Justin Sullivan

This article first appeared in Trend Investing on September 5 but has been updated for this article.

Following the recent passing of the Inflation Reduction Act (US$369b for climate change), it has now become very important for companies wanting to sell EVs in USA to meet the new rules so they remain competitive and qualify for half or all of the US$7,500 electric car subsidy.

Key points of the Inflation Reduction Act (qualification requirements)

- 50% of the $7,500 subsidy – Electric cars are manufactured or assembled in North America.

- 50% of the $7,500 subsidy – An escalating % of the EV’s raw materials must be extracted or processed in the US or a US free-trade partner.

- Exclusion: From 2025, any of the applicable critical minerals contained in the battery of the vehicle were extracted, processed, or recycled by a “foreign entity of concern”.

Note: The last dot point above basically rules out batteries coming from China unless we see any amendment.

Summary of the key EV-related changes in the Inflation Reduction Act

On August 9, Green Car Congress reported:

Inflation Reduction Act mandates escalating battery critical mineral requirements to qualify for EV tax credit……Among the changes are an extension of the tax credit through 2032, the removal of the unit-sales cap of 200,000 per OEM, and a new mandate for qualified cars being assembled in North America. Further, the bill as currently written mandates escalating levels of critical minerals to be sourced from the US or a country with a free-trade agreement with the US……Specifically, the bill requires (Part 4, Sec. 13401. subsection [E](1)[A]) that the “percentage of the value” of the applicable battery critical minerals (as defined later in the bill) extracted or processed in the US or a US free-trade partner or recycled in North America, be:

40% for a vehicle placed in service before 1 January 2024;

50% for a vehicle placed in the service during calendar year 2024;

60% for a vehicle placed in service during calendar year 2025;

70% for a vehicle placed in service during calendar year 2026; and

80% for a vehicle placed in service after 31 December 2026.

The bill places similar restrictions on the percentage of value of the components, but leading up to a 100% requirement for vehicles placed in service after 31 December 2028. The bill then goes on to exclude specifically any vehicle placed in service after 31 December 2024….. which any of the applicable critical minerals contained in the battery of the vehicle (as described in sub-section [E](1)[A]) were extracted, processed, or recycled by a “foreign entity of concern”……There are 72 EV models currently available for purchase in the United States including battery, plug-in hybrid and fuel cell electric vehicles. Seventy percent of those EVs would immediately become ineligible when the bill passes and none would qualify for the full credit when additional sourcing requirements go into effect. Zero.

Comment

The above changes will potentially have a profound effect, as intended, to rapidly create a North American (and USA free trade countries) supply chain. This supply chain will need to very urgently develop battery materials processing and mining, or risk missing part of the subsidies, and hence be at a disadvantage to competitors.

The USA has around 15 battery megafactories in planning, including potentially two from Panasonic Corp. [TYO:6752] (OTCPK:PCRFY) (to supply Tesla (TSLA)). The question is where will they source their raw materials and where will they be processed, so as to meet the Inflation Reduction Act requirements?

And the answer is quite obvious? North America (notably Canada) and Australia. Both Canada and Australia have abundant battery and EV raw materials and are considered safe and friendly countries by the USA, qualifying for the Inflation Reduction Act.

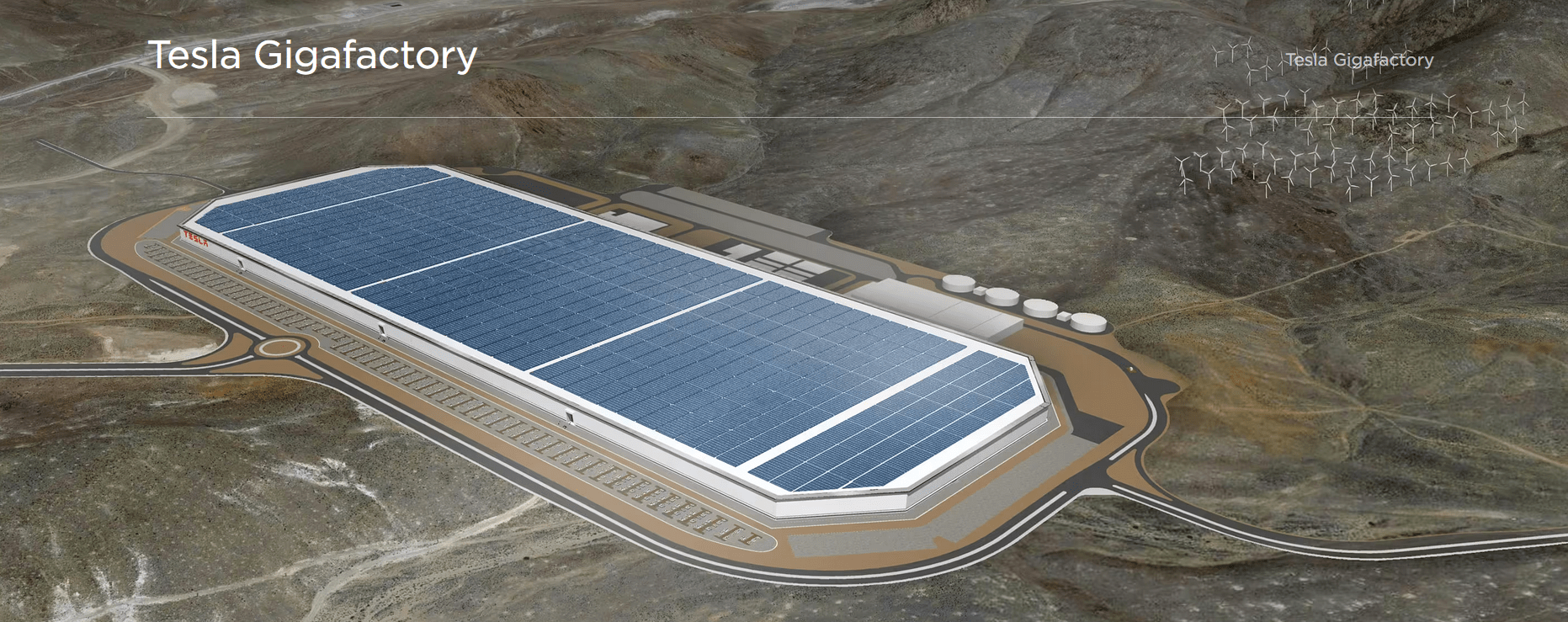

Schematic image of Tesla’s first battery gigafactory – Giga Nevada

Tesla

Tesla’s next gigafactory will likely be in Canada

Our forecast is that Tesla will soon announce Canada as its next gigafactory location, to supply Tesla’s (and Panasonic’s future) USA EV manufacturing plants. Some details of our thoughts:

Q4, 2022 – New Tesla battery gigafactory and/or LiOH/Li carbonate/Li phosphate conversion plant in Canada to be announced. Possible also for a cathode facility with nickel and cobalt processing. May also be a JV. Spodumene supply initially potentially from NAL (75% Sayona Mining [ASX:SYA] (OTCQB:SYAXF)/ Piedmont Lithium [ASX:PLL] (PLL)) and potentially Nemaska Lithium (50% Livent (LTHM)) or other Canadian juniors in time. Production to potentially start by 2025.

We think an electric vehicle factory in Canada is possible, but not that likely.

- Piedmont Lithium Signs Sales Agreement With Tesla (was based on the Carolina Lithium Project in USA)

Tesla’s next factory (or gigafactory) after Canada maybe in Australia

With less confidence, we view Australia as a possible next site after Canada for a factory (or gigafactory), quite possibly a LiOH/Li carbonate/Li phosphate conversion plant, most likely in Western Australia. Some details of our thoughts:

2023 – New Tesla or Tesla JV LiOH/Li carbonate/Li phosphate conversion plant in Western Australia to be announced. Spodumene supply from Liontown Resources [ASX:LTR] (OTCPK:LINRF) (from 2025) and potentially Pilbara Minerals [ASX:PLS] (OTCPK:PILBF) (from 2025) and Core Lithium [ASX:CXO] (OTCPK:CXOXF). Production to potentially start by 2026.

Regarding lithium supply which is key for Tesla this decade to maintain EV production ramping at 50% pa

If Tesla was to do similar to the above ideas (lithium conversion facilities in Canada and Australia) with a total of 60,000tpa LCE production (30,000 from each), then that would secure Tesla enough lithium to supply 1.2m additional Tesla Model Y/3 RWD cars per year or 600,000 Cybertrucks per year.

The CapEx cost for LiOH/Li carbonate/Li phosphate conversion facilities would be about US$1.2b (US$600m each). Opex would be the cost of spodumene plus about US$2-3,000/t conversion costs, so a lot better than paying market prices for LiOH/Li carbonate/Li phosphate.

Tesla already has off-take agreements with Piedmont (albeit from the stalled Carolina Lithium Project) and Liontown Resources (up to 150,000tpa spodumene). By mid-2024 to 2025, Pilbara Minerals will have an additional ~300,000tpa of spodumene available as they expand to 1mtpa with their P1,000 plan.

- EV Makers Must Partner With Miners to Secure Key Metals. “Australia-based lithium producer Pilbara Minerals says the industry needs more joint ventures to boost refining of battery raw materials.”

Finally, the above plan would all fit the Inflation Reduction Act (“IRA”) that requires EV manufacturing/assembling in North America and 40% (ramping higher this decade) of raw materials supply from North America or free trade agreement countries such as Australia. Note also to get the new subsidy in USA Tesla would not be able to source from China or so-called unfriendly countries. Hence the urgency for Tesla to build a new ‘U.S. friendly’ supply chain, starting from 2024 (based on the current outline in the IRA).

While the above is ‘hypothetical’, it really becomes quite important to a) Secure EV raw materials supply (especially lithium), and b) Qualify for U.S. EV subsidies.

Companies most likely to benefit

The companies most likely to benefit from Tesla building an ore processing/conversion facility in Canada and Australia have already been mentioned above in the article. Over time, the lithium juniors with mid-term production potential could also benefit.

The companies most likely to benefit from Tesla building a gigafactory in Canada are:

Lithium: See article

Spherical Graphite – Syrah Resources [ASX:SYR] (OTCPK:SYAAF) (off-take deal with Tesla), Nouveau Monde Graphite Inc. [TSXV:NOU] (NMG) (“Tesla visits graphite mine and factory in Quebec”).

Synthetic Graphite – Novonix Limited [ASX:NVX] (NVX) (Anode Materials division, located in Chattanooga, Tennessee, USA).

Nickel and Cobalt – Vale S.A. (VALE) (off-take agreement with Tesla), BHP Group (BHP) (off-take agreement with Tesla), and some juniors such as potentially Electra Battery Materials [TSXV:ELBM] (ELBM) (Quebec Battery Valley (Becancour)) is also home of Electra Battery Materials), Talon Metals [TSX:TLO] (OTCPK:TLOFF)/Rio Tinto [ASX:RIO] (RIO) JV and others.

Rare earths – MP Materials Corp. (MP), Lynas Rare Earths Limited [ASX:LYC] (OTCPK:LYSCF), Vital Metals [ASX:VML] (OTCQB:VTMXF).

Further reading

Tesla Model 3 and Model Y continue to be highly popular with EV buyers – Source: Tesla

Tesla website

Conclusion

It is looking increasingly likely that Tesla will announce Canada as their next gigafactory location within the next few months (Q4, 2022). Our view is this is maybe some battery materials conversion facility (most likely lithium, but also perhaps nickel and cobalt). It could also be a battery gigafactory. Probably in Becancour, Quebec region or Thunder Bay, Ontario region. Canada looks very likely given its abundance of battery raw materials and proximity to the USA.

We also see a chance Tesla’s next move would be something similar, but this time in Western Australia, to again take advantage of the locations abundance of battery raw material projects.

This article contains our best thoughts and research; however, Elon Musk may well do something unusual and completely different.

As usual, all comments are welcome.

Be the first to comment