Nature/iStock via Getty Images

The Eastern Company (NASDAQ:EML) announced strong orders and deliveries of returnable transport packaging at Big 3 Precision and business acceleration thanks to new vehicle launches by OEMs. In my view, further reorganization of non-core business activities and new acquisitions could accelerate expected FCF even further. Even taking into account potential risks, after running a few DCF models, I believe that the company is undervalued.

The Eastern Company

With some 150 years of experience in the field, The Eastern Company, through its three large production segments, is a multinational corporation that offers engineering services and solutions for different industries.

The key three large companies that belong to the Eastern Company are The Big 3, Velvac, and Eberhard, whose activities differ in specific points but are always aimed at large-scale solutions for industrial activities. Velvac is mainly dedicated to the production of components of tractors used in medium and high-load infrastructures. Eberhard offers customized services for the development of industrial products such as vehicles. The Big 3 offers different products for the storage and maintenance of hand keys and different tools used in this type of market. More information about the operations of these three business segments is found at the company’s website.

Company’s Website

The company was founded in 1858, which means that management has accumulated a lot of know-how and business connections over the years. In my view, the business has been able to adapt and take advantage of changes in the ways of providing engineering solutions, including recent sales of some of its businesses and acquisitions of companies with specific emphasis on wide margins.

With that being said about the company’s long-term history, let’s note that the most recent quarterly reports were quite impressive. In the last report, management noted demand across its core markets and strong orders as compared to previous years. Considering this information, I believe that The Eastern Company appears to be an interesting read.

We believe this sustained growth demonstrates that our businesses are effectively executing on the very favorable long-term demand trends across our core markets. Strong orders and deliveries of returnable transport packaging at Big 3 Precision account for most of the growth in the quarter, compared to the same period last year. Source: Quarterly Release

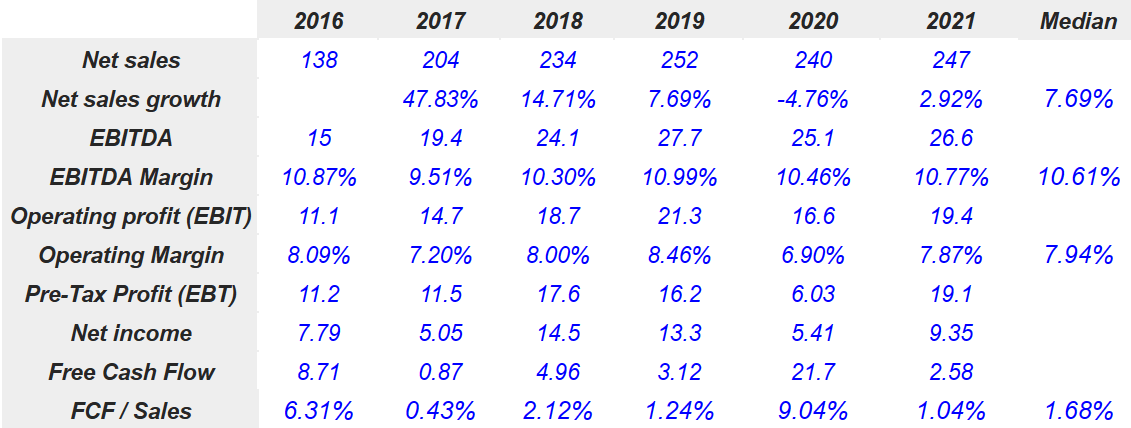

The Eastern Company Reported A Median EBITDA Margin Close To Double Digit And Median FCF/Sales At Around 1.68%

I studied closely some of the figures reported in the last five years. I believe that the company’s financial figures will likely not be far from the previous financial stats.

A year ago, The Eastern Company’s net sales stood at close to $247 million with a net sales growth of 2.92%. Management also reported EBITDA of $26.6 million, together with an EBITDA margin of 10.77% and an operating profit of $19.4 million. The pre-tax profit stood at $19.1 million along with a net income of $9.35 million. Finally, the free cash flow would stand at $2.58 million with an FCF/sales close to 1.04%. The median sales growth stood at 7% with an EBITDA margin of 10% and an FCF margin of around 1.6%.

marketscreener.com

Healthy Balance Sheet

In my view, before having a look at the company’s balance sheet, readers may want to read the commentary given by management. The Eastern Company remains overall very optimistic and confident about the future even considering potential increases in interest rates.

Overall, our balance sheet remains solid. Our liquidity continues to improve, demonstrated by a strong current ratio of 2.9x for the third quarter of 2022. We repaid nearly $3 million of debt and repurchased over 10,000 shares of our common stock in the third quarter of 2022, both of which also reflect on our confidence in our strong liquidity. Moreover, we believe that we are prepared for a rising interest rate environment, with nearly 55% of our term debt locked in at a fixed interest rate of 3.19% through an interest rate swap agreement. Source: Quarterly Release

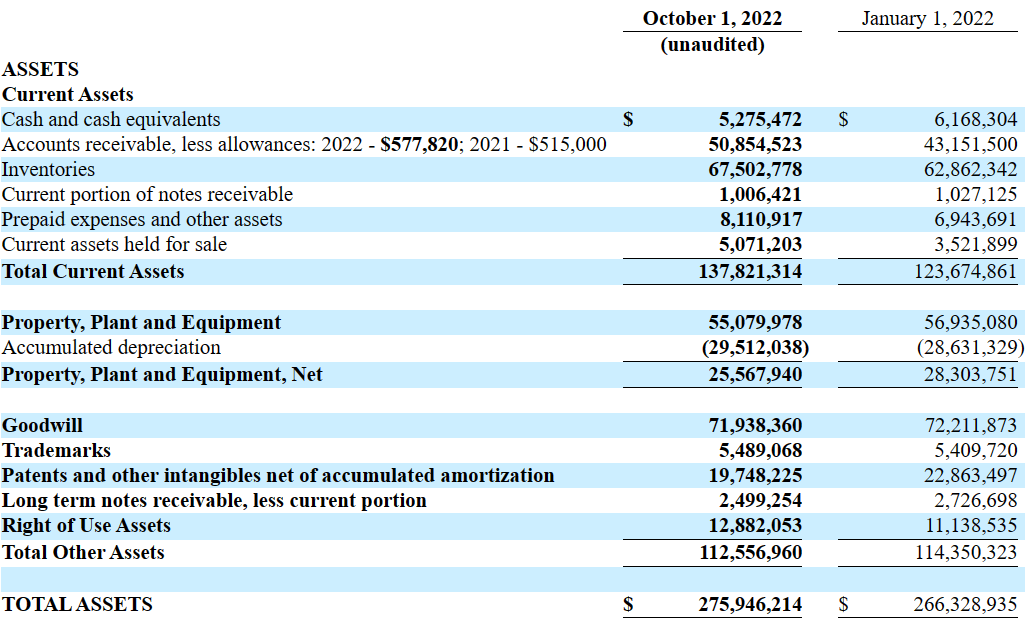

As of October 1, 2022, The Eastern Company reported cash worth $5.2 million in addition to accounts receivable of $50.85 million, inventories of $67.5 million, and prepaid expenses worth $8.1 million. Besides, total current assets stand at $137.5 million, close to 2x-3x the total amount of current liabilities. I believe that liquidity does not seem a problem right now.

Non-current assets include property worth $55.07 million with an accumulated depreciation of $29.51 million, property of $25.5 million, and goodwill of $71.9 million. Patents and other intangibles are worth $19.7 million with the right of use assets worth $12.8 million. Finally, total assets stand at $275 million.

10-Q

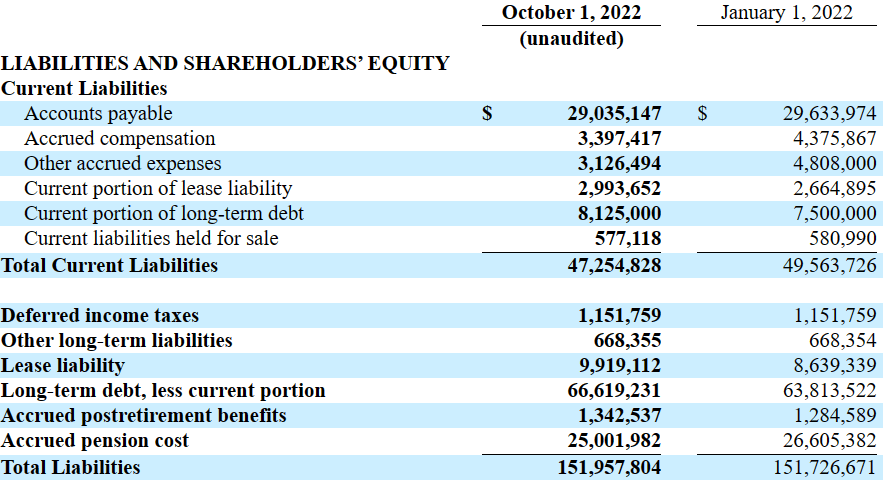

As of October 1, 2022, The Eastern Company reported accounts payable of $29 million along with accrued compensation of $3.3 million. In addition to other accrued expenses worth $3.1 million, the current portion of lease liability stands at $2.993 million with a current portion of long-term debt of $8.1 million. Finally, total current liabilities stand at $47.2 million.

The deferred income taxes were equal to $1.1 million with lease liabilities worth $9.9 million, long-term debt of $66.61 million, and accrued pension cost of $25 million. Finally, total liabilities would stand at $151 million.

10-Q

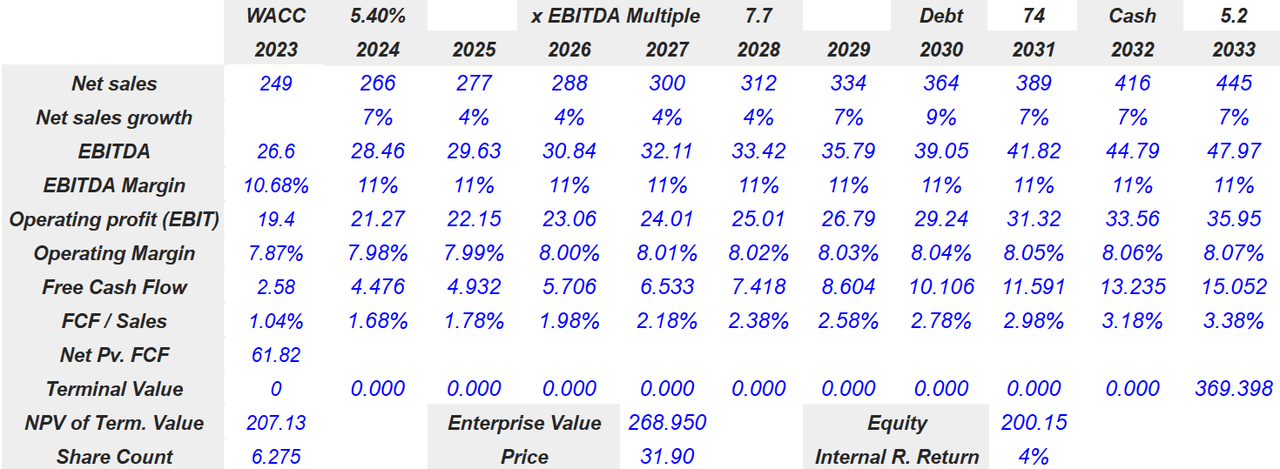

Under My Base Case Expectations, The Implied Price Would Stand At $31.9 Per Share

Under my base case scenario, I assumed that The Eastern Company’s investments in the transport packaging business will successfully generate revenue growth. In this regard, let’s note that in the last quarterly report, management indicated that OEMs are expected to increase the number of models in the market, which could accelerate The Eastern Company’s business. We are talking about growth of close to 50%.

Growth in our transport packaging business is the result of our recent investments in this business and the increase in new vehicle launches by OEMs. According to Bank of America, OEMs expect to launch 245 new models during 2023-26, or an average of 61 per year. This rate of vehicle launches is more than 50% above the average number of models launched per year between model years 2003 and 2022. Source: Quarterly Release

Without straying from the core of its business model, The Eastern Company declared that it is considering acquisitions that do not have a timely presence on the engineering solutions market as long as these allow it to increase the flow of assets and capital and obtain short-term profits to invest and develop new innovations for its products. In line with this rationale, the divestiture of Argo EMS is worth noting, which seems to be a non-core business. In my view, it is beneficial that The Eastern Company decided to mainly focus on business segments that are really beneficial for the company’s bottom line.

Subsequent to the end of the third quarter we also divested Argo EMS which will further streamline our portfolio of businesses and build scale in our largest businesses. In August of last year, we announced our intent to divest our non-core businesses. With the transaction announced October 18, 2022, we have completed the sale of all non-core businesses. Source: Quarterly Release

My numbers under my base case scenario would include 2033 net sales of $445 million together with 2023 net sales growth of 7%. Besides, 2033 EBITDA would be $47.97 million accompanied by an EBITDA margin of 11%. 2033 operating profit would be $35.95 million, with a free cash flow of $15.052 million and an FCF/sales close to 3.38%.

Author’s DCF Model

The net present value of FCF would be $61.82 million. I obtained, with an EV/EBITDA multiple of 7.7x, a terminal value of $369.398 million and an NPV of terminal value of $207.13 million. By including a share count of 6.275 million, with an enterprise value of $268.950 million, I obtained a price of 31.90 per share, equity of $200.15 million, and an IRR of 4%.

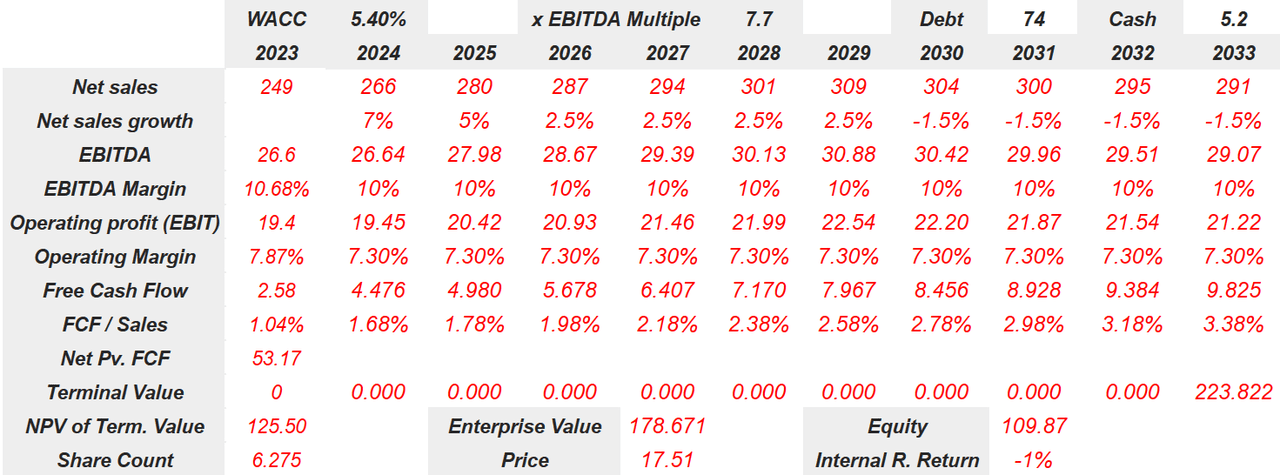

Under Several Risks, The Implied Fair Price Could Stand At $17.5 Per Share

In my view, by providing design solutions for large industries, Eastern Company’s activities are likely to remain active, and industries can continue to function normally, despite various setbacks due to economic instability or force majeure circumstances such as the covid pandemic.

In my view, one of the great cons in terms of the positioning and innovation of its products is that the patents and intellectual properties of these may be almost non-existent, as they are products with a historical presence in the markets and tools whose nominal value is not in itself so high, unless they contain a technological development that serves the particular facilities of the industries. In this regard, in my view, lack of innovation could lead to revenue not growing as much as expected.

Besides, sales in international markets were not of great significance, which shows the lack of global positioning and the company’s lack of experience in this regard. In my view, the company does not have expansion strategies in this sense, but rather a strengthening of its position in the local market. Investors may believe that the company is not that ambitious, which may lead to lower equity demand.

Another risk that this company faces is the great dependence on the acquisition of raw materials from China, whose taxes are variable and have withholding rates that currently oscillate around 25 % of the total cost. Sudden variations in this sense or even disruptions in the commercial relationship between China and the United States could affect the business of Eastern Company. In any case, although it is common practice in industries of this type of magnitude, the dependence on supply chains with high degrees of globalization is currently under question, since, as demonstrated by both the Covid pandemic and the recent Russian military intervention on Ukraine, transportation networks and costs can undergo drastic changes that affect the business operations of any company.

Ultimately, we can add that the lack of diversification in production can play a negative role in the development of the company. In other words, Eastern Company offers services that are contracted mainly by large industrial operators, which have highly favorable macroeconomic projections. However, within this industry, there are also revolutions and transfers of mechanical infrastructures to digitization as well as automation in the different phases of production.

Under the conditions depicted in this scenario, I forecasted 2033 net sales of $291 million with a net sales growth of -1.5%. On the other hand, 2033 EBITDA will likely be $29.07 million accompanied by an EBITDA margin of 10%. 2033 operating profit would be $21.22 million with an operating margin of 7.30%. Free cash flow would stand at $9.825 million together with FCF/sales of 3.38%.

Author’s DCF Model

The NPV of future FCF would stand at $53.17 million, and with an EV/EBITDA multiple of 7.7x, the terminal value stands at $223.882 million with an NPV of $125.50 million. Besides, the enterprise value would stand at $178.671 million with an implied price of $17.51 per share, an equity valuation of $109.87 million, and an IRR of -1%.

My Takeaway

The Eastern Company didn’t only announce strong new orders in 2022, but also business acceleration thanks to investments in the transport packaging business. In my view, new vehicle launches by OEMs could effectively accelerate the company’s revenue growth in the coming years. Besides, in my view, further reorganization of non-core businesses and perhaps new acquisitions could enhance future free cash flow. Even considering risks from lack of international efforts or lack of innovation, the company appears undervalued.

Be the first to comment