Mario Tama

Thesis

From time to time, market sentiment creates very absurd situations. And I found Altria (NYSE:MO) currently in such a situation. Its FWD dividend yield currently stands at 8.29% as you can see from the chart below, approaching its FY1 P/E of 9.4x and almost on par with its FY3 P/E of 8.69x.

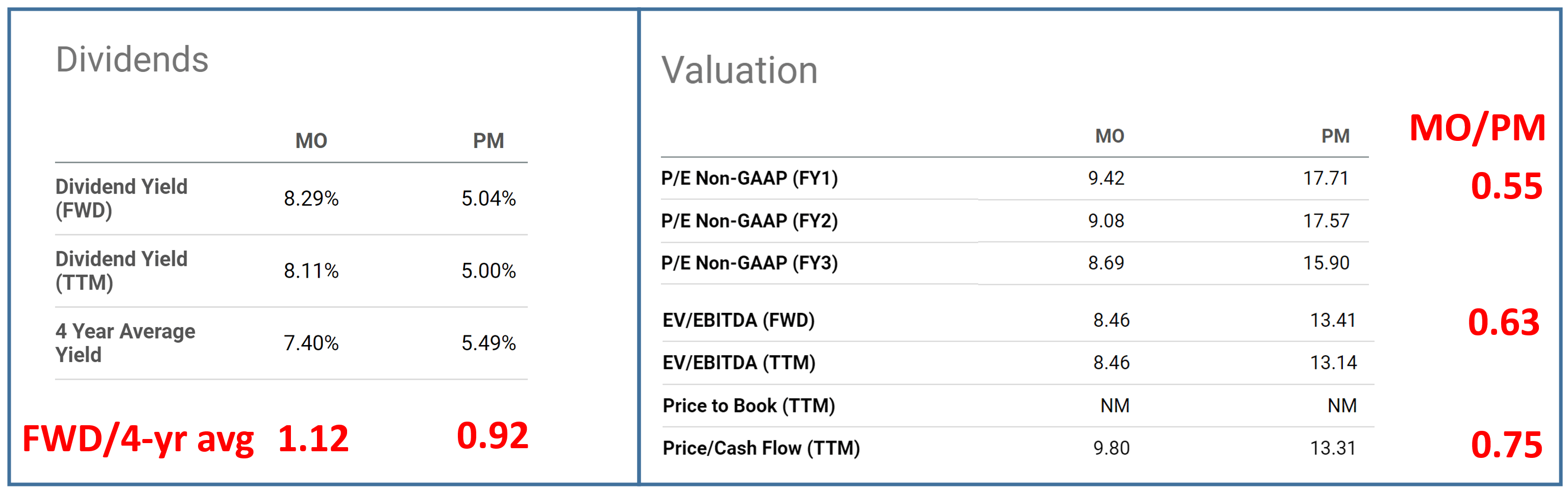

To contextualize these numbers a bit better, the table below also compares the dividend yield and valuation metrics against a close peer Philip Morris International (PM). As you can see, MO’s current FW dividend yield of 8.29% is not only far above PM (5.04%), but also above its own 4-year average yield of 7.40% by almost 90 basis points (or 12% in relative terms). In terms of P/E multiples, MO’s FY1 P/E of 9.42x is only about half (55% to be exact) of PM’s 17.71x. Of course, MO has a higher debt ratio and therefore direct P/E comparison is not exactly accurate. Thus, let’s check a leverage-adjusted valuation multiple such as the EV/EBITDA ratio. As seen, MO’s FWD EV/EBITDA ratio sits at 8.46x, also a large discount from PM’s 13.41x by 37%.

Admittedly, the market has good reasons to discount MO’s shares, and I will detail some of the immediately in the next section. However, my core argument here is that these discounts are so overblown that they are becoming absurd. And more often than not, absurdity in the stock market creates opportunities with unusual return potentials.

Source: author based on Seeking Alpha data.

MO’s Challenges

Let’s start with the good reasons why the market is discounting MO. The company has been posting mixed results in recent quarters. Take the previous quarter as an example, revenues decreased by about 6% compared to the previous year. And a leading driver behind the decline was a 3% decrease in the Smokeable Products group, a secular problem and also a very good reason for the pessimistic sentiment.

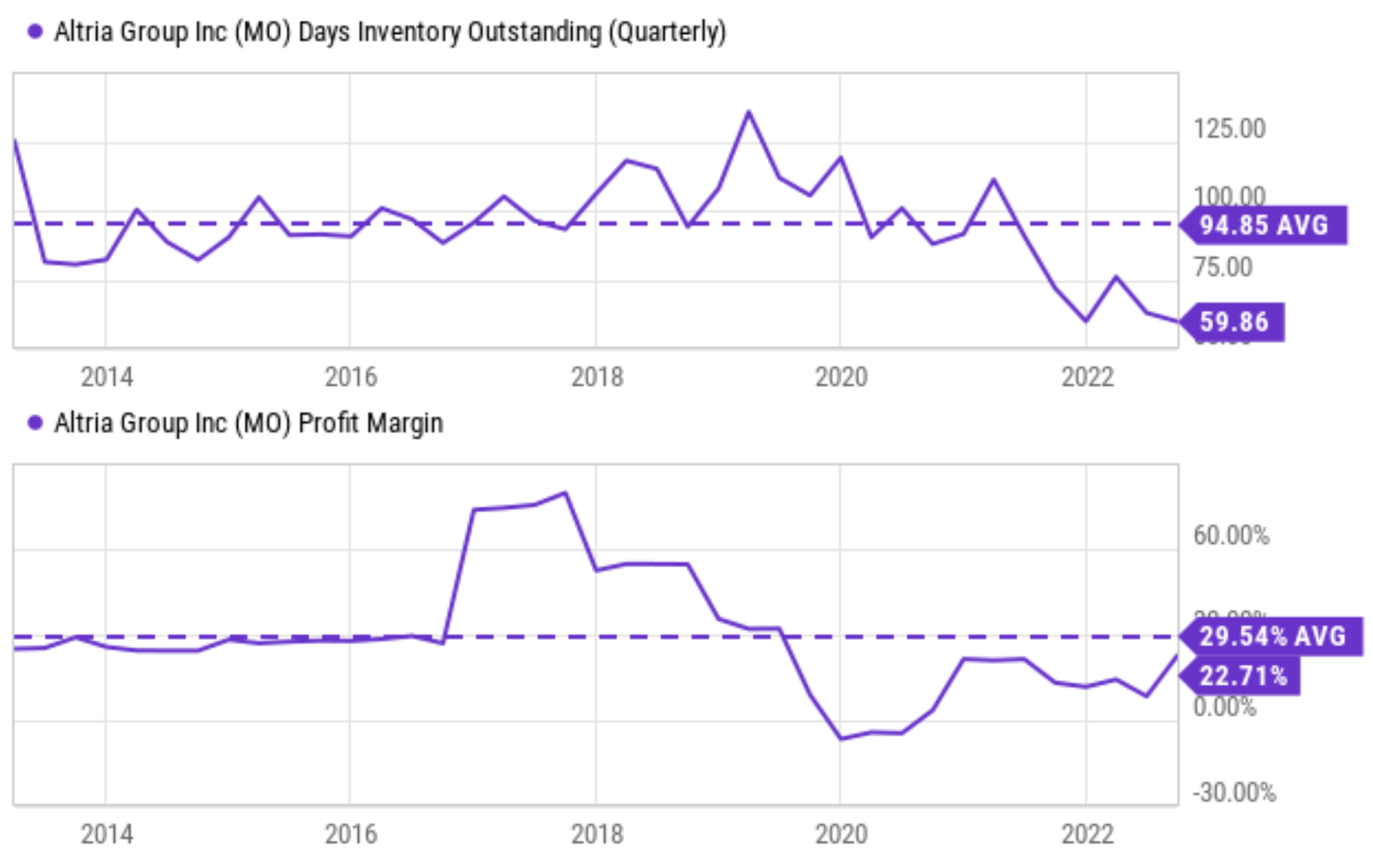

However, if we dig into the financials a bit further, the picture does not look so gloomy anymore. First, part of the top-line decline was due to the sale of the company’s wine business in October 2021. And more importantly, the company was able to partially offset the decrease in shipment volume with higher pricing and lower promotional investments. Actually, the company has been demonstrating such pricing power in the long term as seen in the chart below.

As you can see from the top panel (which shows its days of inventories outstanding on a quarterly basis), its current inventories are at about 60 days, actually near the lowest level in a decade. To me, this is a clear signal that it has no trouble selling its products despite the price increases and also the fear of an overall economic slowdown. And from the bottom panel, you can see that its current profit margin of 22.7% is quite close to the historical average too.

Source: Seeking Alpha data.

Projected growth and return potentials

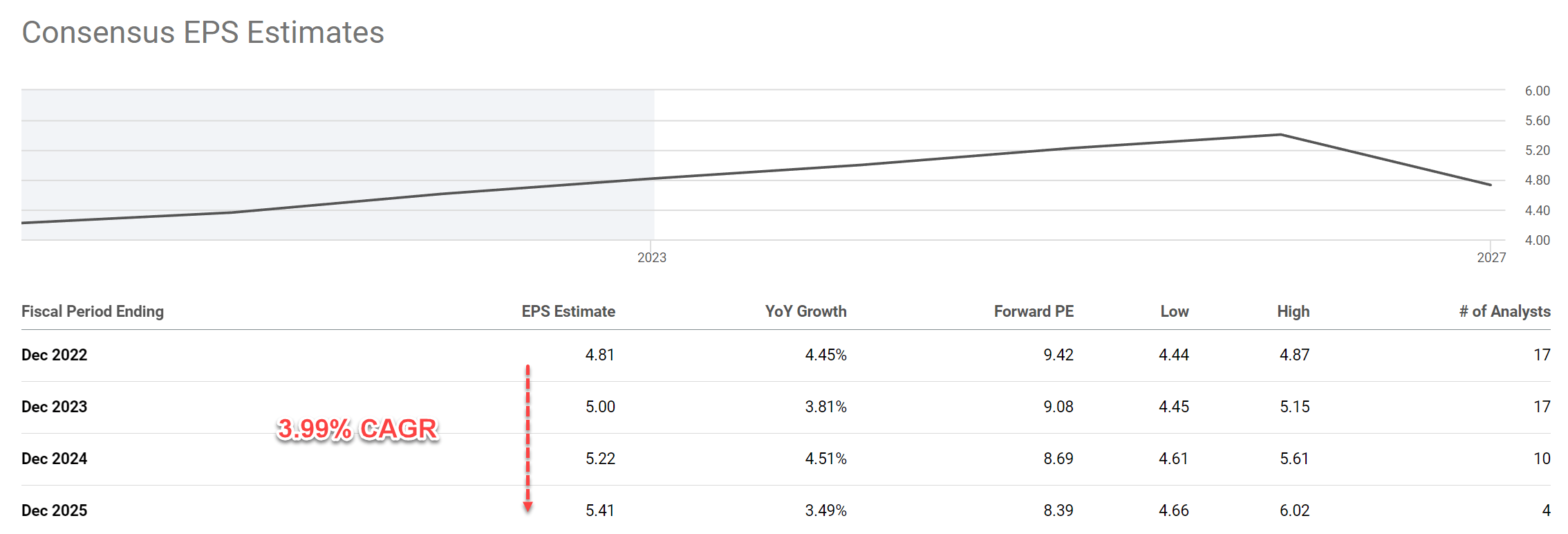

Looking ahead, consensus estimates project a relatively slow growth curve ahead for the next few years as seen in the chart below. To wit, consensus forecasts an EPS growth from $4.81 in 2022 to $5.41 in 2025, implying an annual growth rate of only 3.99% CAGR.

Source: author based on Seeking Alpha data.

I view the above projections to be a bit on the pessimistic side. As detailed in my earlier articles, MO’s ROCE (return on capital employed) has been consistently averaging above 100% (as high as Apple’s). With a 100%+ ROCE, a modest 5% reinvestment rate (“RR”) would fuel 5% real growth rate (growth rate = ROCE * RR = 100% * 5%). As just mentioned, MO has been demonstrating strong pricing power in the long term. And therefore, I feel it is totally justifiable to add an inflation escalator to its growth, which would push its nominal growth rates to the upper-single digit.

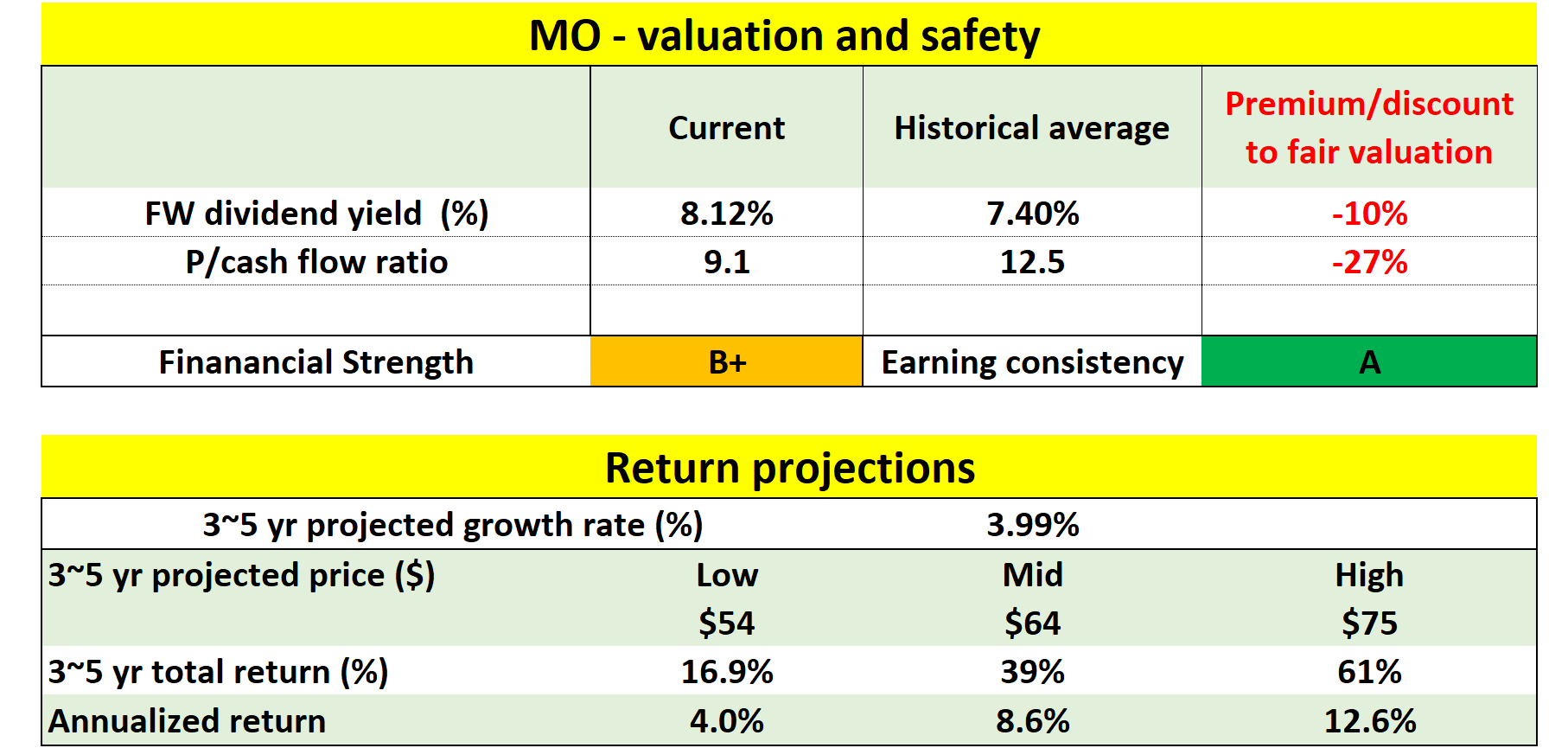

However, under its current extreme valuation compression, even a pessimistic growth rate projection could generate large investment returns already as shown in the chart below. As aforementioned, MO’s valuation is about 10% discounted in terms of dividend yield and about 27% in terms of P/ cashflow multiples.

Given such large valuation discounts, my projections show a favorable return profile even with the 3.99% growth rates provided by consensus estimates. As seen, for the next 3~5 years, I am projecting the total return to be in a range of 16.9% to about 61%, translating into an annual return of 4% to 12.6%. Furthermore, note that a large portion (more than 8%) of the return would be provided through the current dividend already, creating a highly asymmetric investment opportunity.

Source: author based on Seeking Alpha data.

Other risks and final thoughts

Besides the secular decline in its smokable products, MO faces a few other risks also. The macroeconomic environment remains challenging, due to high levels of inflation, elevated costs for energy and commodities, and global supply-chain concerns. The war in Ukraine is also disrupting MO’s business. These issues could pressure tobacco consumers’ disposable income and impact MO’s revenues. However, as argued above, MO has demonstrated the power to adjust the price and improve its operational performance to combat these issues and help support earnings.

A bigger risk involves its ongoing regulatory case regarding JUUL. Since the FDA ordered JUUL to take its e-cigarettes off the market back in June 2021, this regulatory case has had several turns. The ban was suspended in July 2021 and subjected to further review. In early September 2021, JUUL agreed to pay ~$440M to settle claims in 34 U.S. states and territories. The eventual outcome of this regulatory case would create a large impact on MO’s role in the alternative product categories and also market sentiment. Although my view is that the current valuation has already priced in the worst possible outcome already.

To conclude, the market certainly has good reasons to discount MO’s valuation given the headwinds, both in the long term (such as the secular decline of its traditional products) and also in the near term (such as the inflationary pressure). However, my thesis is that the market has drastically overreacted to the degree of absurdity. And history has taught us that absurdity often creates unusual opportunities.

Be the first to comment