Dilok Klaisataporn

Introduction.

This article clarifies my position on NMS reform, as laid out in the previous post. Specifically, I believe the ideal NMS would include many facets of financial futures technology but would compete with both the current futures markets and securities markets. A better structure unites the two technologies to create a third market structure.

The article focuses on two major differences between my Simple Market structure (SMS), the current NMS, and the SEC’s proposed reform (characterized by Larry Tabb.)

- First, to assure investors are not trapped into paying a monopoly or regulation-induced premium that exceeds the resource cost of the SMS, the structure of governance of the SMS would be owned by its investors (ala Vanguard),

- Second, to avoid one critical flaw of both the current and SEC-proposed NMS, the SMS will be separated from the other two significant market structures, just as financial futures are separated from the NMS today. That way, investors that don’t use SMS will not bear its costs. A major failing of the NMS is that investors don’t choose any aspect of their trade execution other than their retail broker.

Dispute with Tabb

I realized when I read Larry Tabb’s response to my most recent article that my position concerning the use of futures market technology could easily be misinterpreted. I nonetheless suspect that after clarification, Tabb and I will continue to differ sharply about the desirability of various practices of the futures markets. (See my most recent article and Tabb’s comment.) Tabb is dismissive about the possible value to retail investors of adopting practices of the futures markets. In the interest of advancing the market structure discussion, this article attempts to clarify my pro-futures-tech position.

A different measure of market structure cost

My perspective on cost-benefit analysis is always based on resource costs, not prices charged to customers. My reasoning is that monopoly and restraint of trade issues (or any market condition where prices are based on something other than resource cost) are not a result of trading technology, but of a poorly conceived structure of marketplace ownership.

If you view, as I do, market structure as an external cost borne by market users without the kind of within-agreement choice that life insurance customers, for example, have – it makes sense to deny market providers access to the profits they might generate over costs.

Thus, my analysis focuses on the resource costs of markets, much easier to measure than the price a competitive provider would charge. I am no fan of the publicly held ownership of exchanges these days.

It is my focus on resource cost and Tabb’s focus on market prices that explains, I believe, some of our difference of opinion. First a description of futures market strengths and weaknesses, from a resource cost perspective.

Futures’ strengths and weaknesses

There are some good things and some bad things about futures market technology.

First the bad things. The bad things, critically, are not properties of futures market technology. They are properties of CME implementation of futures technology.

- The CME is a monopoly. That’s bad. How did CME become a monopoly?

- The economics of trading, always and everywhere, drives transactions into a single location in time and space, if not interfered with. That is, the central limit order book (CLOB) is an economic-efficiency-driven structure, not a regulatory structure. Futures and securities trading in unfettered competition is always going to produce a single dominant market.

- Because it is a publicly traded firm, the CME exists to return a profit to its shareholders. As the market theory promises, the price of trading will exceed its cost in a monopoly such as CME Group. Not good.

- Second, the CME has unwisely limited itself to futures trading. The traded instruments of futures markets are contracts based upon a spot market security (or commodity). Futures-only exchanges are never going to provide users with the most efficient use of their capital because the result of the futures-spot market split is two markets for a single risk. This splits liquidity that could be centralized in a single market. The absence of joint futures/spot market trading also leads to inconsistencies between futures and related spot markets that detract from the contribution to the markets of both.

- Third, other features of CME/ICE futures markets are anachronistic. For example, CME/ICE futures contracts typically trade a futures contract that delivers once every quarter – typically the March cycle (March, June, September, December). This cycle coincides roughly with the crop cycle. Crop cycle delivery makes perfect sense in the commodities markets traded before the introduction of financial futures (the early 1970s). But not so much for the financial futures markets.

Now the good things. The good things about futures are a result of the technology that all the futures markets exhibit.

- First the futures-style clearinghouse. Futures were designed by grain traders, chronically thinly capitalized relative to the capital absorbed by the huge American markets for grains. This led them to design their markets to economize on the capital needed to stabilize trading – hence the innovation of the futures-style clearinghouse where the exchange becomes a party to each trade, a seller to every buyer, a buyer to every seller.

- Second, price-risk-related margins. The less regulation-bound futures markets are not stuck with securities exchanges’ Reg Q-determined, volatility-independent margins. Market-determined margins are at once safer and more customer-friendly.

- Third, one-step clearing. The infrequent exchange of ownership between seller and buyer in futures markets does wonders for the cost of clearing. Only a fraction of 1% of transactions ever includes a transfer of ownership.

Tabb’s case against the futures market model of trading

- Tabb rightly catches the ridiculously excessive profitability of futures markets today. There was a time in my memory when the CME stopped charging a transaction fee altogether around June. Even then the exchange budget was inflated. But futures exchanges are not inevitably a monopoly. The absence of inter-exchange competition for markets is a failure of the imagination of the collective marketplace. Multiple futures exchanges for one single spot security sometimes happen briefly in the presence of fluid trading technology. As Tabb pointed out, each contract is constrained by the need to pass through the clearinghouse of a single exchange. But there are opportunities for inter-exchange competition. (Interexchange competition for the gold futures market continued for more than a decade until CME bought COMEX.)

- Futures customers suffer from monopoly pricing. Monopoly pricing in any competitive environment including securities trading is inevitable but not necessarily a bad thing. It is a bad thing only if customers are adversely affected. An exchange owned by its customers would be on one hand less likely to charge a monopoly price for its services. On the other, whatever the level of prices, customers would receive any excess payments over resource costs through marketplace ownership.

- Tabb also rightly points out that the market is also dependent on CME/ICE to make market structure changes. There will be other sources of change – surely Leo Melamed cannot be the last person to ever innovate market structure – but they will be no doubt infrequent.

- I differ with Tabb about whether securities markets are cheaper than futures, but that is because Tabb looks at customer price and I look at resource costs. I doubt that Tabb would disagree that futures resource costs are less than the cost of securities markets’ legion of transaction engines.

- Optimality of CLOB is also an unresolved dispute. Tabb asks rhetorically “Should the most sophisticated trader get the same price as me? The sophisticated trader has a whole team on their side, they get the best research, hire specific traders, and get the best support. Why shouldn’t my 100-share order get a better price than 100 shares from a large money manager with 99,900 shares behind it?” I don’t get this Tabb query. The “sophisticated trader” pays for its team. If shares were coffee beans, would Tabb argue that I should pay less for my retail bag of coffee beans than Starbucks pays for its bag of beans?

- Finally, “Complexity isn’t always the enemy” claims Tabb. But in comparing the many stock exchanges and AFTs that process shares to the two transaction engines that process futures contracts, complexity is most certainly a major enemy. Outrageously, the SEC wants to introduce yet another market into the already too-complicated NMS. Indeed, futures are too complicated too. They only appear simple by comparison to the NMS.

A better market structure

Our current market structure, with or without the SEC’s proposed changes, inevitably creates an exchange monopoly – or worse, the government-regulation-induced mob of false competitors we call the NMS. A broader change in our current market structure that truly puts retail investors in the driver’s seat would give investors:

· An option to govern

Put customers in charge of both the provision of market services and the choice of providers. Our current structure denies customers a vote on their preferred market structure. Instead, their brokers choose their market structure for them. That is an obvious flaw.

-

An option to control the entire market structure – all investment fees and services

More than modifying or adjusting securities or futures markets, I believe that given an alternative that combines the two markets, both financial futures and securities markets would be reduced to irrelevance. Modification of the securities themselves to better meet investor needs, rather than focusing solely on the needs of issuers would make any exchange a stronger competitor than the current market providers.

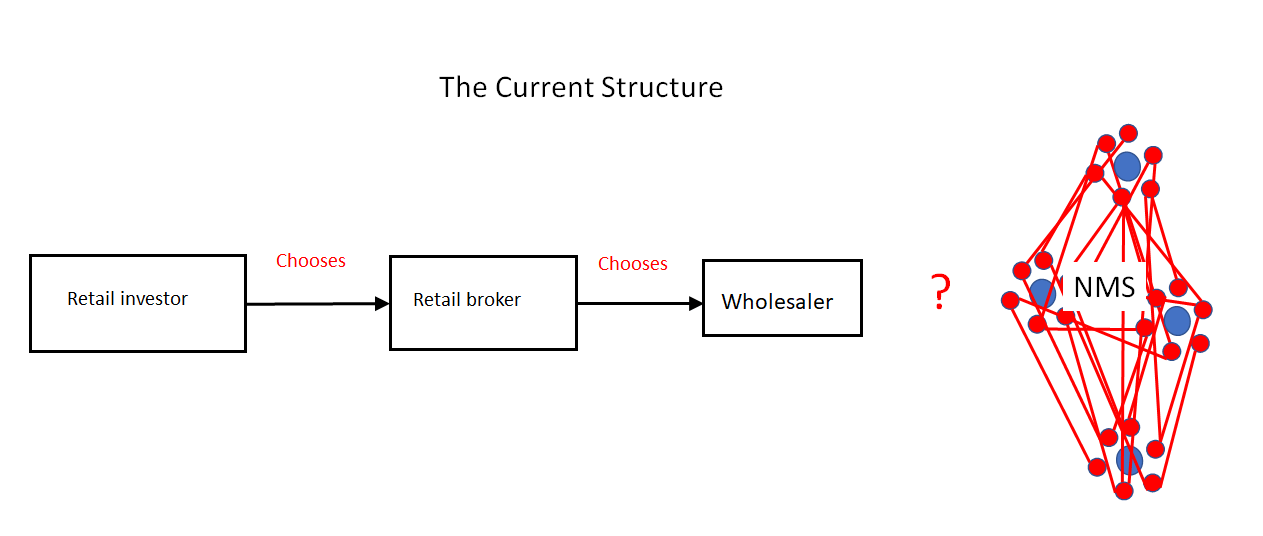

The graphic below displays the current horizontal NMS market structure. The retail investor has no control over the transaction engine used in the futures market or the securities market. The menu of investment choices is also determined jointly by exchanges and issuers, not investors.

The current market structure (Author)

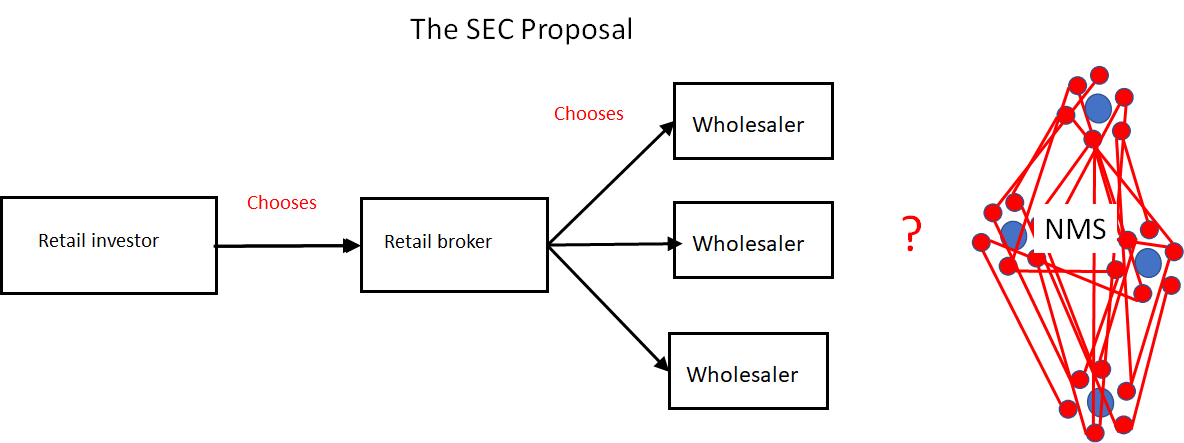

The next graphic shows the SEC’s alteration, giving retail brokers a choice of wholesalers in an auction. This second separate transaction that affects the cost of every retail trade can only increase the resource costs of retail investors.

The SEC proposal (Author)

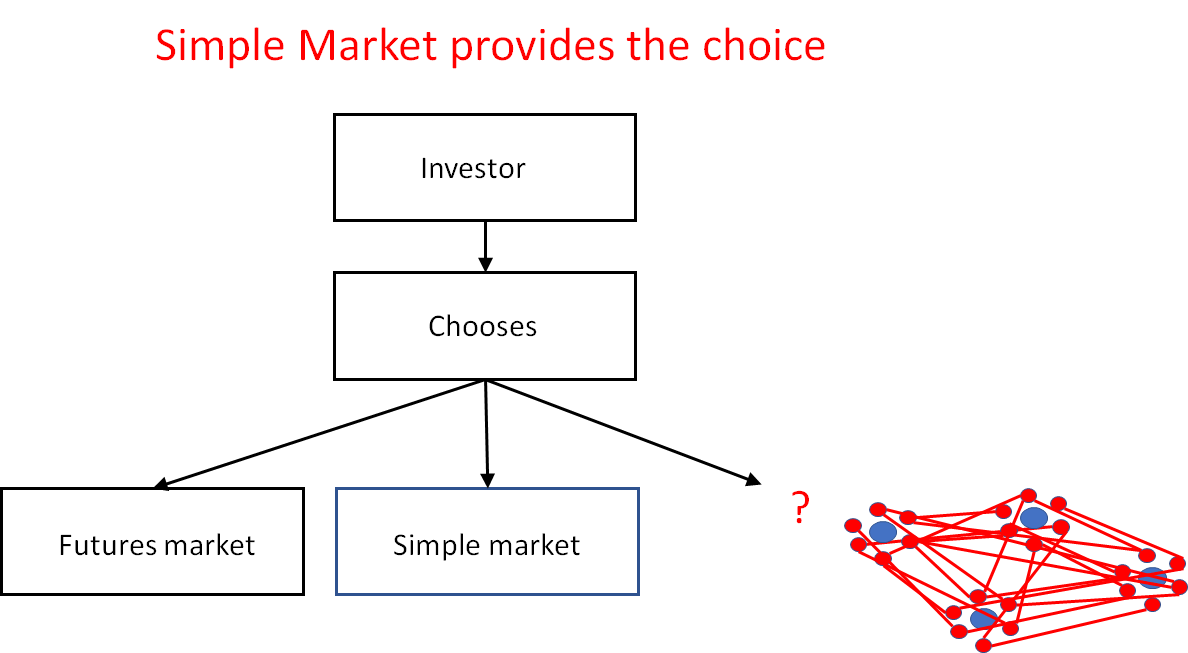

The final graph shows a proposed vertical market structure. The message here is that investors do not bear the cost of all parts of this structure. The investor pays only for their choice. Investors also control every facet of the costs and services provided if they choose one of the proposed structures. Moreover, in the SMS, the investor governs the structure itself and can influence the instruments available for investment.

The Simple Market Structure (Author)

Conclusion

This article is intended to clarify my proposed Simple Market Structure. It points out that I advocate some, but certainly not all the futures market structure. I view the most important aspect of the proposed SMS as the possibility that retail investors can control every aspect of their investment process, including a part in the design of the instruments they trade. Financial instruments that fail to meet the needs of investors are among the most significant failures of the NMS and futures.

Be the first to comment