BlackJack3D

Investment Thesis

Tenable Holdings Inc (NASDAQ:TENB) is a high-growth technology company with top-line revenue growth in the high double-digit percentages on a YoY basis.

It is sustaining huge accounting losses, mainly due to a high amount of non-cash Stock-Based Compensation (“SBC”). However, the SBC amount is relatively reasonable when compared to its much higher amount of revenue generated.

TENB maintains a healthy balance sheet with substantial liquid assets of cash and short-term investments. Its debt might be rising but the debt servicing ratio is low and manageable.

The company is positive in free cash flow for the last 3 years and is currently significantly undervalued. In my opinion, this presents a good investment opportunity for investors.

Company Overview

TENB offers solutions for the emerging cybersecurity subcategory known as Cyber Exposure. Tenable.io and SecurityCenter are two examples of the company’s enterprise products. Networking infrastructure, desktops, and on-premises servers are just a few examples of the traditional IT assets that Tenable.io controls and measures for cyber risk. It is possible to run the Security Center on-premises, in the cloud, or in a hybrid environment. Security Center is designed to manage and measure cyber exposure across traditional IT assets. It supports a number of sectors, including finance, healthcare, retail, energy, and others. In addition to the Asia Pacific, TENB is present in the Americas, Europe, the Middle East, and Africa.

The company derived the lion’s share of its profits from recurring subscription arrangements, as noted in the latest annual report:

Our recurring revenue, which includes revenue from subscription arrangements for software and cloud-based solutions and maintenance associated with perpetual licenses, represented 94.6%, 93.6% and 91.8% of revenue in 2021, 2020 and 2019, respectively.

Income Statement Analysis

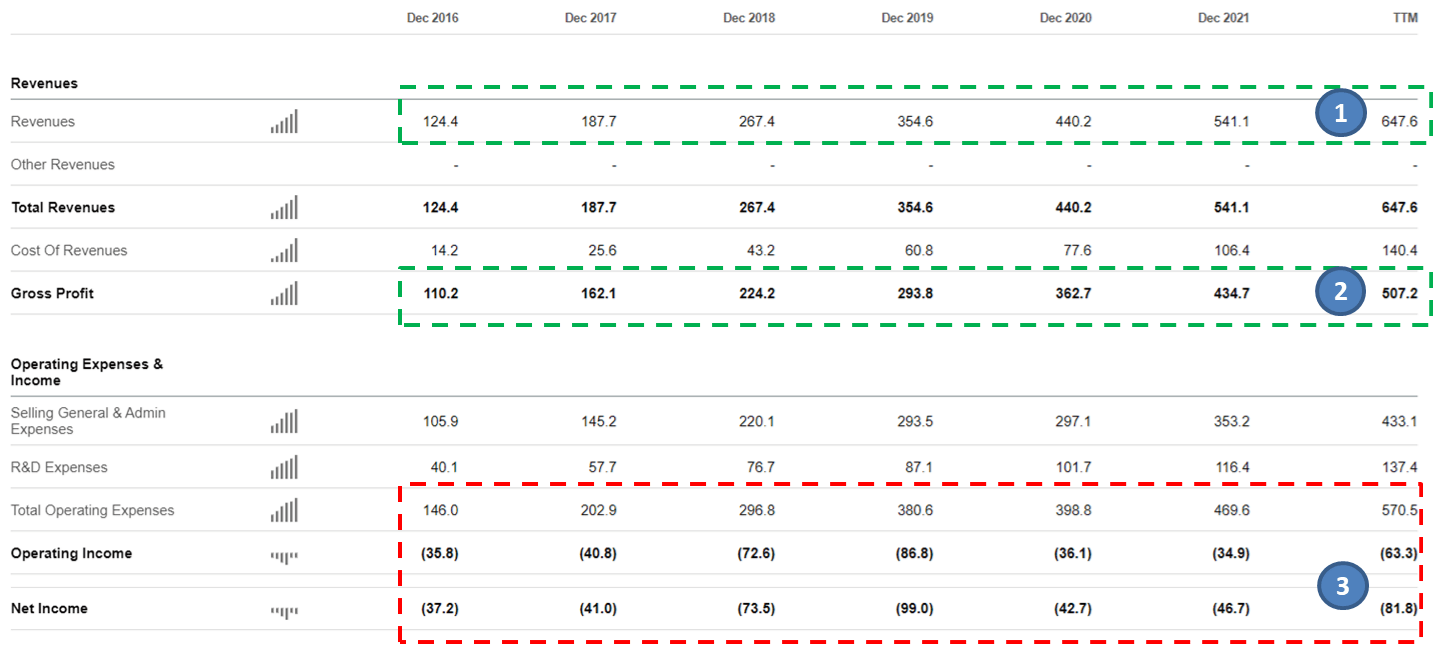

We will look at some key financial figures from Seeking Alpha’s Income Statement to get some insights:

Income Statement (Seeking Alpha)

Here are some observations:

- TENB has maintained a very favorable top-line growth since 2016. The growth has been more than 20% on a YoY basis.

- The cost of revenue has been kept low enough to allow the benefits from the rising top line to trickle down to the gross margins. TENB has consistently maintained an envious gross margin of more than 80%.

- Unfortunately, the operating costs of such high growth are just as enormous. Operating expenses have been consistently increasing since 2016 and there is no sign that it is slowing down.

- The effect of such high operating expenses manifests itself in the bottom line of operating and net income. Both are currently in negative territory at the moment.

Overall, in my opinion, TENB fits the profile of a high-growth but still unprofitable technology business. In the current environment of rising inflation, this is fundamentally a headwind that a company of such profile needs to deal with.

Balance Sheet Analysis

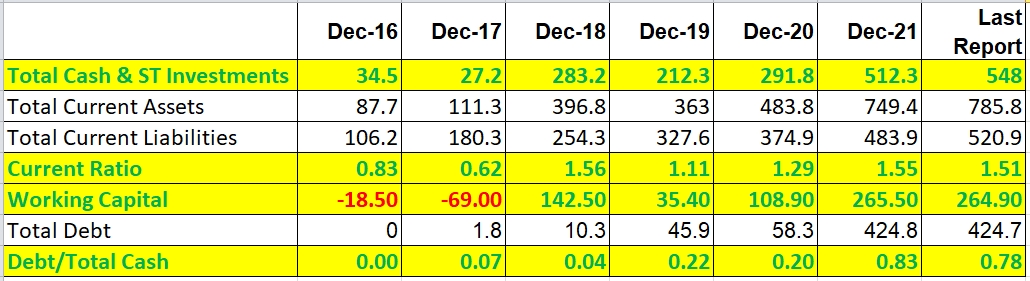

We will look at some key financial figures from Seeking Alpha’s balance sheet.

Balance Sheet (Seeking Alpha)

We can observe that:

- The TENB has consistently maintained a positive amount of liquid assets (Cash and ST investment) since 2016.

- From 2018, its current ratio was greater than 1, meaning that over the years, the company has accumulated more assets than liabilities to maintain positive working capital.

- The company’s Total Debt has been consistently increasing since 2016 and this could be a concern if this increment goes out of control. Fortunately, when compared with the total amount of cash on TENB’s balance sheet, the debt volume has been kept relatively lower than the amount of cash it is holding. This means the company has the means to pay up all these debts using only their liquid cash assets if they ever chose to do so.

- Still, the current total “debt/total cash” currently sits at 0.78, which is inching close to the amount of cash it has on the balance sheet. In the long run, it is unclear whether the company’s debt will eventually outstrip its cash on the balance sheet.

In the short term, TENB will need to make sure it can still service the interest expenses incurred on its debt. Ideally, in my opinion, the company should be able to service all its interest expenses using its cash flow generated from core operations. If this is not possible, the company will have to issue more shares to raise capital, which dilutes shareholders’ interest.

Alternatively, refinancing its debt at the mercy of an unfavorable environment of rising interest rates is also not ideal.

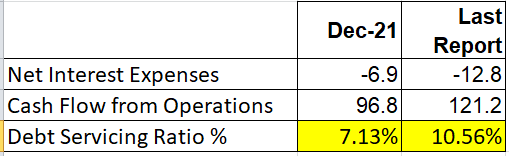

To understand if the company is able to pay off its interest expenses, we calculate the “Debt Servicing Ratio” by comparing the “Net Interest Expense” against the “Cash Flow from Operations”.

Debt Servicing Ratio (Seeking Alpha)

Right now, we can see the “debt servicing ratio” is approximately 10%. In my opinion, a figure that is less than 30% is considered healthy and not a cause for concern.

Still, this figure has increased from 7.13% in Dec-21 to 10.56% in the last reported period. Investors should monitor whether the debt servicing ratio will go out of control in the long run.

Overall, in my opinion, as of now, TENB has maintained a very healthy balance sheet.

Cash Flow Analysis

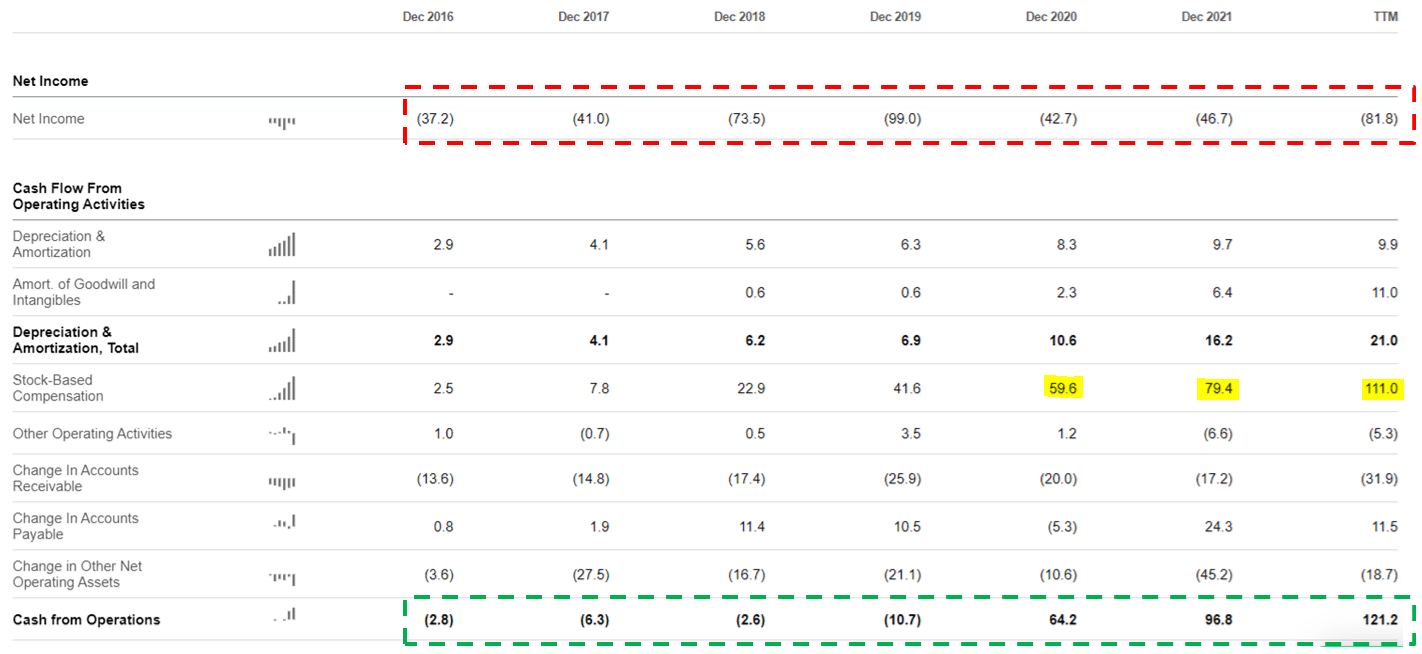

We will look at some key financial figures from Seeking Alpha’s Cash Flow Statement:

Free Cash Flow (Seeking Alpha)

We can observe that the company used to be operating with a negative cash flow profile until the financial year of 2020 when it turned positive for the first time. Since then, its cash position has gotten better. If we include the company’s CAPEX, its latest free cash flow now sits at $104.5M

Overall, over the last 3 years, the company’s free cash flow is growing at a CAGR of 33.52%.

Stock-Based Compensation

Analyzing the cash flow statement also reveals the fact that the company is spending a lot on SBC.

As discussed in an earlier section, the company is unprofitable in Net Income. Most of the cost is due to a large amount of non-cash SBC cost. If we just add back this cost item to the net income, TENB can easily achieve positive cash flow.

Stock-Based Compensation (Seeking Alpha)

As noted in the company’s latest annual report describing its Operating Expenses, SBC is one of the major contributors to its operating costs.:

Personnel costs are the most significant component of operating expenses and consist of salaries, benefits, bonuses, payroll taxes, stock-based compensation and any severance.

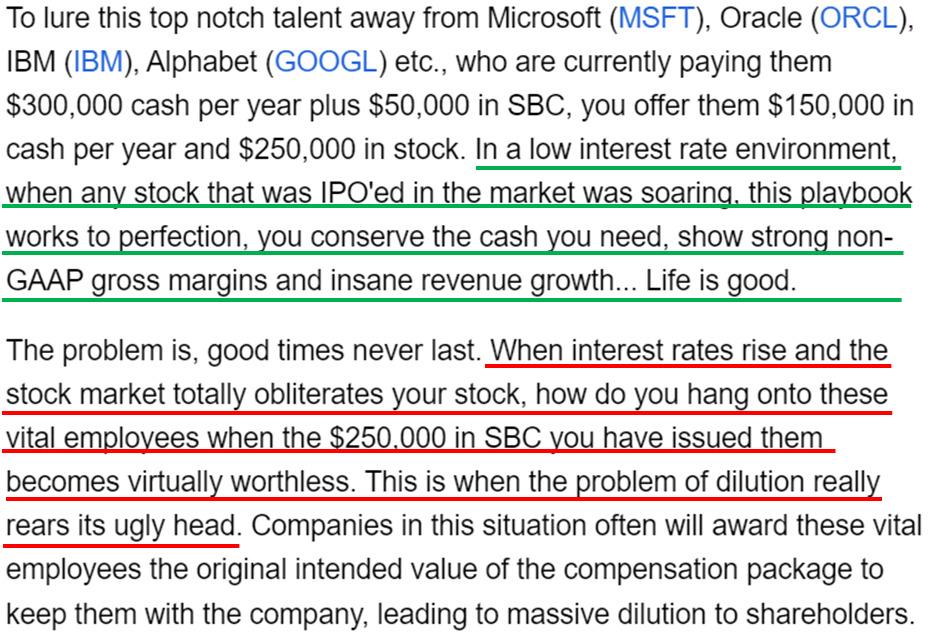

Relatively small, growing tech companies like TENB like to use SBC to reward their employees to stay with the company and benefit from the company’s rapid growth. SBC is not without risks. In my opinion, this recent article from Seeking Alpha described the pros and cons of SBC very well.

In this screenshot of the article, I underlined the pros of SBC in green and the cons in red:

Article by Confoundedinterest (Seeking Alpha)

The author even provided a list of companies that operates with a “growth focus yet under 20% SBC expense as a percentage of revenue”. This appears to be the author’s opinion on what is considered the ‘reasonable’ use of SBC.

We discussed above that TENB is a high-growth company, growing its free cash flow by a CAGR of more than 30%. With the last reported SBC of $111B and revenue at $647.6M, the percentage of SBC against revenue will be 17.14% (under 20%).

From this perspective, TENB’s current SBC amount is still considered ‘reasonable’.

Valuation

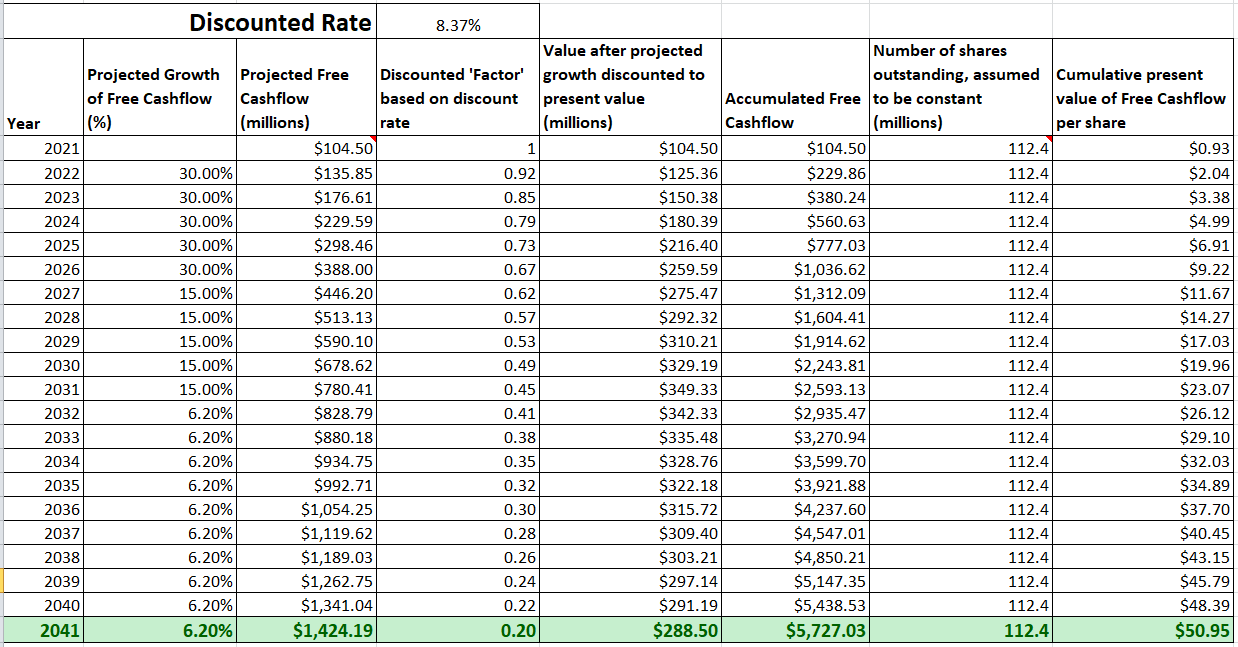

We will calculate the intrinsic value of the company using the Discounted Free Cashflow model (“DCF”) with a 20-year timeframe.

The following assumptions and values will be used:

- The last reported ‘Total Common Shares Outstanding‘ is $112.4M.

- The last reported ‘Total Cash & ST Investments’ is $ 548M.

- The last reported ‘Total Debt’ is $424.7M.

- The latest Free Cash Flow during the TTM period is $104.5M (described in the previous section).

- The discount rate is estimated to be 8.37%, taken from the WACC value.

- The company has been growing its FCF at a CAGR of 33.52% for the last 3 reported years. We will round off the growth figure to 30% and assume that it can maintain this growth for at least the next 5 years:

- For the next 5 years, we assume the company’s growth in FCF tapers to just half at 15%.

- For the last 10 years, the company is assumed to grow at the ‘median value’ of the U.S. GDP growth rate of 6.20%.

DCF (Author’s Calculation)

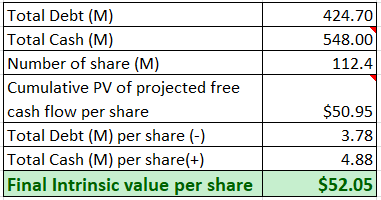

Based on the above inputs, the present value (“PV”) of the projected Free Cash Flow per share for TENB is $50.95.

DCF (Author’s Calculation)

Taking into account the total debt and cash that the company is holding, the final intrinsic value is about $52.05.

At the current price of $40.50, TENB’s share price is currently undervalued and selling at a discount of about -22% (40.5/52.05 -1).

Risks

Generally, the company is currently experiencing very high growth in top-line revenue and cash flow. However, it is still not profitable in the accounting bottom line. As discussed earlier, this is primarily due to the massive SBC issued to allow employees to have a vested interest in the company’s growth.

Although we concluded in the previous section that this SBC amount is currently still reasonable, investors should observe whether it grows and become out of control in the long run.

Conclusion

TENB is a high-growth company that is currently sustaining accounting losses on a consistent basis. Most of the losses are due to the huge amount of SBC incurred.

We analyze further that the current amount of SBC, while huge in absolute amount, is still relatively reasonable when compared to how much revenue the company is having.

The balance sheet is healthy with a substantial amount of cash assets, working capital, and manageable debt. Free cash flow is also positive and rising for the last 3 years.

The company is currently significantly undervalued, selling at a discount of ~22%. Investors should consider this as a good opportunity to enter a position on TENB stock.

Be the first to comment