Daleta

Last week saw the S&P 500 (SP500, SPX) posted its first weekly loss in about a month. The culmination of a VIX expiration, Fed minutes, and monthly options expiration helped break the equity market down on Friday and potentially ended the summer rally dead in its tracks.

Now maybe about when things get interesting, with Jackson Hole this week and a slew of Fed officials pushing back against the markets, concluding with Jay Powell himself on Friday, August 26.

Anchored In Reality

While equity markets have been in fantasyland focused on a make-believe dovish Fed pivot, the bond and currency markets have been anchored in reality. That reality shows there is no pivot, and those who bet on a pivot coming will be proven wrong.

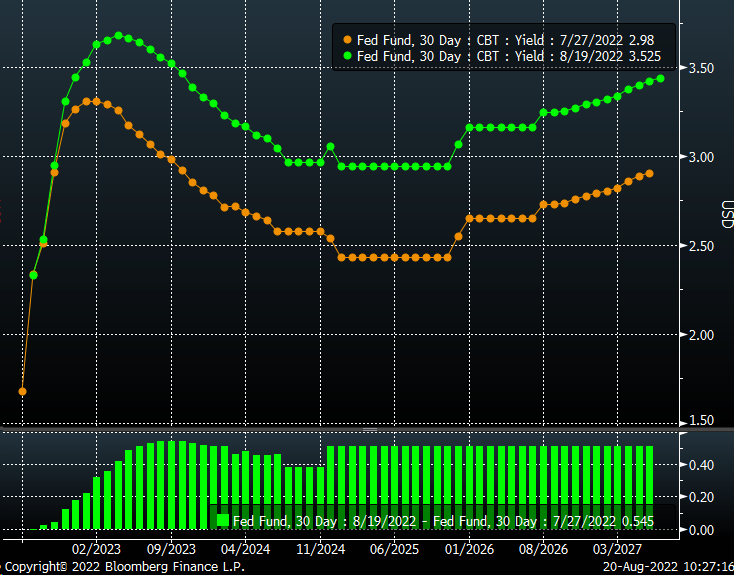

The Fed Fund Futures shows us that rates have moved sharply higher since the July FOMC meeting, with two more full rate hikes priced starting in May 2023 until the beginning of 2024. On top of that, the peak rate has shifted from January 2023 to April. The Fed Funds Futures are now pricing in more rate hikes and staying higher for longer.

Bloomberg

Not only that, but the spread between the December 2022 and the December 2023 Fed Funds contracts has narrowed to just -11 bps, from more than -40 bps in July. That is a massive shift in just a short period, indicating that the market is pricing fewer rate cuts in 2023.

Bloomberg

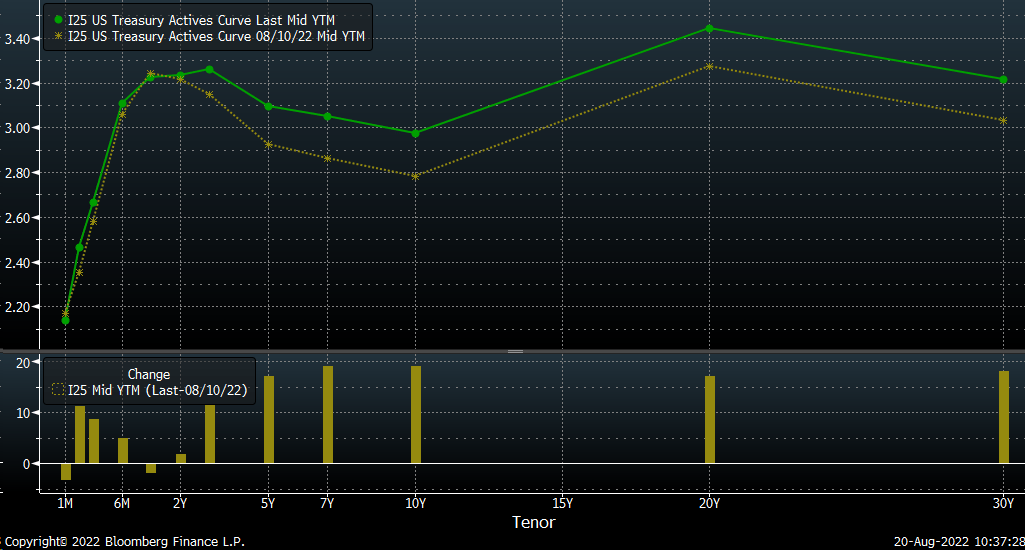

Even nominal yields appear to agree and have risen sharply since the weaker-than-expected CPI and PPI reports. Instead of rates falling, they have increased. Look at the yield curve, with the rates rising between 15 and 20 bps on the 5-Yr Treasury out to the 30-year Treasury. Meanwhile, 2-yr rates have remained unchanged. If the market viewed a dovish pivot or that inflation would suddenly come crashing down, then rates should be falling, not rising.

Bloomberg

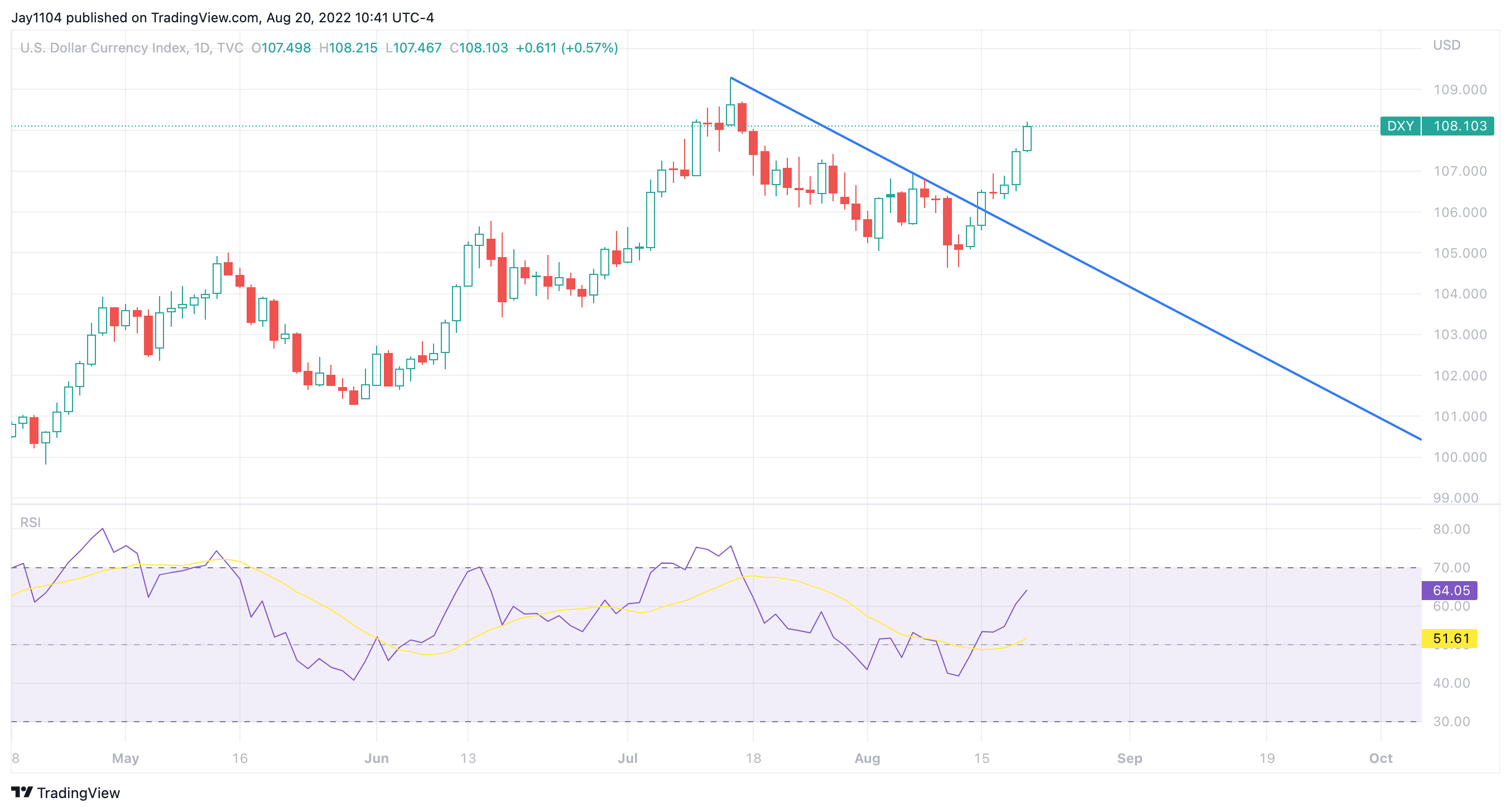

Even the dollar index has risen significantly. After initially plunging following the CPI report, the dollar index has broken out, surpassing a critical downtrend. It has increased by nearly 4% since August 11 and almost 1.5% from its July 27 lows. The dollar has been rising because it sees more hawkish monetary policy, and it had a massive move higher following the Fed minutes on August 17.

TradingView

Unhinged

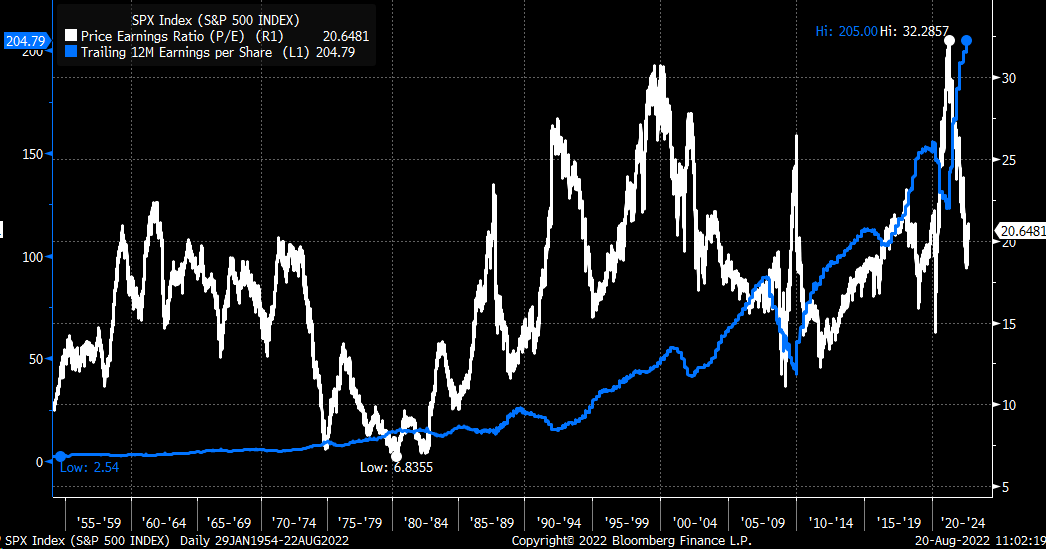

Meanwhile, since July 14, the S&P 500 has risen by 13.6% through August 19 and by as much as 15.7% at its August 16 peak. That has pushed the S&P 500 PE ratio on a trailing-twelve-month basis up to 20.6. That is more than 3 points higher than its historical average going back to the year 1954 of 17. The most jaw-dropping feature may be that in the 1970s and the early 1980s, the last time inflation was this high, the PE ratio was below 10. The big difference between now and then was that rates were much higher in the 1970s and 1980s.

Bloomberg

The high inflation rates of the 1970s and 1980s pushed the nominal 10-yr rate to around 16% at its peak by 1981. Meanwhile, the spread or the difference between the 10-yr rate and the y/y CPI rate was positive. Right now, that spread is profoundly negative at more than 6%. The only two other times in recent history that happened were in 1975 and 1980. It would suggest that if the inflation rate doesn’t start coming down quickly, nominal yields will need to push much higher in the future.

Bloomberg

The big problem is that the S&P 500 earnings over the past twelve months have been around $204, and at 17 times earnings, the value of the S&P 500 would fall to approximately 3,480. But the higher rates have to rise, the lower the PE multiple would need to contract. For example, if the PE returned to the December 2018 low of around 16, the S&P 500 would be worth around 3,200.

Bloomberg

In typically equity market fashion, it has become detached, while the reality is again reflected in the bond market, the currency market, and the Fed Funds Futures. Equities tend to be irrational when they either rise or fall, but this time they have become unhinged, and this recent summer rally may fade away even faster than it came to be.

The summer fade may be especially true if Powell can deliver a message that is clear and direct and not one that is two-sided. Add to that a slew of economic data set to be released between September 1 and 3, which may likely support rates going much higher, and staying there for some time.

Be the first to comment