MBPROJEKT_Maciej_Bledowski

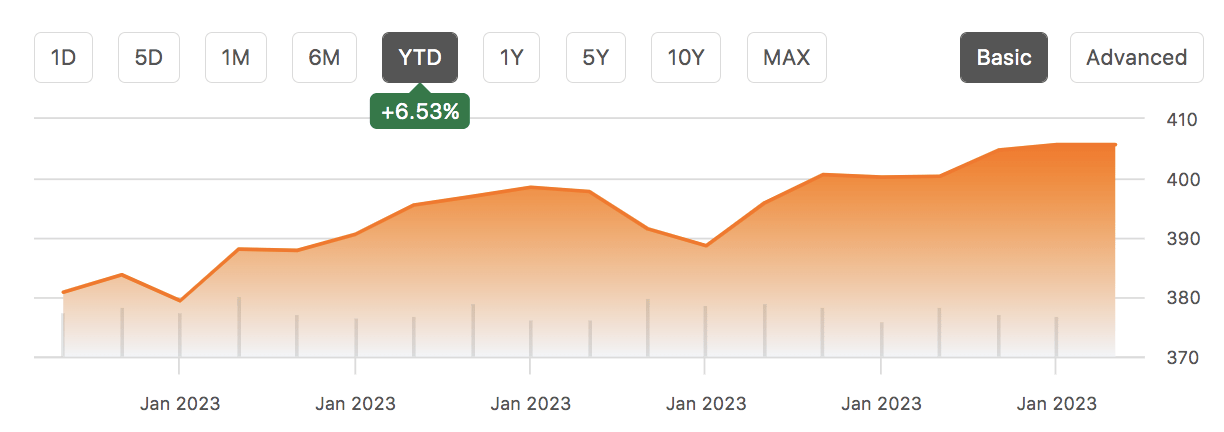

The SPDR S&P 500 Trust ETF (NYSEARCA:SPY) has received significant support since the turn of the year, yielding more than 6% in price returns. The breath of debate about the exchange-traded fund’s (“ETF’s”) year-to-date performance is far and wide. However, a uniform explanation of the fund’s recent performance needs to be established to lend investors objective information, allowing for a basis to develop investment strategies.

The SPY is constrained to the S&P 500 index (SP500) and presents infinitesimal tracking errors. Therefore, this article assesses the ETF and the S&P 500 index interchangeably.

Seeking Alpha

Assessing And Determining Returns

The common rhetoric is that the SPY’s year-to-date recovery is bound to factors such as moderating inflation, higher than anticipated U.S. GDP, a Covid reopening in China, and softening non-core inflation. Although these features are cohesive with a bullish argument, more depth is required to comprehensively understand the SPY’s latest return distribution.

Seeking Alpha

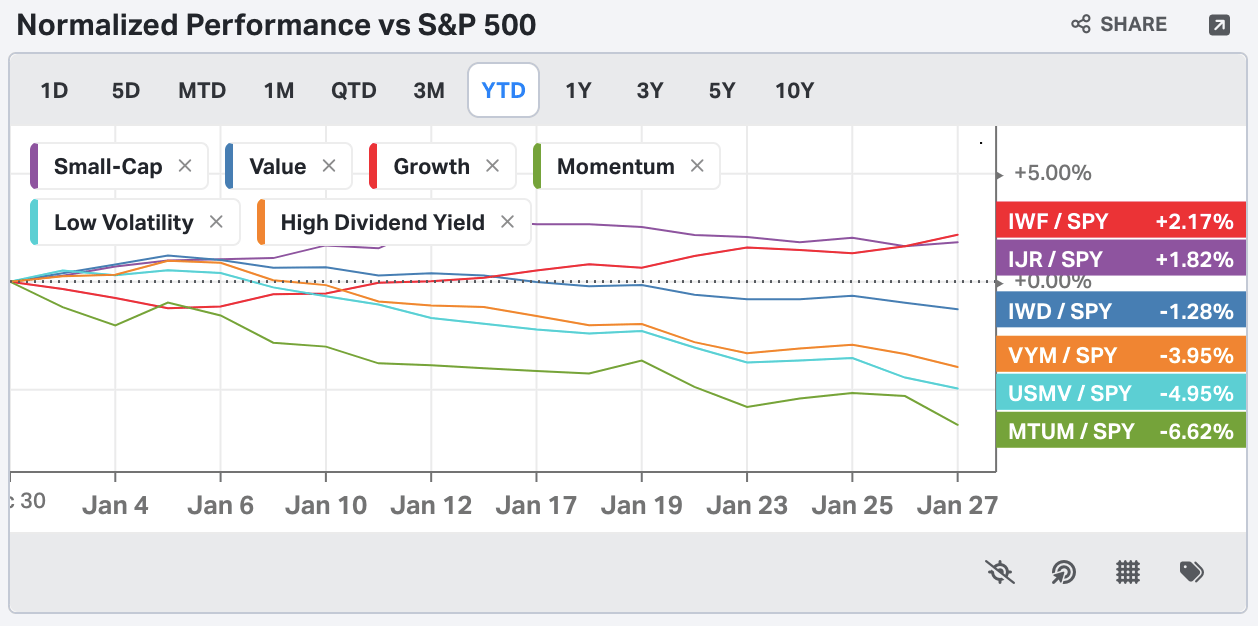

A cross-style diversified portfolio, such as the S&P 500, has illustrated robust year-to-date returns. However, segments such as growth and small-cap stocks are experiencing excess returns. Note that modern financial theory contradicts the great Warren Buffett’s claims that the market cannot be timed and that a general index fund will beat high-conviction investment portfolios.

Segment Relative Return Vs. S&P 500 (KoyFin)

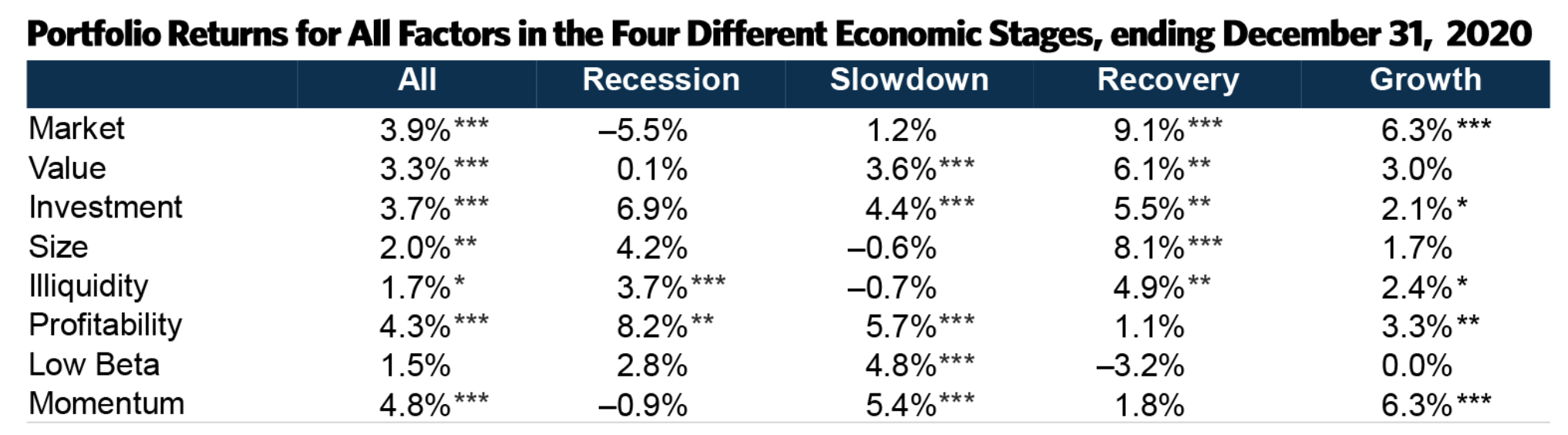

A regression analysis of the U.S. stock market by Research Affiliates illustrates the effectiveness of market segmentation during various stages of the economic cycle. At Pearl Gray, we believe the global economic outlook is uncertain; however, we think the most likely scenarios for 2023 will be a recession or a recovery.

What is our premise?

As mentioned earlier, various qualitative factors have improved since last year. In fact, the macroeconomic picture is a lot brighter than many anticipated for 2023. Nevertheless, interest rates remain elevated, and inflation has a long way to recede before reaching its 2% to 3% benchmark. Thus, it will be no surprise if contractionary policies resume, consequently sinking the U.S. and global economy into the abyss.

To conclude this section, headline data indicates that if our macroeconomic assumption of a recession/recovery midpoint realizes during 2022, the market will grant preference to small-cap stocks (size in the diagram below), securities with low CapEx (investment in the diagram below), quality stocks (profitability in the diagram below), and value assets.

An early recovery could result in the market portfolio outperforming other segments. However, onboarding recession risk is not worth it, in our opinion.

Research Affiliates

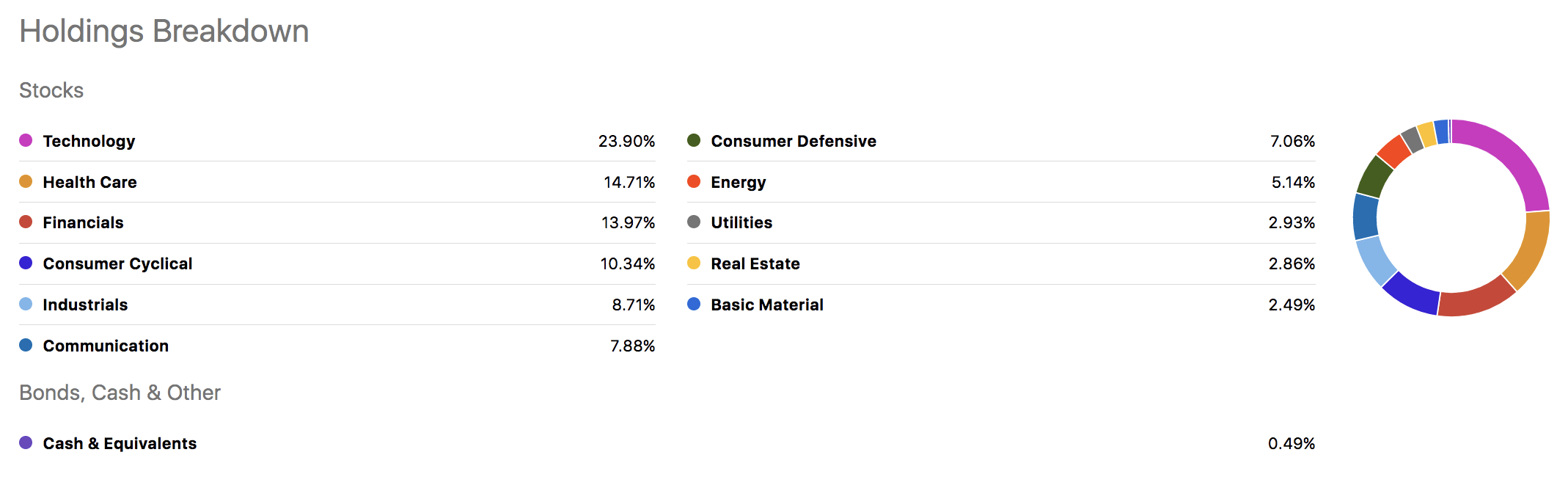

Portfolio Allocation

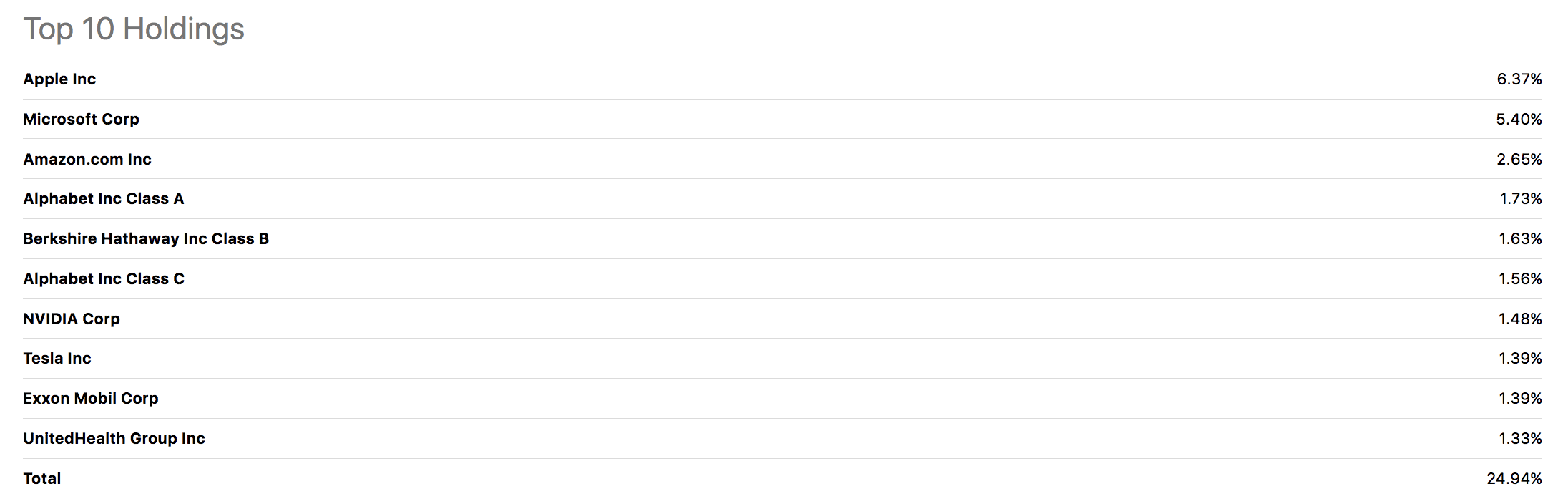

The SPDR S&P 500 Trust ETF’s top 10 holdings provide a wide enough breadth to apply representative sampling as a means of assessing the vehicle’s prospects.

At face value, the SPY’s allocation to technology and consumer cyclical stocks might seem risky. However, the idiosyncratic features of the ETF’s constituents must be considered.

Focusing on technology first, companies such as Microsoft (MSFT), Alphabet (GOOG), and NVIDIA (NVDA) possess high volatility, leaving them vulnerable to recession risk. However, they also contain quality risk factors such as liquidity and profitability. As such, we remain neutral on these bets, coherent with Research Affiliates’ regression analysis and our own judgment.

Seeking Alpha

Furthermore, the SPY owns shares in consumer cyclical stocks. We believe cyclical stocks could jolt this year after a severe selloff last year. More specifically, we think large market capitalization cyclical might bounce as market participants opt to invest in quality companies at low prices.

Seeking Alpha

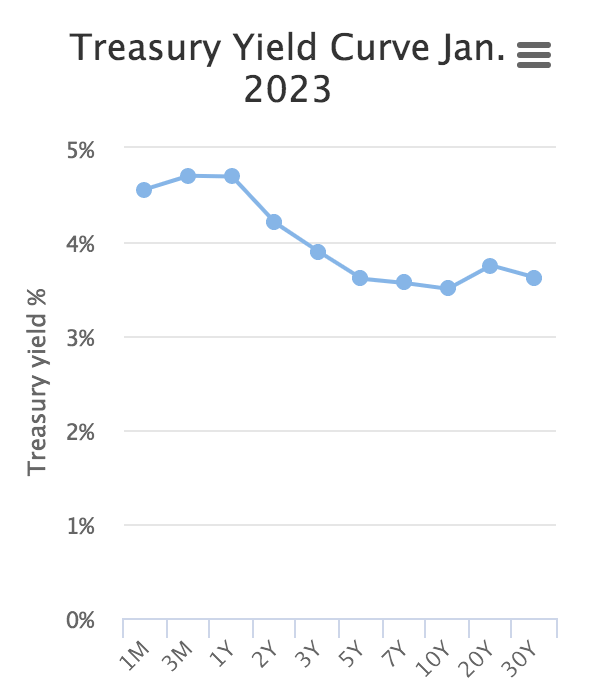

Lastly, the SPDR S&P 500 Trust ETF’s exposure to financials is encouraging as interest rates remain supportive. On top of that, recovering equity and bond markets will likely add value to banking stocks’ balance sheets.

Although we are bullish on banking stocks, we remain cautious of the yield curve’s continued downward trajectory. Banks typically borrow at short-term rates and lend with longer durations. Thus, banks could face significant obstacles if a deep recession unfolds and the yield curve’s downward slope sustains.

U.S. Yield Curve (Gurufocus)

Valuation & Carry

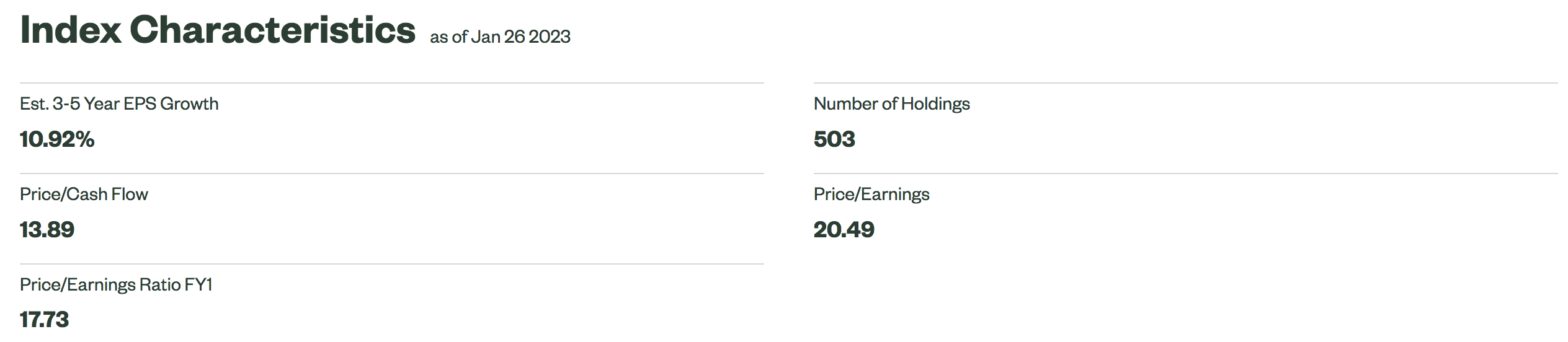

Asset returns are parted into two components, price appreciation and carry. The SPDR S&P 500 Trust ETF’s valuation metrics provide an enticing juxtaposition. For example, the fund’s P/E ratio is elevated; however, its earnings-per-share growth remains robust, suggesting an elevated P/E is not a concern.

State Street

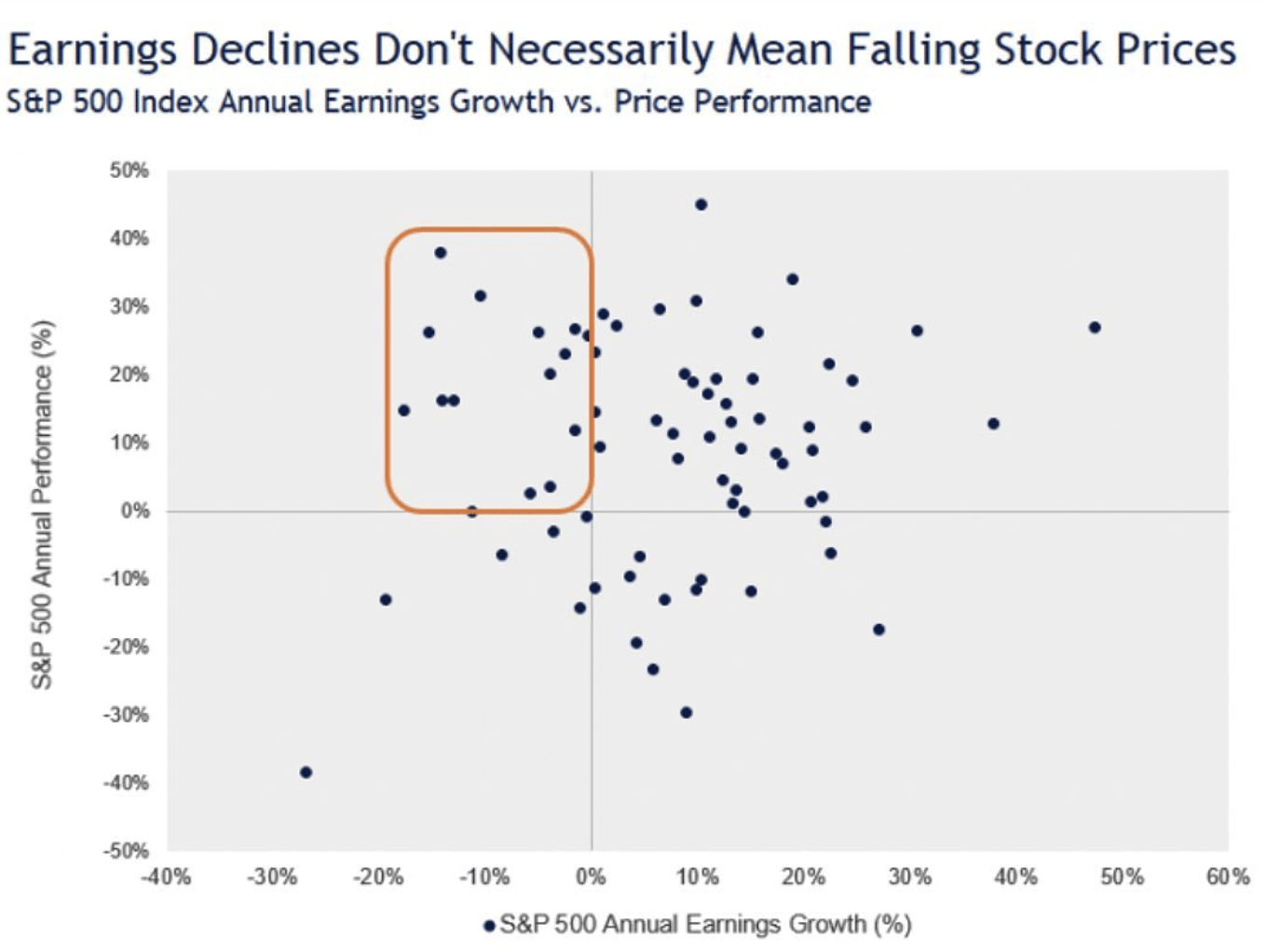

Looking at valuation ex-ante, we are concerned about potential earnings compression, which would reset the ETF’s valuation base. However, receding earnings do not necessarily result in a market drawdown, which is a crucial consideration.

Market Radar

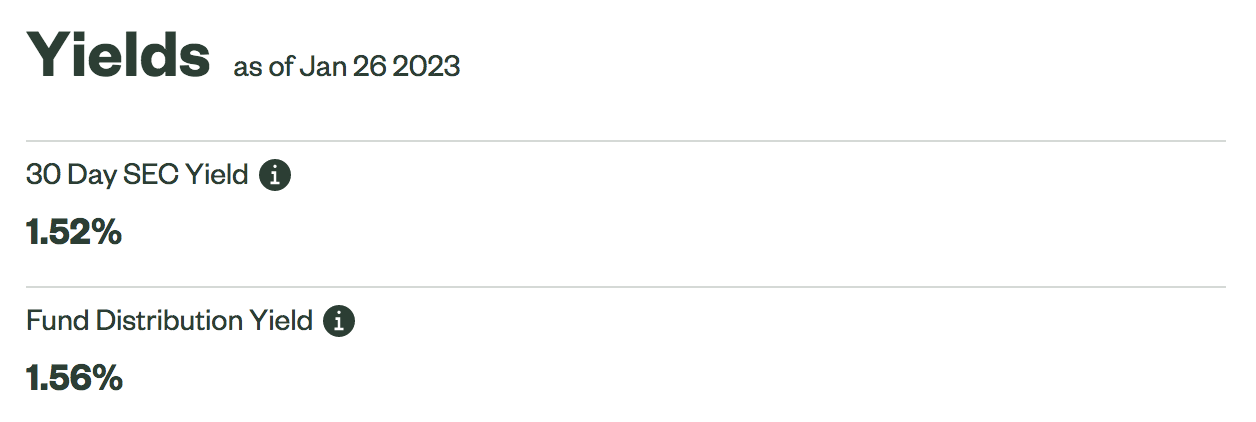

Although the ETF’s valuation metrics are reasonable, its income-based prospects are underwhelming, with a dividend yield of merely 1.56%. In our opinion, there are better income-generation vehicles out there.

State Street

Final Word

Stock returns and concurrent economic circumstances are not always coherent. Headline macroeconomic variables suggest that the S&P 500 and SPDR S&P 500 Trust ETF could suffer from slight earnings compression. However, regression analysis conveys that specific stock segments might surge in either a recessionary period or during the early stages of an economic recovery.

The SPDR S&P 500 Trust ETF’s allocation in high-quality stocks and “beat down” cyclical assets could be advantageous this year. However, exposure to financials might jeopardize the vehicle’s prospects if the yield curve’s downward slope sustains.

Despite various positives, much uncertainty remains, leading us to favor high-conviction portfolios over a diversified portfolio such as the SPDR S&P 500 Trust ETF. Additionally, considering potential earnings compression, the ETF’s subdued dividend yield could soon be accommodated with higher price multiples.

- We hereby upgrade SPY to Hold.

Be the first to comment