“Fascism is capitalism in decay.” – Vladimir Lenin

Looking at the growing rifts between the 27 members of the European Union, with Hungary being singled out by the European Commission while getting support from Poland, when it came to the difficult task of choosing a title analogy we decided to go for the 27 Club. The 27 Club is a list consisting mostly of popular musicians, artists, actors, and other celebrities who died at age 27. The deaths of several 27-year-old popular musicians between 1969 and 1971 led to the belief that deaths are more common at this age. Music biographer Charles R. Cross wrote:

“The number of musicians who died at 27 is truly remarkable by any standard. [Although] humans die regularly at all ages, there is a statistical spike for musicians who die at 27.”

Following BREXIT, the European Union is now composed of 27 countries, and given the potential economic collapse coming from extremely serious energy woes, one might wonder if indeed we will not be witnessing in the near future the demise of the European Club 27, with no additional members making it pass the 27 number hence our tongue in cheek title.

In continuation to our previous conversation, we are increasingly concerned by the rapid deterioration of consumer confidence, in conjunction with widening credit spreads. As such, the latest rise of 75 bps of the Fed is adding increasingly more pressure on the “energy dependent” European Union.

In this conversation, we would like to continue to look at the deterioration of the European context through additional indicators, as well as Mack The Knife (US dollar + Real rates) given the continuation of his murderous rampage, putting even more pressure on high beta in general and asset prices in particular.

Europe’s consumer confidence is crumbling and there are signs of a rapid tightening in credit conditions

In our conversation “The European crisis: The Greatest Show on Earth”, we indicated:

“When it comes to credit conditions in Europe, not only do we closely monitor the ECB lending surveys, we also monitor on a monthly basis the “Association Française des Trésoriers d’Entreprise” (French Corporate Treasurers Association) surveys.”

But, you might rightly ask why our specific focus on France?

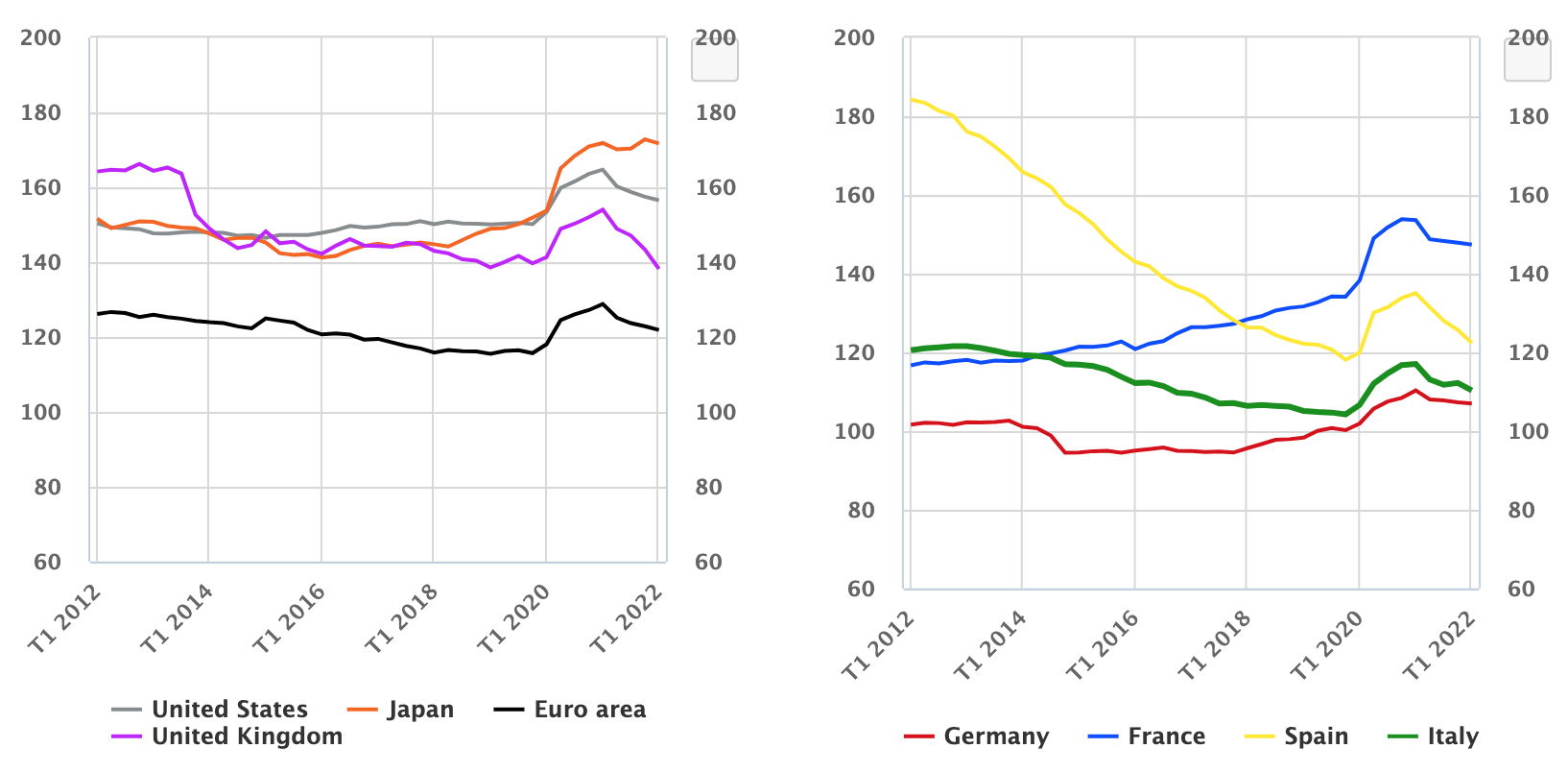

Non-financial private sector debt ratio (in % of GDP) of France stands at 147.4% of GDP and remains the largest one among the main euro area economies according to Banque de France:

NFC Debt (Banque de France)

As such, NFCs rely on bank lending to cover a large share of their new financing needs, which is sensitive to bank lending rate conditions. Second, the trade-off between bank loans and bond issuance is determined by the relative cost of these two debt instruments. Finally, shocks that move equity markets affect, through equity revaluations, the market leverage of firms, which in turn translates into adjustments of debt-related risk premia. You get the drift.

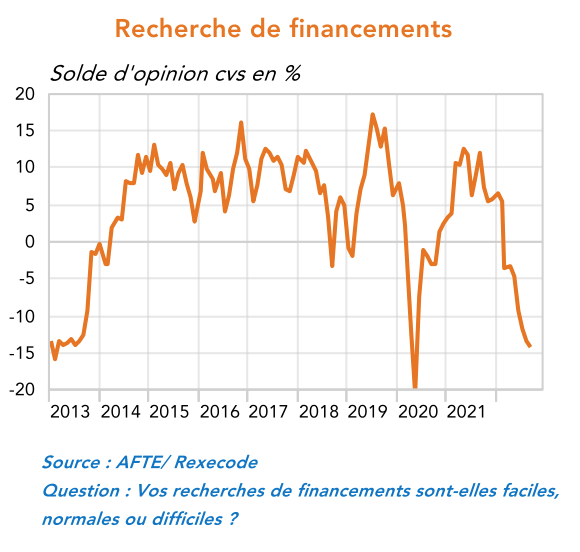

As per the below charts from AFTE/Rexecode, and given the hiking path followed by central banks, ECB included, on top of “energy woes”, credit conditions are rapidly “tightening”:

“The judgment of the treasurers of large companies and SMEs on the search for funding continued its decline in September, but it was much more measured (by 0.7 points). Fundraising is therefore seen as being difficult, the indicator being well below its average “long term.”

Source of financing (AFTE Rexecode)

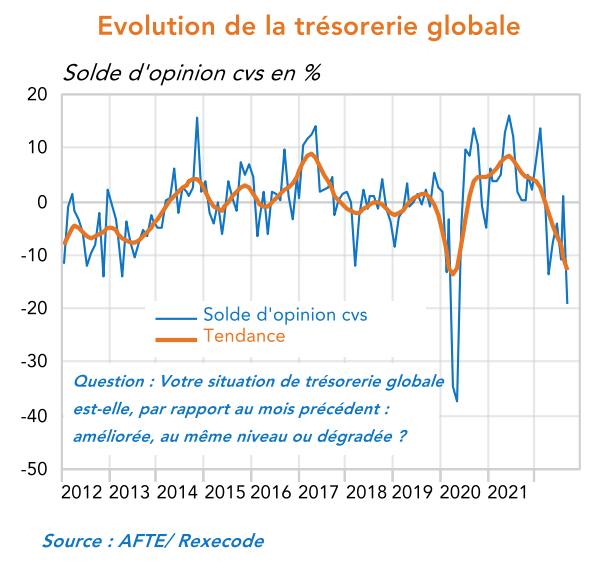

Also in the AFTE latest survey, there is now a clear trend in the deterioration in the global cash situation showing up for French Corporate Treasurers:

Global Cash situation France (AFTE Rexecode)

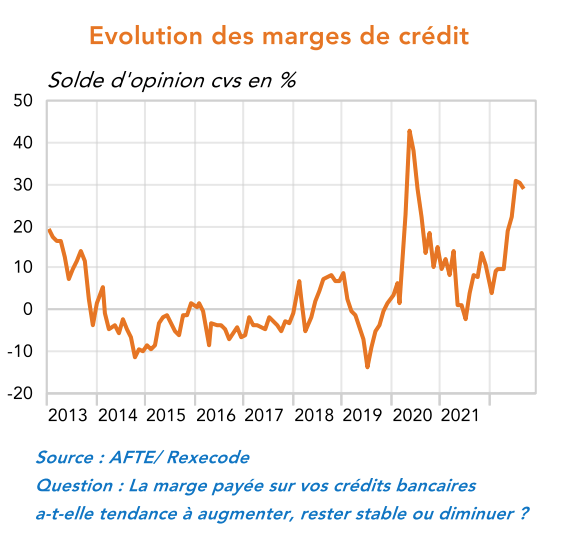

As well, in AFTE’s latest survey, we can now see a clear trend in the deterioration of financial conditions for French corporate treasurers:

“Does the margin paid on your credit facilities have a tendency, to rise, fall or remain stable?”

Credit Margins (AFTE Rexecode)

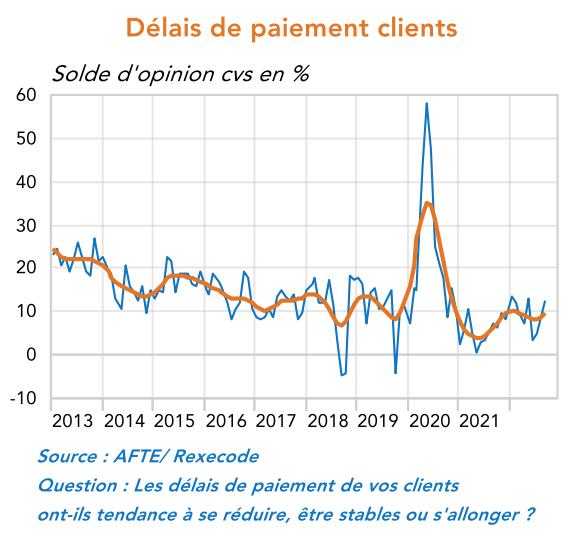

One particular important indicator we follow is the rise in Terms of Payment as reported by French corporate treasurers. The monthly question asked to French Corporate Treasurers is as follows:

“Do the delays in receiving payments from your clients tend to fall, remain stable or rise?”

Delays in payments (AFTE Rexecode)

While so far we do not see from French Corporate Treasurers a deterioration in the above indicator, we do think we will see a rapid deterioration and an increase in the rise in Terms of Payment.

Going forward, we will closely be monitoring these additional signals coming from French corporate treasurers to measure the impact on the overall financial conditions in Europe.

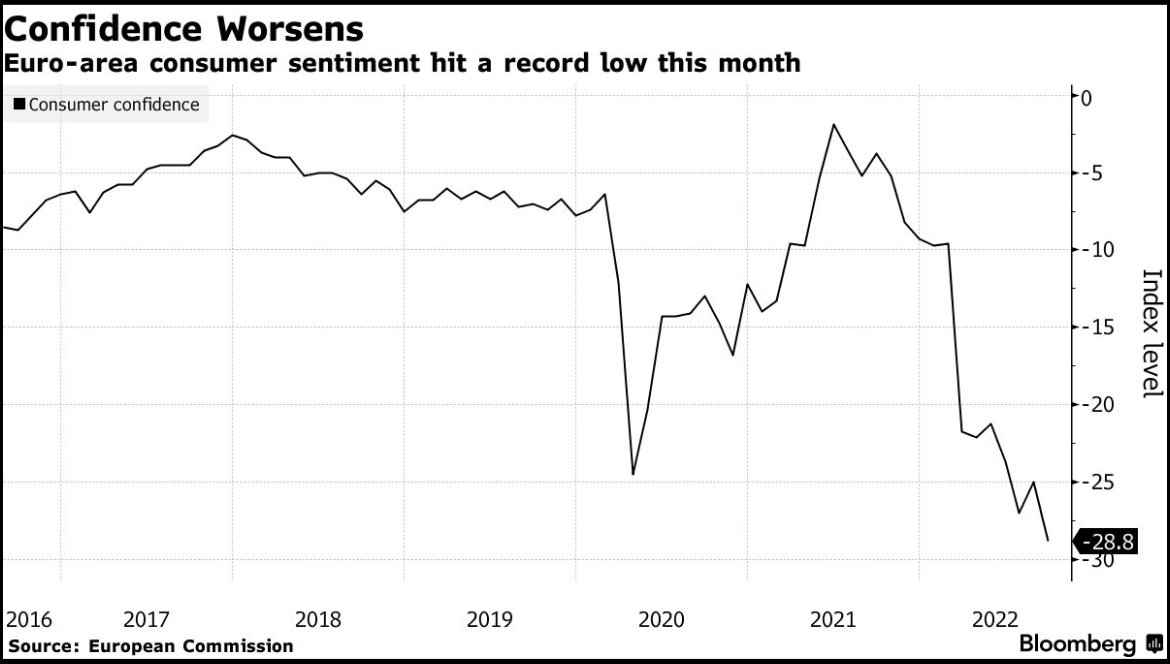

On top of rising pressure thanks to tightening financial conditions and rising energy prices, no wonder Europe’s Consumer Confidence is in the proverbial doldrums:

EU consumer confidence (Bloomberg – Twitter)

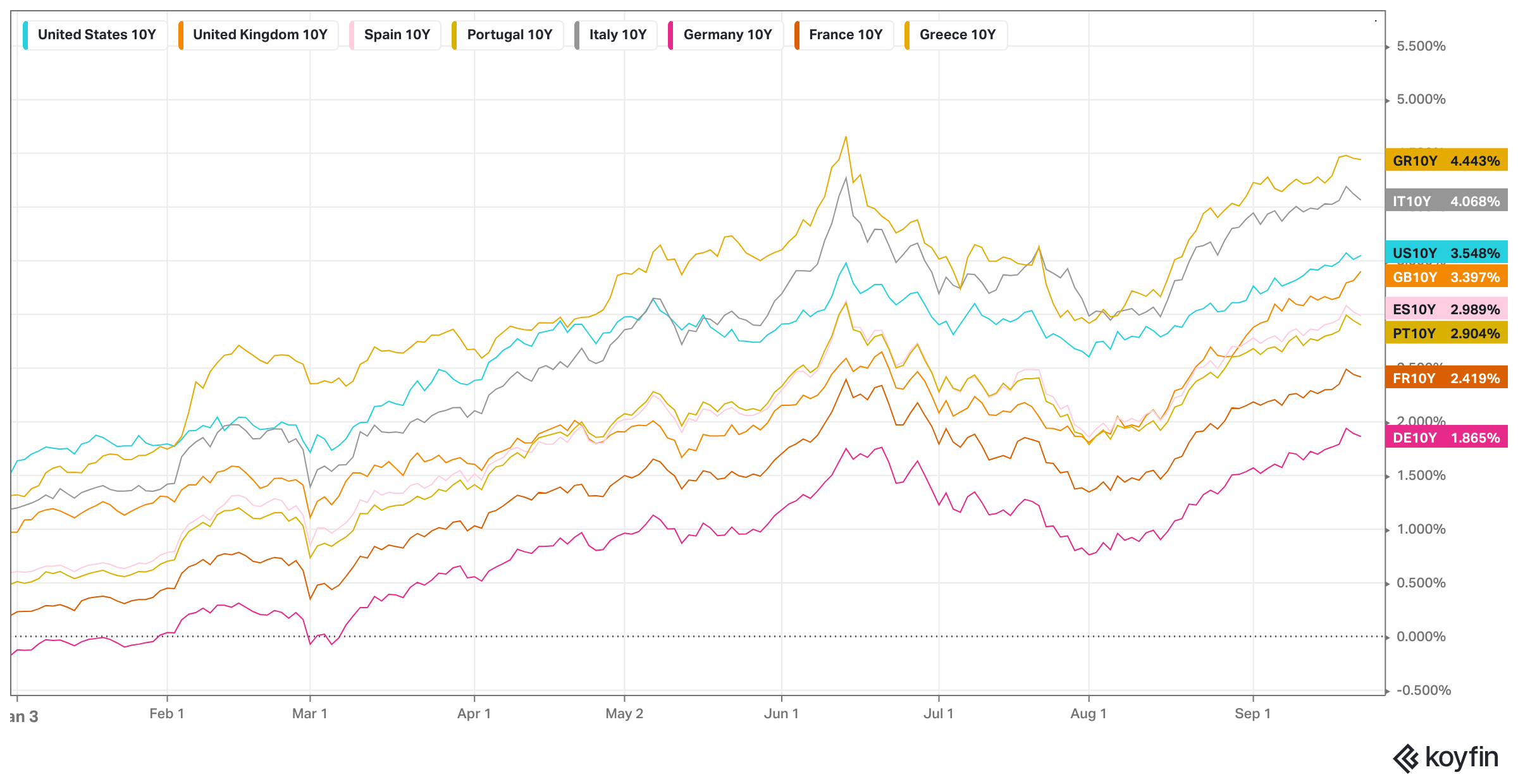

You can add to the mix the significant rise in European Government Bond Yields:

Bond yields (Koyfin)

On top of these European woes, the latest German PPI is giving no respite to the ECB:

“With German PPI inflation hitting 45%, we have a 7 sigma (one in a billion years) divergence to CPI. This suggests two things 1) European bonds yields are moving higher and will take Treasuries for the ride 2) European corporates are facing massive margin compression.” – Julian Brigden

German PPI (Julian Brigden – Twitter)

On top of rising cost of financing, the energy bill for Europe as a whole is already “significant”:

“The bill for Europe’s energy crisis is nearing 500 billion euros as governments rush to soften the blow of soaring prices, according to a think-tank” – Bloomberg

Europe Energy bill (Bloomberg – Twitter)

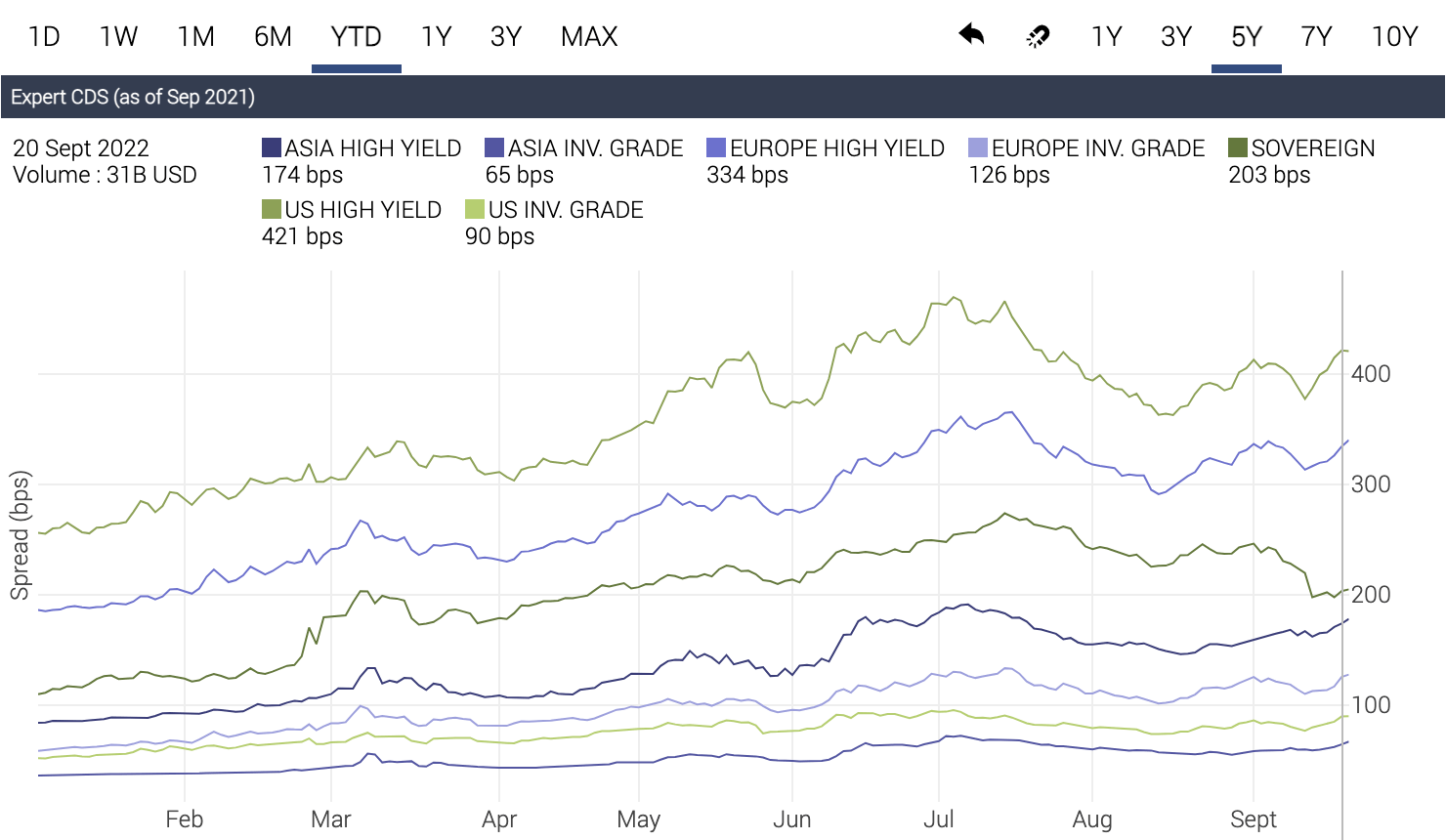

Overall, global CDS 5-year YTD indices are starting to widen again in credit land, showing that the summer “grizzly” rally is done and that a weaker tone is now firmly in:

Global CDS (Datagrapple.com)

We think European High Yield CDS should be much wider than US. We have seen a higher weakness in cash, but “synthetic” CDS Europe HY should be much wider than US. (421 bps vs 340 bps). As such, we expect an acceleration in the widening in European credit vs US.

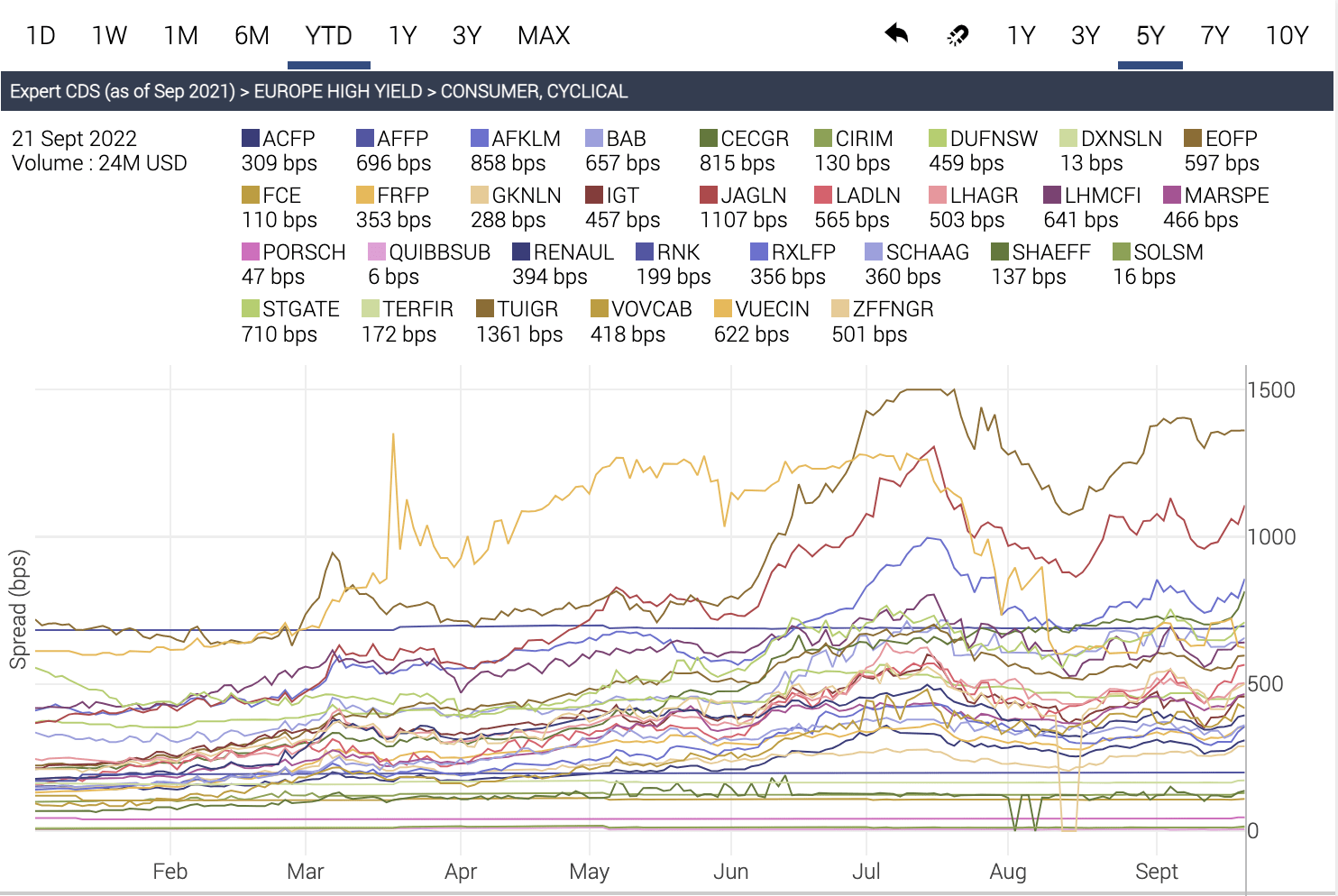

CDS wise, stress is already showing up in 5-year CDS European High Yield Consumer and Cyclical names:

European HY CDS (Datagrapple.com)

To repeat ourselves from our previous conversations, given credit growth is a stock variable and domestic demand is a flow variable, the most predictive variable for default rates remains credit availability. Given credit availability is quickly “disappearing”, you do not need to be a “rocket scientist” to forecast “credit events” in the not-so-distant future in “credit land”.

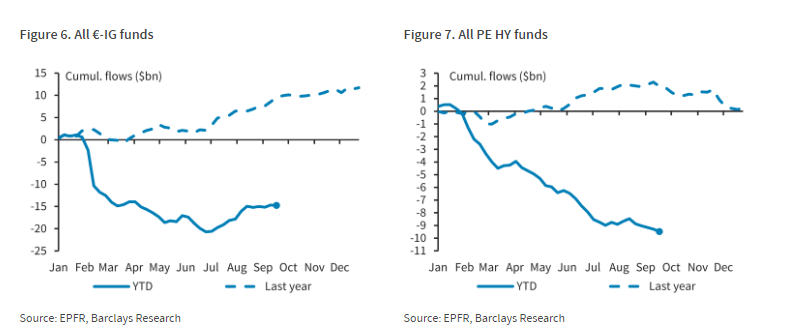

Another sign in rising weakness in credit markets can be ascertained from Cumulative flows in Investment Grade and High-Yield funds:

Credit flows (@creditjunk – Twitter)

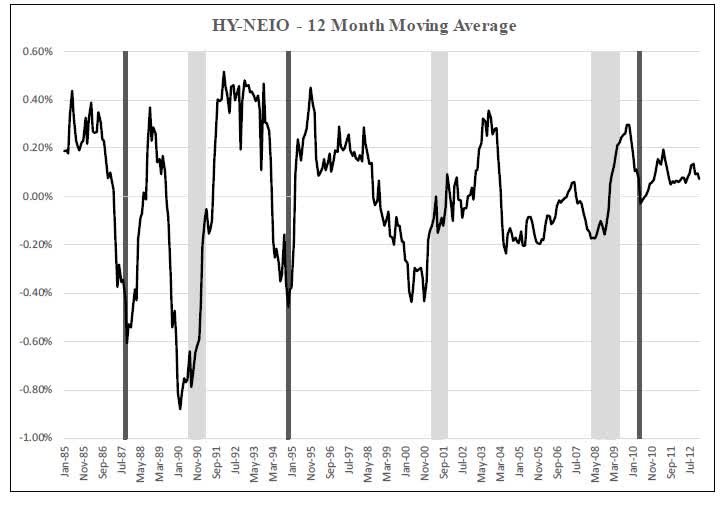

In 2018, we pointed out a Wharton paper written by Azi Ben-Rephael, Jaewon Choi and Itay Goldstein published in September and entitled “Mutual Fund Flows and Fluctuations in Credit and Business Cycles” (h/t Tracy Alloway for pointing this very interesting research paper on Twitter).

This paper points to using flows into junk bond mutual funds as a gauge of an overheated credit market to tell where we are in the credit cycle. Could that be finally a reliable “Boom to Bust” indicator?

“Several measures of credit-market booms are known to precede downturns in real economic activity. We offer an early indicator for all known measures of credit booms. Our measure is based on intra-family flow shifts towards high-yield bond mutual funds. It predicts indicators such as growth in financial intermediary balance sheets, increase in shares of high-yield bond issuers, and downturns of various measures of credit spreads. It also directly predicts the business cycle by positively predicting GDP growth and negatively predicting unemployment. Our results provide support for the investor demand-based narrative of credit cycles and can be useful for policymakers.

A large body of literature in macroeconomics and finance studies the link between credit markets and macroeconomic cycles. A pattern that emerges from the data is that credit booms precede downturns in macroeconomic activity. This pattern attracts considerable attention from academics and policymakers: if credit markets are at the root of macroeconomic fluctuations, then it is important to better understand what drives credit cycles and identify leading indicators to try and design policies that will moderate them.

In this paper we show that investor portfolio choice toward high-yield corporate bond mutual funds is a strong predictor of all previously identified indicators of credit booms. An increase in our measure in year t predicts credit booms marked by the other indicators in the literature in years t+1 and t+2. These other indicators include the proportion of low-quality bond issuers (Greenwood and Hanson, 2013; López-Salido, Stein, and Zakrajšek, 2017), the degree of reaching for yield in the bond market (Becker and Ivashina, 2015), balance sheet growth in financial intermediaries (Schularick and Taylor, 2012; Krishnamurthy and Muir, 2015), and various measures of credit spreads (Gertler and Lown, 1999), in particular the excess bond premium (EBP) recently proposed by Gilchrist and Zakrajšek (2012).

Wharton HY Flows (Wharton)

In addition, our measure, as a leading indicator of credit booms, positively predicts GDP growth and negatively predicts unemployment rates in years t+1 and t+2 (before they turn in the reverse direction in year t+3).” – source Wharton paper, by Azi Ben-Rephael, Jaewon Choi and Itay Goldstein

Given the current rate of outflows and the rapid tightening in “financial conditions”, this is a clear indication that the credit cycle has obviously turned, and default rates are going to spike in the not-so-distant future. As such, watch what credit spreads are doing.

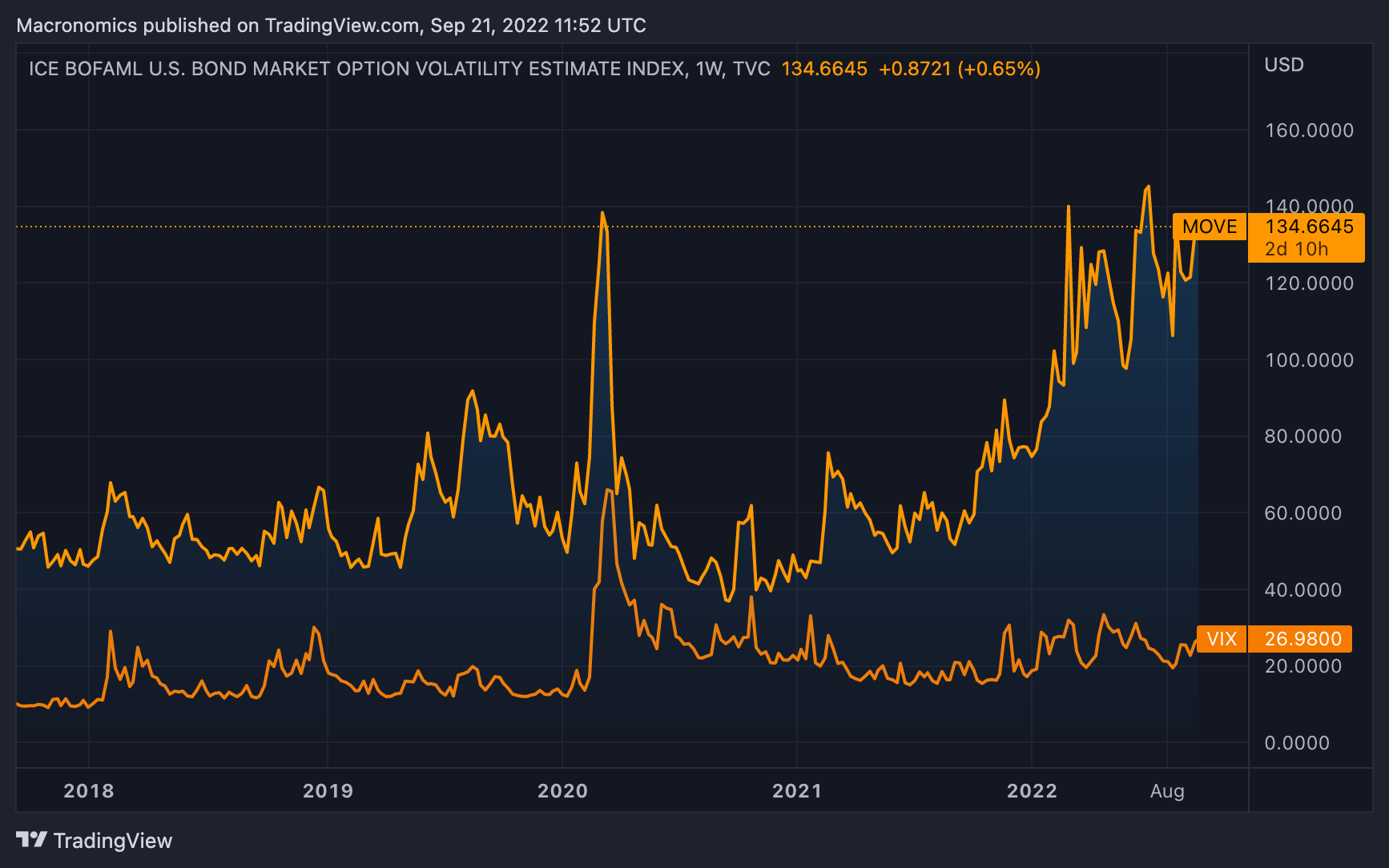

Bond volatility and Mack The Knife (US dollar and real yields) go hand in hand

Any spike in rates volatility is obviously negative for asset prices given carry players, risk-parity investors and other pundits love one thing, and that’s low rate volatility. If you want to understand why asset prices are selling off and why credit markets are feeling the pain. Forget VIX, MOVE matters way more:

VIX and MOVE (TradingView)

As such, both the move in the US Dollar and bond volatility are wreaking havoc on asset prices. Following the most recent Fed hike, the markets are now realizing that indeed, Jerome Powell has some Volcker vibes in him:

FED HIKES (Bloomberg – Twitter)

As we posited on numerous occasions, in terms of the pain inflicted to Emerging Markets, this is our “reverse osmosis” theory playing out:

“In a normal “macro” osmosis process, the investors naturally move from an area of low solvency concentration (High Default Perceived Potential), through capital flows, to an area of high solvency concentration (Low Default Perceived Potential). The movement of the investor is driven to reduce the pressure from negative interest rates on returns by pouring capital on high yielding assets courtesy of low rates volatility and putting on significant carry trades, generating osmotic pressure and “positive asset correlations” in the process. Applying an external pressure to reverse the natural flow of capital with US rates moving back into positive real interest rates territory, thus, is reverse “macro” osmosis we think. Positive US real rates therefore lead to a hypertonic surrounding in our “macro” reverse osmosis process, therefore preventing Emerging Markets in stemming capital outflows at the moment.” – Macronomics, August 2013.

Watching with interest the numerous convolutions in Emerging Markets, with Gold taking the proverbial sucker punch thanks to the bloody rampage of “Mack the Knife” (King Dollar + positive real US interest rates), We discussed in our conversation “Osmotic pressure” back in August 2013 seems to be playing out for the weakest EM “cells” out there:

“The effect of ZIRP has led to a “lower concentration of interest rates levels” in developed markets (negative interest rates). In an attempt to achieve higher yields, hot money rushed into Emerging Markets causing “swelling of returns” as the yield famine led investors seeking higher return, benefiting to that effect the nice high carry trade involved thanks to low bond volatility.” – Macronomics, 24th of August 2013

As we pointed out in our previous conversation:

“Leveraged players and Carry traders do love low risk-free interest rates, but they do love even more low interest rate volatility. This is the chief reason why over the past couple of years, billions of dollars have poured into high yielding assets like risky corporate bonds, emerging market currencies, and dividend paying stocks, driving risk premiums to absurd low levels (as per the levels touched in negative yielding European government bond space…). With rising interest rate volatility, one would expect leveraged players, carry traders and tourists alike to start feeling even more nervous for 2023” – Macronomics September 2022

And, as indicated by David Goldman in 2013:

“Heightened risk translates into a greater desire to hold cash balances (and that means a higher dollar, because most people pay bills in dollars and therefore hold cash balances in dollars). To get higher cash balances, market participants sell things like raw materials.” – David P. Goldman

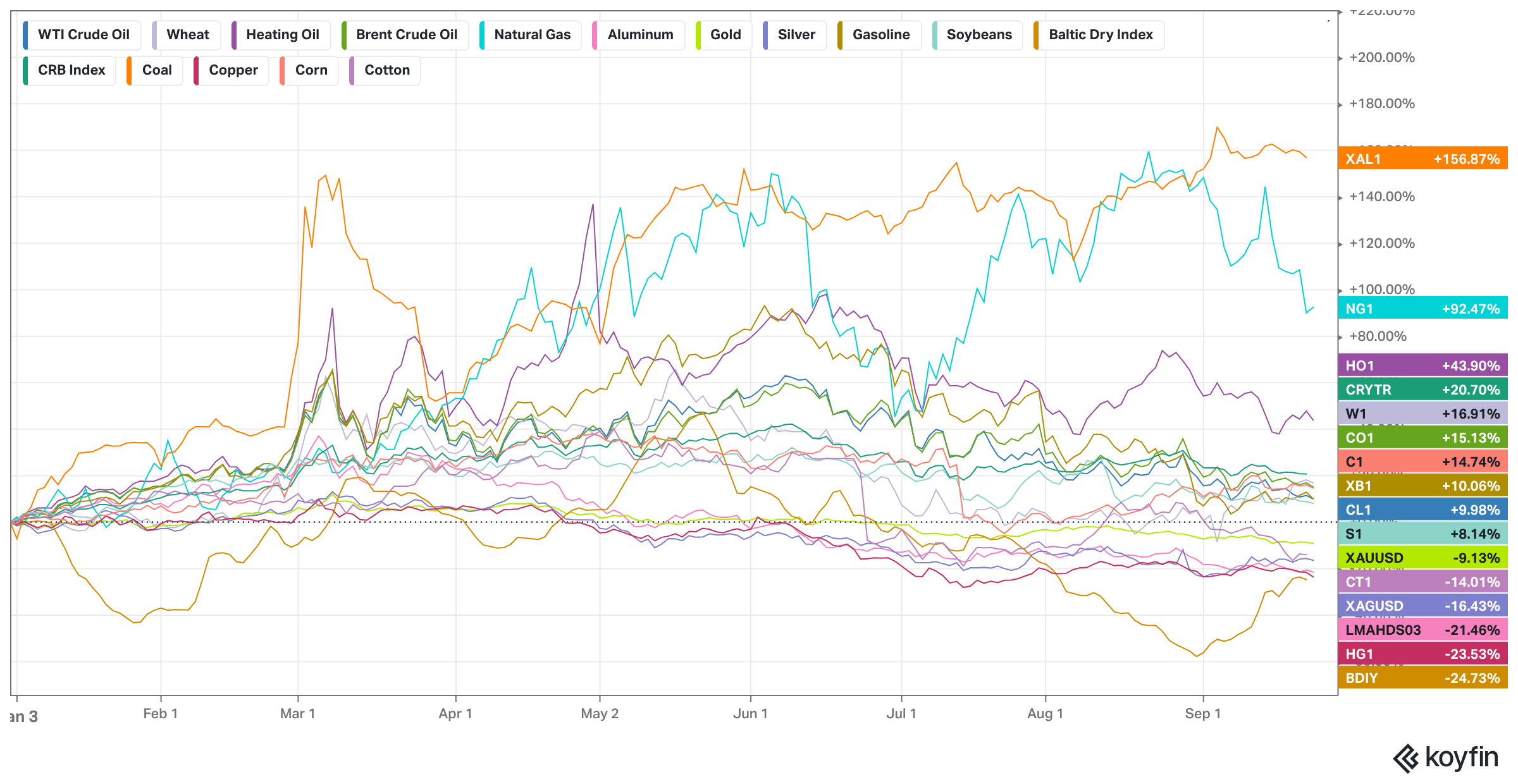

Because of fears of dollar scarcity, thanks to QT and the Fed gradually turning off the monetary spigot, the commodities rout in industrial metals has been about raising dollar cash/playing defense:

Commodities YTD (Koyfin)

Of course, the surge of oil, natural gas and coal can be attributed to the current energy woes plaguing the 27 Club.

On a final note, we could not resist and find it appropriate to quote it again now, given the way we chuckled when we read the following comment from a credit desk in 2016:

“Equities = Hope, Credit = Reality, unfortunately, Reality follows Hope until the Hope dies, then Reality settles in.”

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment