Xiaolu Chu

Thesis

Tesla, Inc. (NASDAQ:TSLA) CEO Elon Musk heads into his company’s highly anticipated Q2 report card with the headlines that he probably didn’t envisage at the start of 2022. Notwithstanding, dealing with several tough challenges is not insurmountable to Musk. He arguably had tougher calls to make in Tesla’s earlier days as it struggled to stay out of bankruptcy at times.

However, Tesla is no longer the upstart EV maker but a global leader with a market cap of $729B. Therefore, much is at stake for investors who are parsing the growth trajectory of TSLA at its current valuation. Investors will ask whether TSLA can continue the monstrous growth it achieved over the past few years.

Therefore, the recent headlines that suggested BYD Company (OTCPK:BYDDF) significantly outperformed Tesla in China’s NEV wholesale shipments in June weren’t going to augur well. Notably, it occurred despite Giga Shanghai notching an incredible month in June, shipping a record 78.9K vehicles. Hence, the competition is heating up rapidly in China, as BYD reportedly plans to meet a 300K monthly production target in August.

Some Tesla commentators highlighted that about 50% of BYD’s H1’22 NEV sales were attributed to BEV, with the rest hybrid. Sure, Tesla is still the King of BEV. But, investors need to ask themselves why Chinese consumers have propelled BYD to the top of the NEV ranking in China with hybrids. What matters is that BYD’s NEV portfolio has delivered a massive breakthrough in China, and consumers are lifting its sales above Tesla.

Coupled with its “money furnaces” of Berlin and Texas, the Street has justifiably lowered Tesla’s estimates markedly. However, the market has already de-rated TSLA since April. As price action is forward-looking, investors need to ask what it takes for the market to re-rate TSLA again, heading into its Q2 card.

The Market Has De-rated TSLA

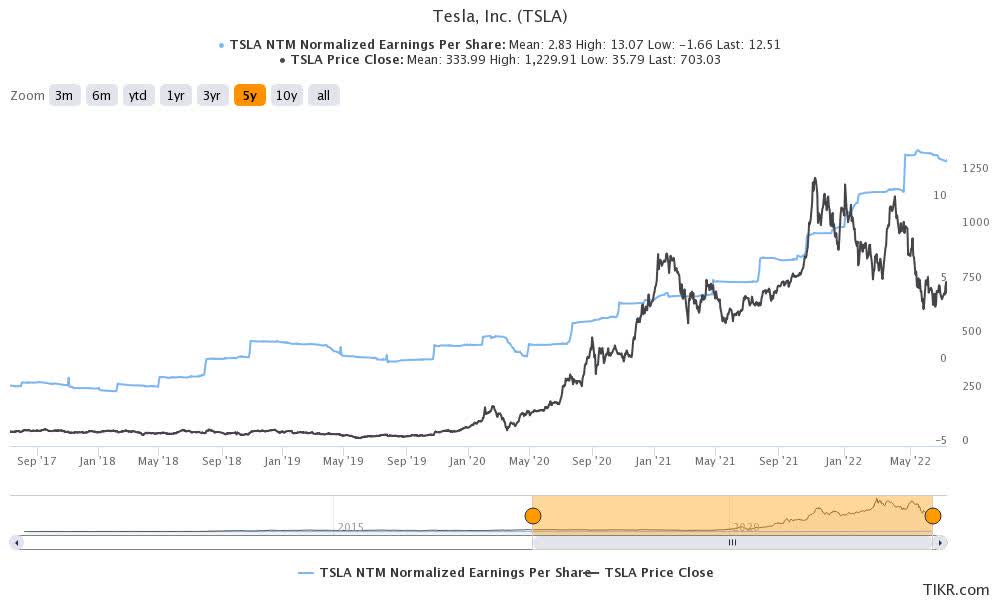

TSLA EPS trend (TIKR)

Investors can glean the relationship between TSLA’s adjusted EPS trend and its price over the past five years. The gap closed markedly since TSLA’s massive surge from its March 2020 COVID bottom.

However, that trend has deviated since its April highs, as the market de-rated TSLA. We think the bifurcation is now apparent. Can TSLA close the gap with its EPS estimates trend? Will Q2’s report card justify a re-rating of TSLA given the markedly lower expectations?

Unfortunately, we think the market has been on point. We discussed in our previous article why the market formed those ominous bull traps (significant rejection of buying momentum). It demonstrated that the market wouldn’t let the buying upside carry on further. But why?

A Q2 Beat Is Unlikely To Undo Tesla’s Malaise

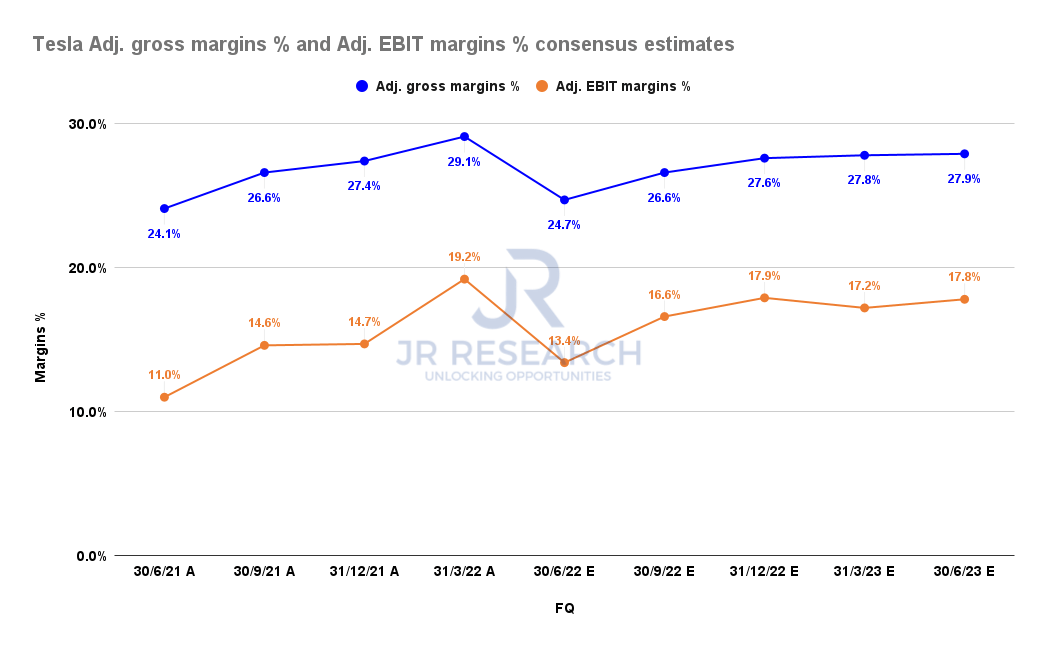

Tesla adjusted gross margins % and adjusted EBIT margins % consensus estimates (S&P Cap IQ)

We cautioned investors in our Q1 update that Tesla could find repeating its gross margins performance unlikely, even before the headwinds hit it hard. However, the bullish Street analysts were still highly optimistic about its ability to sustain its performance then. But, things have changed markedly since its April optimism (again, price action preceded the analysts’ downgrades).

As seen above, the consensus estimates (bullish) on Tesla’s Q2 overall gross margins have been revised markedly to 24.7%, way below Q1’s 29.7%. Consequently, Tesla is projected to post an adjusted EBIT margin of 13.4%. If it pans out, it would be Tesla’s worst performance since the lows in Q2’21.

Moreover, Tesla is not projected to recover its Q1 peak through Q2’23. Nevertheless, we think the estimates are credible with the Street’s inherent optimism, headwinds in Berlin and Austin, and tougher competition in its global markets.

So, Tesla’s margin profile improvement is not looking as good as before.

Tesla revenue change % consensus estimates (S&P Cap IQ)

In addition, Tesla’s revenue growth is expected to decelerate markedly and is trending down on average. Therefore, we believe that investors should be able to gain more fundamental insights from the market’s de-rating of TSLA. For a premium-priced stock, the market will not cut TSLA any slack.

The company needs to deliver almost perfect report cards quarter after quarter. There’s simply no room for error, whether the headwinds are directly attributed to Elon Musk or not.

So, we think even a Q2 beat will not lead to the re-rating of TSLA. Unless Tesla can communicate a growth trajectory way ahead of the Street’s estimates, the embedded premium is not helping matters.

And recall that Elon Musk emphasized in Tesla’s Q1 call that it can produce “over 1.5M cars” in 2022. However, the revised consensus estimates downgraded that expectation, indicating 1.39M in FY22. Therefore, a material de-rating could follow if Musk updated an even lower guidance than the Street’s lowered bar.

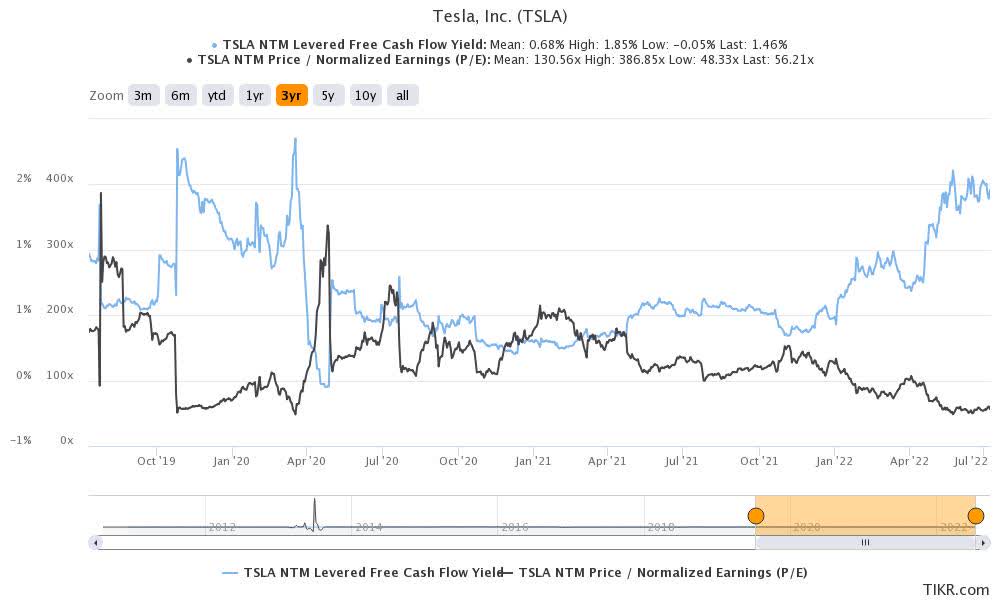

TSLA – Overvalued At 1.5% FCF Yield Or 56x NTM P/E

TSLA valuation metrics (TIKR)

The market has consistently supported TSLA stock at close to 50x P/E previously. But, recall that Tesla delivered a revenue CAGR of 50.4% over the past five years. As a result, the market was willing to cut TSLA some leeway as it led the world in the transition to EVs.

However, it’s clearer that Tesla could even be losing that lead in China to BYD and possibly much tougher competition in Europe and the US as the legacy OEMs continue to grind for output.

Therefore, investors must ask whether it still makes sense for the market to re-rate TSLA at >50x P/E as growth and profitability could have peaked in the medium term? We think probably not.

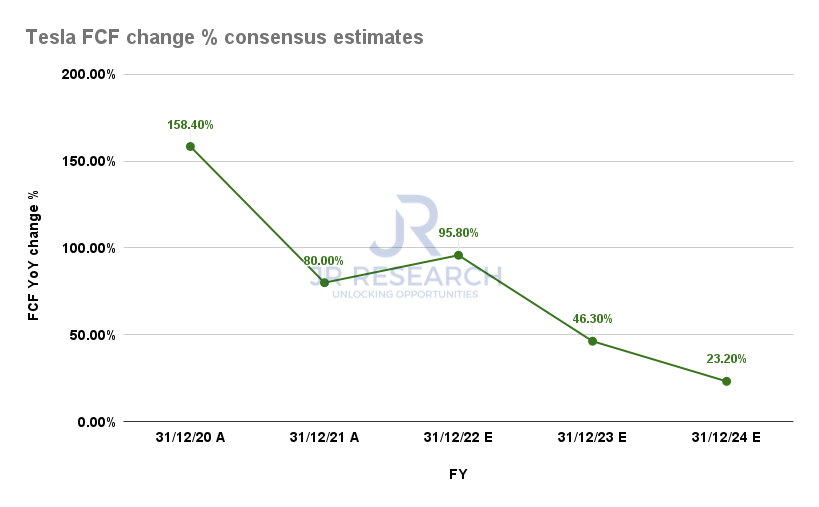

TSLA FCF change % consensus estimates (S&P Cap IQ)

How about Tesla’s free cash flow (FCF)? With markedly slowing revenue growth, it makes sense that the market turns its attention to its FCF growth.

Unfortunately, investors will likely need to prepare for massive disappointment here. Tesla’s FCF growth is projected to slow dramatically through FY24, reaching 23.2%.

We believe the market’s de-rating is justified with an NTM FCF yield of just 1.5%. TSLA is overvalued. It simply cannot justify its growth cadence any further.

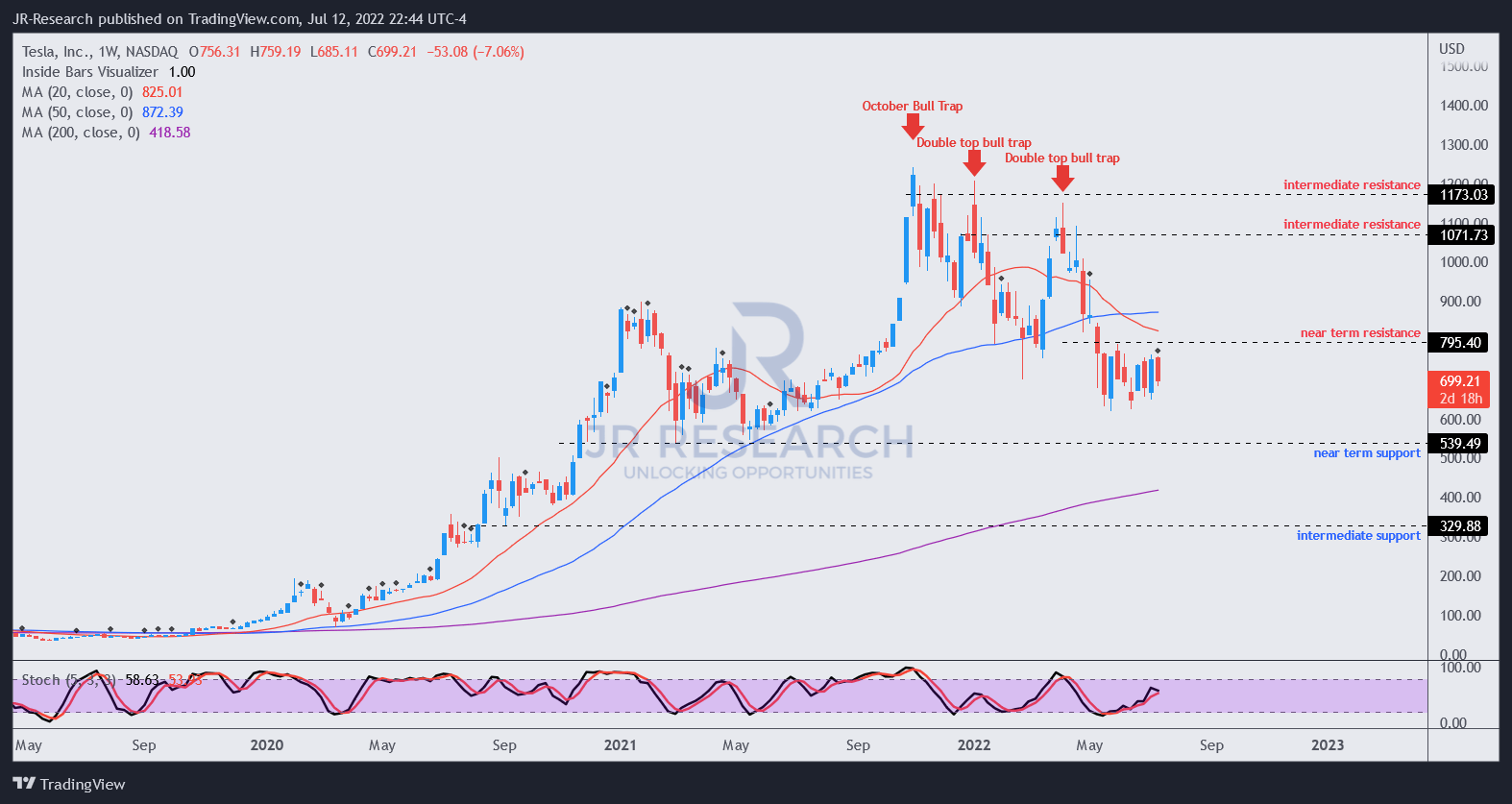

TSLA – Bullish Momentum Is Gone

TSLA price chart (TradingView)

There have been significant developments since our last update on its price action. Notably, the near-term resistance ($800) has been validated, as TSLA remains mired below it. Notwithstanding, it remains to be seen whether the current zone is an accumulation or distribution phase.

However, we posit that the market is likely to de-rate TSLA further. Note that it has already lost its bullish bias. Furthermore, it’s starting to move into a downtrend (not validated yet). Coupled with the validation of its near-term resistance, the market could form another lower-high bull trap before forcing TSLA lower.

Therefore, investors are urged to let the price action play out and not add to the current levels. A further retracement to its near-term support ($540) looks increasingly likely.

Instead, investors should consider executing directionally bearish set-ups at appropriate price levels to capitalize on TSLA’s bearish bias.

Is TSLA Stock A Buy, Sell, Or Hold?

We reiterate our Hold rating on TSLA.

The expectations on Tesla’s Q2 card have been revised markedly downwards. So, unless Tesla delivers a hugely overwhelming card, we believe it’s unlikely to move the needle on TSLA stock in the near term. Instead, we posit that the market could likely focus on what Elon Musk guides for FY22’s delivery, given the headwinds seen in Q2. The Street is looking at 1.39M against Musk’s Q1 guidance of over 1.5M.

Moreover, TSLA stock remains overvalued, given markedly slowing growth estimates. Coupled with a bearish bias and a recently validated resistance zone, we urge buyers to avoid adding at the current levels.

Be the first to comment