Matheus Obst/iStock Editorial via Getty Images

Azul (NYSE:AZUL) is one of the two largest Brazilian airlines. The company specializes in the domestic market, with a diverse fleet of airplanes.

I issued hold ratings on the company in December 2021 (down 52% since) and August 2022 (down 34% since).

In this review I keep my hold rating, under the belief that the company is far away from being able to obtain revenues or profits that justify its current market cap, even though it trades at prices similar to those of the pandemic. On the positive side, the Brazilian market seems to have stabilized, and the company is not far away from breakeven, which removes significant solvency risks.

Note: Unless otherwise stated, all information has been obtained from AZUL’s filings with the SEC.

Business description

For a more detailed description, please visit my articles from December 2021 and August 2022.

Bad industry: Airlines is not a great sector in general. High fixed costs make participants compete on volume, destroying pricing. Customers are in most cases very concerned with pricing and can spend significant time looking for cheap flights. Government regulation or cheap financing makes under-profitable competitors remain in the industry. Unless a company has a specific competitive advantage, airlines are not great.

Azul has some advantages: AZUL has shown that it can charge a premium per kilometer flown compared to Gol Linhas Aereas Inteligentes S.A. (GOL) or LATAM Airlines Group S.A. (LTMAQ). The company is also the single operator in many smaller airports in the country. While GOL has a single aircraft model, AZUL uses different sizes to better adapt to Brazil’s differentiated population density.

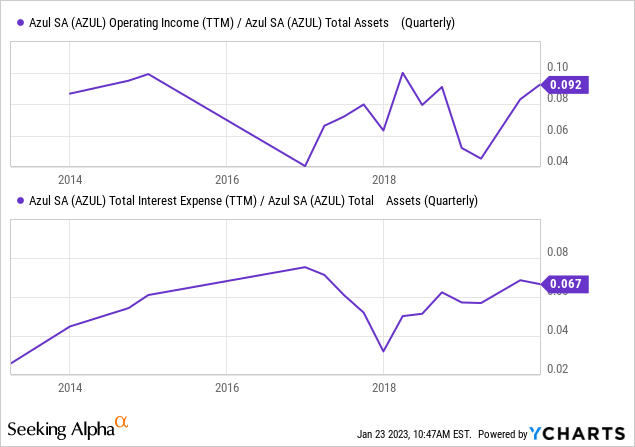

Return on assets is low and financing costs high: Because the industry requires assets but it is competitive, it tends to earn a low return on those assets. If these are financed externally, they may not earn a sufficient return. This is currently AZUL’s biggest problem, given that it was true before the pandemic (chart below), but even more so today, with financing costs up.

Brazil market is growing: Although in December 2021 I warned against the general confluence thesis that Brazil’s airborne passenger traffic would match that of the developed economies, in August 2022 I posted data showing that airborne traffic was indeed increasing as a percentage of transportation against road traffic for interstate travel. This data point does not imply that Brazil’s passenger traffic will match that of the developed economies, but does imply that people choose flying when possible and affordable.

Recent developments

Brazilian rates are burning: Although most of AZUL’s debt liabilities are dollar denominated, the increase in Brazilian rates is burning the company’s financial expenses. For R$1.5 billion in reais denominated debt the company is paying an effective rate of 18%, against 7.5% for R$8 billion in dollar denominated debt.

The Brazilian market stabilized: Recent traffic data from November and October 2022, published by Azul, shows that domestic traffic is actually down YoY. This implies that the recovery stage after the pandemic is mostly over.

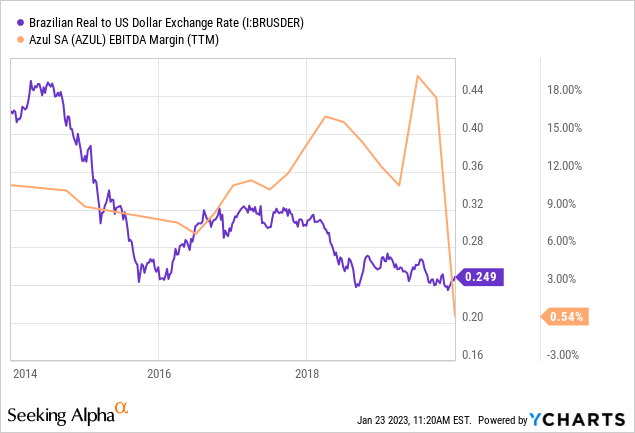

Prices are recovering faster than costs: Brazil takes a long time to accommodate after a devaluation, which makes many companies lose margins if they import some of their inputs. For example, AZUL’s yield per kilometer flown was the same in 2017 as in 2021, according to the company’s fundamentals spreadsheet, yet that meant that in dollar terms, the yield was 20% lower. Costs were 20% higher in reais for the same period (both with and without fuel)

Fortunately, prices are recovering fast, with the average yield per kilometer already 30% higher than one year ago (although costs also grew 18%).

Valuation and solvency risk

I will work with a light set of assumptions to prove that the company is still overvalued, and a stronger set of assumptions to test the company for solvency risks.

The lighter set of assumptions implies Brazilian rates going down significantly, so that AZUL’s Brazilian cost of debt stays around 10% (from today’s 18%), and the company sustains a 30% EBITDA margin. The stronger set implies higher Brazilian rates (18% cost) and 20% EBITDA margin.

Common assumptions for both models:

- Brazilian effective income tax rates of 35%

- Lease costs of R$4.2 billion per year (R$2.6 billion in the financial account, R$1.6 billion in the depreciation account).

- The BRLUSD exchange rate remains stable at around R$5 per $1.

- Dollar denominated debt of R$8 billion (paying 7.5%) and reais denominated debt of R$1.5 billion.

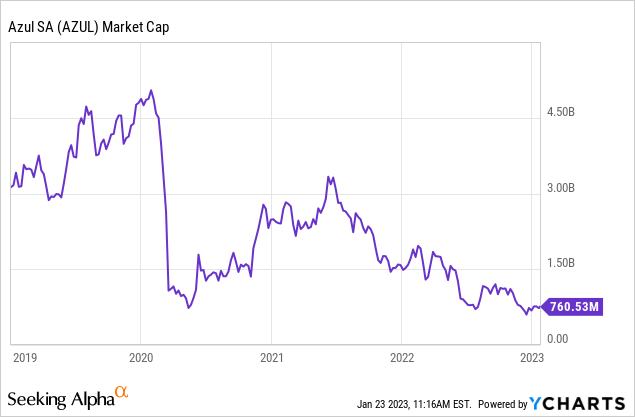

Starting with the first set of assumptions, I test how much revenue would be needed to justify the company’s current market cap of $750 million, with a return of 10% ($75 million or R$375 million). The company should earn R$576 million pretax, plus R$4.2 billion for leases and R$750 million for interest charges. That adds up to R$5.5 billion EBITDA, which divided by a 30% margin leads to about R$18.3 billion in revenues.

That implies revenues 15% above the current level, annualized from 3Q22 revenues of R$4 billion. Again, the model is optimistic because it assumes lower financing costs and a high EBITDA margin.

Under this same model the company should not have solvency issues, because its breakeven is at R$16.5 billion.

For the stronger model, breakeven moves to R$25 billion in yearly revenues. We do not even need to calculate how much is required for a 10% return on the company’s market cap. The difference arises from higher financing costs (not so much, R$120 million more), but mostly from a lower EBITDA margin.

Which EBITDA margin is correct?

I believe the 30% EBITDA margin is not a generous assumption, because the company sustained that same margin between 2016 and 2019, a period during which the exchange remained stable at around R$4 per $1.

Further, I believe that AZUL’s EBITDA is affected mostly by the BRLUSD exchange rate volatility. Because Brazil’s markets take some time to adjust to new costs, rate movements tend to generate medium term variations in EBITDA levels. Therefore, it could be said that the key assumption is a relatively stable exchange rate.

Conclusions

Although AZUL trades at a market cap that is lower than that of the pandemic period, I believe the stock is still expensive.

The reason is that even under relatively optimistic (although not crazy) assumptions, the company should grow revenues by 15% to provide a good return on its market cap. Growing revenues that much seems difficult considering the Brazilian market seems to have stabilized.

On the other hand, if the relatively optimistic assumptions do not hold, the company is even more overvalued, and presents solvency risks. The key assumption is that BRLUSD rates remain stable, which affects AZUL’s EBITDA margins.

Be the first to comment