings call:

While we were pleased with our execution against a challenging supply picture, near the end of Q3, we started to see a shift in consumer behavior, where broad-based inflationary pressures, coupled with the threat of recession are dampening consumer demand industry-wide.

With a weaker demand outlook, our retail partners are moving to increase promotions and lower inventory. In consideration of this, we took immediate action to adjust our strategy and match our operational footprint to this new outlook for Q4 and 2023.

First, we decided to pause, our branding campaign. As we discussed, the initial awareness spend was a test implemented to measure via paid account uplift over our baseline subscriber run rate.

However, despite creating nearly one billion impressions and a promising list in consideration in the first six weeks, the volatility of the baseline in this market makes it difficult to effectively measure and evaluate the efficacy and ROI of the spend. So this spend is paused indefinitely, until we see the market return to a more positive and stable trajectory.

Second, we initiated a review of expenditures across the company to identify areas of further optimization of our business. We have well-defined plans to lower run rate in various areas of OpEx to ensure we are structured to maintain our most important levers of top line growth and achieve our long-range plan in the most efficient and disciplined manner.”

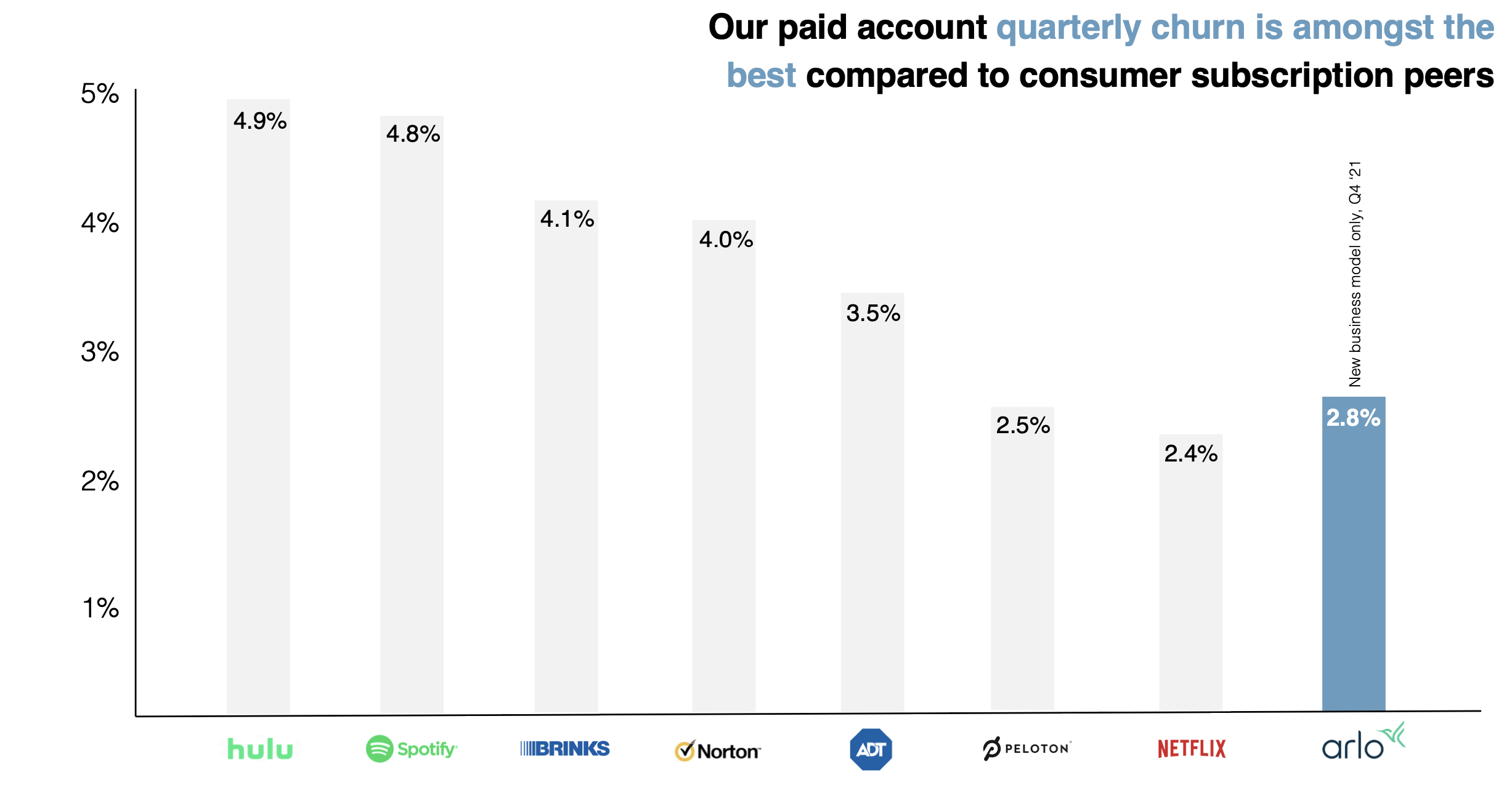

So far, however, while new hardware sales may be impacted by macro headwinds, we have not seen any impacts to churn. Arlo’s paid account churn rate of 2.8% has remained consistent with prior quarters (flat to Q2) and lower than security peer ADT as well as other consumer services:

Arlo churn comparison (Arlo Q3 earnings deck)

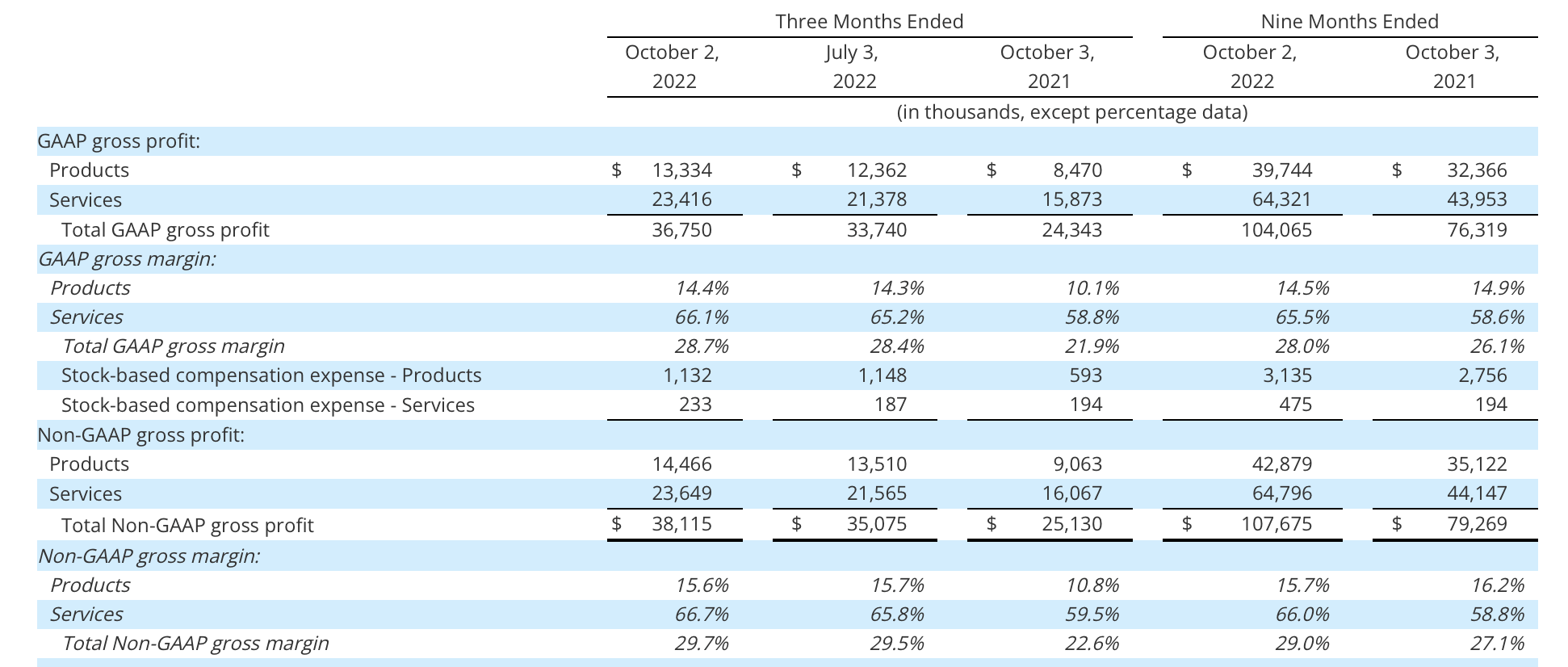

Services are driving margin expansion

Continued account growth and low churn are helping Arlo’s revenue mix tilt toward services, which represented 64% of total revenue in Q3. Services margins themselves are improving, up 720bps to 66.7% in Q3 driven by economies of scale – which have helped Arlo’s overall gross margin jump 710bps on a pro forma basis to 29.7%:

Arlo margin breakdown (Arlo Q3 earnings deck)

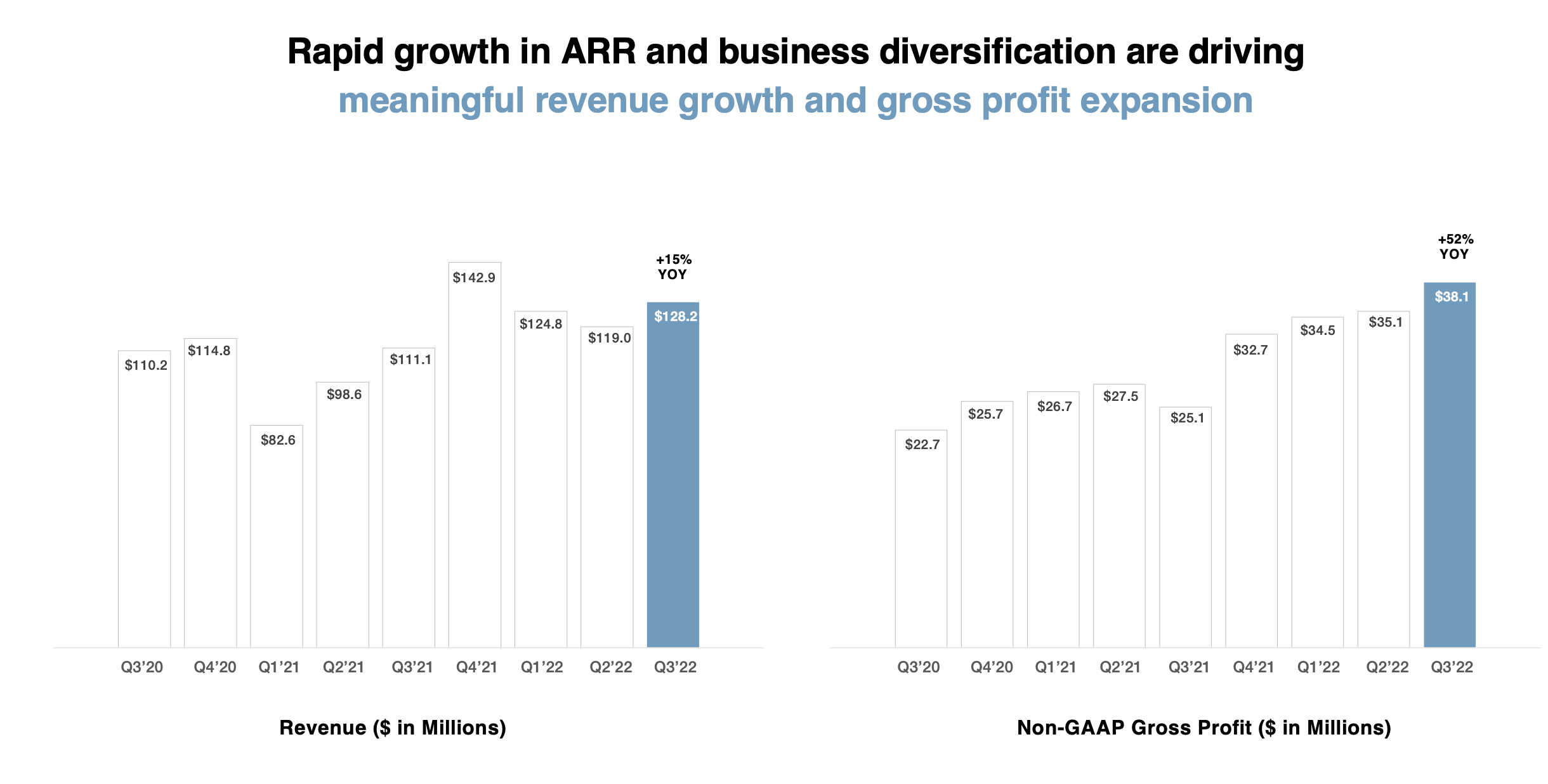

Worth noting as well is the fact that pro forma gross profit dollars grew 52% y/y to $38.1 million, as shown in the chart below:

Arlo pro forma gross profit growth (Arlo Q3 earnings deck)

On top of the expense review that Arlo conducted in Q4 with the aim to slice out 10% of its global workforce, there’s a compelling path to profitability here as Arlo continues to build up its high-margin ARR stream.

Key takeaways

With clear tailwinds in its low-churn subscription business that continues to add paid accounts at a rapid rate, I see no reason not to bank on Arlo while it’s held down by pessimism. Especially with the stock’s low valuation and generous cash balances, I view Arlo at <$4 as a low-risk bet. Stay long here.

Be the first to comment