RomoloTavani

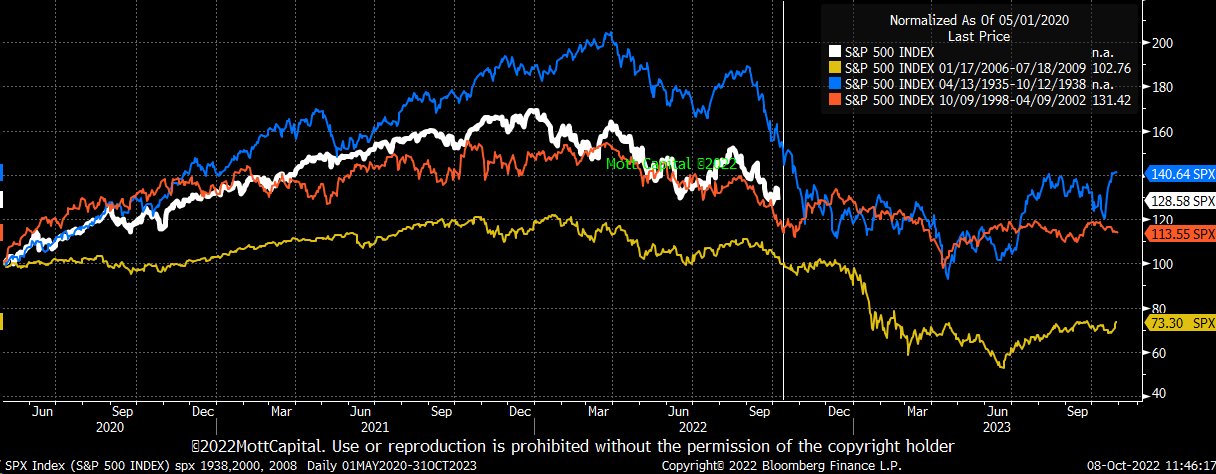

The bear market of 2022 still has further to run based on historical trends and valuations versus interest rates. The 2022 S&P 500 continues to trace bear markets of 1937, 2000, and 2008, which is more an indication of the ebb and flow of human nature than past and future events.

The mid-August peak served as another turning point for the S&P 500, leading to a new September low. At this point, the historical references of the great bear markets of the past suggest another low is due sometime around October 25, give or take a couple of days, followed by an upward move and perhaps some consolidation.

Bloomberg

An October New Low?

From a perspective of events that could lead to a continued decline and bottom at the end of October, a better-than-feared earnings season could be one such event. Whether a late October low will be the bottom or a short-term low is yet to be seen, but given how high valuations are, more work will need to be done for the bottom to be put in place.

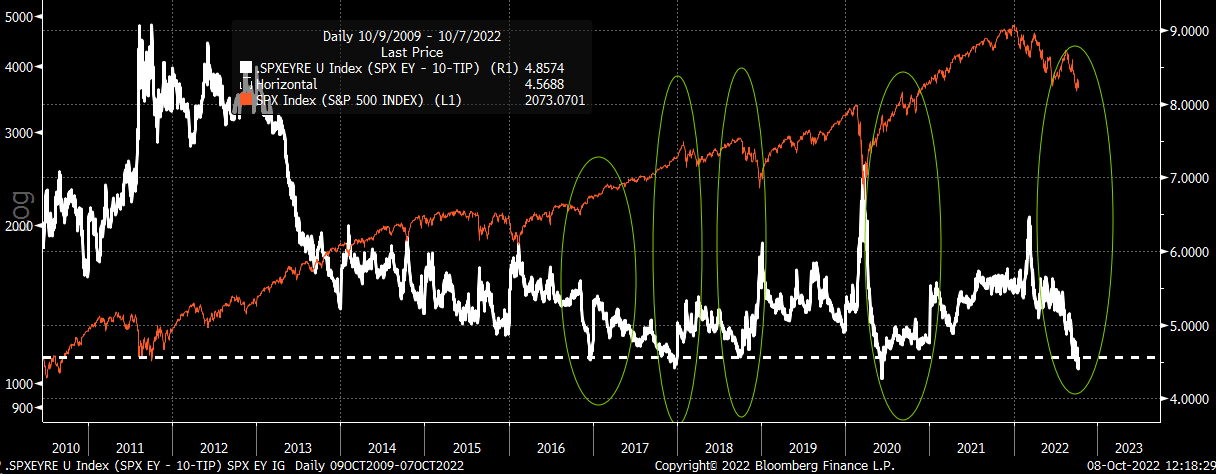

It’s All About Rates

The S&P 500 earnings yield for 2022 minus the 10-Yr real yield is currently 4.56%. Historically, that is at the lower end of the range and associated with market tops, not bottoms. For example, the 4.5% region was visited in December 2016, January 2018, October 2018, and June 2020. The only case that didn’t see a significant decline was in December 2016, when the index consolidated sideways for nearly three months.

Bloomberg

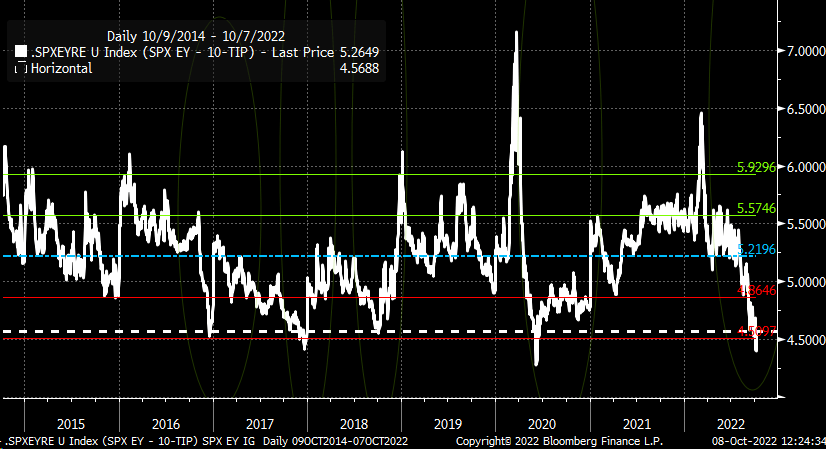

Since 2014, the average spread between the S&P 500 current year earnings yields and the 10-Yr real yield has been around 5.2%, with a standard deviation range of 4.87% to 5.57%. Currently, the S&P 500 premium to the 10-yr TIP is more than two standard deviations from the average. The spread would need to rise by 30 bps to get the index back to within one standard deviation, or by 65 bps to return to the historical average.

Bloomberg

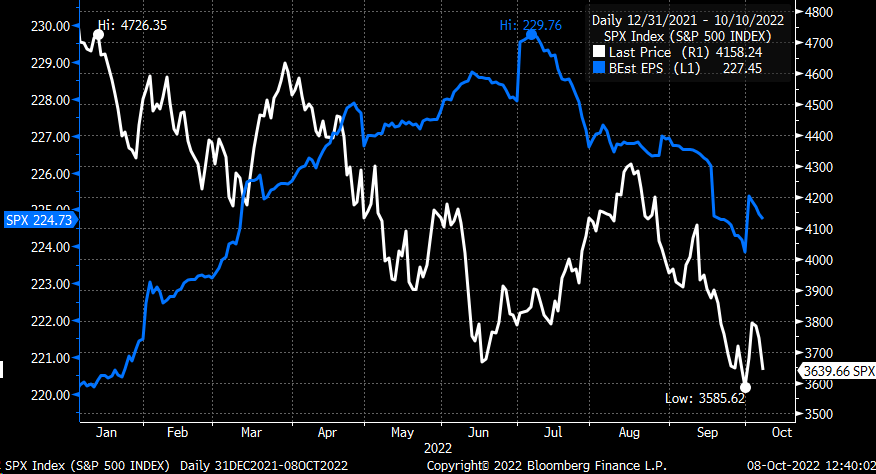

Another 9% Decline?

The S&P 500 has an earnings yield based on 2022 earnings estimates of 6.17%. An increase of 30 bps would increase the yield to 6.47%, and an increase of 60 bps would increase the yield to 6.77%. The earnings yield is simply the inverse of the PE ratio, which means the current PE ratio is 16.2 and would need to fall to 15.4 or 14.7 to bring the S&P 500 back to a historically average fair value.

With the earnings estimates for 2022 currently tracking at $224.73, it would value the S&P 500 in a range of 3,460 to 3,300. That would equal a further decline in the index of around 5% to 9%.

Bloomberg

What will tell us when this bear market is over is more likely to be interest rates and the dollar index, as these will likely provide a much better signal than other metrics. Because if rates continue to rise, the S&P 500 will need to continue to decline with the pace of rates risings.

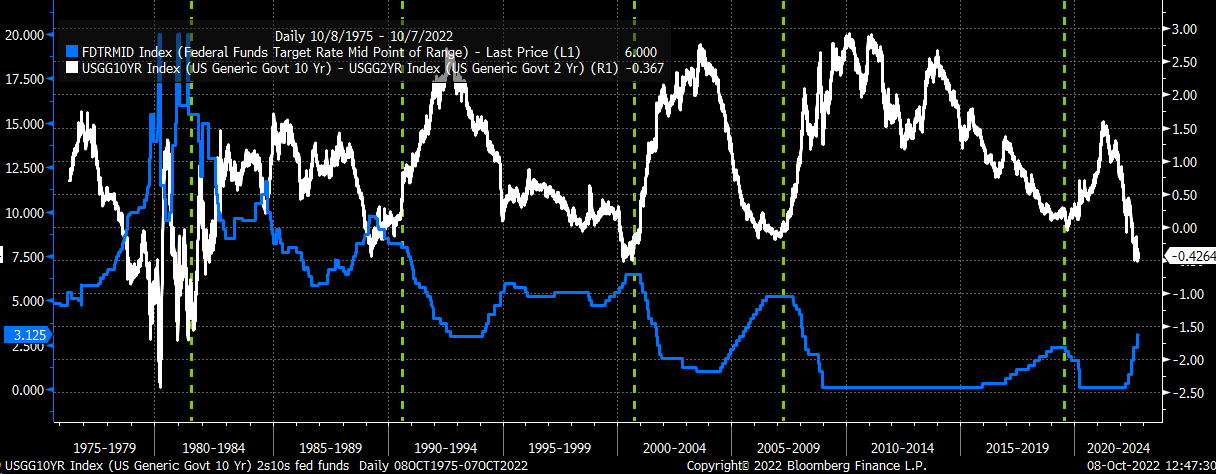

Rate Cuts?

Typically, the 10-year minus the 2-year spread tells us when the Fed is about to start cutting rates. It is at the point where the spread begins to rise that tends to serve as the best reference for the end of a rate-hiking cycle and the start of a rate-cutting cycle.

Bloomberg

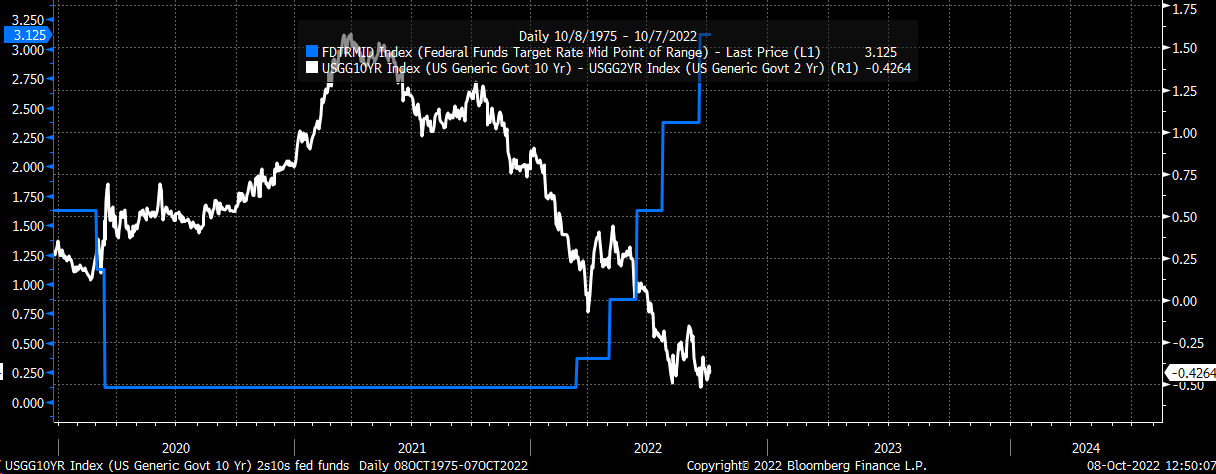

As the market anticipates Fed rate cuts, the 2-Year yield begins to fall back to the 10-Year. It is the opposite, with the 10-2 year spread just recently making a new low in September and showing very little if no signs of turning higher.

Bloomberg

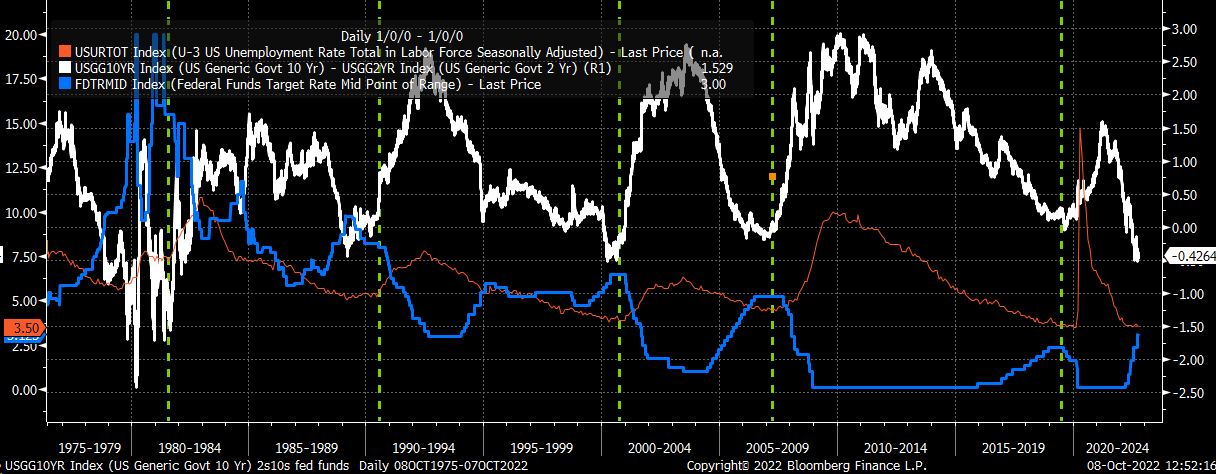

Meanwhile, the best way to determine when the 10-2 Year spread may begin to rise is by looking at the unemployment rate because that tends to be a very good predictor of where yields are heading. Typically, when the unemployment starts to run higher, it indicates that the 10-2 year spread will widen, suggesting a rate cut cycle is near.

Bloomberg

In this case, Friday’s job report showed the unemployment rate fell to 3.5% from 3.7% last month and back to its July lows. That leaves the spread between the ten and 2-year Treasury nowhere close to putting in a bottom, and means the Fed is probably nowhere close to finishing its rate hiking cycle.

If the Fed is nowhere close to finishing its rate hiking cycle, then rates probably aren’t finished rising. Thus, the equity market bear market cycle probably still has further to run, even if the equity market finds a short-term bottom at the end of October.

Be the first to comment