gopixa

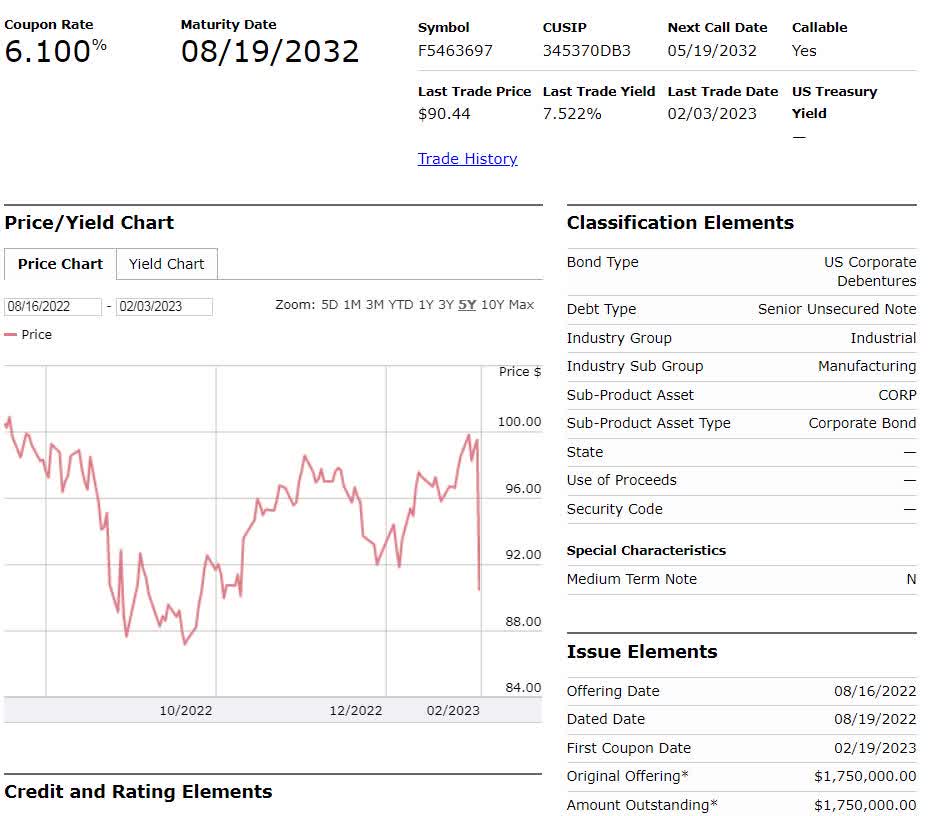

Ford Motor Company (NYSE:F) stock took a hit last Friday after the automaker posted a disappointing fourth quarter earnings report. Coinciding with the drop in the price of the stock, the company’s long-term debt also sold off, with the non-callable issues seeing steeper declines. The company’s 6.1% coupon bond maturing in 2032, which was issued less than six months ago, dropped nearly 10% to 90 cents on the dollar, yielding 7.5% to maturity. Last year, I wrote about my apprehensions towards investing in Ford’s long-term debt. Despite the pullback, I believe that Ford’s bonds are still overvalued and investors should be concerned about the company’s future interest expenses.

FINRA

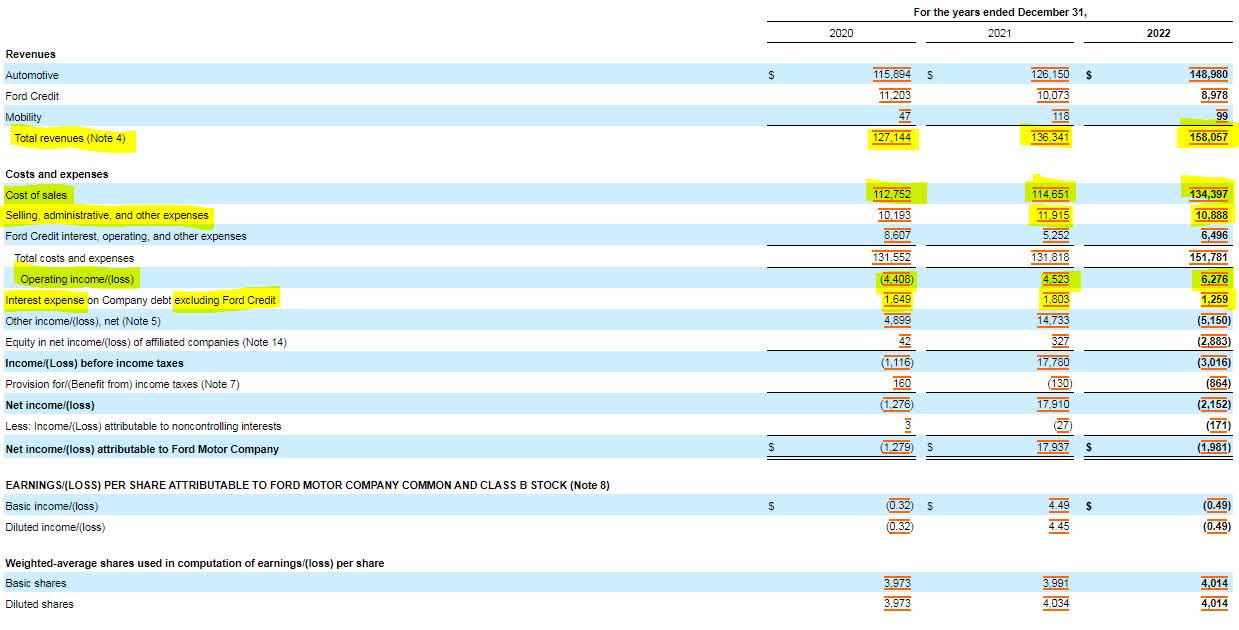

Not everything in Ford’s financial reporting was bad. The company grew revenues in the full year of 2022 by $22 billion. While cost of sales creeped right up with revenues, the company controlled its SG&A costs and was ultimately able to grow its operating income by more than $1.5 billion. The company saw a steep decline in other income (due to realized and unrealized losses on investments), which ended up being for noncash related reasons.

SEC 10-K

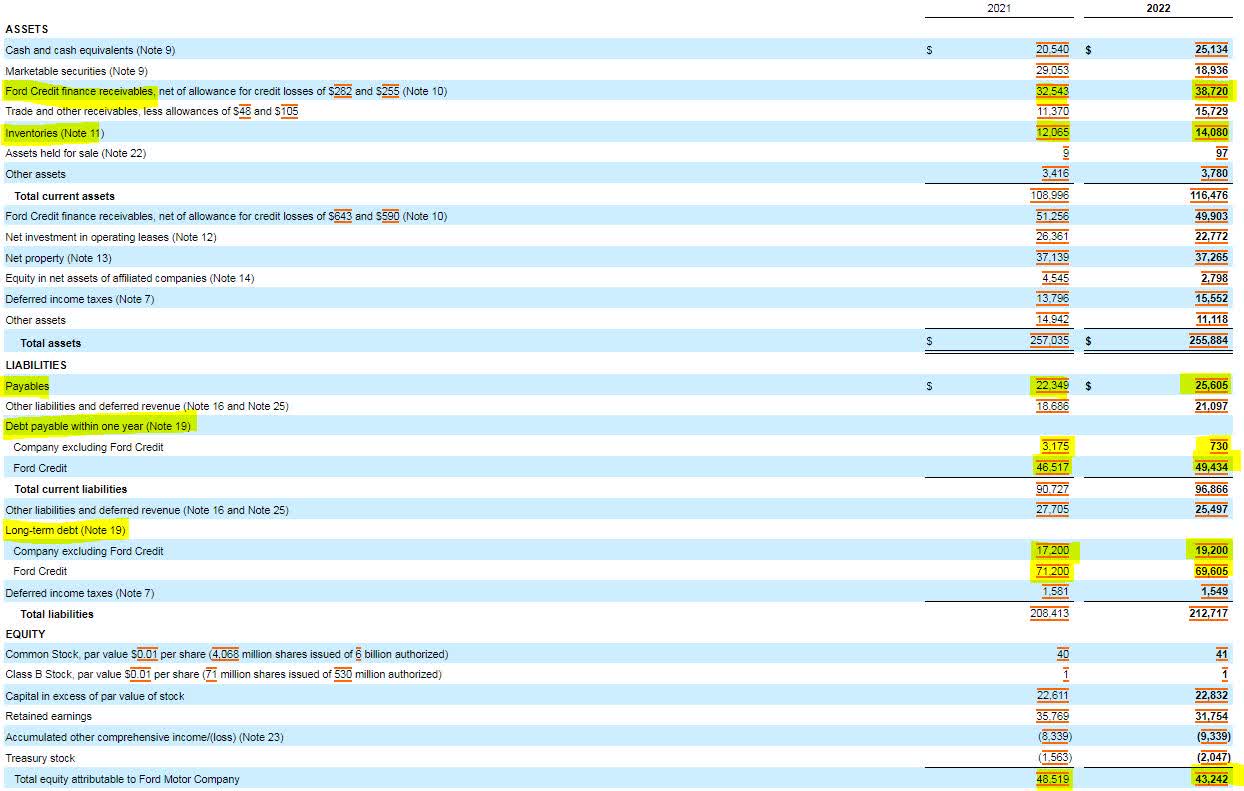

Ford’s balance sheet showed incremental changes across the company in 2022. In terms of assets, the company saw an increase in finance receivables and inventory, which both require cash burn. Near-term payables to vendors ticked up by $3 billion, while short-term and long-term debt remained fairly constant at $50 and $89 billion, respectively. The combined cash and marketable securities did drop by $5 billion.

SEC 10-K

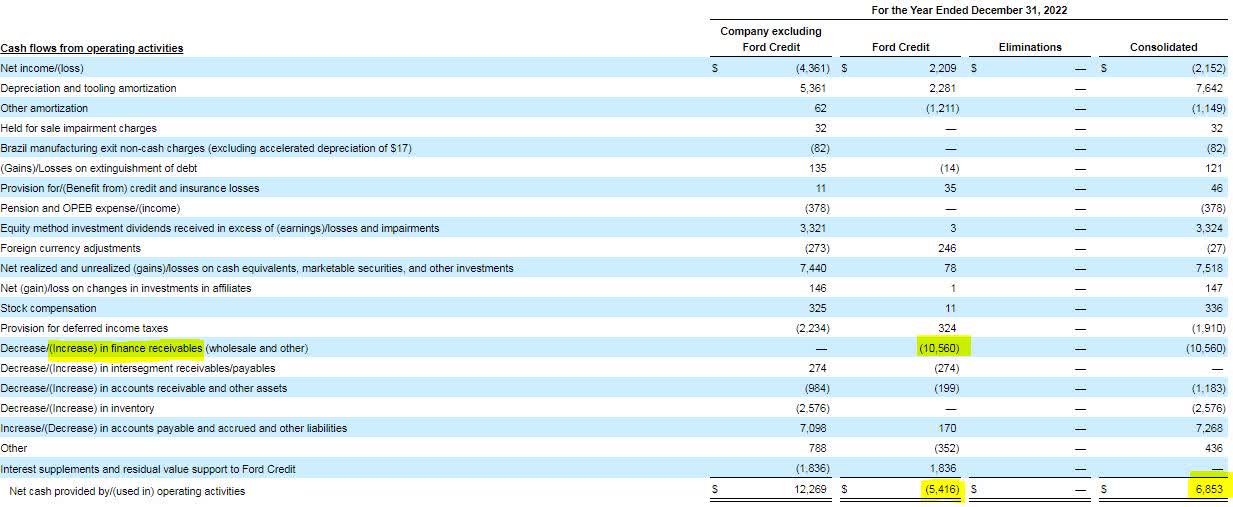

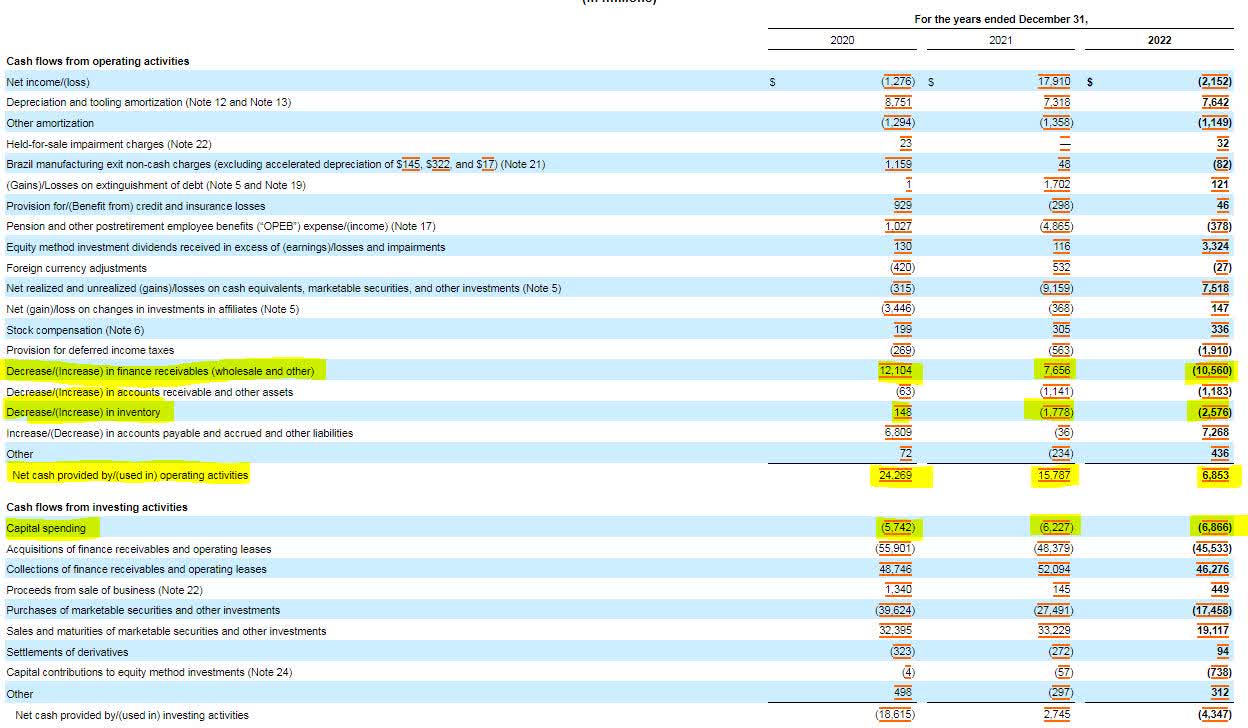

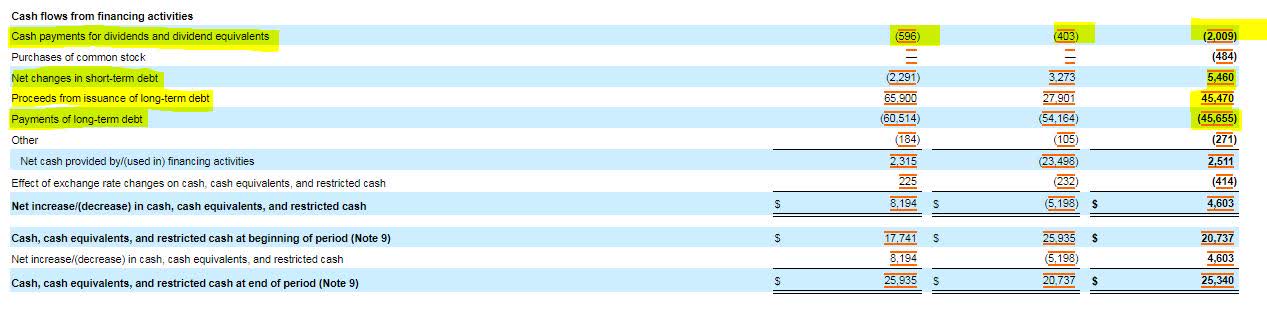

Where I have the most concern is in reviewing Ford’s statement of cash flows. Cash flow from operations declined by nearly $9 billion in 2022, driven by an increase in Ford Credit receivables and inventory growth. Working capital burned so much of Ford’s cash that it ended up with $0 free cash flow for the year, compared to $9.5 billion a year ago. Furthermore, the company opted to pay $2.5 billion in dividends and share buybacks, which ended up coming out of cash on hand. The company’s announcement of a special dividend further constrains cash flow.

SEC 10-K SEC 10-K SEC 10-K

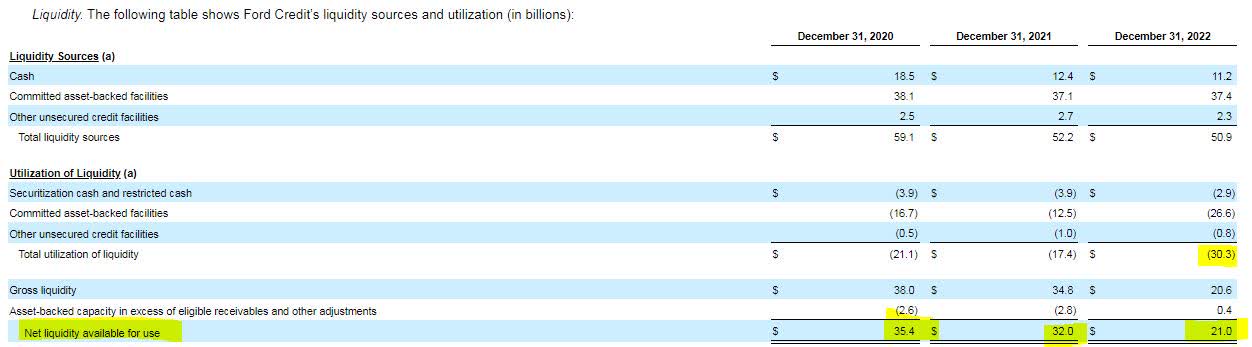

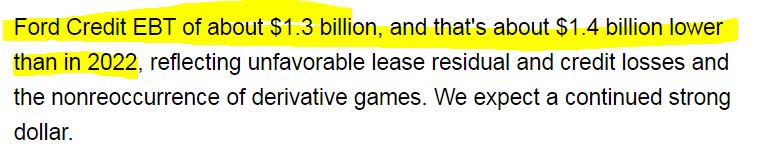

When examining Ford’s financials further, it is becoming clear that the Ford Credit segment is becoming a problem. For 2022, Ford Credit’s earnings before taxes fell by more than $2 billion. Its net liquidity dropped by $11 billion to $21 billion, and its financial leverage ticked upwards. Making matters worse is that management projected another halving of Ford Credit’s earnings for 2023 in the earnings conference call, which is expected to drop by $1.4 billion.

SEC 10-K SEC 10-K Seeking Alpha Earnings Transcript

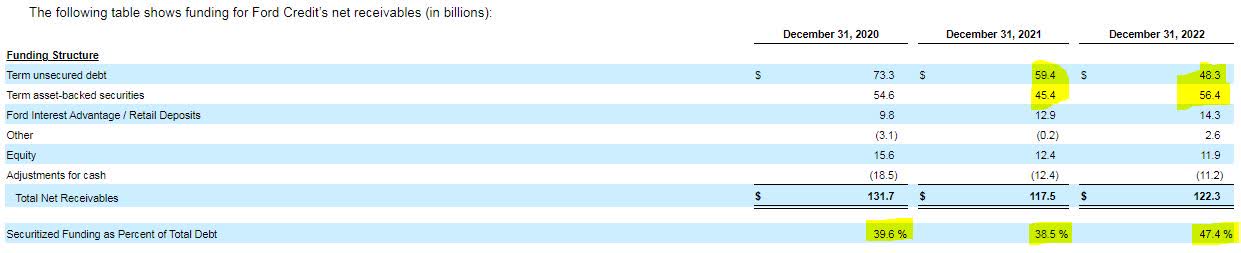

What seems most shocking from the conference call and earnings presentation is the lack of mention of Ford’s debt and the current interest rate environment. While the 10-K does mention interest rate risk, it is compiled in a five-page section describing the various risks the corporation faces. To management’s credit, Ford has shifted away from unsecured debt and towards more asset-backed securities to fund its receivables. Asset-backed securities usually have lower interest rates, but investors need to be cautioned regarding the full scope of Ford’s debt.

SEC 10-K SEC 10-K

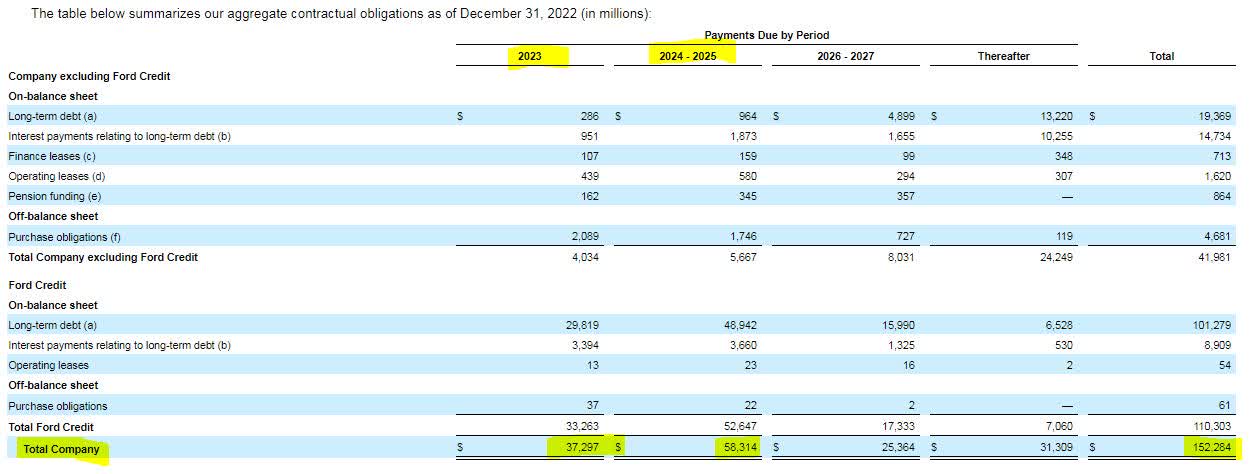

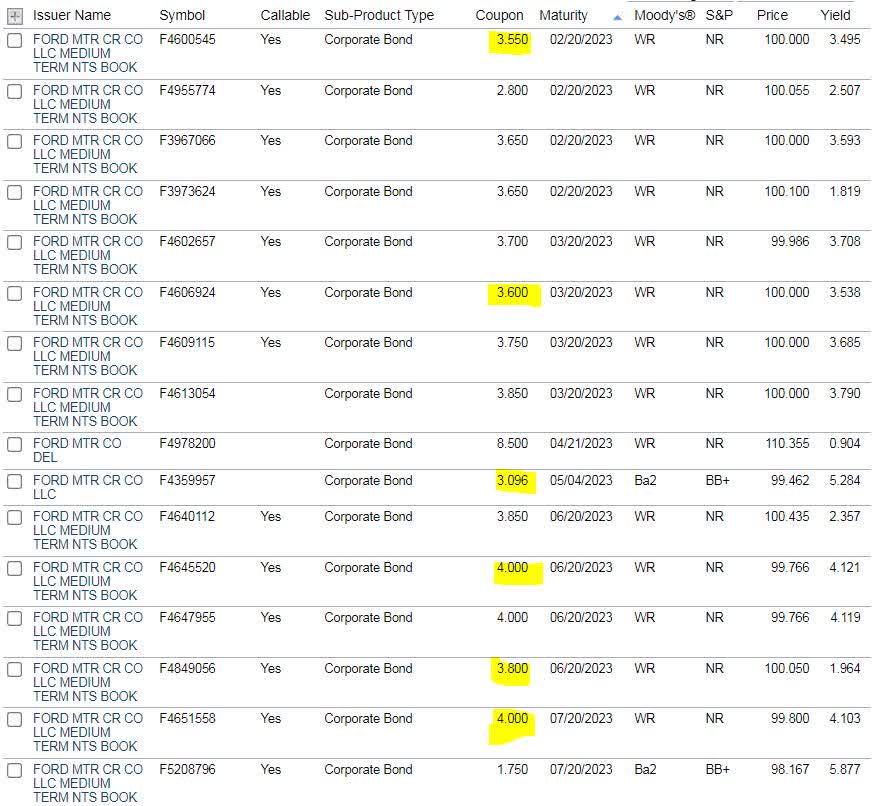

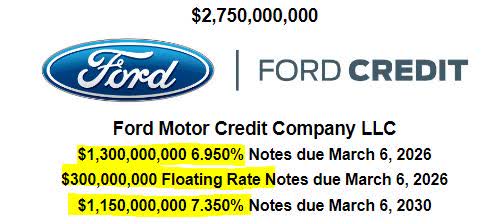

Ford has $37 billion in debt obligations coming due in 2023 and $58 billion coming due in 2024 and 2025 combined. Out of the $95 billion coming due in the next three years, approximately $80 billion is existing principal of long-term debt and $7 billion is interest payments. Ford’s upcoming debt maturities mostly have coupons ranging from 3.5% to 4%. Ford’s newest debt issuance has three notes, with the lowest fixed rate being 6.95%, and floating rate notes of SOFR plus 295 basis points (roughly 7.2% at today’s levels). The refinancing of $80 billion in debt is set to conservatively double Ford’s interest expenses, which would cost the company roughly $2.4 billion per year.

SEC 10-K FINRA SEC 424B New York Federal Reserve

While pressures in the auto market will undoubtedly lead to sales challenges in 2023, investors need to keep their eye on Ford’s debt situation. Ford’s cost to borrow is growing and its free cash flow has disappeared. It seems only a matter of time before the dividend is sacrificed to preserve cash. While solvency isn’t an issue yet and Ford’s long maturity debt is trading at returns above its benchmark, I believe the upcoming earnings erosion will put more pressure on Ford and the bonds. Until then, I’m staying on the sidelines.

Be the first to comment