steinphoto

Thesis

We rate ProShares Short 7-10 Year Treasury (NYSEARCA:TBX) a sell, because we believe that the longer term interest rates have reached a plateau and most likely will drift lower from the current levels.

Historical Analysis and Background

TBX is the inverse of the ICE U.S. Treasury 7-10 Year Bond Index; it is design to realize the negative of the index on a daily basis. The opposite of TBX is IEF. While IEF is an income fund suitable for long term investing, TBX is mostly used as a hedge instrument.

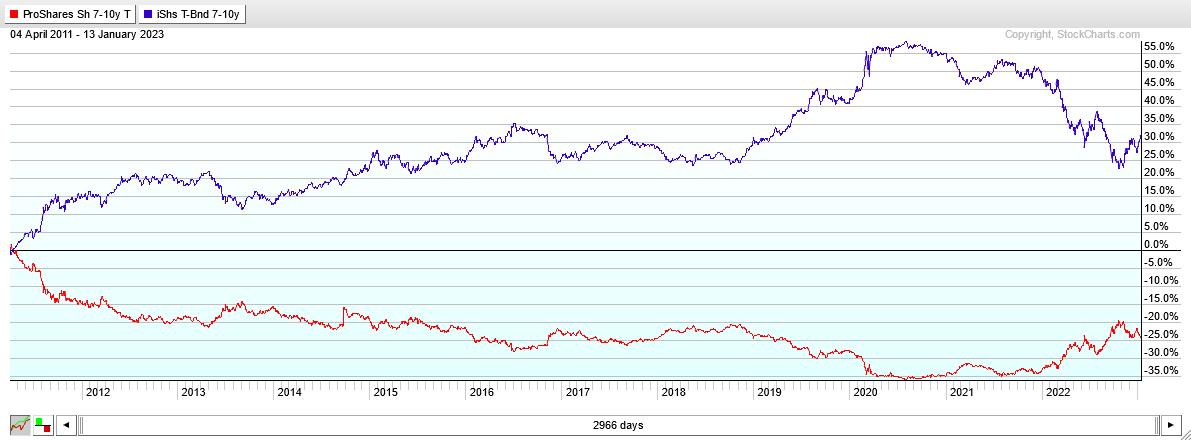

The chart below shows the evolution of TBX’s total return since its inception on 4/4/2011. Overall, since its inception, TBX returned -24%. Over the same time period, IEF returned 31%.

stockcharts.com

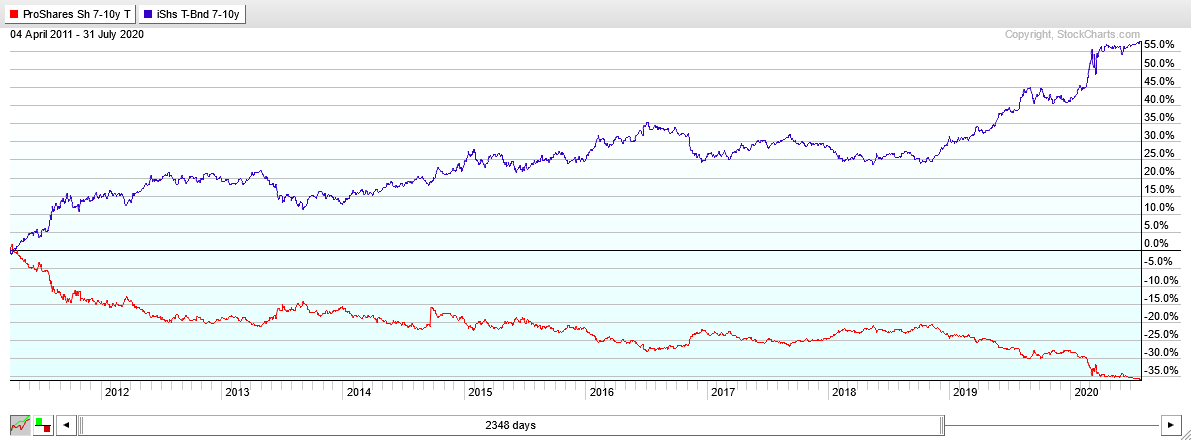

For the time period from 4/4/2011 to 7/31/2020, IEF returned 58%, TBX returned -35%. Obviously, IEF did a decent work in generating income, while TBX would have continuously lost value.

stockcharts.com

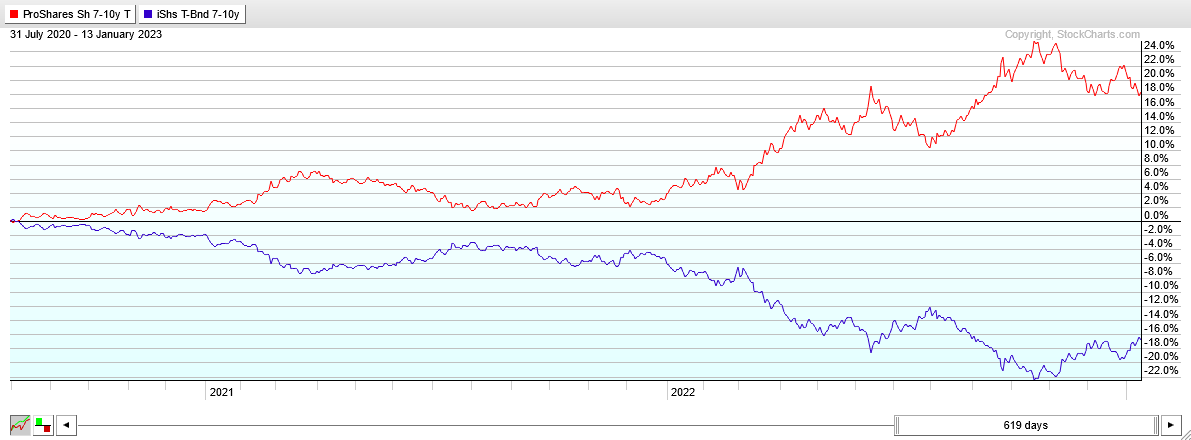

Things started changing after 7/31/2020. The next chart shows the change in the funds behavior; TBX started growing, while IEF stared losing value.

Between 8/1/2020 and 12/31/2021, TBX gained 3% and IEF lost 5% although during that period the fed funds rate was 0%. One can assume that the bond market was early in anticipating the changes in Fed policies to come.

The big changes materialized from the beginning of 2022, and the rate of change accelerated in March when the FED started its rate increases. Between 12/30/2021 and 10/20/2022, TBX gained 25% and IEF lost 22%

stockcharts.com

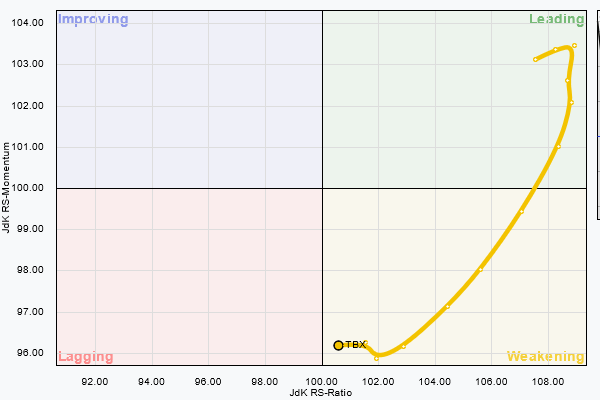

Current Intermediate-Term Trend

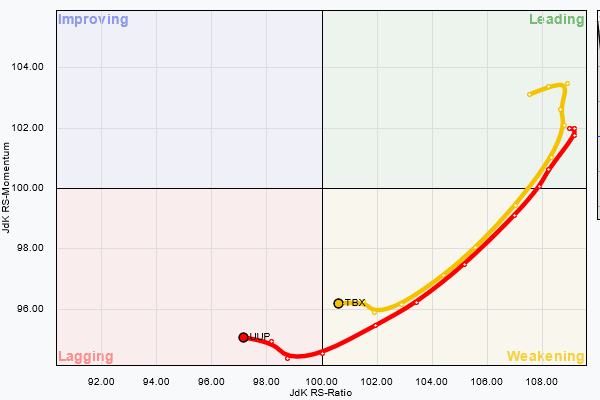

Since its peak on 10/20/2022, TBX has declined -6.12%. The next plot is a 12-week Relative Rotation Graph of TBX. It shows a strong weakening of both TBX momentum and relative strength.

stockcharts.com

An interesting insight into the relationship of interest rates, dollar strength and treasury bond prices can be seen in the next plot. One can see that the US Dollar leads the Treasury bonds.

stockcharts.com

From the above graphs we infer that TBX will move to a “lagging” status. Therefore, we expect a continuous decline in TBX over the next half a year.

Risk Factors

The change in the market environment that occurred in the second half of October 2022 was caused by a combination of factors such as the easing of inflation worries, the US Dollar price decrease and the expectation that the Fed is almost done with raising the interest rates.

These factors may change course and put pressure on the Fed to increase rates a lot more and for a longer period of time. Under different circumstances, that may lead to an increase in yields of long-term treasuries. But under the current circumstances, large increases in interest rates will cause a severe recession, and that would lead to deflation and a decrease, not an increase in bond yields.

Conclusion

I rate TBX a SELL.

From August 2020 to October 2022, TBX would have been highly profitable as a long position. It would have been an ideal risk-off asset during the 2022 stock bear market. In my opinion, that opportunity is gone.

Be the first to comment