Justin Sullivan

Meta Platforms (NASDAQ:META) successful performance in Q4 shows that talks about the decline in popularity of Facebook and Instagram were way too premature given the fact that Mark Zuckerberg noted during the latest conference call that the number of people that use the company’s family of apps is the highest it’s ever been. At the same time, the improvement of the company’s financials coupled with the growth of Reels and WhatsApp gives even more reasons for optimism as it seems that Meta would be able to keep its momentum for the rest of 2023 which could lead to further creation of additional shareholder value along the way.

Proving Doubters Wrong

A year ago, there was this misconception about the decline in popularity of Meta’s main apps such as Facebook and Instagram as the company reported its first decline in active users. However, shortly after the business managed to recover as the recent earnings results for Q4 that were released a few days ago showed that the number of people that use Meta’s apps is the highest it’s ever been.

During the quarter, Meta recorded a total of 2.96 billion daily active people and 3.74 billion monthly active people across all of its apps which indicates that the decline that was experienced a year ago by the company was just a temporary setback that it was able to overcome. Add to this the fact that Meta managed to beat the street estimates for Q4 despite major headwinds while its peers such as Google (GOOG)(GOOGL) and Snap (SNAP) disappointed the street, and it becomes obvious that Meta’s strong portfolio of products and services is likely to remain popular across a big part of the global population in the future.

What’s also important to mention is that Meta has also managed to address the exuberant spending issue for which it was criticized by a lot of shareholders in recent months and announced a forecasted decrease in total expenses and capital expenditures this year thanks to various optimization efforts.

As such, it’s now time to update the company’s DCF model to see whether it makes sense to add Meta’s stock to the portfolio after the aggressive rally of its stock that was caused by the great performance in Q4.

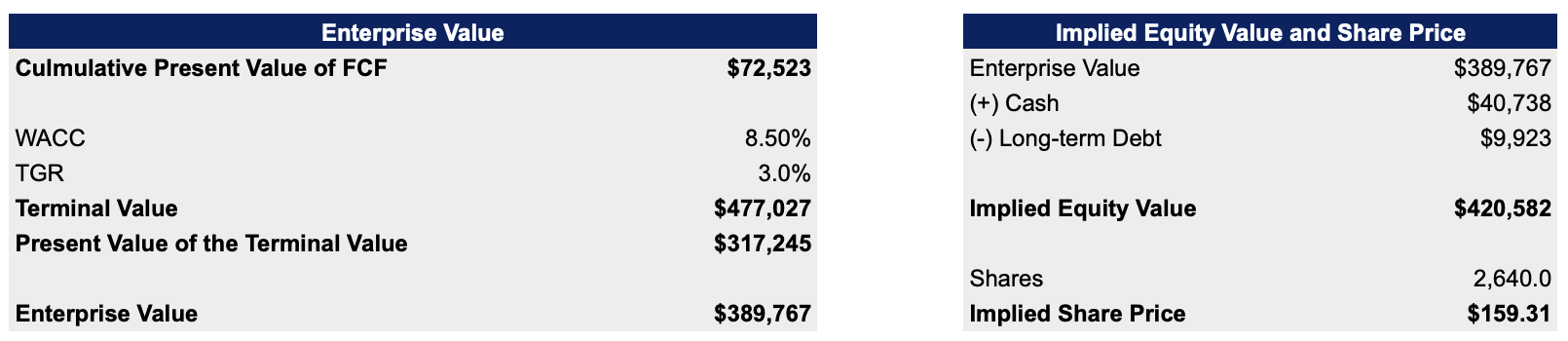

In recent months I’ve already made two DCF models which showed Meta’s fair value to be $161.37 per share and $196.89 per share in the base case and an optimistic case, respectively.

In this new updated model, the top-line assumptions for the next three years are mostly in-line with the street estimates after which the growth stabilizes by around 10%. EBIT as a percentage of revenue remains to be the average of the previous three years. The effective tax rate is increased to 20% and is mostly in line with the management estimates which predict the rate to be in the low 20s. The D&A as a percentage of revenue is the average of the previous three years, the change in net working capital stands at 1% of revenues for the following years and CapEx is also mostly in-line with the management predictions for 2023 after which it gradually decreases. The WACC of 8.5% and the terminal growth rate of 3% are the same as they were in my previous models.

Meta’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

This model shows Meta’s enterprise value to be $390 billion while its fair value is $159.31 per share, below the current price of ~$190 per share.

Meta’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

This updated model mostly shows a similar fair value as in the base case before even with several tweaks, but it doesn’t mean that the stock will depreciate to such levels. While an increase in a tax rate along with a slight decrease in EBIT from before negatively affected the fair value in this model, a potential improvement of the top-line performance alone could easily lead to the upward revision of assumptions and a subsequent improvement of the valuation. The future top-line growth rate is already relatively depressed in comparison to historical periods and given the fact that Meta has several growth catalysts up its sleeves, there’s a case to be made that the company could outperform those assumptions and make the street improve its outlook for the following years as well.

The Growth Is Far From Over

While at first, it might seem that there’s no upside in Meta’s stock after the recent appreciation, I still decided not to close my position in the company as there are several growth catalysts that could help the business to outperform the expectations and assumptions in the model which could lead to a higher valuation.

First of all, while an annual decline in revenues in 2022 due to the change of Apple’s privacy policy coupled with the worsening macroeconomic environment is one of the biggest negatives for Meta last year, the company’s recent investments into the improvement of its algorithms by expanding its AI capabilities could offset Apple-related losses.

During the latest conference call, Mark Zuckerberg has been mentioning how investments in new AI tools could help the company to improve its performance and help advertisers grow their businesses. He stated that in Q4 advertisers saw over 20% more conversions in comparison to the year ago thanks to Meta’s investment in the expansion of its AI capabilities. As a digital advertiser myself, I can say that the ROAS on my ads for my export-oriented side business has been improving in recent months when running ads on Instagram in comparison to even a year ago when the change of Apple’s privacy policy made it unprofitable to use Meta’s advertising tools.

Add to this the fact that the management along with the street expect growth in 2023 even though we could be on a brink of a recession indicates that Meta has all the chances to recoup its 2022 losses and create additional value thanks to the strength of its portfolio of social media products.

At the same time, both Reels and messaging ads continue to outperform expectations which shows that Meta has all the chances to establish a greater presence in the short-form video and messaging fields that could lead to the ability to generate additional several billions of revenue.

Considering all of this, it’s safe to say that Meta’s growth story is far from over and I’m even more optimistic now about its future as the successful monetization of new products coupled with cost optimizations and the improvement of the company’s algorithms could lead to a further appreciation of its stock in the foreseeable future.

Risks To Consider

While Meta’s recent performance is certainly something that should be celebrated by its investors, there are still several risks that need to be considered.

First of all, there’s a risk that its stock could nevertheless depreciate in the following weeks after a major rally due to the weak earnings results of its Big Tech peers which could drag the whole market down.

Secondly, Meta will continue to burn cash on its metaverse project that has no guarantee to succeed in the future. The company’s latest earnings presentation shows that its Reality Labs division incurred a $4.3 billion loss in Q4 alone and given Mark Zuckerberg’s determination to continue to expand Meta’s metaverse at a steep cost investors need to brace for the possibility that the overall losses could be greater than expected as was the case in Q3.

Thirdly, there’s still a possibility that Meta would once again be required to increase its capital expenditures to new record levels to continue to improve its AI capabilities to ensure that advertisers continue to use its tools as the inability to track iPhone users the same as before could have a great recurring cost over time. This could also hurt the company’s bottom line and its valuation.

The Bottom Line

Meta’s latest earnings results indicate that a weak performance in the first half of 2022 was a temporary setback as the aggressive growth of its family of apps in recent months proves that the business has major competitive advantages in the social media field that could help it to retain its momentum in 2023. A further monetization of Reels and WhatsApp is one of the main catalysts that could help Meta to keep its growth story alive in the following quarters which makes me even more confident in the company’s long-term success.

Be the first to comment