Albina Gavrilovic/iStock via Getty Images

Intro

We wrote about StealthGas Inc. (NASDAQ:GASS) back in September of last year when we stated that the company needed market conditions to cooperate to see healthy share price gains. Although the company reported sales ($34.89 million) and earnings beats ($6.7 million) in the third quarter, shares are more or less flat since we penned that piece just over three months ago.

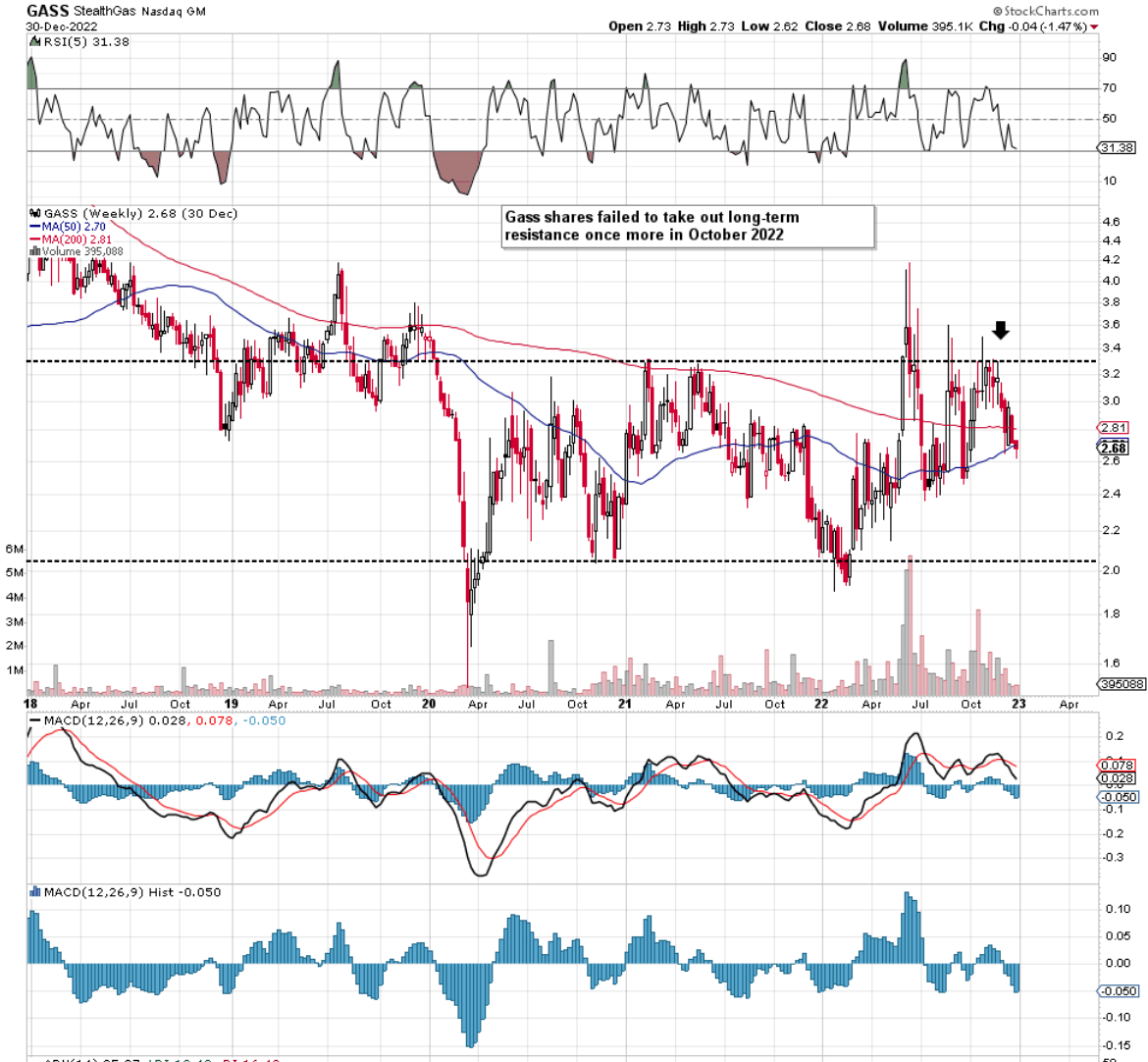

What was noteworthy from a technical standpoint was how shares once more could not break out above long-term resistance in October of last year. In fact, shares are down well over 20% since that October top last year which has subsequently turned that 10-week moving average lower. Although shares may move lower here over the near term, StealthGas’ very keen valuation has meant that short-sellers for the most part have been kept at bay (Short interest ratio of 0.75%).

Gass Long-Term Technical Chart (Stockcharts.com)

Improved Capital Structure

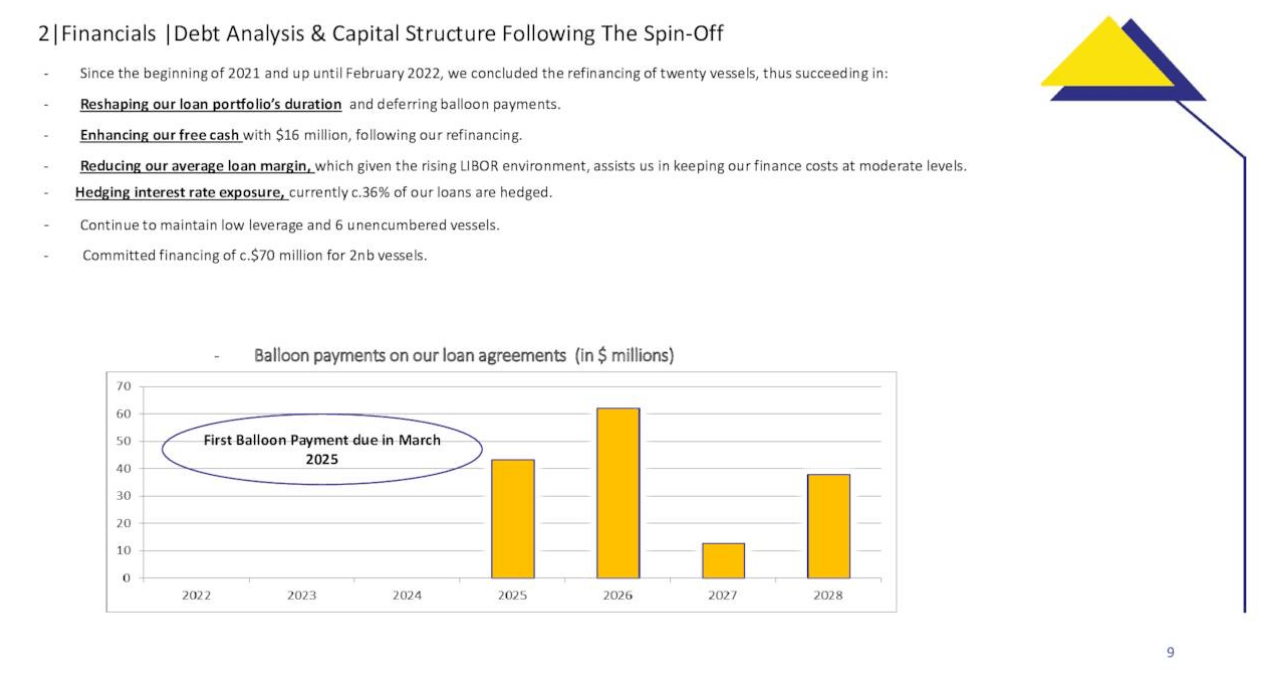

Suffice it to say, from a technical standpoint, StealthGas remains a hold despite the company’s bullish fundamentals across a range of metrics. For one, we see below how StealthGas’ spin-off has really improved the company’s capital structure which has resulted in much-improved operating leverage in the right trading environment. Furthermore, rising rates and a lower spot preference should enable the market price in future cash flow numbers more accurate than before. More cash flow generation will in turn enable management to expand its LPG fleet in size over time. A larger focused LPG fleet would have the potential to really grow the company’s earnings if indeed the right trading conditions were to present themselves on a sustained basis.

Gass Capital Structure Following Spin-Off (Q3 Company Presentation)

Elevated Risks

Risks to GASS’ business on the other hand (which could seriously impair the company’s earnings growth curve due to the high fixed cost nature of the business) stem from rising inflation globally as well as another significant spike in Covid cases in a country such as China, for example (World’s largest LPG importer). Just one headwind in any of the above would most likely lead to suppressed LPG demand especially if a serious Covid outbreak were to gain traction.

Suffice it to say, GASS shares are where they are because the market has priced in the ramifications of both the strengths of the business as well as the prevailing risks. This is something that value investors many times cannot fathom. The fact that shares are trading with a book multiple of 0.2 and a forward GAAP earnings multiple of 3.35 seems ludicrously cheap on the surface. However, the market clearly believes the valuation is not sufficiently low enough when compared to the company’s present profitability. Therefore, the valuation in earnest needs to go lower or profitability needs to go higher to move the share price in earnest.

Encouraging Forward-Looking Earnings Estimates

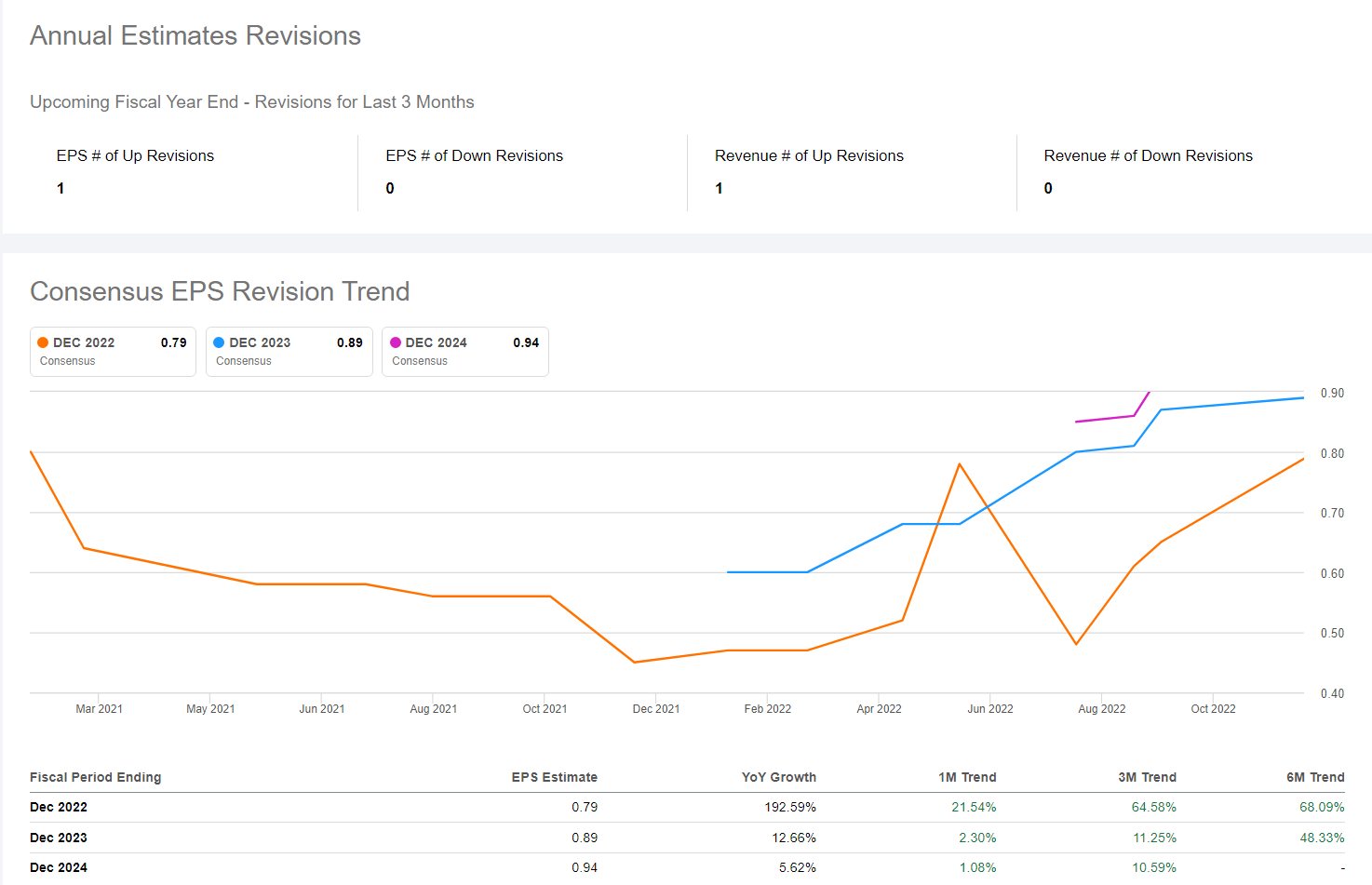

With respect to this, GASS bulls should be encouraged by how forward-looking earnings estimates continue to impress as we see below. Analysts are expecting the shipping company to report $0.79 per share this year followed by $0.89 per share in fiscal 2023. If next year’s present earnings estimate is beaten, for example, one is looking at a GAAP 2023 earnings multiple of under 3 which is what we want.

GAAP: Annual EPS Revisions (Seeking Alpha)

Bottom-line profitability though (given GASS’ sizable debt load) will continue to be dictated to a large degree by how interest rates move going forward. In fact, we just have to look at the Q3 this year to see how gross interest expense grew sequentially from $2.8 million to $3.6 million. Although management states that GASS is protected somewhat against higher interest rates by having a declining debt load & hedges on a sizable percentage of its debt, the company’s present $284 million debt load still stands at almost three times the company’s present market cap. This is why (In terms of trading conditions), GASS needs to stay ahead of the curve to ensure there is ample EBITDA to be able to drop to positive bottom-line profits.

Conclusion

Therefore, to sum up, we will continue to be guided by the technicals in this play. From a “value play” perspective, shares remain ultra cheap but GASS needs substantially more growth before shares have any possibility of breaking out of their long-term trading range. We look forward to continued coverage.

Be the first to comment