CHUNYIP WONG

Energy stocks have predictably fallen in recent weeks as oil prices generally fall in the winter months due to lower demand. This presents a buying opportunity, especially for more stable midstream companies that that are insulated from commodity price swings. Plus, what’s better for income investors is that the lower prices have pushed dividend yields back to attractive levels.

This brings me to TC Energy (NYSE:TRP), which now yields over 6% after materially fallen from the $50 level at the end of last month. As shown below, TRP is now within several percentage points of its 52-week low. This article highlights why TRP is a bargain buy at present.

TRP Stock (Seeking Alpha)

Why TRP?

TC Energy is a leading energy infrastructure company operating pipelines, storage, and power generating assets in Canada, U.S., and Mexico. It has more than 60K miles of oil and natural gas pipelines, more than 650B cubic feet of natural gas storage, and generates 4,200 MW of electric power.

TRP has a strong presence in the bitumen-rich Athabasca oil sands of the province of Alberta, Canada. Beyond that, TC also has presence in the gas-rich Marcellus and Utica shale basins in Appalachia, and its pipelines also carry gas to the U.S. Gulf Coast for export. This has enabled TC to deliver annual dividend growth for its shareholders for over 2 decades.

Like its peers, TRP is seeing strong demand for its services, and recently revised its 2022 comparable EBITDA outlook to be higher than last year, expecting 4% YoY growth. This is driven by strong volumes, including U.S. natural gas pipeline flows that averaged nearly 26 Bcf per day during the third quarter, equating to 6% growth over the prior year period. TRP also has a strong backlog of projects, and continues to execute on its C$34 billion capital program with $2.6 billion invested during the last quarter.

Risks to TRP include its recent Keystone oil spill, which may take weeks to clean up. In addition, TRP is getting regulatory scrutiny around its special permission to run its systems at higher pressure, making it unique among U.S. oil pipelines. Moreover, TRP carries more peers than some of its midstream counterparts with net debt to EBITDA over 5x. However, S&P still assigns TRP with a BBB+ credit rating due to the diversity of its business model which, includes steady utility operations.

Plus, management plans to bring leverage down to a more reasonable 4.75x through asset sales of liquid pipelines, enabling it to focus on its core gas assets and operations. In a recent interview this month, the CEO noted that reducing oil exposure would also help it to reach its emissions reduction goals. CEO Francois Poirier stated that there are “no sacred cows” and asset dispositions could include its Keystone pipeline, which could also eliminate its risk of future spills on this pipeline

Moreover, TRP is making good progress on its signature Coastal GasLink project, which is now 75% complete. The company’s utility segment provides good diversification and it’s also making commendable efforts to transition to renewable and low carbon projects. These were noted during the recent conference call:

Our power and energy solutions business produced exceptional results during the quarter and continues to play a greater role in our diversified portfolio of energy infrastructure assets. Strong availability at Bruce Power combined with peak pricing in Alberta contributed to a 41% year-over-year increase in comparable EBITDA for the segment.

We also progressed several renewable and low carbon projects, including the 81 megawatt Saddlebrook Solar project announced in October, which will be the first utility scale solar project to be fully developed and delivered by TC Energy, thereby progressing the development of our capabilities in that area.

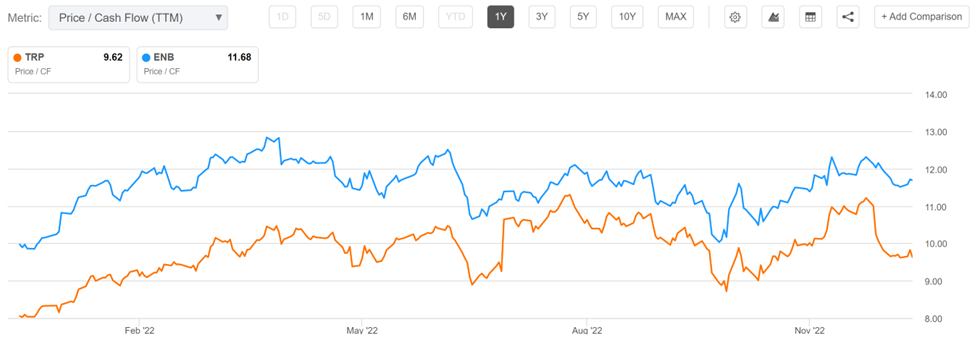

Lastly, I find TRP to be attractively valued after the recent drop in price, pushing its dividend yield to 6.3%. Management also stated their intention to maintain a 3 to 5% annual dividend growth rate going forward. TRP also trades at a meaningful discount to its Canadian peer, Enbridge (ENB), with a price to cash flow of 9.6x, compared to ENB’s 11.7x. Morningstar has a $48 fair value estimate while analyst have an average $43 price target.

TRP Price to Cash Flow (Seeking Alpha)

Investor Takeaway

TRP is a solid midstream company that has proven to be reliable with dividend growth for over two decades. It’s seeing strong demand for its services and its diversified business model and renewable projects helps to de-risk potential weakness in any one area.

Furthermore, non-core asset sales could help TRP to achieve its leverage target. Lastly, I believe TRP has the potential to close at least some of the valuation gap with ENB as its projects come online, and the recent price drop presents an opportunity for income investors to lock in a high yield.

Be the first to comment