Kirkikis/iStock Editorial via Getty Images

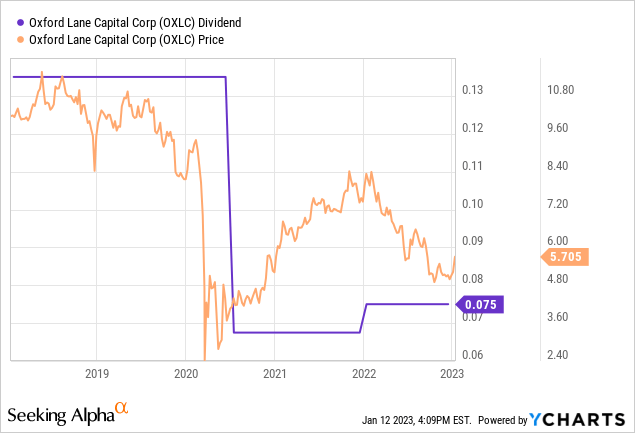

Investors go through two stages after discovering Oxford Lane Capital (NASDAQ:OXLC). The first is shock at the $0.075 monthly payouts. A 16% yield paid monthly is rare, but has become more common in recent months following the more than a year-long rout of stocks. The second is healthy scepticism. A yield that fat rightly looks like a trap and income investors should not just chase payouts whilst being oblivious to the broader reasons the yield is so high.

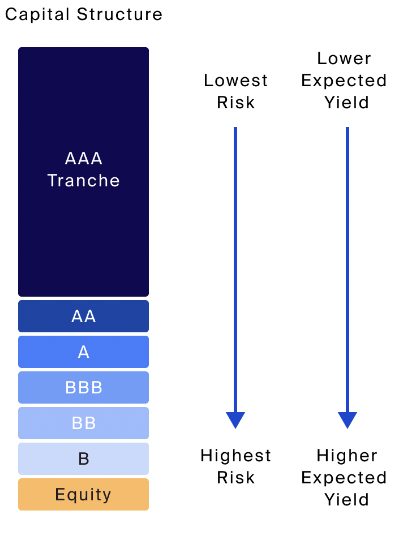

Yield is a function of price and the closed-end fund is down by 31% over the last 12 months to swell a monthly payout that’s been cut by 44% from its pre-pandemic averages. The CEF invests in the relatively esoteric space of collateralized loan obligations (“CLOs”). These are financial products composed of different tranches of pooled corporate loans. The interest and principal payments from the underlying loans are paid out to investors in the different tranches.

The Tale Of The Commons

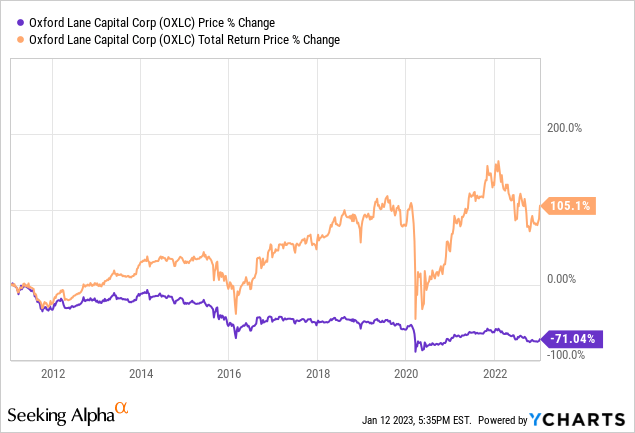

Is Oxford Lane a buy? This depends on your risk tolerance. The CEF invests in the equity tranche of CLOs, the riskiest part formed from portfolios of unrated and low credit-rated loans. The $920 million Greenwich, Connecticut-based CEF went public in 2011 at $20 per share but has since declined by 71% since then.

But to many investors Oxford Lane Capital means income. The CEF just has to maintain its monthly payouts and allow its shareholders to reinvest these. On a total return basis, the CEF is up markedly by around 105% since its IPO date. The income forms the bulwark for the company’s investment proposition and the core reason for holding.

Wealthmanagement.com

The yield has pulled higher because the CEF is down from a recent high of $8.40 as recession fears mount and interest rates are set to be hiked to a nearly two-decade high. Indeed, a Bloomberg survey has placed the chance of a US recession this year at 70% just as the Fed fund rates are expected to increase to between 5% and 5.25%.

At its core, Oxford Lane is an arbitrage fund with returns being driven by the difference between the cost of the CLO debt tranches and the interest income derived from the portfolio of floating-rate bank loans. Further, CLOs also benefit from term, non-recourse leverage without mark-to-market triggers. Hence, Oxford Lane does not face margin calls or liquidation if the market value of the underlying corporate loan portfolio falls.

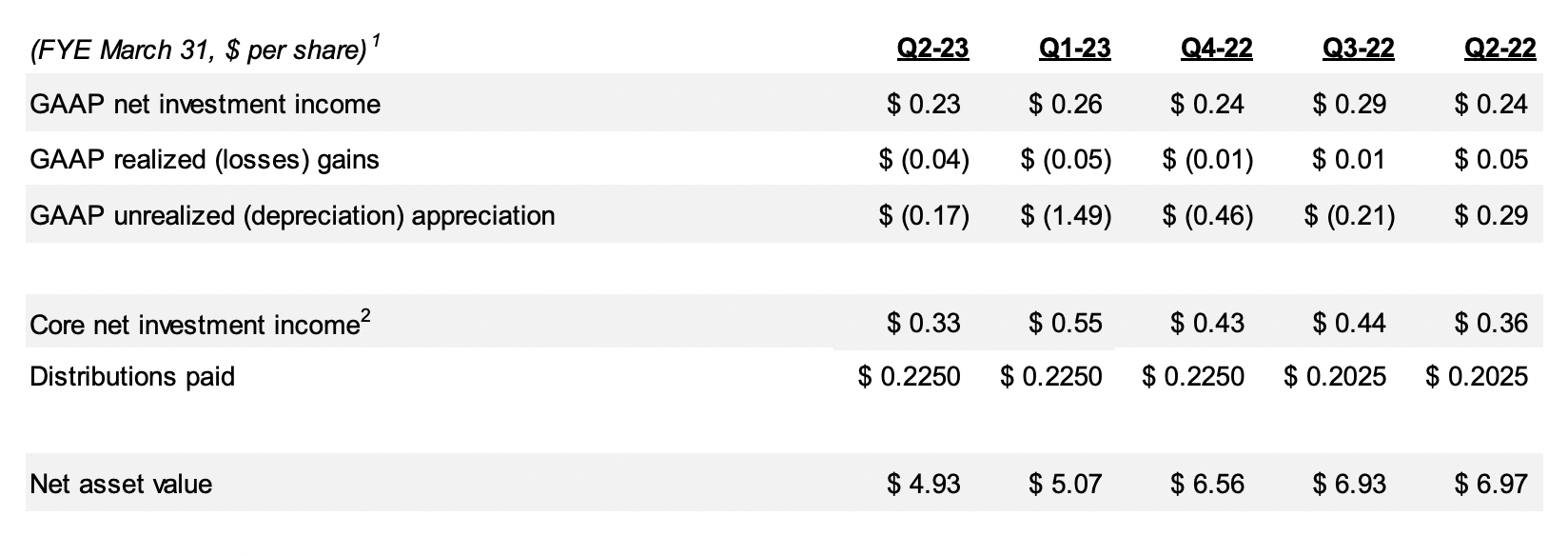

The CEF last reported revenue of $64.7 million for its fiscal 2022 second quarter ending September 30, 2022. This was up by $1.2 million from the first quarter and drove GAAP net investment income of $36 million, around $0.23 per share. Core NII was $51.1 million, around $0.33 per share, and was down from $0.55 in the prior quarter and from $0.36 in the year-ago comp. The monthly payouts over three months are broadly covered by NII.

Oxford Lane Capital

NAV ended the quarter at $4.94, maintaining a downward trend that has seen NAV fall by around 29% from its year-ago figure. In spite of this, the CEF has historically traded at a premium to its NAV. The current premium to NAV stands at 16.23% and highlights just how much emphasis investors have placed on the payouts. The CEF’s weighted average effective yield on its CLO equity investments at current costs stood at 16.1% as of the end of the second quarter, up by 20 basis points sequentially from 15.9% in the first quarter. This was on a total portfolio that grew to $1.238 billion as of the end of the third quarter from $1.115 billion in the year-ago period.

The Tale Of The Preferreds

Oxford Lane Capital 6.75% Cumulative Series 2024 Term Preferred Shares (NASDAQ:OXLCM) offer another way to gain exposure to the CEFs CLO portfolio in the same monthly payout structure as the commons but without the dividend cuts and price volatility.

QuantumOnline

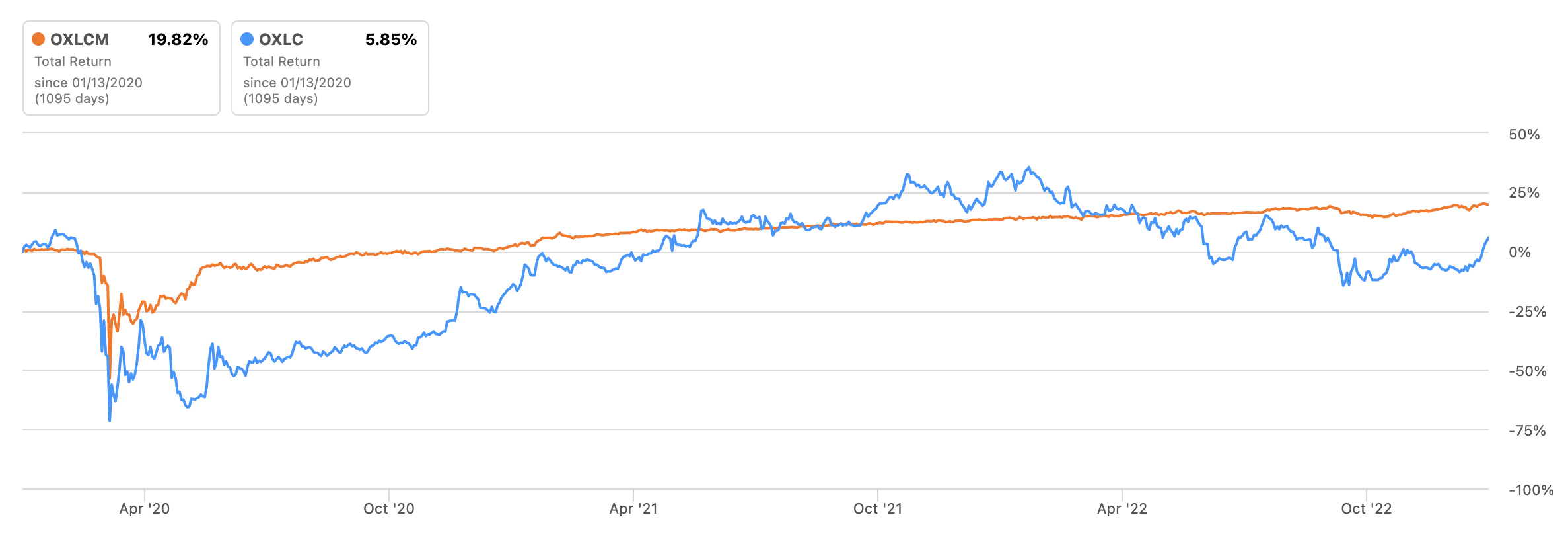

These pay an annual coupon of $1.69 in monthly instalments which works out to be a yield of 6.75% with the preferreds currently trading at their redemption price. Whilst the income is currently less than half of the yield on the commons, they’ve still outperformed on a total return basis over the last three years.

Seeking Alpha

OXLCM is up nearly 20% versus 5.85% for OXLC. It has moved in a stable line to underscore just how little volatility the preferreds owners are subjected to. They also have a maturity date, somewhat uncommon for preferreds where the bulk trade on perpetual clauses. This means that Oxford Lane is fully obliged to buy back the preferreds as of June 30, 2024. Hence, whilst they currently trade past their June 2020 call date, preferred owners have around a year and a half of safe coupon payments to look forward to.

QuantumOnline

Oxford Lane has four other preferreds trading and two notes. The 2024 term preferreds offer a shorter time to maturity than the marginally higher-yielding 2029 term preferreds (OXLCN). This nearer-term maturity creates certainty and means lower volatility versus the other securities. It also places in view the broadly risk-averse income investors that are the ideal buyers of these. The likelihood of the preferreds dividend being cut in the period until maturity is close to zero, opening up what will be total coupon payments of $2.535 and a yield to maturity of 10%. Against an expected recession, volatile energy markets and elevated inflation, a near-certain 10% return is worthy of consideration.

Be the first to comment