HJBC

Today it is Société Générale Société anonyme time (OTCPK:SCGLF, OTCPK:SCGLY) (“SocGen”). The company just released its Q4 and Fiscal Year 2022 results, beating equity research analysts on net income profits and announcing a €440 million buyback. Before analyzing SocGen accounts, we would like to reiterate our buy rating target based on: 1) a compelling valuation with a good stock price entry point based on its Tangible Book Value; 2) a strategic plan with expected savings; 3) a sufficient capital buffer to sustain the “Russian loss”; and 4) ALD investment case included in Mare Evidence Lab’s Sum-of-the-Part valuation.

Starting the latter buy case point, here at the Lab, we are long-term investors in ALD. This was mainly due to the following:

Leasing/long-term renting for both B2B and B2C is growing at a higher rate than the auto production

A progressive EV fleet means fewer maintenance costs and a higher margin for the future

ALD debt is backed by car fleet residual value. Used cars are much more expensive right now and we see this trend as being priced in by the market.

We recommend to our new readers check up on our previous articles so that they are well acquainted with the story up to now:

- BNP Paribas with Arval

- SocGen: We Reiterate Our Buy Rating.

In conjunction with SocGen, ALD also posted its results early this morning.

ALD financials in a Snap

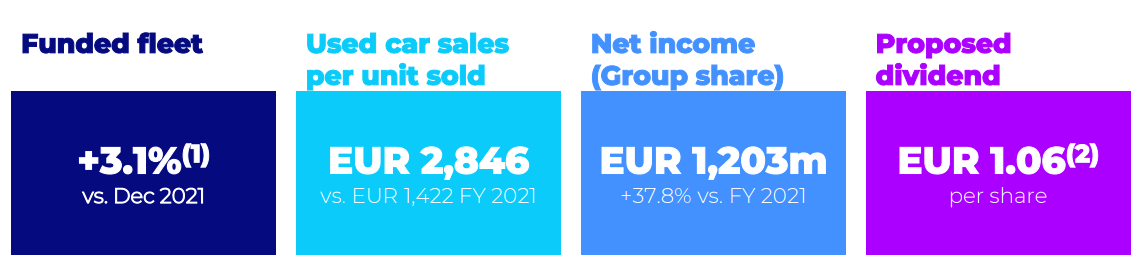

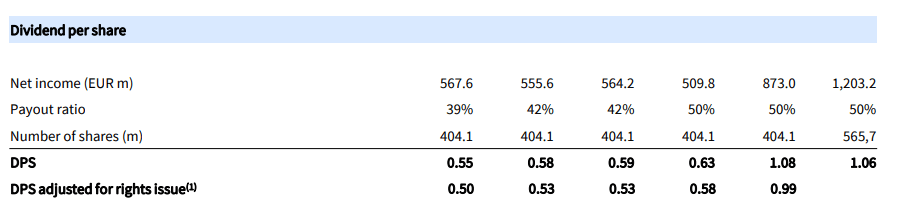

Aside from the financial considerations, ALD fleet management contracts were up by 14.6%, and this was supported by the latest LeasePlan acquisition. The company’s order book remains at a high level, confirming our thesis on B2B and B2B market. To support our buy recommendation, the company is ahead in EV penetration, and more important to note is the fact that the Used Car contribution delivered exceptionally high results from €437.7 million to €747.6 on a yearly comparison. In addition, reporting the management’s comment “this favorable supply/demand situation is expected to remain in place also in 2023.” Looking at the P&L aggregate level, the cost/income ratio was at 46.9% while the cost of risks remained at a very low level of 20 basis points. With ALD’s operating leverage, EPS then increased by 35% compared to the 2021 results. If approved, ALD is planning to pay a dividend per share of €1.06 with a current yield of 8.55%.

ALD dividend per share evolution

SocGen Q4 and FY Results

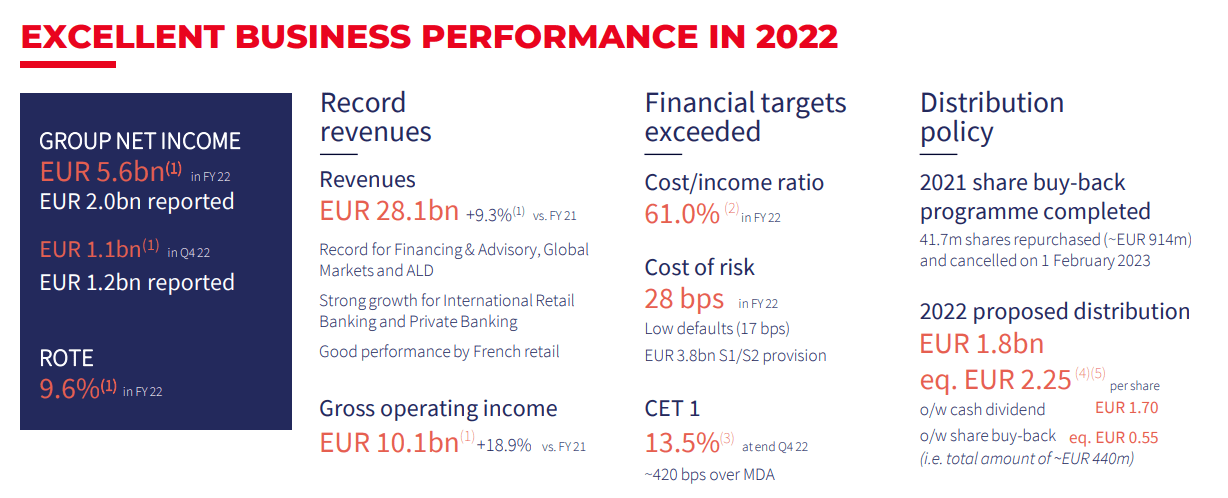

In Q4, France’s third-largest bank SocGen reported a profit of €1.16 billion, exceeding analyst consensus forecasts of €834 million thanks to strong performance in its corporate and investment banking division. However, it was down 35% compared to last year’s end-quarter results as the bank increased provisions for non-performing loans, which in an uncertain economic environment grew almost five-fold to $413 million. In addition, the bank’s margin improved by 4% to 6.89 billion thanks to higher trading revenues beating the consensus estimate at €6.42 billion.

Aside from the strong ALD financial performance, the result was driven by the global markets and leasing division as well as the growth of its private banking and international retail banking businesses. This is not coming as a surprise, here at the Lab, in our EU baking universe coverage, we said that global banking and international retail activities were particularly boosted by the rise in interest rates.

SocGen financials in a Snap

Conclusion and Valuation

SocGen’s CET1 ratio stood at a solid 13.5%, confirming its ECB capital requirements. For this reason, the French bank proposed a cash dividend of €1.70 per share and reaffirmed its financial objectives for 2025, which include a cost/income ratio of less than 62% and a return on tangible equity of 10%. Furthermore, this year the company planned a share buyback for €440 million, which is worth approximately €0.55 per share.

The new CEO was the key person in promoting the alliance with the U.S. wealth manager AllianceBernstein Holding for equity trading and research. This reorganization was rewarded by the market, indeed, in the last three months, SocGen stock price was up by 17.6% on the Paris Stock Exchange. As a reminder, last year, BNP Paribas bought the remaining 50% stake in a research firm called Exane and is now working to expand its business in the United States. Similarly, the joint venture with AllianceBernstein should expand SocGen’s presence in the U.S.

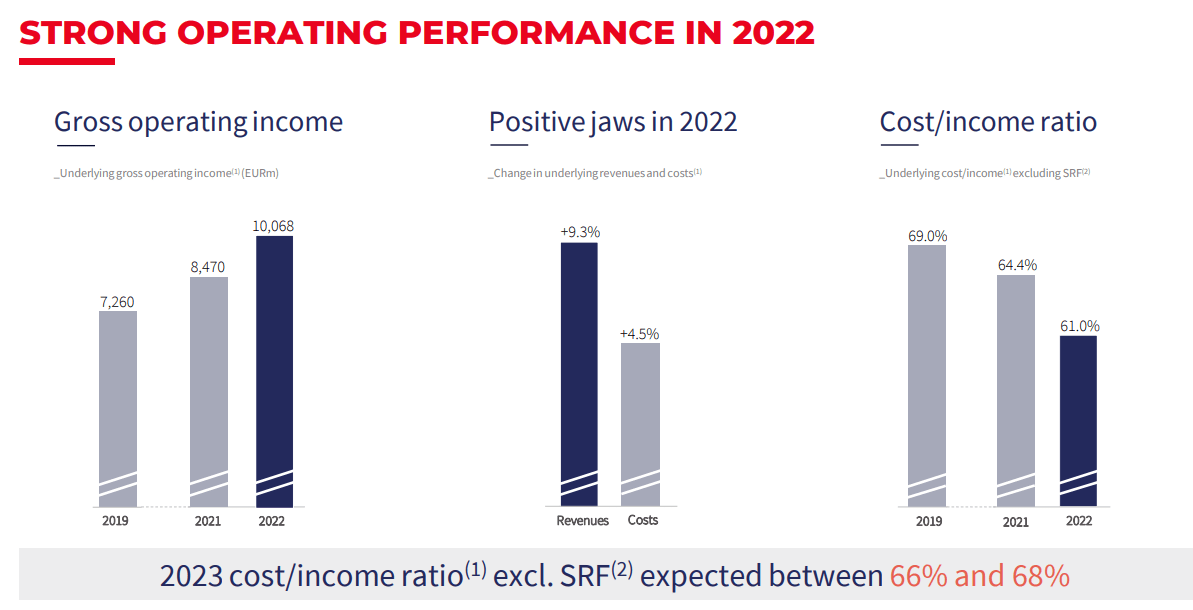

In our buy recap, the SocGen cost/income ratio is in line with the indications, so we decide to leave unchanged our forecast, and its Russian exposure was down by almost 45%. Regarding our valuation, SocGen is still trading at a Price-to-Tangible-Book of 0.38x versus its historical average of 0.53x, so we confirm our buy rating target at €30 per share.

SocGen cost/income ratio evolution

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment