Byrdyak

All it took was one data point, and now the market is suddenly not only seeing things the way Powell sees them but is now pricing in the potential for more than two more rate hikes in 2023.

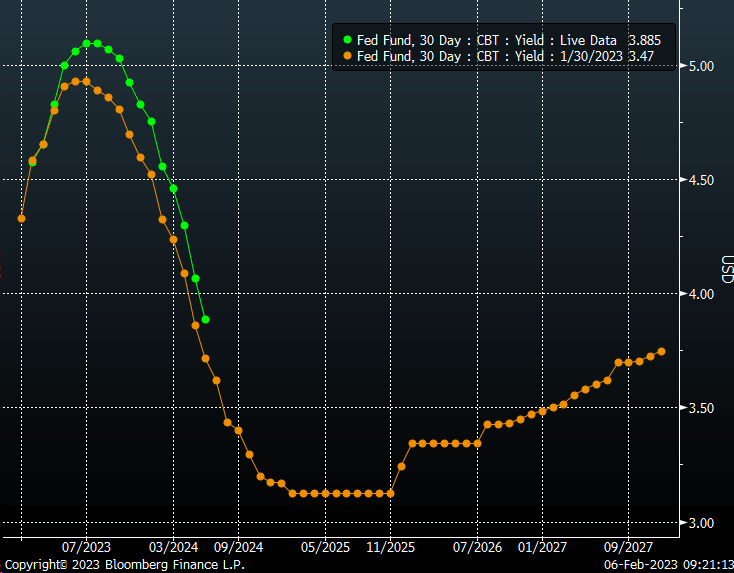

Fed Funds Futures have surged higher since the Job report on Friday. The curve now illustrates a terminal rate of 5.1% by July, but more importantly, the market now sees rates at 4.83% by December, up from 4.6% just a week ago.

Bloomberg

Additionally, the market isn’t done because it also sees the odds of potentially more than two more rate hikes in 2023, with the odds for a third rate hike in June now creeping higher. While the odds are still low, this is a significant reversal in market psychology and needs to be watched as data continues to roll out.

Bloomberg

These higher rate expectations result in the entire nominal yield curve shifting, with the 2-year rate now trading at 4.43% and up around 20 bps since last week.

Bloomberg

The problem is that the higher the expectation is for the Fed to raise rates, the higher the 2-year rate will increase. The 2-year nominal rate is now trading 40 bps below the December 2023 Fed Funds futures, a level it hasn’t traded at since June 2022. That spread should probably rise, with the 2-year nominal rate increasing to the December Fed Funds Future rate.

Bloomberg

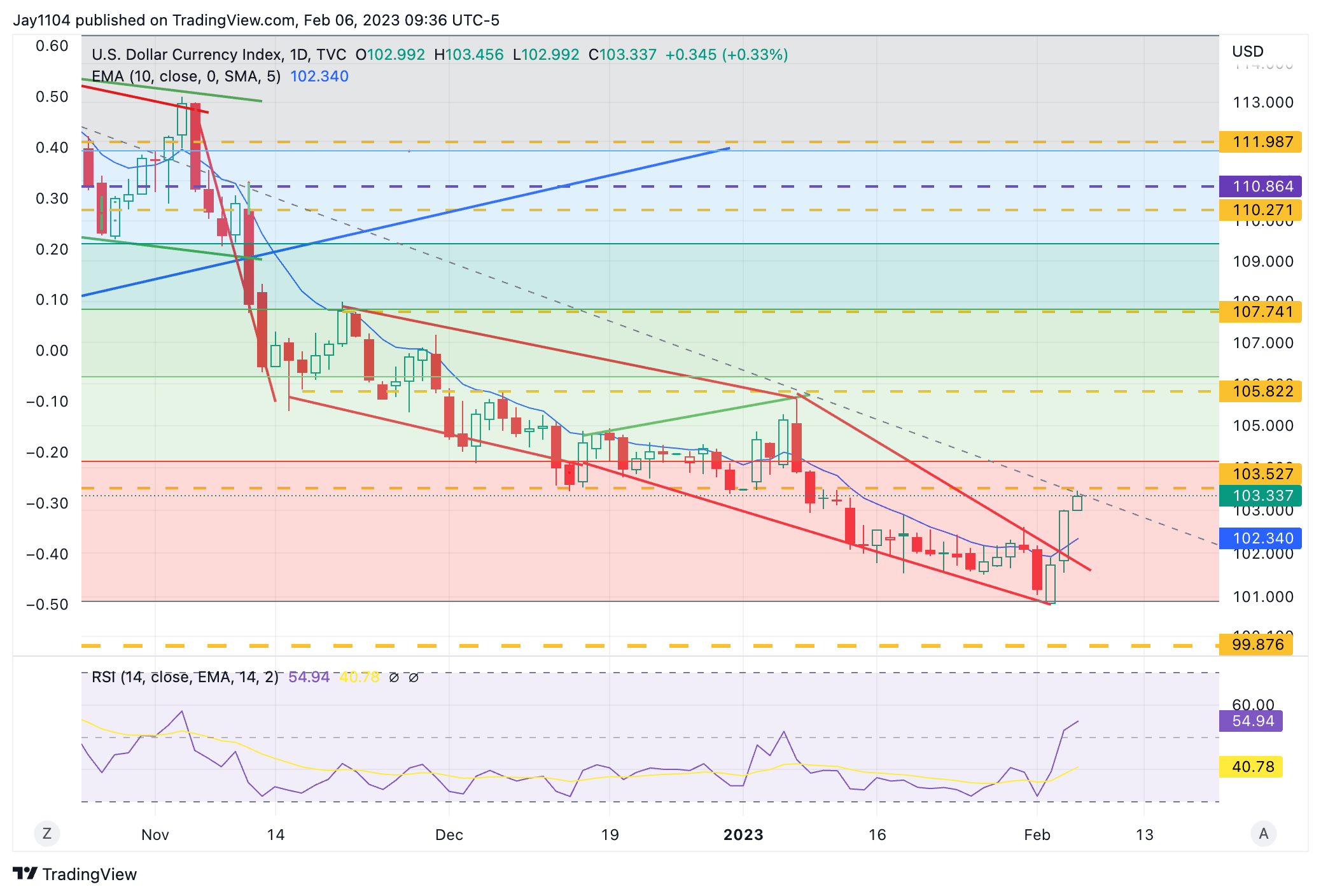

The higher rates climb, the more likely the dollar index continues to rise; it appears to be breaking out following the more robust data and the massive repricing in the expected path of monetary policy.

Trading View

Higher rates and a strong dollar should result in financial conditions beginning to tighten, which will be a killer for an S&P 500 that has seen its liquidity sucked out of it as the Treasury General Account has risen and reverse repo activity has been stable. The Fed continues to reduce the size of its balance sheet.

Bloomberg

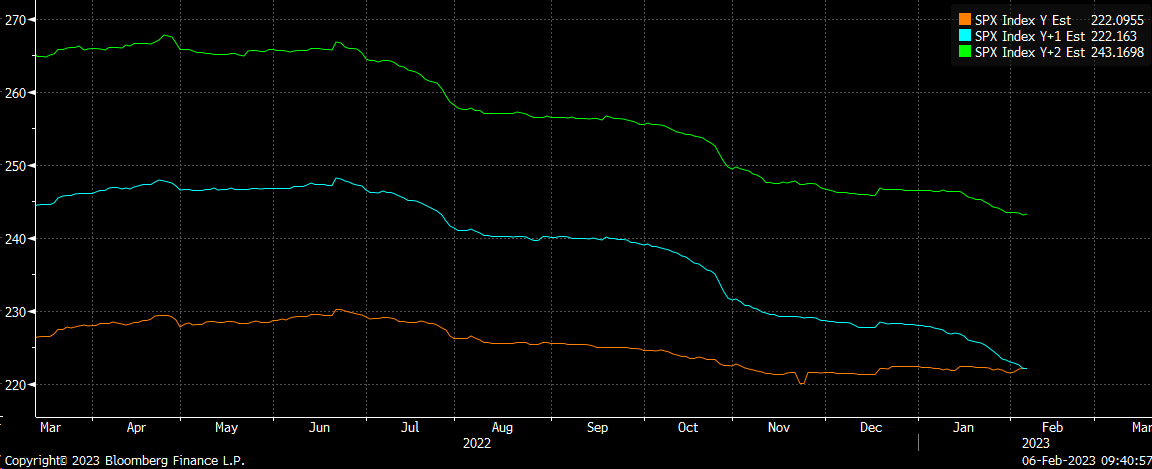

Additionally, the S&P 500 is estimated to have no earnings growth in 2023 compared to 2022. Still, investors pay roughly 18.5 times 2023 earnings estimates in the face of tightening financial conditions and liquidity sufficiently drained from markets.

Bloomberg

As long as the economic data remains healthy, it will only suggest that rates go higher and that not only will there be no rate cuts in 2023 but that the Fed may have to push rates beyond their 2023 forecast of 5.1%. That will make next week’s CPI report even more critical than just a week ago.

Currently, the estimates for that CPI report suggest an uptick in CPI month-over-month, rising by 0.5% from a decline of 0.1% in December, and CPI rising by 6.2% year-over-year down just slightly from 6.5% in December. A hotter-than-expected reading in CPI would mean game over for the January bull market hopefuls and that the Fed may not be finished raising rates once it reaches its 5.1% target.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Join Reading The Markets Risk-Free With A Two-Week Trial!

(*The Free Trial offer is not available in the App store)

Find out why Reading The Markets was one of the fastest-growing SA marketplace services in 2022. Try it for free.

Reading the Markets helps readers cut through all the noise by delivering stock ideas and market updates, and if you want to learn how and why markets behave the way they do, this is the place.

Be the first to comment