CreativaStudio/E+ via Getty Images

Editor’s note: Seeking Alpha is proud to welcome Coldlake Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Tempur Sealy (NYSE:TPX) is the largest bedding provider globally. It is well positioned to achieve above-average growth as a result of the company-specific actions that are driving EPS growth. The growth is supported by its strong competitive position (size and distribution capacity) and a backlog of opportunities to expand margins (new products and overseas markets). This is aided by a comparable capital allocation strategy that balances shareholder returns and expansion prospects.

Business overview

TPX is a leading manufacturer, retailer, distributor, and designer in the $120 billion global bedding business. Mattresses and adjustable and non-adjustable foundations account for 91% of the company’s 2021 sales, with the remaining sales made up of pillows, mattress covers, sheets, cushions, and other comfort items. These are available at various price points through its well-known brands, including: Tempur-Pedic, Stearns & Foster, Sealy, and other private labels and OEM products.

TPX has operations in over a hundred countries, with more than 80% of its sales taking place in North America. Europe is the second-largest market, followed by the Asia-Pacific area. The business expanded its foothold in the UK bedding manufacturing and retail industry in 2021 with the acquisition of Dreams Topco Ltd. The rivalry and product design within the global bedding market are still largely regionalized. In the highly competitive US market, which is dominated by the top 3 manufacturers, Sealy and Tempur-Pedic rank as the top two most popular mattress brands.

Competitive advantages

- Portfolio of leading brands: Along with its private-label products, TPX runs three well-known brands with a global presence: Tempur-Pedic, Sealy, and Stearns & Foster.

- Variety of offerings: The extensive selection of foam and innerspring mattresses, as well as complementing accessories like foundations and pillows, gives it a wide range of contact points for merchants and customers.

- Strong distribution: TPX’s presence in more than 650 company-owned locations, a global network of independent merchants, and e-commerce sites contribute to its capacity to reach consumers and to gather valuable insights into their attitudes and behaviors.

- Focus on consumer preferences: TPX uses websites to offer a curated range of SKUs for a few chosen launches. This gives management special knowledge of customer preferences and buying patterns, enabling management to make any necessary adjustments whenever needed to continuously win its share of customers.

Investment thesis

Bedding sales have started to moderate since late CY21 and have remained weak till date given the rising inflationary pressures. While the level of promotions has been increasing to combat the industry’s weakness, it has been producing friction with the need to increase pricing as OEMs look to offset further inflationary pressure.

A key part of this thesis, as we continue to see softness in housing and home improvement activities, is for management to go hard on its company-specific initiatives to grow revenue and improve profitability.

New product launches

As successful new product launches, investments in technology and production, enabling improved service levels, and regional expansion combine to drive growth ahead of the bedding industry, TPX can continue to beat broader home furnishings peers. Over the past few years, management has constantly expanded into new projects while leveraging its exposure across price points and categories.

Two examples of recent or upcoming product launches are:

- Stearns & Foster brand (launched in 2Q22), which is aimed towards customers with higher incomes who want classic innerspring products yet have similar price points to Tempur-Pedic. This is a wise move since it boosts TPX’s presence in the premium/luxury market, which fetches a larger profit margin.

- New Sealy Collections (recently launched): A premium range focused on giving advancements in comfort and support, while Naturals was created with sustainability in mind. Management also intends to introduce a gel grid option in 4Q at a relatively cheaper price point to serve the mass market.

TPX’s ability to continuously innovate and launch new products is one of the reasons leading to revenues increasing at an 8% CAGR since 2015, while the bedding sector has risen at a pace of 5% CAGR over the same period. Although the macroeconomic environment is changing, management is still gunning for double-digit sales growth.

Acquisition of Sherwood

In 2020, TPX purchased an 80% stake in Sherwood for $4m, one of the top 10 US bedding manufacturers. In the overall scheme of things, I believe this offers a lot of benefits since TPX is able to combine its experience in foam with Sherwood’s knowledge in manufacturing traditional innerspring. This acquisition should unlock a further TAM of >$500m as it gives TPX:

- Greater purchasing bargaining power and supplier agreements: More advantageous deals with important retailers and other distribution partners could be possible as a result of increased control over manufacturing and delivery across a wide variety of items and price points.

- Enhance its position as the supplier to retailers: In order to provide customers with high-quality, in-demand items, retailers and other significant distributors have resorted to TPX’s established base of operations and logistics for supplies. I believe that increasing manufacturing will enable the business to successfully pursue private-label possibilities, enabling long-term development.

- Further increase operating leverage: Increased production rates boost incremental profits, while backward integration makes it easier to negotiate prices for crucial supplies.

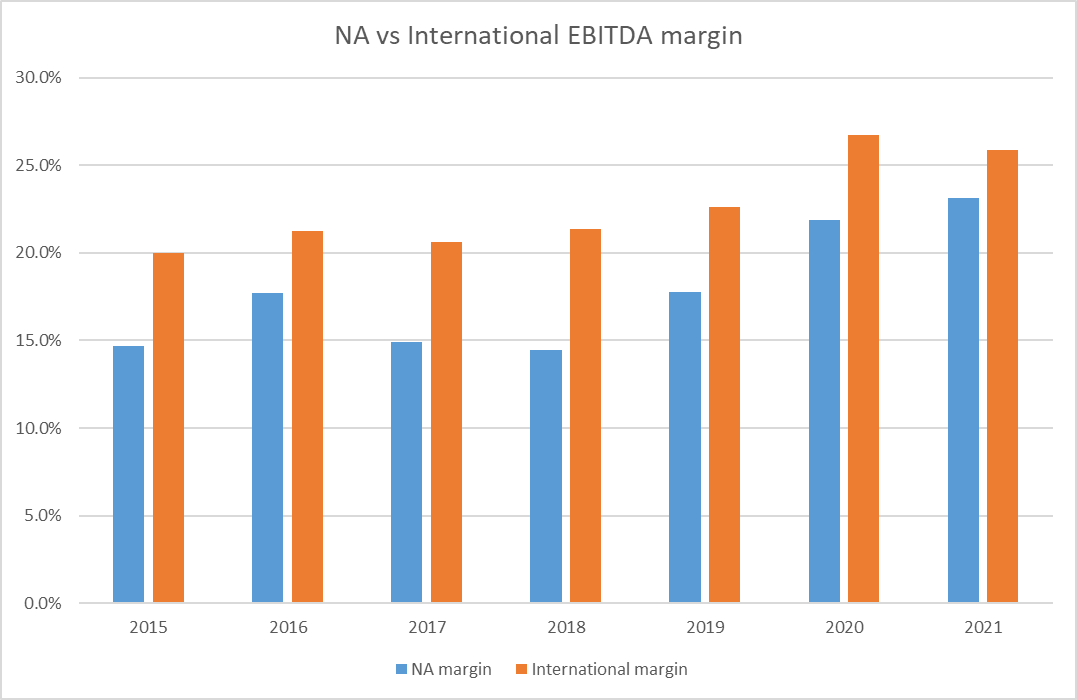

Investing internationally

The international segment accounts for ~20% of TPX EBITDA as of FY21. The majority of TPX’s international presence is in Europe, where it has greater profitability and is FCF positive due to its leading position in the ultra-premium segment.

Own model

Europe

TPX’s European segment has slowly but steadily increased its profitability and generated significant cash flows. This is due to TPX’s dominant position in the ultra-premium market sector. Despite this, management is dedicated to investing in a variety of growth opportunities while preserving acceptable margins after the purchase of Dreams, a prominent UK-based retailer (Aug 21). Currently, some of the company’s innovations are being tested in Scotland and Ireland, with an eye toward France and Spain. The way I see it is that this is an approach similar to that of TPX local operations back in the United States in that more cheap units are provided to foster expansion while returns are constantly monitored. Hence, even though the invasion of Ukraine required several new Tempur products to be delayed until 2023, I am fairly optimistic about TPX’s capability to continue expanding in Europe-which should continue to improve margins due to the mix shift effect.

China

Looking farther out, China seems promising as well. Brand Sealy has a substantial presence as a result of a joint venture in which it has a 50% stake. After finding great success in Korea with its European-made goods, TPX has set its sights on China. As a result of the current state of international affairs, management is being extra careful about making any new investments at this time. Once things settle down, there is no reason why TPX cannot leverage its connections with major international suppliers to maximize its return on invested capital.

Capital allocation

Management pays close attention to maximizing shareholder returns. They plan for a 15% dividend payout ratio and are committed to repurchasing 10% of their shares each year. As a result, earnings should continue to grow at a historical pace over the next couple of years. This includes developing its global footprint, launching new goods and expanding the direct-to-consumer channel quicker than conventional brick and mortar shops.

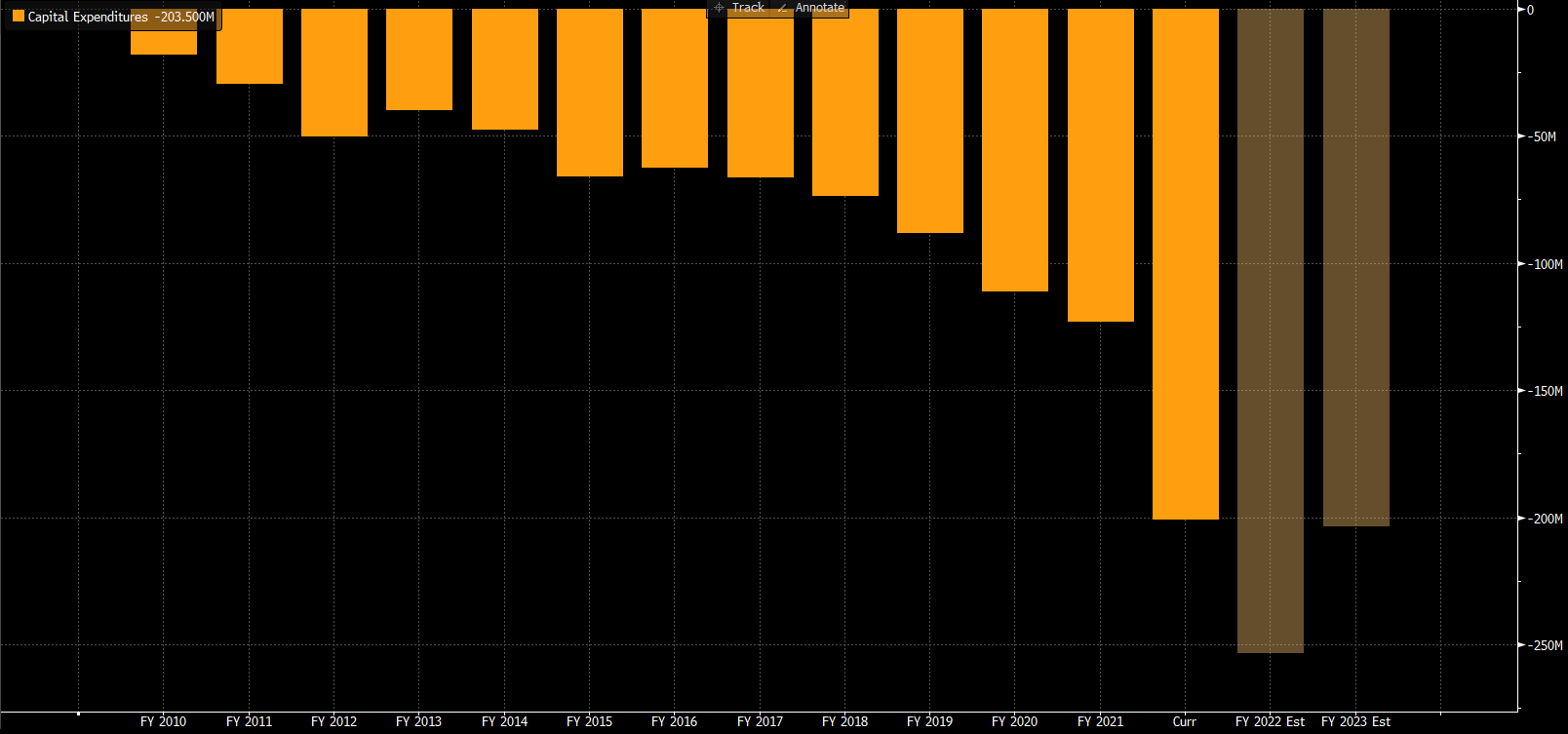

CAPEX

Expected capital expenditures of $250 million or more in 2022 attest to the company’s commitment to fostering sustainable growth. The average annual CAPEX averaged between 2011 and 2019 was ~$60 million. The majority of TPX’s budget increase this year will fund the construction of a larger chemical tank farm, warehouse, and foam pouring plant. TPX also opened a brand-new factory in Dallas the year before in an effort to increase its market share.

Bloomberg

The strategic benefits of backward integration, I believe, outweigh the fact that these items have lower margins than TPX main sales. As a result, I anticipate that future investments in this area will bear fruit overtime.

All in all, as successful new product releases, investments in technology and manufacturing, improved service levels, and regional development combine to drive growth ahead of the bedding market, TPX should continue to outperform wider home goods peers.

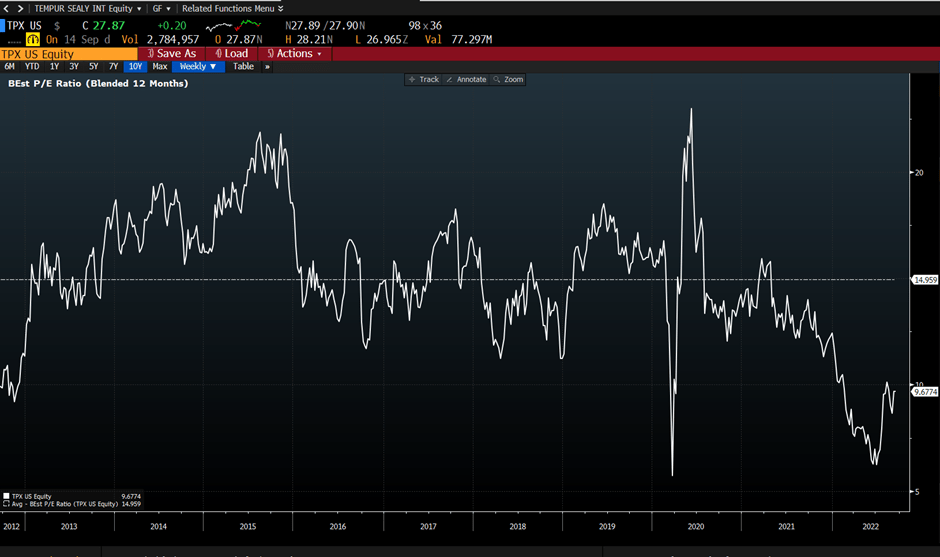

Valuation

Valuation of building products peers has largely declined over the course of the year, reflecting the slowdown in consumer spending and macro uncertainty.

Bloomberg

As volume continues to decline for the remainder of FY22, I anticipate that growth will be sustained by price increases (they have the perfect reason to raise prices-inflation). While boosting pricing mitigates some margin reduction, the nature of the business’s high fixed costs would cause volume decrease to negatively impact profits (i.e., high decremental margins).

My model assumes a through-cycle performance until 2024, when I expect demand to stabilize and the supply chain environment to improve. As stated in my thesis, I think TPX’s market position improves as it acquires market share, and its margins should increase (relative to pre-covid levels).

It is not demanding to achieve 30% returns at the current 9x forward earnings valuation, assuming it trades back to the historical multiple (though with a slight discount once we adjust the current interest rate environment), and it prints the following earnings algorithm: lsd-msd% topline growth and 150bps margin expansion (from 2020 levels).

Own model Bloomberg

Risks

Inflation and rate hikes

In the event of further rate hikes, which is increasingly likely given the recent CPI data, it will further hurt consumer sentiment, thereby hurting TPX on both the topline and cost levels. Since TPX’s products are typically higher-priced items, the impact of rising prices has a lot more impact than other daily necessities.

Concentration of customer revenue

TPX’s top 5 customers represented 1/3 of its revenue. There are 2 main risks associated with this. First, any loss of one of them would be hugely detrimental to its financials and scale. Second, these key customers have some level of customer bargaining power to negotiate for better rates, and if they scale up to be a larger part of the revenue mix, it could hurt TPX’s margin.

Conclusion

TPX is a long at the current valuation, where the market is pricing the business as a melting ice cube business (usually valued at 10x earnings). My research suggests this is not true. TPX is the market leader and has multiple avenues to continue driving topline growth that is margin accretive. As the business rides through the near-term macro headwinds, it should continue to outperform peers.

Be the first to comment