Scott Heins

Super Micro Computer, Inc., or Supermicro (NASDAQ:SMCI), reported its FQ2’23 earnings release last week, corroborating a solid quarter when it announced its prelim release in mid-January.

However, SMIC has underperformed the S&P 500 (SPX) (SPY) since our previous update, which also saw it fall nearly 20% after we published, as we urged investors to brace for impact.

SMCI got hit by a short seller attack in the form of Spruce Point Capital Management. The short seller raised several questions including customer revenue concentration, free cash flow conversion, and corporate governance issues.

With the recovery from its January lows, SMCI bulls have likely used the recent selloff to buy the dips, leveraging the broad recovery in growth and tech stocks.

So, should investors who missed buying the recent dip join the bandwagon now, post-earnings?

SMCI Bulls could argue that SMCI’s “low valuations” favor buying the dips. CEO Charles Liang also highlighted in its earnings commentary, in response to a question about deploying its stock repurchase authorization: “That’s why I said, the PE is so low and cash flow is strong. Why not [utilize the buyback?]”

On the note about cash flow, Spruce Point mentioned in its report that Supermicro has a “poor history of converting revenue to cash.”

Supermicro FCF margins % and Adjusted EBIT margins % consensus estimates (S&P Cap IQ)

A closer look at Supermicro’s past FCF margins could indicate why Spruce Point wanted to remind investors about its ability to sustain its FCF, despite robust revenue growth.

Moreover, Wall Street analysts with a consensus Buy rating are not convinced that Supermicro could maintain its FY23 FCF margins in FY24.

Why? Because Supermicro’s revenue growth could normalize further after a blistering pace over the past two FYs.

Management’s FY23 guidance suggests that Supermicro could post revenue of $6.5B to $7.5B, indicating a revenue growth range of between 25% and 44%. In all honesty, that’s a pretty wide range for investors to model, which seems rather unusual if the company has solid visibility over its growth drivers.

Considering that the company is focused on several large server customers like Advanced Micro Devices (AMD), Intel (INTC), Nvidia (NVDA), and Meta (META), we expected clearer visibility, given their buildout cadence.

However, we believe prudence is warranted, particularly in the aftermath of Intel’s horrendous Q4 performance and disappointing Q1 outlook. Moreover, Meta has also paused its spending, which we believe was also inferred in Supermicro’s earnings commentary, as the Supermicro customer who accounted for 22% of its revenue in FQ1. Spruce Point and Northland Capital’s defense against the short call also brought up the revenue concentration with Meta.

However, Supermicro reported that it didn’t have a customer who accounted for more than 10% of its revenue in FQ2, highlighting that it could diversify its revenue base.

We believe Supermicro remains well-primed to leverage the product refresh/upgrades cycle in H2 as its server customers get ready to ramp volume production. Moreover, with Meta focusing on building out its AI infrastructure to circumvent its signaling challenges, it should bolster Supermicro’s long-term growth drivers.

Furthermore, the company has committed to adding more customers, likely leveraging the AI-driven hype now as companies look to build their competitive advantage with advanced AI models. As such, it should benefit from its close partnership with Nvidia, leveraging the increased demand for training and inference workloads.

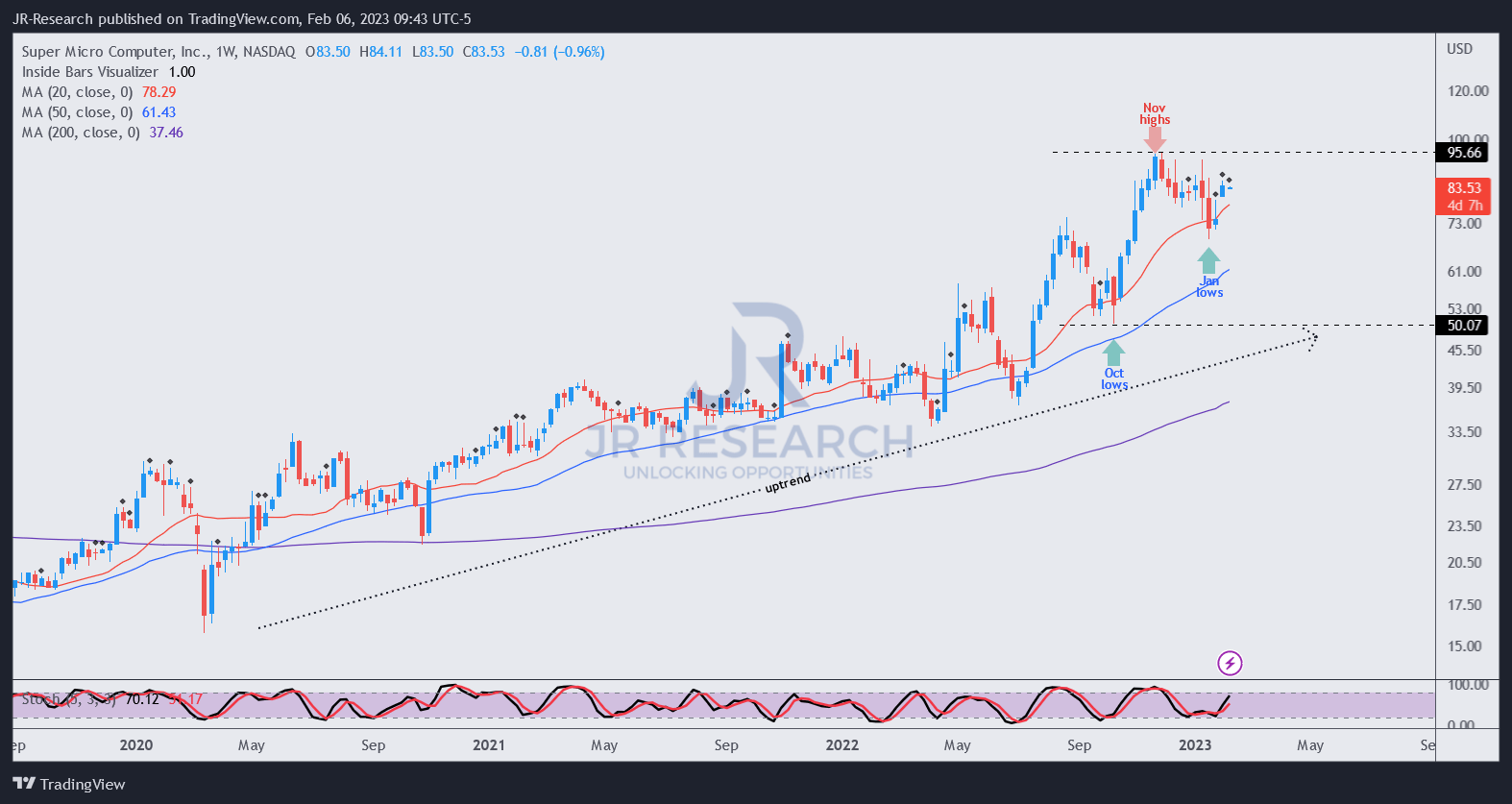

SMCI price chart (weekly) (TradingView)

Despite the pessimism by Spruce Point, we don’t agree that investors should consider shorting SMCI.

It has a clear medium-term uptrend, indicating that long-term buyers are confident of buying the significant dips. Hence, it implies shorting could be a perilous endeavor (over time).

Also, it’s still expected to remain FCF profitable through FY24, and its NTM EBITDA multiple of 5.9x is not aggressive relative to its peers’ median of 6.7x.

Despite that, SMCI’s price action still warrants caution, likely suggesting why it has failed to outperform the market since January. SMCI has failed to gain sustained upward momentum since forming its November highs.

With Supermicro’s growth potentially normalizing after a robust performance over the past two FYs, a healthy correction and consolidation could help to reset some of that recent over-optimism.

We encourage investors to remain patient.

Rating: Hold (Reiterated).

Be the first to comment