KanchitDon/iStock via Getty Images

Investment Thesis

Spotify (NYSE:SPOT) is the market leader in music streaming but has not yet turned this into profit. According to the company itself, the revenue could be $100B in 2030. However, I think this target is quite unrealistic. Spotify is difficult to analyze because it´s a guessing game to predict how margins and costs will develop. So far, costs have increased at the same rate as revenue. For this and other reasons, I would not invest in the company at the moment.

Industry Overview

The global music streaming market is expected to grow at a compound annual growth rate of 14.7% from 2022 to 2030. In 2021, the estimated market size was $29B, according to grandviewresearch.com. Several factors are driving this growth. One of the main drivers of growth has been increasing global Internet and smartphone coverage. However, this growth driver will likely soon end as almost the entire world is already connected to the Internet and owns smartphones.

As internet speeds are getting faster, the streaming quality is improving, and more services are offering lossless streaming. Additionally, the future possibilities of VR and AR are expected to create new application areas in the music streaming market. For example, concerts could be streamed in virtual reality, allowing users to move around and explore the concert from different perspectives, creating unique and immersive concert experiences such as virtual backstage tours or special effects that would not be possible in a traditional concert setting. This also allows people worldwide to attend concerts virtually, which they would not have the opportunity to do in real life due to their geographical location or cost. Furthermore, streaming companies are expanding into other areas, such as podcasts, audiobooks, and other offerings like relaxation techniques and active meditations.

The goal of Spotify

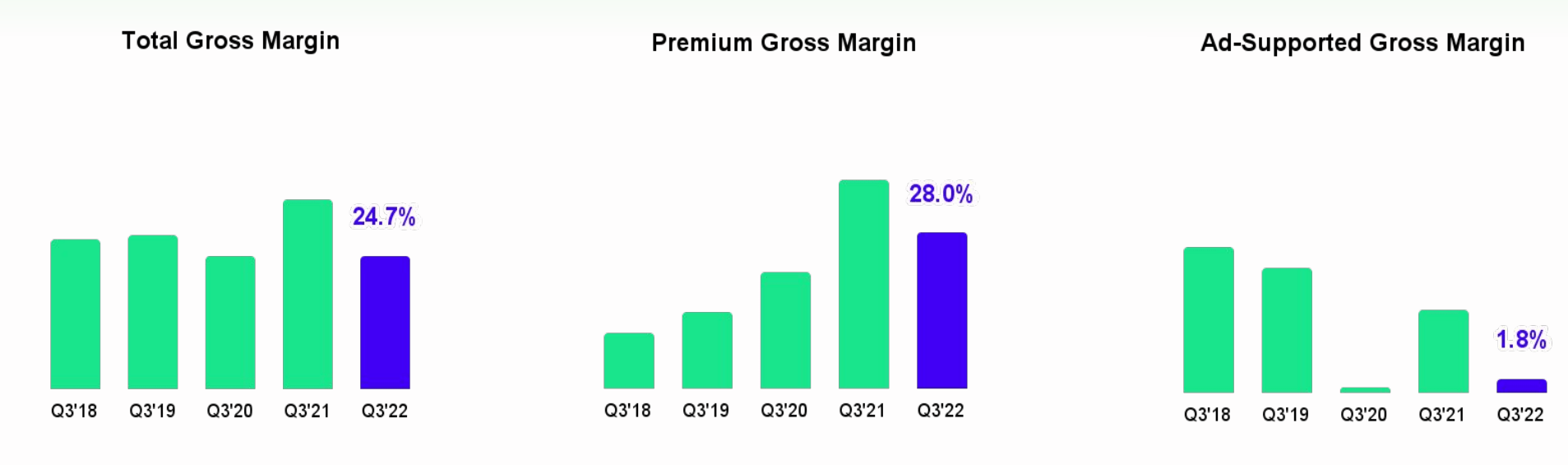

Spotify is the leading digital music service, holding a 30% worldwide market share, ahead of competitors Apple Music (14%), Tencent Music (13%), Amazon Music (13%), and YouTube Music (9%). At Investor Day 2022, Spotify CEO Daniel Ek discussed the company’s growth strategy, which includes expanding its podcast and audiobook business through acquisitions to become a comprehensive platform for users, artists, and advertisers. Ek predicted annual revenue of €100B and a gross margin of 40% over the next decade, compared to €9.6B and 26.3% in the last fiscal year.

So from everything I see, I believe that over the next decade, we will be a company that can generate $100 billion in revenue annually, and that we can achieve a 40% gross margin and a 20% operating margin.

And I know it seems challenging to put all this into a financial model, because frankly this type of company has never existed before, that is exactly my point. The businesses that never existed before are always the most valuable to have invested in over the long term.

CEO Daniel Ek

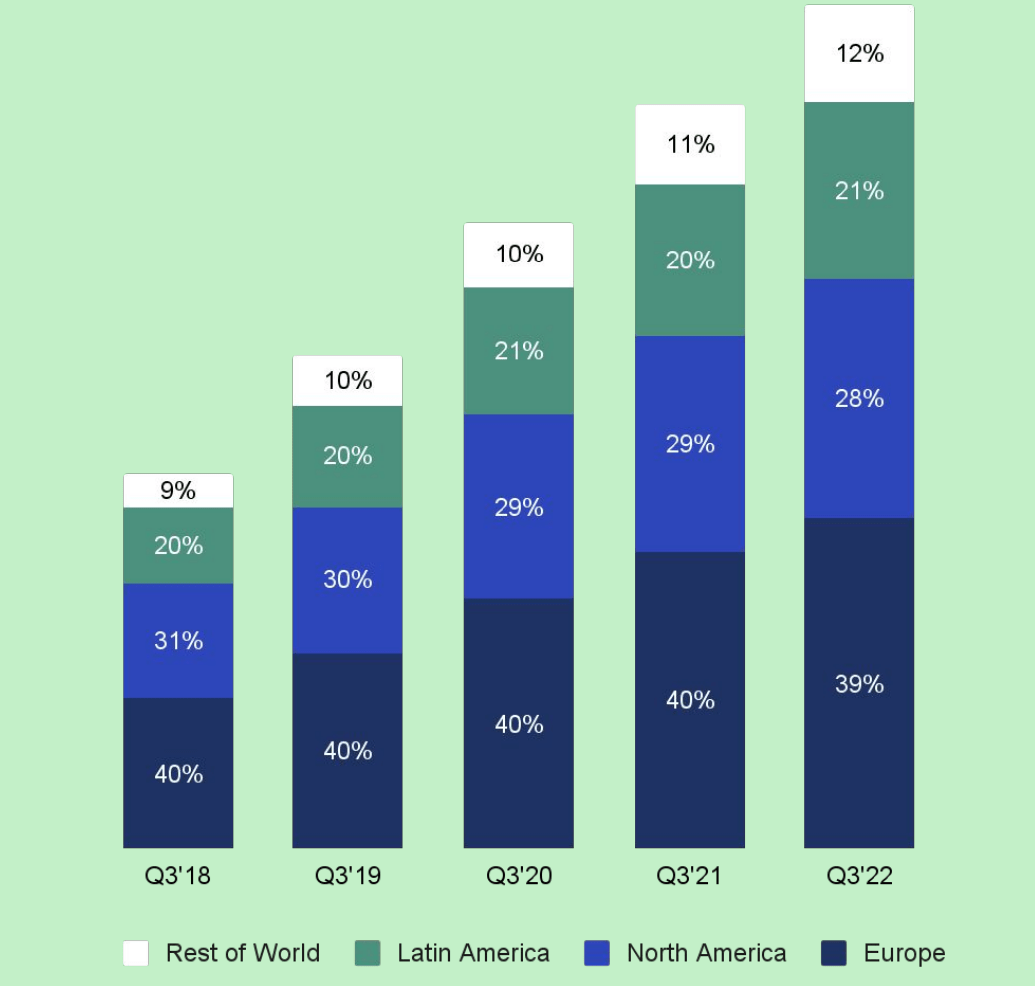

Here are some figures about the current situation: Total MAUs grew 20% Y/Y to 456M, up from 433M last quarter and above the guidance by 6M. According to the company, the growth came mainly from the Indian and Brazilian markets. Premium subscribers grew 13% Y/Y to 195M, up from 188M last quarter. This growth was also primarily driven by Latin America.

Spotify Q3

Recent results & financials

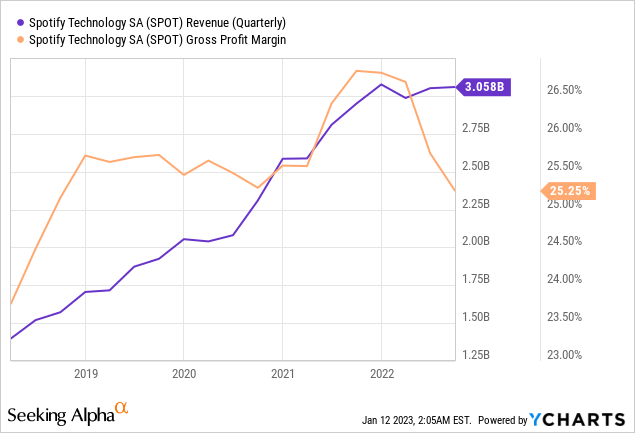

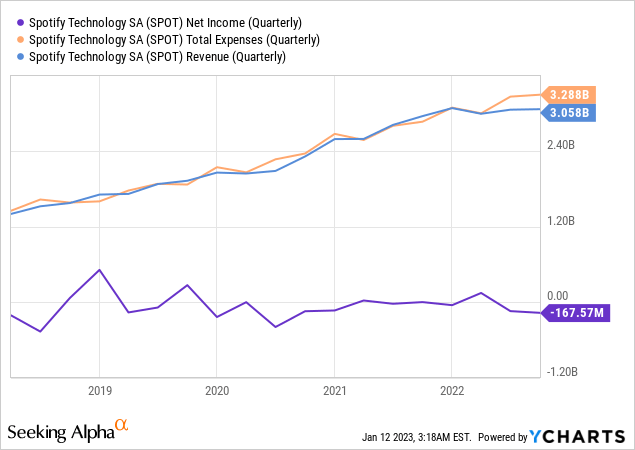

In the last quarter, only 13% of Spotify’s revenue came from advertising. The majority of revenue, 87%, is generated from premium subscriptions. For 2022, revenue will be approximately $12.53B, and EPS about -$2.5.

Given this year’s revenue of $12.53B, the management target of $100B in 2030 looks ambitious. That is an eightfold increase, and an 8x increase in Premium users would correspond to 195M x 8 = 1.56B.

Of course, this calculation is incorrect because Spotify is relatively inexpensive in many countries, and if incomes were to rise there, Spotify would be able to adjust its prices upward. In western countries, however, the price increase potential is limited because of constant competitive pressure. They could get away with being slightly more expensive than the competition, but that has limits.

There are also other sources of revenue, such as potentially higher advertising revenue from small artists who pay to get more coverage. The management says that the goal is one billion users, and the revenue per user should increase strongly to reach this ambitious goal of $100B.

Right now, we’re on track to more than double our reach to over 1 billion users. And with our vertical platform strategy, over time our ambition is to build the business toward an annual ARPU of €100. This means, on average, looking at both free and paid, we can significantly increase the total revenue across our entire user base.

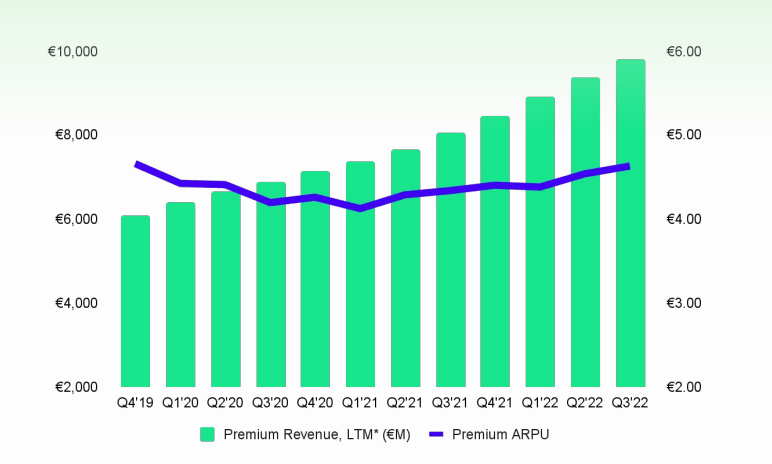

An annual worldwide ARPU (average premium revenue per user) of €100 would mean that these billion people would have to be premium users, and the whole world would have to pay the current Western prices. Both assumptions seem pretty unrealistic to me. According to businessofapps.com, Spotify’s ARPU has fallen from €4.89 in 2018 to €4.29 in 2021. An ARPU of €100 would be a 23-fold increase while doubling the number of users. That seems too far-fetched to me. In addition, Spotify is not active in China at all, which means that over a billion people are excluded from the possible users.

Q3 Spotify

Valuation

The company is currently valued at an enterprise value of $15.7B. The market cap is $17.5B, and the total debt is $1.83B. At the moment, earnings per share are still negative, and analysts do not expect them to become positive until 2025. This is mainly due to high capital expenditures.

Spotify is experiencing a growth period accompanied by an increase in operating costs. These increased by 65% compared to the same quarter of the previous year. This results from various acquisitions, higher personnel expenses, and higher costs for research and development. The company did not meet the profitability expectations of analysts, as reflected in the EBIT and gross margin figures. These shortfalls are attributed to global economic and political factors and currency fluctuations caused by the continued strength of the US dollar. These costs negatively impacted the EPS, resulting in a significant loss of $0.86.

Otherwise, the valuation is relatively tricky here. The P/S ratio is only 1.4, which looks pretty cheap for the market leader in the music streaming sector. However, it is probably justified that it is so low because this revenue does not generate a profit. Overall, I find it virtually impossible to predict future margins. These are developing relatively slowly in a positive direction for premium users, but where these could stand in 2025 or even later is a guessing game.

Q3 Spotify

The same applies to how the cost structure will develop in relation to sales. For years, both have developed in parallel. Will this change at some point in the future? When exactly and why? In my view, these questions cannot be answered – the company itself is talking about a possible $100B revenue in 2030, but no analysis can be made based on this statement – after all, companies are not always correct, especially when they are talking about seven years in the future.

Therefore, I would like to refrain from a cash flow analysis looking years into the future, which in my view, simply contains too many variables and is too much of a guessing game. Ultimately, the question of valuation depends on whether user numbers and revenue per user continue to grow strongly because Spotify is obviously a scalable company. But I think a billion (premium) users seem unrealistic. There’s too much competition and too many people unwilling to pay the premium price.

According to fastgraphs, analysts estimate EPS of $2.23 in 2025. That would still be a P/E of 41 on the current share price.

Risks

The music streaming industry, and therefore Spotify, has several additional risks. On the one hand, it is a possible form of entertainment and thus competes not only with other music streaming services but also with Netflix, YouTube, Audible, and so on. This is less of an issue when users pay a subscription fee anyway, but the less you use a service, the more likely you are to cancel it. Furthermore, there is an intense concentration on only a few major music labels (Warner, Universal, and Sony), which means they have some power over Spotify. You could also see it as a mutual dependency, but in my view, the music labels have more power. In a price war, Spotify would suffer more if the labels’ music disappeared from their platform but is still available on other streaming services. Ultimately, it doesn’t matter to the music labels which service the consumers choose.

Share dilution and insider selling

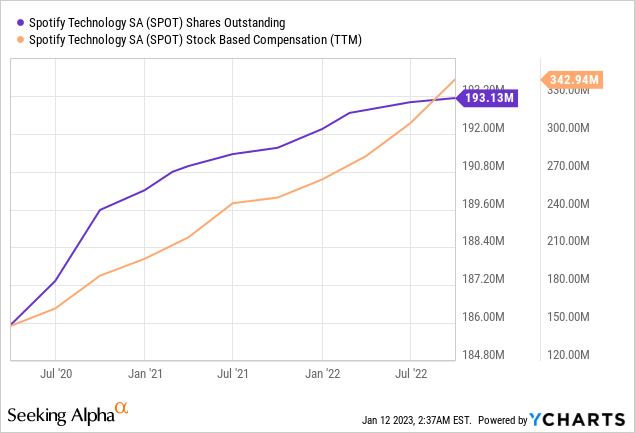

I always want to look at stock dilution and whether there is insider selling. I have not been able to find any information about insider sales. The number of shares has been increasing relatively slowly but steadily for years. Stock-based compensation is increasing even faster and currently adds up to about 3% of sales. So as a shareholder, you have a steady, slow headwind.

Conclusion

Spotify undoubtedly offers a good product. But so far, the company has not managed to turn this good product and the millions of users into sustainable cash flow that shareholders can also benefit from. I would not invest here primarily because the future (financial) development is hard to assess. This analysis is much easier if there are already positive cash flows, announced share buybacks, a dividend, or similar. In addition, Spotify does not have a moat from my point of view, but users could switch at any time and transfer their playlists. Overall, I think there are better investment opportunities in the current market. Adobe (ADBE), for example, also has a subscription model but makes a lot of money and has a much larger moat. I’m also not convinced from a user perspective. I used to be a premium user, but I find the combination of YouTube without ads plus YouTube Music more attractive, so I switched.

Be the first to comment