diegograndi

In one of our recent notes, we argued that the strong January jobs report was good news for stocks and does not change the Fed’s new messaging that the disinflationary process has started. Investors can look forward to a slowing pace of rate hikes, opening the door for a “Fed pivot” this year. This point appears to have highlighted an underlying confusion as to what exactly a Fed pivot means, sometimes referring to completely different scenarios between a complete flip in policy direction or just a move to hold rates steady. We’ll attempt to settle the debate below.

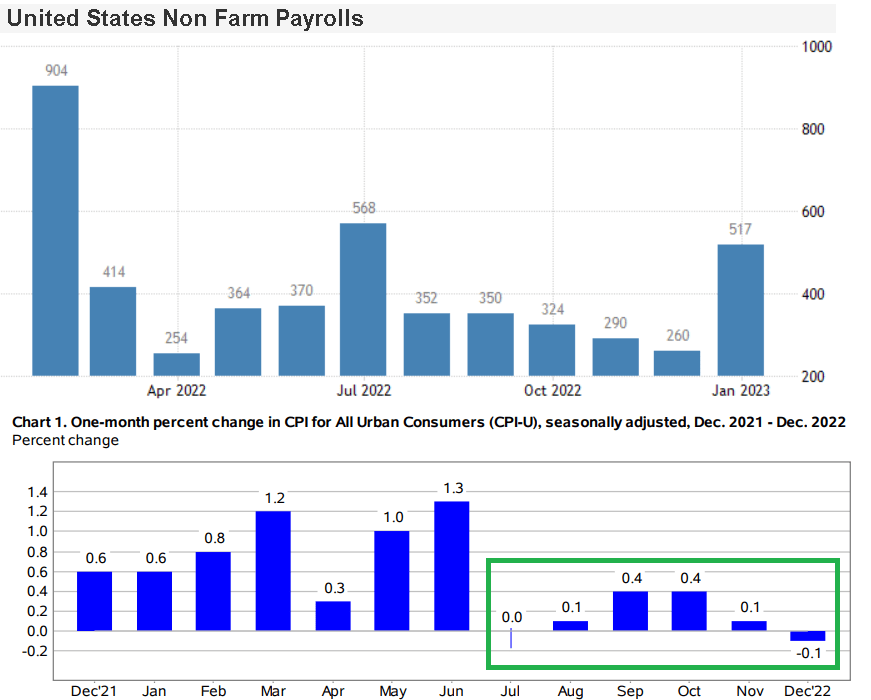

The first point here is that we’re bullish and expect more upside in the S&P 500 (SPX). From the latest jobs report, our thesis is that inflation may have disconnected from near-term labor market dynamics. Whether the payroll numbers showed the economy added 50k or the 517k jobs in January, it may no longer be a primary driver of consumer prices at this stage in the cycle.

The evidence is simply looking at the data where the CPI has already declined from a peak of 9.1% last year averaging a monthly increase of just 0.1% since July, during a period when the U.S. economy added 2.7 million net jobs. The modest monthly average wage growth is not moving the needle compared to what was a bonanza for salary increases and bonuses at the end of 2021. All this is good and plays into the next steps in Fed policy with an expectation that inflation continues to slow.

Trading Economics/BLS

We can also recognize that the factors that led to inflation hitting a 30-year high were primarily based on exceptional circumstances like excess pandemic-era stimulus, supply chain disruptions, and the commodity price spike early last year. Those structural pressures are now easing.

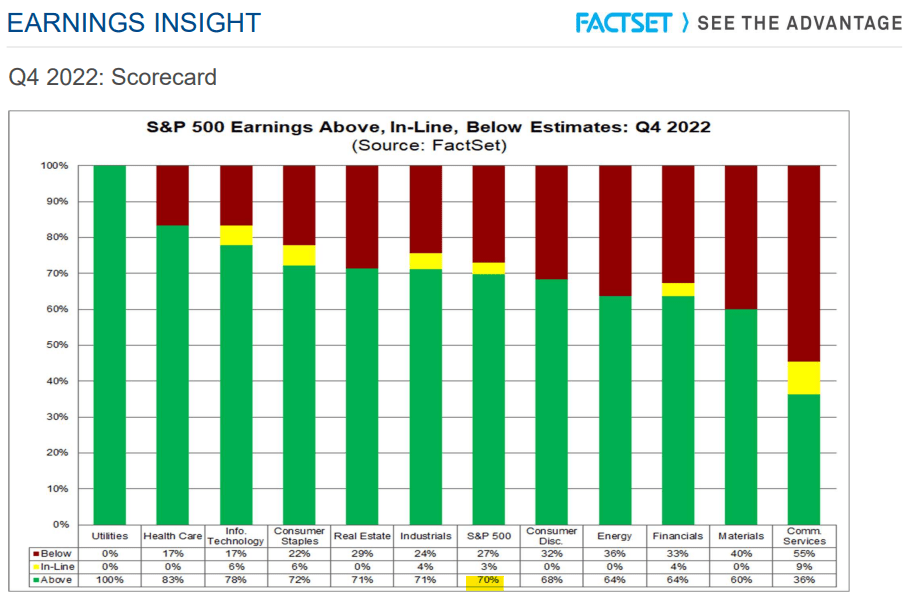

All this is in an environment where the U.S. economy has proven to be resilient despite higher interest rates. The ongoing Q4 earnings season has been highlighted by companies remaining profitable and generally beating earnings expectations. The latest data shows that with 50% of S&P 500 companies already reporting, 70% delivered EPS above estimates.

FactSet

The combination of cost savings efforts and a push towards efficiency is working to support margins with examples like Meta Platforms, Inc. (META) and The Walt Disney Co. (DIS) providing a blueprint for how companies are managing.

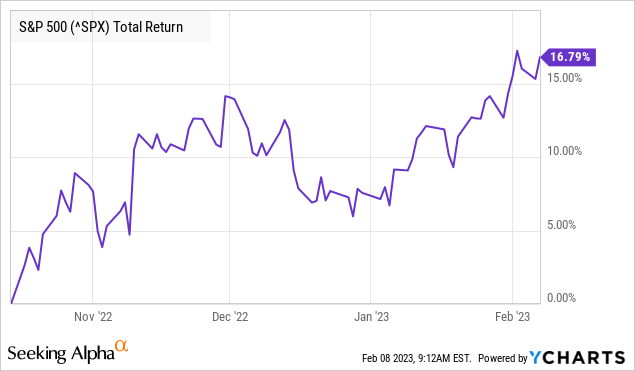

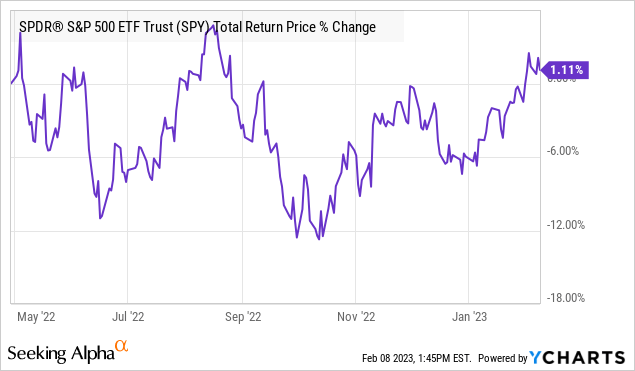

Clearly, we’re not the only ones following this narrative considering the strong rally in the S&P 500, up more than 16% from its 2022 low, making a strong case that “the bottom” is in. The outlook today is a world away from the conditions and uncertainty that defined the first half of last year.

What Is A Fed Pivot?

What the market is focused on now is attempting to decipher the next steps in Fed policy. The idea of a Fed pivot continues to be debated which has become problematic considering various definitions or an underlying misunderstanding.

The way we’re using the term refers to a simple change in the Fed’s policy stance, holding rates steady following a series of rate increases (or cuts). In the current environment, that means pulling back from the uber-hawkish talking points and aggressive rate hikes that defined 2022.

This is in contrast to some believing the notion that a pivot must imply a direct rate cut from here, as an immediate reversal from tightening to easing monetary policy conditions.

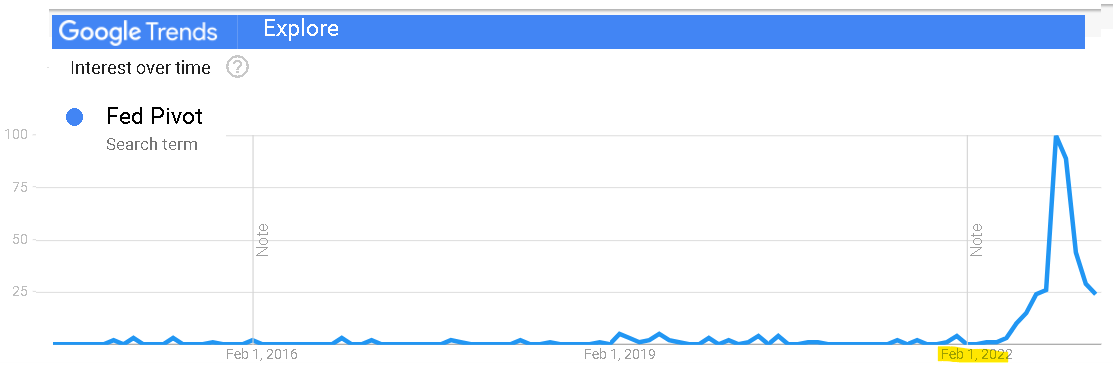

It’s mostly an issue of semantics but it’s telling that the buzzword gained traction in 2022 entering the financial market lexicon in force based on data from Google Trends. The debate has come from both sides covering when, if, and how a pivot would play out utilizing various meanings between a cut, pause, or just change in messaging. The scenarios have different implications.

Google

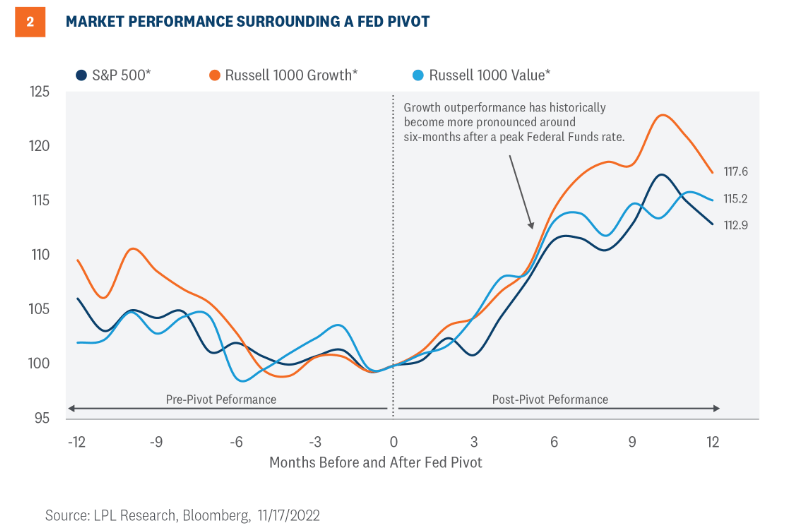

Our line of thinking is echoed by large financial institutions describing a future “pause” as effectively a pivot, irrespective of forming an opinion on the impact on equity prices. BlackRock, Inc. (BLK), for example, predicted back in October a slowdown in the pace of rate hikes as a pivot precursor. We like this clear definition from the investment advisory firm LPL Financial.

We define a policy pivot as simply the end of a rate hike period marked by when the fed funds rate peaked, and not necessarily a shift in policy to rate cuts.

The group shares impressive data suggesting growth stocks have historically outperformed following a Fed pivot. Since the 1970s, the average peak return for the market has been around 17% across a 12-month timeframe after reaching a fed funds rate peak from a hiking cycle. Again, no immediate rate cuts are necessary to capture the positive benefits of the policy change.

LPL Financial

There’s no argument that compared to the string of 75 basis point increases to the Fed Funds rate in 2022, the latest rate hike of 25 basis points, slowing from the prior 50bps increases, has already moved in that direction.

The Fed holding rates steady through an FOMC meeting this year would suggest success in its strategy to bring down inflation. A pause would be the first step to a potential rate cut, whether that materializes later in 2023 or into 2024. Even as Jerome Powell recently indicated no plans for rate cuts this year, the Fed has also shown to be open to adjusting policy and messaging over time.

If the CPI trends firmly under 3% later this year, with no signs of a resurgence, the Fed would have the flexibility to eventually cut because the inflation expectations would justify it, independent of where the unemployment rate is or the strength in the economy. In other words, the CPI/PCE data is the main indicator of importance as it relates to Fed policy, not the jobs number, housing data, or even the level of stocks.

Blame The Doom-And-Gloomers

We’ll blame some of the pivot confusion on “doom-and-gloom” pundits for originally framing the discussion into a sort of scarecrow argument. Going back to last year when the SPX was trading around $3,600, the improbability of a change in Fed policy was used by some as a carrot to affirm a bearish case.

The story went that bulls were wishing for a pivot to save the market on an absurd scenario that the Fed would cave into the pressures of a crashing economy, and make an about-face by slashing interest rates while abandoning their mandate as inflation ran out of control. This false premise helped justify a thesis that stocks had more downside because the Fed would instead keep hiking into perpetuity viewing the CPI as only accelerating.

If we fast forward, that line of thinking has not aged well. In our view, the mistake that this group made was discounting the ability of inflation to fall faster than previously expected while overplaying the negative impacts of higher rates.

The developments of recent months and the market action have drilled several holes into the sinking ship in the bear case for stocks that dominated the narrative for much of 2022. From what we’ve seen.

- Inflation is not out of control.

- The economy is not crashing- there is no deepening recession.

- The labor market remains stable with no signs of surging unemployment.

- Companies are not reporting ballooning losses.

- The apocalyptic scenarios have not panned out.

Bears Are Running In Circles

So putting all those strikes together, it’s easy to see why stocks have rallied thus far in 2023, considering what was a low base of expectations and underlying extreme pessimism at the end of 2022.

Investors that may have been sitting on the sidelines now incrementally adding exposure to equities as an asset class, along with short sellers covering positions, are fueling the repricing of the market higher. To be clear, there is nothing wrong with maintaining a cautious approach or even preparing for any given pullback. There are always individual stocks that go up or down for any number of reasons.

At the same time, perma-bears still waiting for the S&P 500 to make a new low will need to keep moving the goalposts. Pillars of the 2022 bearish case for stocks based on themes like “higher rates for longer” and a proverbial hard-landing of the economy are now outside the consensus.

That group must reconcile an apparent contradiction of a belief that economic conditions are quickly deteriorating against the view that inflation will re-accelerate higher. Yes, either one could still play out, but working with probabilities, those put options are moving further out of the money.

Remember that the S&P 500 is currently up from levels in Q2 2022, and it’s the bears that have been falling for traps over the period, expecting a deeper crash at every turn. Bulls are in a better spot over the last several months.

What’s The Next Market Catalyst

Investors can mark their calendars with four key dates over the next six weeks. We get the January CPI report next week, followed by the February payrolls and February CPI update in early March, all coming ahead of the next Fed meeting.

- February 12th – January CPI report

- March 10th – February non-farm payrolls report

- March 14th – February CPI report

- The next Fed Meeting – March 22nd

The setup here is simple. Confirmation inflation is trending lower for the two pending months of data will be massively important for the next steps in monetary policy. Our call is that the data can push the Fed closer to a real pause, with a single 25 basis point hike followed by holding the Fed Funds rate steady at the May meeting.

Chairman Powell has already said the group is data-dependent, and a continuation of the trends we’ve seen in December and November would go a long way to bring that fabled dot plot terminal fed funds rate forecast for 2023 a tick lower compared to the last December update. A downside “cold” surprise to the CPI would be even stronger for risk assets, pulling forward the possibility of a rate cut sooner rather than later.

While energy and commodity prices led to a decline lower in the CPI since last year, we expect more favorable trends in “core” to be the new story in the first half of this year. Keep in mind that many of those price hikes in consumer goods and services were indirectly tied to commodities with companies passing along higher transportation and logistics costs. That wave has passed.

Reports of car companies like Tesla, Inc. (TSLA) and Ford Motor Co. (F) cutting auto prices are real-world examples of the disinflationary process that help balance the noise in other items of the consumer basket. The correction in the housing market could also begin to be reflected in the “shelter” component of the CPI, which has thus far been stubborn, as another disinflationary factor to drive the annual inflation rate lower against tough comps from 2022.

With the February payrolls report, some normalization compared to the January blowout is to be expected. The only surprise from another positive jobs number will be from those that have been looking for rising unemployment since early last year. Worker average hourly earnings will be the real monitoring point.

Where Do Stocks Go From Here?

With a baseline that a Fed pause is more likely than a cut, that in itself should be positive for stocks. If corporate earnings keep outperforming expectations while the economy averts a deep recession as inflation trends lower, the difference of the cycle terminal fed funds rate held steady at 5.0% or even 5.25% is only a secondary consideration.

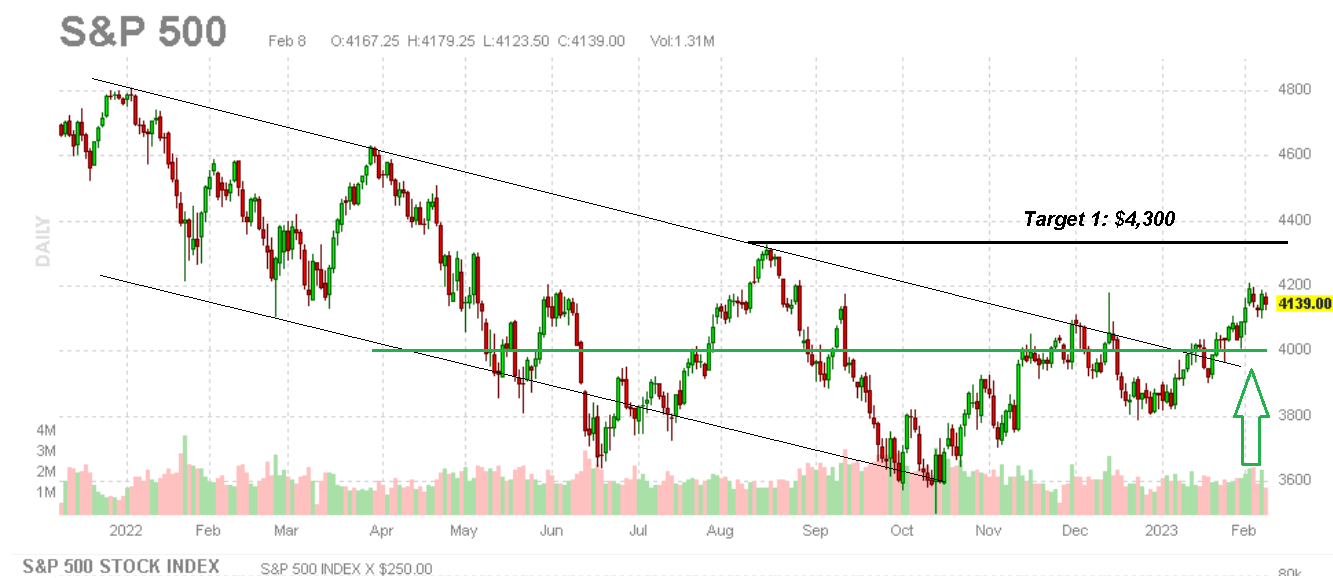

With SPX above $4,000, bulls are in control and our target is $4,300 returning to a level last reached in early August. The difference now is that the bears are the ones sweating heading into the next couple of CPI reports and Fed meetings. We argue that the outlook is stronger today than at any time over the last year, with fewer uncertainties. The market action is now defined by a return of buy-the-dips.

As optimistic as we may seem, we also recognize nothing goes in a straight line and the daily headline volatility is to be expected. Sharply higher energy prices, with oil above $110/bbl, would add new inflationary pressures as a risk to watch. Earnings from high-profile mega-cap leaders also have the potential to shift market sentiment. Our line in the sand is going to be at $3,800 as the critical level of support stocks must hold over the next several months.

finviz

Be the first to comment