Justin Paget

“Desperation is the raw material of drastic change. Only those who can leave behind everything they have ever believed in can hope to escape.” – William S. Burroughs

Today, we take a look at The St. Joe Company (NYSE:JOE). The company has been the beneficiary of the large-scale migration from the northeast as well as places like Chicago, where people have sent an influx of emigres to the Sunshine State over the past decade. This migration accelerated during the pandemic.

Through its large land holdings in Northwest Florida, the company has reaped the benefits of increased land prices this exodus has driven. The shares have been weak this year thanks to the slowdown of the housing market thanks to much higher interest rates. However, the company is well positioned to continue to profit from this intrastate migration. The shares attracted some small insider buying in June as well on the equity’s pull back. An analysis follows below.

Seeking Alpha

Company Overview:

The St. Joe Company is based in Panama City, FL. The company owns approximately 170,000 acres of land in Northwest Florida. St. Joe has three business segments. The first ‘Residential’ plans and develops residential communities of various sizes for homebuilders or retail consumers by primarily sells developed homesites and parcels of entitled or undeveloped land. The second ‘Hospitality’ owns and operates a private membership club, golf courses, beach clubs, retail outlets, marinas, and other entertainment assets. The final segment ‘Commercial’ engages in leasing of commercial property, multi-family, a senior living community, and other assets as well as grow and sell pulpwood, sawtimber, and other forest products.

The stock currently trades just above forty bucks a share and sports an approximate market capitalization of $2.4 billion. The company’s multi-family and senior living portfolio now has over 1,000 units, with a current occupancy rate of 93%. Three more multi-family and senior living projects under construction. Its commercial leasing portfolio consists of approximately 981,000 square feet, which also is 93% leased currently. New village centers under construction could add an additional one million square feet to that portion of the company’s portfolio. The company opened a Homewood Suites hotel in March and has six other hotels under construction. Most of the value of the company is via its land bank holdings and that is what we primarily concentrate on in this article.

May 2018 Company Presentation

Second Quarter Results:

On July 27th, the company posted second quarter results. The company had GAAP earnings of 29 cents a share as revenues slipped just over five percent from the same period a year ago to $68.2 million. It is important to note because the bulk of revenue is due to the timing of homesite sales and a mix of sales from different residential communities, it can be ‘lumpy.‘ In the first quarter, the company had just under $65 million worth of revenues, which was up 57% from 1Q2021. Leasing revenue increased by 45% and hospitality revenue increased by 31% from 2Q2021. In the first six months of this year, revenues have increased 17% from the same period a year ago to $133.1 million.

Analyst Commentary & Balance Sheet:

The company gets next to no analyst coverage, and I cannot find one analyst firm rating on the stock over the last year. Only approximately four percent of the outstanding shares are currently held short. The CEO bought 3,200 shares worth of stock in three transactions in May and June. These were the first insider buys in the stock in over a year. Via the last balance sheet snapshot from Seeking Alpha, the company ended the second quarter with approximately $135 million of cash and marketable securities against roughly $470 million worth of long-term debt on its balance sheet.

Verdict:

The hardest part of the St. Joe story is management doesn’t make a lot of data available. The last investor presentation was in 2018, and other than the quarterly earnings press release, there are no conference call transcripts to dig into. One can’t value the company via its sales or earnings as its core asset is its 170,000 acres as well as building and facility holdings. Dividing the stock’s market cap by its acreage puts a value on each acre of just over $14,000.

All acreage is not created the same, and an acre can yield multiple home sites. In the second quarter of this year, each homesite averaged $83,000 whereas each homesite in the same quarter a year ago yielded an average of $164,000 per homesite. In 2020, the company depleted only 2% of its land bank to generate $143 million of revenue, and land values have gone up substantially since then.

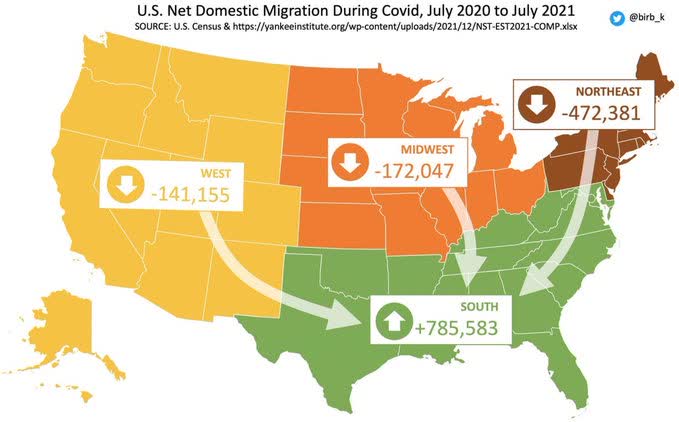

Some 280,000 net New Yorkers migrated to Florida over the decade that ended prior to the pandemic. They were joined by their brethren from the Northeast looking for warmer weather, a lower cost of living and no state income tax. The Midwest and other parts of the country have also migrated to the Sunshine State over the past decade.

U.S. Census

That has made Florida one of the fastest-growing states in the union for several decades. That migration accelerated during the pandemic and hasn’t let up since. This should be a long-term tailwind for the value of the company’s land holdings.

One of the biggest hindrances to shareholder value is the lack of data and communications from management. A few solid investor presentations could highlight the underlying value of its holdings, especially in light of a dearth of coverage from Wall Street. Leadership seems reticent to do this for some reason, however.

That said, I find St. Joe a solid ‘sum of the parts‘ story. I bought the stock heavily after the lockdowns ended as I saw what was happening with migration patterns (I had an apt in NYC at the time). I sold most of those holdings in the mid $50s earlier this year, as I figured rising mortgage rates would impact most housing plays significantly.

That said, anything below $40 seems a solid long-term bargain. Given options on JOE are quite liquid, I will be adding to my holdings via covered call orders at anything below this level.

“The tragedy is not that we are alone, but that we cannot be. At times I would give anything in the world to no longer be connected by anything to this universe of men.” – Albert Camus

Be the first to comment