Torsten Asmus

2023 January’s Two Market Narratives

a) The Goldilocks, Inflation has Peaked Narrative and

b) The Impending Recession Narrative

The Goldilocks, Inflation Has Peaked Rally

The year started with the “Inflation has peaked” narrative as evidenced by a somewhat Goldilocks jobs report with decent growth in new jobs, but importantly, a moderate rise in wages, benign CPI and PPI reports, and lower inflation expectations from The New York Fed Consumer Survey and the University of Michigan’s Consumer Survey.

All of these led to a drop in 10 year treasuries from 3.745% to 3.337%, before recovering to 3.405% on Friday, Jan 21st.

The Goldilocks Jobs Report

On Jan 6th, 2023 December 2022, Non Farm Payrolls came in with a print of 223,000 net new jobs, which was the smallest gain in about two years. More importantly, hourly earnings rose only 4.6%, Year on Year – the lowest increase since mid 2021 and substantially below its March 2022 peak of 5.6%

Lower Inflation Expectations

The University of Michigan’s consumer survey was also positive for the markets with a lift in the consumer sentiment index to 64.6, 8% higher than December’s 59.7. It was way ahead on estimates of 60.4. Crucially, annual inflation expectations have now come down to only 4% from 4.4% in December. This too was the lowest reading since April 2021.

Somewhat Benign CPI and PPI Readings

On January 12th, The CPI report for December also showed that headline inflation was moderating with a small 0.1% drop from November and 0.3% increase in core inflation. Nothing too exciting, yet reassuring for markets, which saw a peak monthly increase of 1.3% in July, last year.

The root cause for the decline was a massive drop in the gasoline index which fell 9% from November and 1.5% YoY. The annual increase was 7.3%, however that too was taken as benign because it was the smallest annual increase from February of 2021.

However, shelter was the outlier with a monthly rise of 0.8%. It is still showing the lagged effects of the massive pandemic property boom. Unless there are significant drops in the shelter index, the Feds might think it would be too early to slow down rate hikes. I believe that the drop in existing home sales, of 18% YoY, and 5.1% MoM in December, and the lowest annual increase of only 2.3% in existing median home prices suggest that shelter inflation even though lagged is underway. Prices have fallen month over month for six consecutive months now.

In tandem with the CPI reading, the Producer Price Index also showed inflation slowing with a drop of 0.5% in December, which was the largest since the pandemic began. Importantly, the foods gauge receded 1.2% MoM – the largest drop since December 2020. Before we begin to celebrate too much this was still 6.2% higher than the previous year, but thankfully the softest since March 2021.

The New York Fed Consumer Survey added some more fuel to the fire, with median year ahead inflation expectations dropping to 5% and 3 year ahead expectations coming in at only 3%.

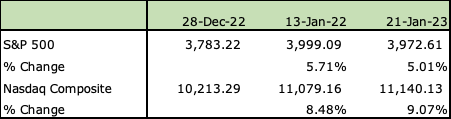

Looking at each economic indicator in isolation, there really wasn’t much to celebrate, but when every indicator beat expectations it resulted in a solid rally of 5% for the S&P 500 (SPX) and 9% for the Nasdaq Composite (COMP.IND).

S&P 500 and The Nasdaq Composite (Seeking Alpha)

No surprise that the interest rate sensitive Nasdaq Composite handily beat the S&P 500 9% to 5%.

The Chinese market reopening also added fuel to the fire. As Chinese authorities finally gave up the much despised, COVID Zero policy and opened up the economy, stocks rallied hoping that Chinese demand would finally resume after almost three years, helping the world economy and removing supply chain bottlenecks as well.

The Impending Recession Narrative

High Reserves Provisioning

Throwing in a spanner to the rally were recessionary indicators, led by bank earnings, with the top four, JPMorgan Chase (JPM), Bank of America (BAC), Citibank (C) and Wells Fargo (WFC) provided a whopping $6.2Bn worth of loan reserves for Q4-2022. JPMorgan alone kept aside $2.6Bn. I don’t believe this is entirely sandbagging – bankers clearly sees risks ahead for inflation stretched borrowers.

Retail Sales Weakness

Retail sales dropped 1.1% in December, the largest decline in a year. Adding insult to injury, the commerce department revised November’s drop lower still.

The rot was across the board – Just three of 13 categories posted an increase, with ex-autos and non store retailers each declining severely at -1.1%, while food services and drinking places fell – 0.9%.

Manufacturing Slump

In tandem with weaker retail sales, according to Fed data, Industrial production dropped 0.7% in December, much higher than consensus and close to the bottom of the range from several economists. This was the third consecutive monthly decline, underscoring how weak the US economy has already turned in the face of demand challenges and higher interest rates in 2022. Could we already be in a recession? ING’s James Knightley thinks so

Coming on the back of such a poor retail sales report, [the production plunge] reinforces the message that recession is on its way and we could in fact already be in it,” he said.

The Weakness in Housing

The drop of 18% in existing home sales and 6 consecutive monthly declines in home prices, underscore that the bubble created from housing demand and high median home prices during the pandemic is finally cracking and is likely to drag down the economy with it.

The slowdown in labor markets

Even as we continued to about 223,000 net new jobs in December, The Wall Street Journal reported that the number of workers out of a job for about 3½ to 6 months has risen sharply since last spring.

In December, 826,000 unemployed workers had been out of a job for about 3½ to 6 months, up from 526,000 in April 2022, according to the Labor Department. Earlier this month, the number of people seeking ongoing unemployment benefits, known as continuing claims, was 26% above half-century lows reached last spring.

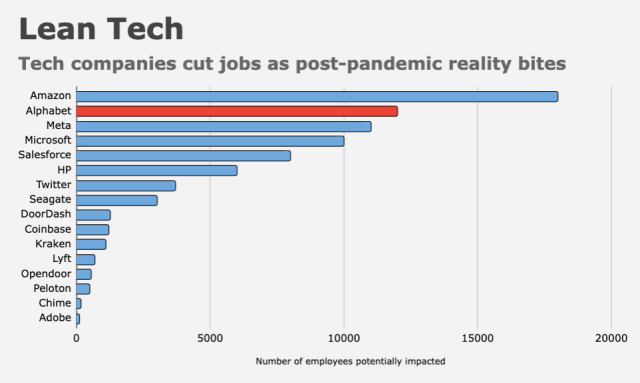

Adding to this weakness, is the large number of high paying tech layoffs as shown the chart below. I expect this number to keep increasing as more bloated tech companies realize that the growth spigot has been turned off.

Tech Industry Layoffs (The Heisenberg Report)

A Likely Earnings Slump

According to FactSet, the S&P 500 Now Projected to Report Year-Over-Year Earnings Declines in Q1 2023 and Q2 2023, analysts are revising earnings down, they expect fourth quarter – 2022 S&P 500 earnings to decline 3.9%. They expect earnings to continue deteriorating further in Q1-2023 and Q2-2023 dropping 0.6% and 0.7% respectively.

According to FactSet, at the individual sector level:

At the sector level, 10 of the 11 sectors have witnessed a decline in estimated earnings for the first half of 2023 since September 30, led by the Consumer Discretionary, Communication Services, and Materials sectors. Overall, six sectors are now projected to report a year-over-year decrease in earnings for the first quarter, and three sectors are predicted to report a year-over-year decrease in earnings for the second quarter. The Materials and Health Care sectors are the only two sectors predicted to report a year-over-year decrease in earnings for both quarters.

Key Takeaways

In my opinion, based on the signals above, recessionary fears should occupy center stage for 2023.

I believe that inflation has peaked and I think a 3.5 to 4% inflation target for 2023 is achievable. Last year I wrote that the Feds will implicitly or explicitly abandon its 2% inflation target. I stand by that. Mohamed-El-Erian certainly thinks so. Chasing wage inflation down and putting people out of work is unlikely to be a Fed strategy as the economy continues to get weaker. And as you can see from the layoffs from the tech sector a lot of wage inflation is likely underway even as we go to print. The tech layoffs confirm my belief that overplaying the need to bring wages down is unnecessary and counterproductive. Widespread falls in retails sales, the manufacturing and housing slumps and the expected earnings decline also should be clear indicators that we should we more worried about a recession than thinking of further interest rate hikes to bludgeon the economy.

JPMorgan Chase, Citicorp, Bank Of America and Wells Fargo are not sandbagging for the most part, customers are stretched when paying double digit increases for groceries.

Chasing the S&P 500 on current momentum and purely on the basis on lower interest rates is not a good strategy. A recession has its own set of problems – think of the jobless recovery after the great financial crash. I’m standing by my estimate of 5% lower earnings of 211 for the S&P 500 for 2023.

Besides the rush to buy because of falling interest rates, I also believe that the current rally can be attributed in part to short covering, new allocations from 2023 cash and FOMO (Fear of Missing Out). At an S&P 500 of almost 4,000 I don’t believe that the markets have priced in a recession.

I also believe that a drop in inflation takes away some of the pricing power from corporates, which will show up in softer earnings in 2023.

Be careful of what you wish for is an article worth reading from Morgan Stanley’s strategist Mike Wilson, who categorically explains why “Bad News Is Bad News”. Lower revenues and severance hits from all the layoffs will end up compressing margins, which does not bode well for corporate earnings in 2023.

As we saw from the CPI, the Michigan sentiment, the non farm payrolls and the producer price indices, month on month inflation prints are receding compared to 2022. This bolsters the case for peak inflation. For example, 0.3% monthly increases equate to 3.67% per year. As long as CPI increases stay below 0.3% or 0.35% consistently per month, inflation will not top 4% on an annualized basis.

However, inflation can rear its ugly head again if Chinese demand for oil sends gas prices soaring again. Remember, a vast majority of inflation expectations and cost pass throughs are oil related .

I don’t believe that the recession is going to be severe or long. The massive Fed Fund hikes in 2022 from 0-0.25% to 4.25% to 4.5% were a one-off high impact event. I expect the Fed to add at the most, 2 hikes of 0.5% or spread it over longer with smaller 0.25% hikes in the first half of 2023. And as I stated in this article last December, the Fed has succeeded in bursting the stock market bubble, brought down prices and started containing the housing bubble with its actions. The ensuing layoffs further indicate that the harsh medicine is working. Goldman Sachs is one of the few who actually have a low estimate (only 35%) for a recession in 2023 – Why the US Can Avoid a Recession in 2023. Their reasoning is plausible, given such a massive shock, much of it has already affected the economy, therefore making it unlikely that its recessionary impact would be deep or long.

From the Goldman Sachs article:

Part of our disagreement with consensus arises from our more optimistic view on whether a recession is necessary to tame inflation. We think that a continued period of below-potential growth can gradually rebalance supply and demand in the labor market and dampen wage and price pressures with a much more limited increase in the unemployment rate than historical relationships would suggest. Additionally, while the Fed tightened financial conditions substantially last year, the impact on GDP growth is likely to diminish this year. Like other macro models, our analysis shows that the peak impact of rate hikes on GDP growth is front-loaded. In other words, the drag on U.S. GDP growth from recent aggressive Federal Reserve policy will fade as 2023 progresses.

Investing in 2023

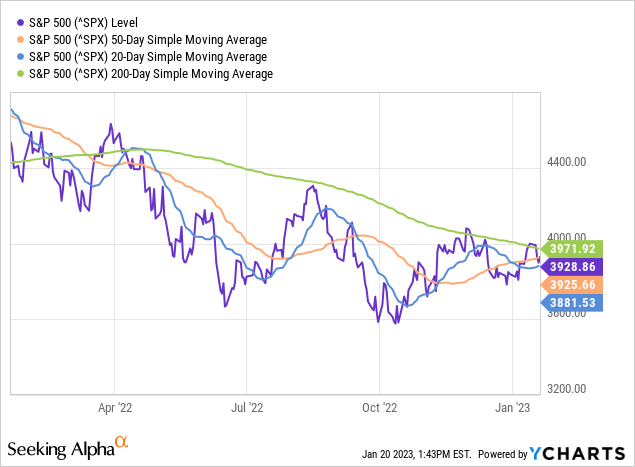

The markets have turned back after flirting with the 200 DMA – this is the third such resistance in the bear market, which has crossed a year.

Even if we cross the 200DMA, I am going to remain cautious and still keep about 15% in cash, because I believe that Q1 and Q2 earnings will be the real test for the market – I’m maintaining we can still test the 3,600 S&P support levels from where the S&P 500 rebounded twice in 2022.

I am going to invest more in Nasdaq growth and tech stocks for two reasons.

a) In a lower interest rate scenario, tech and growth stock multiples will increase. When the 10-year stays at 3.4%, it does give you a few extra multiple points or higher P/Es as compared to the 4.5.% high of last year.

b) There are far more bargains in the Nasdaq, which is still lower than its all-time high of 16,057 by about 30%.

Tech stocks with more secular growth stories have more long term upside in a recessionary scenario, as compared to cyclicals who will struggle more with lower pricing and margin compression.

I’m likely to get a much bigger bang for the buck from the Nasdaq and tech stocks and even though some have recovered from their lows, many are 60-80% below their all-time highs.

Be the first to comment