Jerod Harris/Getty Images Entertainment

Investment Thesis

Sonos (NASDAQ:SONO), a pioneer in multi-room wireless audio systems, is known for its craftsmanship and innovative work. Although its ecosystem could continue to support its organic growth, the company needs to manage its near-term challenge of weak cash flow. After assessing its bullish and bearish cases, we find its current price is fair tilted bullish.

Company Overview

Sonos, founded in 2002 in Santa Barbara, CA, created and debuted the world’s first multi-room wireless audio system. Its products include wireless, portable, home theater speakers, components, and accessories, with content delivered on an open platform. Its pioneering work garnered followers and reviews that eventually formed an ecosystem that continued today.

Strength

Since Sonos created its first products of home audio system, it took almost ten years for their competitions to start emerging and get caught up. And Apple (AAPL) didn’t even enter the competition until almost 14 years later. So Sonos had enough time to build a loyal customer base and solidify its leading position in the space.

Sonos Competition Timeline (Sonos Q3 Presentation)

Being the early innovator, Sonos benefits from a mature and extensive ecosystem of its many product offerings and core user base support. Its open platform acts like a marketplace for content partners, giving customers freedom of choice. It has 130+ content partners that range from music to podcasts, from audiobooks to radio stations, from all over the world. This is also an essential part of its ecosystem – one in which Sonos plays the role of the platform and content host. It calls this the partner ecosystem.

Sonos Content Partners (Sonos Q3 Presentation)

Since competition emerged, Sonos has maintained an average 20% CAGR of user base growth. This is impressive particularly in existing households.

Sonos Sale Growth (Sonos Q3 Presentation)

Its core user base continues to buy additional products. The products sold per single-product household have increased from 2.82 in 2018 to 2.98 products in 2022, while per multi-product household increased from 4.6 to 8.4 products. In this regard, the Sonos ecosystem is where the products complement each other to build out the household’s audio system. That’s why it stems from the need to buy more products for a single household.

Sonos Products Growth per HH (Sonos Q3 Presentation)

Another ecosystem Sonos building out is an e-commerce channel, as it targets consumers to shift from physical to online sales channels. This direct-to-consumer sales channel represented 22.5% of its revenue in 2022, and 24.2% in 2021. It also partners with third-party retailers and custom installers to drive its growth. It generated 21.2% of total revenue through the installer solution channel. Most investors wouldn’t think of Sonos as an e-commerce company, so this seems to deviate from its core product proposition as an audio system provider. But facing its competition (we will discuss in a later section), this branching-out effort could better utilize its already in-place ecosystem to improve revenue. Its overall ecosystem helps increase sales, lower cost, and promote organic growth.

In essence, Sonos still rely on solid research and technological innovation to support its growth. It continues investing in core product and software development with a growing patent portfolio that reached almost 10 folds more than in 2014, again the year its real competition emerged. This protects its premium product offering and leading position.

Sonos Patent Portfolio (Sonos Q3 Presentation)

While in the long term, Sonos’ potential market shares to grow to remain enormous. Sonos has only 9% of the total Affluent Households market and 2% of the Premiums Global Home Audio market, far from being in a dominating position. The company has 45% of its revenue generated from markets outside of the U.S., so this potential market it focuses on is on a global scale as well.

Sonos Long Term Market Potential (Sonos Q3 Presentation)

Weakness/Risks

Weak Near-Term Cash Flow

The company’s TTM operating cash flow less CAPEX has declined to negative for the first time since its IPO. This is both due to the negative operating cash flow in 2022 and the continued rising CapEx overall.

Sonos OpCF minus Capex (Calculated and Charted by Waterside Insight with data from the company)

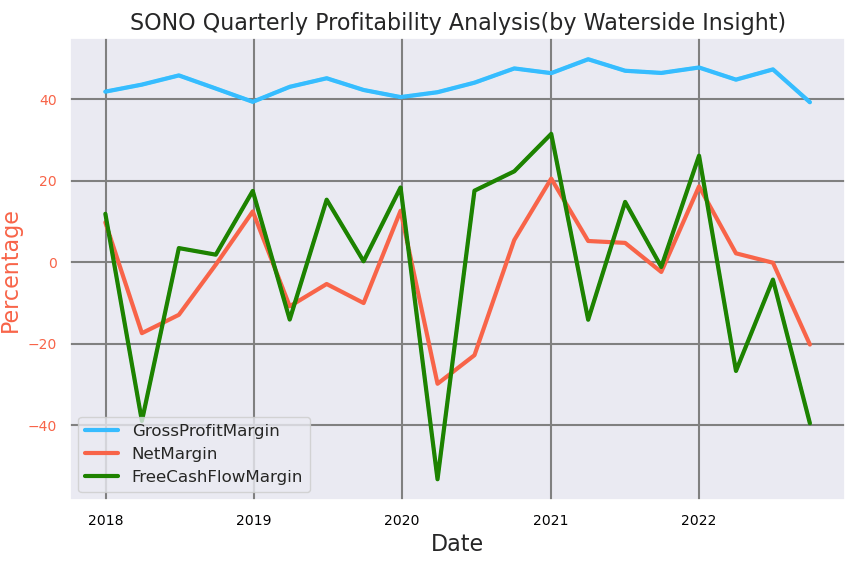

Although its gross profit margin has held up, its net margin and free cash flow margin have been squarely in the negative in 2022, and the downward trend continued in its last reporting. Note that Sonos’ sales have a strong seasonality embedded- it experienced the highest revenue levels in the first fiscal quarter with the holiday shopping season and in-time promotional activities. So that resulted in a lower gross margin but a higher operating margin due to higher sales volume and positive operating leverage. In turn, it has a higher free cash flow margin for the quarter. However, looking at the seasonality in 2022, the decline after the holiday season was more substantial than in previous years. Although the data below is quarterly, it echoes the weakness of the TTM data in the chart above.

Sonos Profitability Analysis (Calculated and Charted by Waterside Insight with data from the company)

Inventory

The company’s inventory build-up reached its highest level since its IPO. Its inventory-to-revenue ratio has reached 1.4 times, substantially higher than in 2021.

Sonos Inventory Analysis (Calculated and Charted by Waterside Insight with data from the company)

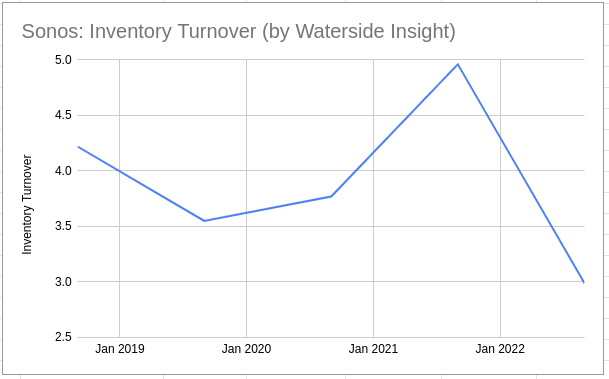

Its inventory turnover experienced a jump in Q3 2021 and a slowdown in 2022.

Sonos Inventory Turnover (Calculated and Charted by Waterside Insight with data from the company)

The inventory build-up reflected the management’s response to the supply shortage it experienced in the past two years that resulted in sales constraints, as the company reported. The turnover rate was not sharply declining even though the inventory level jumped by almost double in 2022. Perhaps that shows some strength in its sales. However, unless this past holiday season can sufficiently lift the sales back to, say 4x, for the turnover rate, it might become a concern in the near term.

Competition

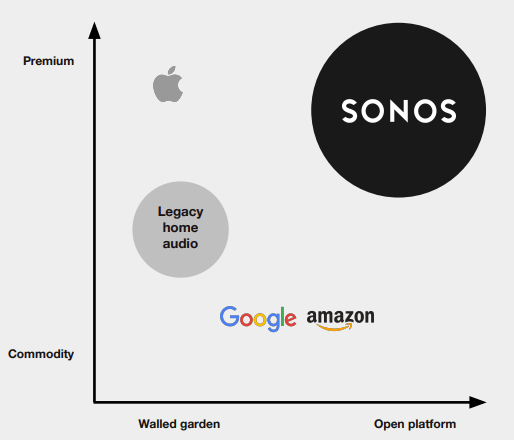

Few companies can say they have a stiff competitor in all three of Apple, Google (GOOG), and Amazon (AMZN), and Sonos is in such a position. If you consider both an open platform and a premium product, it is leading the competition, but the pressure to perform and lead continues to build up. Although Google and Amazon’s systems are not as premia an audio system as Sonos, they have built-in AI functions to help with household activities. Sonos’ e-commerce channels in some way respond to this competition, but without providing some similar functions, it is hard to say if that will edge out potential customers who have never purchased its products or are not in the fan base yet.

Sonos Competition Scale (Sonos Q3 Presentation)

Financial Overview

Sonos Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

Valuation

Taking consideration of all our analysis above, we use our proprietary system to assess Sonos’ fair value with ten years projection forward. The company has volatile cash flow, albeit it is a new public company. We factored in a certain maturity in its later year’s growth that the cash flow would stabilize. What we found is in the most bullish case, where the company has a similar 2023 as in 2022, but pulled back to positive cash flow in 2024, and it can leverage its ecosystem, maintain a steady sales pace and continue to innovate, it was valued at $26.69. In the bearish case, where the financials worsened in 2023 with improvements coming in 2024 but still had negative cash flow, and it recovered later on with more steady growth, it was valued at $11.38. In our base case scenario, where the company has a similar 2023 as in 2022, but a lot of improvements realized in 2024 with yet negative cash flow, and it staged a jump afterward to maintain a good growth rate and become more stable, it was valued at $19.15. In all cases, 2023 is expected to have negative cash flow and challenges, but the main difference was the expectations for 2024. It seems the market is currently pricing closely to our base case. Investors are perhaps taking a wait-and-see mode, but the expectations for 2023 and 2024 would be the main difference affecting their investment decision.

Conclusion

Considering Sonos’ first-comer advantage, thriving ecosystem, and strong innovation capacity, the company still has a lot of growth ahead of it. However, its near-term weakness is visible and might be the first significant challenge for the company to overcome after being publicly listed. We believe its current price is a reflection of both aspects. It is fair-priced, and we recommend a hold for now.

Be the first to comment