ryasick

AI (artificial intelligence) has been an ever-growing topic of conversation with tech companies and investors, and the trend is no different with my articles over the last few months. I first broached the subject by explaining how this recession will provide tailwinds for AI development and deployment. It was ahead of the more major announcements, like Meta Platforms (META). I outlined how Micron (MU) and Nvidia (NVDA) will benefit from the trend. However, due to their high level of retail exposure, the data center-driven AI investments from hyperscalers have been overshadowed. But this isn’t the case for all AI beneficiaries. My latest example and top long pick in this vein is Arista Networks (NYSE:ANET).

If you haven’t been following my AI articles sprinkled over the last few months, I suggest you read them to understand how AI investments are happening because of layoffs and other recession-cautious spending changes.

The basic principle is for large tech companies to implement AI-driven technologies to gain a competitive advantage while cutting costs. In Meta’s case, it needs both to replace its laid-off workforce in content moderation and manual advertising targeting, and advance its automation to scale out the rest of its labor-intensive workforce. In doing so, the company will have a more efficient backend and product, getting itself out from under iOS privacy challenges hampering it over the last year. As a result, it gains both efficiency and a competitive advantage.

Since AI is not a cheap route, requiring the fastest and most resource-intensive servers aligned with the best networking and infrastructure, the large hyperscalers are in the lead to spend.

And boy, can they spend.

AI Spending Playing Out

Meta Platforms

Even as META changed course slightly after its Q3 earnings call – laying off thousands of workers and adjusting CapEx – it remained committed to its AI spending.

For 2023, we expect capital expenditures to be in the range of $34-$39 billion, driven by our investments in data centers, servers, and network infrastructure. An increase in AI capacity is driving substantially all of our capital expenditure growth in 2023.

CFO Commentary, Meta’s Q3 ’22 Earnings Press Release

The only thing it changed in the follow-up SEC filing was tightening the CapEx range:

In addition, we are updating our 2023 capital expenditures outlook to be in the range of $34-$37 billion, narrowed from $34-$39 billion.

The net result is the midpoint of CapEx has come down $1B. But this is nearly immaterial as the specificity of the CapEx growth over 2022 (now an estimated $3B) going almost entirely to AI buildout doesn’t exclude a portion of the rest of CapEx also going to AI in some form or another. The key is the increase in AI capacity, as the other part of CapEx can still directly fund AI capacity or, at the very least, indirectly fund it.

The bottom line is META is spending on AI – increasing its spend on AI – while cutting costs elsewhere in the business.

Microsoft And OpenAI

It’s no secret Microsoft (MSFT) is a massive proponent of AI. It has direct investments in OpenAI, the overnight-born star in the AI world, through its release of ChatGPT (though most in the industry knew about OpenAI from at least its early DALL-E days almost precisely two years ago – the product where it creates an image based on natural language input).

Therefore, it’s clear Microsoft is investing heavily in AI. And more coming every week, it seems.

But don’t take my word for it; read what CEO Satya Nadella had to say about it on its recent earnings call during the Q&A portion:

…yes, the OpenAI partnership is a very critical partnership for us. Perhaps, it’s sort of important to call out that we built the supercomputing capability inside of Azure, which is highly differentiated, the way computing the network, in particular, come together in order to support these large-scale training of these platform models or foundation models has been very critical.

That’s what’s driven, in fact, the progress OpenAI has been making. And of course, we then productized it as part of Azure OpenAI services.

…

So, yes, so I think AI is a place where I think we have differentiated capability at an infrastructure layer for training and inference and the model that sells or platforms for third parties and our first-party applications are getting better because of the use of those AI models.

Putting your money where your mouth is looks like capital expenditures. Microsoft expects CapEx to be driven by its data center infrastructure buildouts. CapEx spend came in at around $6.6B for FQ1:

Capital expenditures, including finance leases were $6.6 billion, and cash paid for PP&E was $6.3 billion. Our data center investments continue to be based on strong customer demand and usage signals.

– Amy Hood, FQ1 ’23 Earnings Call

And is guided to increase in FQ2:

In capital expenditures [for FQ2], we expect a sequential increase on a dollar basis with normal quarterly spend variability in the timing of our cloud infrastructure build-out.

– Amy Hood, FQ1 ’23 Earnings Call

If anything, Microsoft is the closest to the ground regarding AI investment, meaningful AI results, and AI trust among the start-up community. As a result, it facilitates real-world, real-time AI adoption change.

Spending on the cloud/data center is the top priority called out by two of the major hyperscalers. Alphabet (GOOG)(GOOGL) and Amazon (AMZN) show near identical AI priorities, the intensity of AI investments, and time spent discussing AI on their earnings calls, too.

How Does Arista Networks Benefit?

It’s clear hyperscalers are pouring money into AI-related investments, including AI-specific servers, networking, and infrastructure. This is no small feat, and it’s happening as a tailwind in the face of a recession.

It’s no surprise then that Meta and Microsoft are two of Arista’s main customers. The company calls out both specifically in its earnings calls:

Our cloud titan customers are now expected to account for approximately 45% of our revenue for the year with major contributions from Meta and Microsoft.

– Ita Brennan, CFO, Arista Networks Q3 ’22 Earnings Call

It wouldn’t be out of line to say Meta and Microsoft combined likely contribute 30% of ANET’s revenue, give or take, varying from quarter to quarter. Some may say this level of concentration is not suitable for diversification. However, it’s helpful to have such major customers present because their earnings calls provide another set of data points directly affecting Arista.

And so it’s not solely about customer concentration. It’s also about the inner workings of those business dealings. Understanding the supply and demand aspects give us insight into the importance of ANET’s position in the market and the networking sector in general.

What I love about ANET’s management is its directness and transparency, calling it like it is. You don’t get the kind of response ANET’s management provides from many other companies. For example, the specificity regarding its customers, not only by name but also the current business situation with them, brings the investment thesis within reach.

So I think it’s fair to say... the Cloud Titans continue to be strong and couldn’t be better. Especially with Microsoft and Meta, who we fully expect to be greater than 10% concentration. I wish we could ship them more. And I think if they were hearing this call, they would be saying, I wish you could ship us more too.

– Jayshree Ullal, CEO, Q3 ’22 Earnings Call Q&A

That’s a massive ringing endorsement of what part of tech is in demand as AI becomes a more significant piece of the data center pie.

Who would have thought networking would be the golden child of AI structuring?

Well, probably a few, to be sure.

But surely, it’s memory in the form of DRAM and NAND from Micron and GPU-based AI accelerators from the likes of Nvidia that are the primary money makers. And to be fair, those few components are.

But what sets Arista Networks apart is its focus on fully integrated, efficient networking products and its focus solely on enterprise, cloud, and service providers. That means retail weakness doesn’t come into play for ANET, at least not in any direct form, as it does for Micron and Nvidia. As long as cloud and service providers continue to upgrade their infrastructure for AI-related purposes, IoT (internet of things), or even just expansion, Arista is receiving large orders.

And AI spending and general expansion are only gaining momentum as mainstream AI traction takes place before our eyes, ChatGPT being only one example. You won’t be privy to a lot of AI, but some of it, you will. The differences don’t matter in the end when hyperscalers need the equipment to do internal AI, mainstream AI, or expand current AI capacity.

It’s Showing Up In The Financials

This is all well and good, but the financial aspect of Arista’s business matters as much, if not more, than its AI-spurred market.

For starters, estimates have not moved downward over the last month, underscoring analysts’ confidence in the company since its earnings report on Halloween, along with not being affected by broad market weakness since then.

Seeking Alpha

Quite honestly, the community doesn’t see deterioration in any of its estimates. In fact, there wasn’t a single red mark on its earnings revisions over the last month for the next nine quarters.

This is merely professional analyst feedback and doesn’t give us much to go off of, which is why I’ll dig deeper. Nonetheless, seeing positive revisions is a good start. Unfortunately, I can’t say as much for the rest of tech in this regard.

Its recent earnings at the end of October provided its tenth beat and raise, dating back to the pandemic quarter of 2020. Considering the company remains supply constrained, this track record of beats and raises means the company is being held back from even more bullish performance.

Overall, demand for our products remains healthy across all areas of the business, supply challenges continued throughout the quarter, with ongoing supplier decommits, constraining shipments, and requiring higher cost broker purchases and expedite fees.

– Ita Brennan, CFO, Q3 ’22 Earnings Call

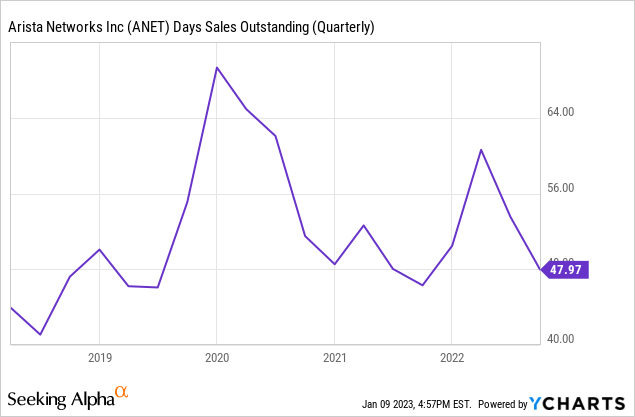

The supply constraint environment has kept inventory days at pre-pandemic levels even though demand is much higher than then, illustrated by the ever-growing CapEx allocation toward data center buildout.

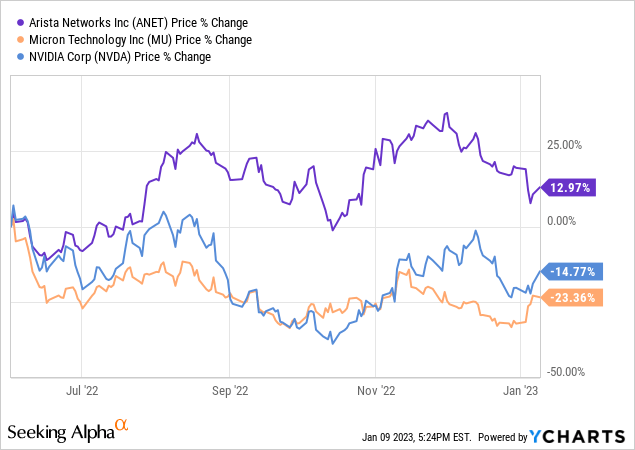

With demand not fading anytime soon and recession pressures only putting hyperscalers in a position to double down on amazingly-more-efficient-than-a-human technology, it’s only a factor of supply keeping up with demand. This differs from consumer demand retreating and falling off a cliff over the last few months. This is what caught Micron and Nvidia in a whirlwind of selling.

But notably, since the summer, this didn’t happen to ANET.

ANET has not had to deal with it because its end markets are driven by massive tens of billions of dollars in investments into world-changing technology, not fickle consumers who can quickly and easily turn the spending spigot on and off.

This is why Arista will continue to outperform growth from other peers, even peers in strong sectors like cybersecurity. Those names are seeing some pain as deal scrutiny increases and deals are delayed or signed for shorter periods. ANET is seeing maxed-out supply, hoping to ship more products to its largest customers.

Valuation And Why I’ve Initiated Here

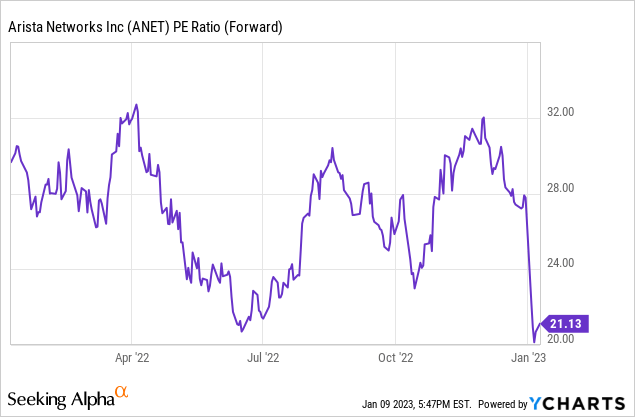

The analyst consensus expects EPS to grow 52% in ’22 and 24.4% in ’23. These estimates will become conservative after ANET beats a few more times with the AI train gaining steam while supply constraints continue to ease. Additionally, these estimates vary widely from the lows and highs, and the low side estimates will likely come up a great deal, pushing estimates toward the high end. Therefore, a 21-times forward P/E seems, at worst, moderately undervalued and, at best, attractively undervalued.

I initiated my position as it fell to the 20-time forward P/E level. This is the stock’s lowest valuation in the pandemic era, even when growth was re-accelerating two years ago. And it remains below even the current consensus for 24% EPS growth this coming fiscal year.

Arista Networks Is In A Prime Spot For Capitalizing On AI Spend

Networking hardware and software looks to be the sweet spot for capitalizing on the billions of dollars being invested in AI. Instead of dealing with the downside of component manufacturers and software providers in more diversified end markets – namely, retail – you get more of a pure play with Arista Networks.

This pure play can be verified across several tech giants as CapEx plans are generally provided for the upcoming year. So while measuring ANET’s business directly helps, the signals are out there to judge its longer-term TAM (total addressable market). Right now, those signals are all pointing toward higher levels of spend for longer periods.

While growth won’t go on forever, the push toward AI is not ending anytime soon. In fact, we may have just started the early adopter phase of the lifecycle. With Meta now using it as its prime growth driver to become leaner and create better ad targeting, these investments won’t slow down in 2024 or 2025. Likewise, ChatGTP hosted on Microsoft Azure just grabbed another gear with its popularity and, more importantly, its utility.

All of these tech titans, as Arista calls them, require faster networking and more of it. I like ANET under $115 and started my position just under $110. I’ll accumulate more if the market provides an opportunity under $100.

Be the first to comment