sefa ozel/E+ via Getty Images

“Without deviation from the norm, progress is not possible.”― Frank Zappa

In today’s feature article, we take our first look at Phathom Pharmaceuticals (NASDAQ:PHAT). This clinical stage biotech concern popped up on our radar screens thanks to some insider buying in its shares in May. An analysis follows below.

Seeking Alpha

Company Overview

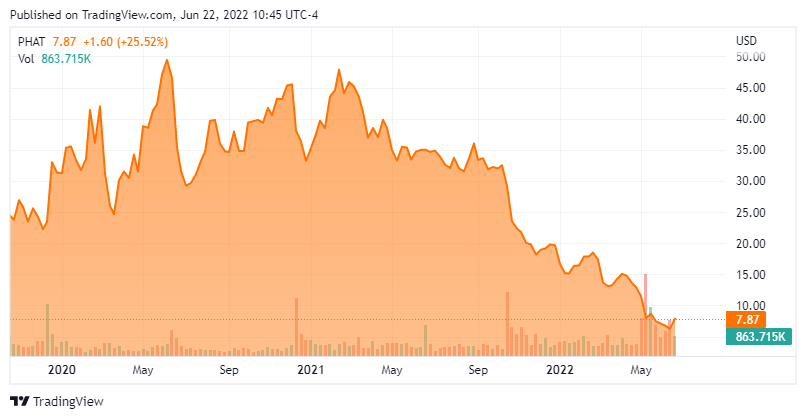

Phathom Pharmaceuticals is based just outside of New York City. The company is focused on developing and commercializing treatments for gastrointestinal diseases. The stock trades right at eight bucks a share and has an approximate $240 million market capitalization.

Company Website

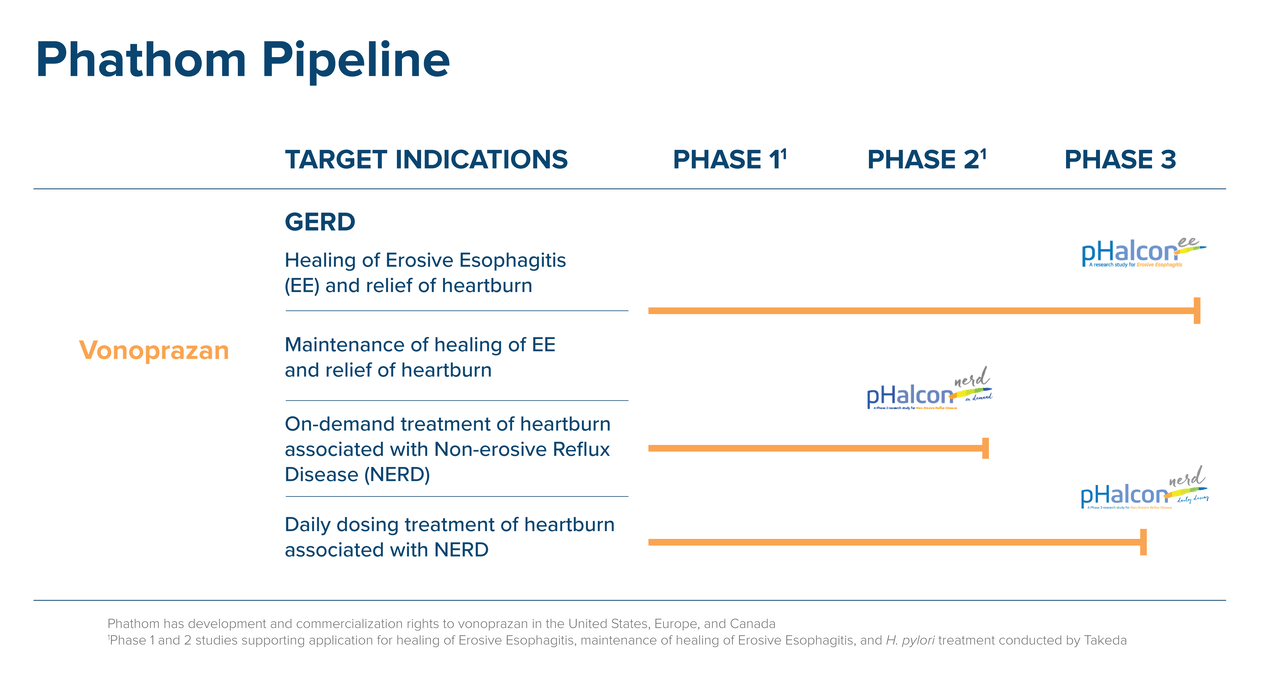

The company’s main asset is a compound called vonoprazan. Three years ago, Phathom acquired the license for the development and exclusive rights to commercialize vonoprazan in the US, Europe and Canada from Japanese drug giant Takeda (TAK). Phathom has made some good progress on the development of this drug which we will cover in the paragraphs below. There are no regulatory milestones as part of this agreement but milestone payouts and royalties on net sales. Vonoprazan is a first-in-class potassium-competitive acid blocker medication that was first approved in Japan early in 2015. Takeda Pharmaceutical’s Takecab (vonoprazan) was the top-selling drug in Japan in December of last year, according to a monthly snapshot report released by Encise. Annual sales were just north of $700 million in Japan for 2021.

Recent Developments:

On May 10th, the company posted first quarter results. Phathom has a GAAP loss of $1.07 a share, about a dime a share worse than expectations.

One week earlier, Phathom received FDA approval for its VOQUEZNA TRIPLE PAK (vonoprazan, amoxicillin, clarithromycin) and VOQUEZNA DUAL PAK (vonoprazan, amoxicillin) for the treatment of Helicobacter pylori (H. pylori) infection in adults. Commercial launch for this indication is expected in the third quarter.

At the end of May, Phathom reported the government agency had also accepted its marketing application seeking approval of vonoprazan to treat adults with erosive esophagitis or EE after a successful Phase 3 study.

Company Website

Vonoprazan is also in development for non-erosive gastroesophageal reflux disease or NERD. The company commenced a Phase 3 NERD development program in the first quarter of 2022. Topline results from this study are expected in 2023.

Analyst Commentary & Balance Sheet

The analyst community has soured on Phathom’s prospects somewhat since early May. Over that time, Evercore ISA downgraded the shares to Market Neutral from Outperform while Goldman Sachs reissued its Hold rating with a $15 price target. Needham did reiterate its Buy rating and $44 price target and Guggenheim maintained its own Buy rating but did reduce its price target to $42 from $48 previously.

Just under 17% of the outstanding shares are currently held short. In mid-May, three insiders collectively bought just over $450,000 worth of shares. These were the first insider purchases in these shares since October of 2019. The company ended the first quarter with nearly $140 million of cash and marketable securities on the balance sheet after posting a net loss of $40.7 million. The company also has an additional $150 million in liquidity for which Phathom is eligible to receive. This consists of $100 million in proceeds from the revenue interest financing agreement announced on May 4, 2022. This agreement provided for an upfront $100 million cash payment and an additional $160 million cash payment upon FDA approval of vonoprazan for treatment of erosive esophagitis. The company also has $50 million from its term loan with Hercules Capital that became available upon the recent acceptance by the FDA of the company’s marketing application for vonoprazan to treat EE.

Verdict

The current analyst consensus has the company losing just over four bucks a shares in FY2022 on roughly $8 million in revenues. For FY2023, analysts project sales to soar within a wide range ($54 million to $149 million) with approximately the same per share loss.

Longer term, there seems a lot of potential here as the company rolls out vonoprazan for the first of hopefully three potential approved indications over the next few years. If the company can achieve sales commensurate to what Takecab is achieving over time in Japan, the shares look undervalued.

The question is how fast can the company achieve significant sales traction and lessen quarterly cash burn. Recent financing has been acquired to facilitate this rollout and insiders seem to be giving the stock a vote of confidence by buying shares. However, given how many small cap biopharma companies have botched initial rollouts in the pandemic age, I am always skeptical at this stage of commercialization. For now PHAT merits a very small ‘watch item‘ position and this is a story we will circle back on in 2023 to assess how the rollout is proceeding.

“The reasonable man adapts himself to the world: the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man.” ― George Bernard Shaw

Be the first to comment