anyaberkut

1. Introduction

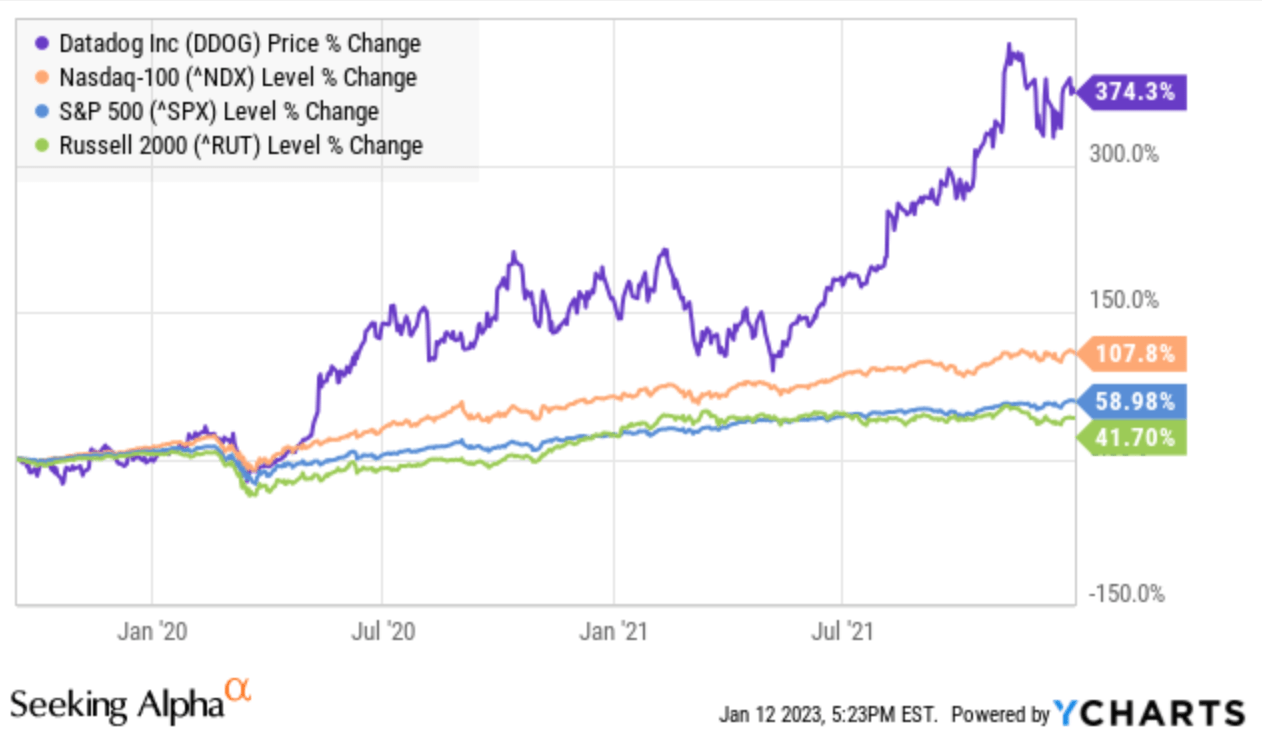

We are in the midst of a bear market and growth stocks have suffered the most. One of them is the hyper growth cloud monitoring company Datadog (NASDAQ:DDOG), which delivered tremendous returns of around 400% for its investors after its IPO until the current bear market (see chart).

DDOG price % change since IPO vs major indices (YCharts)

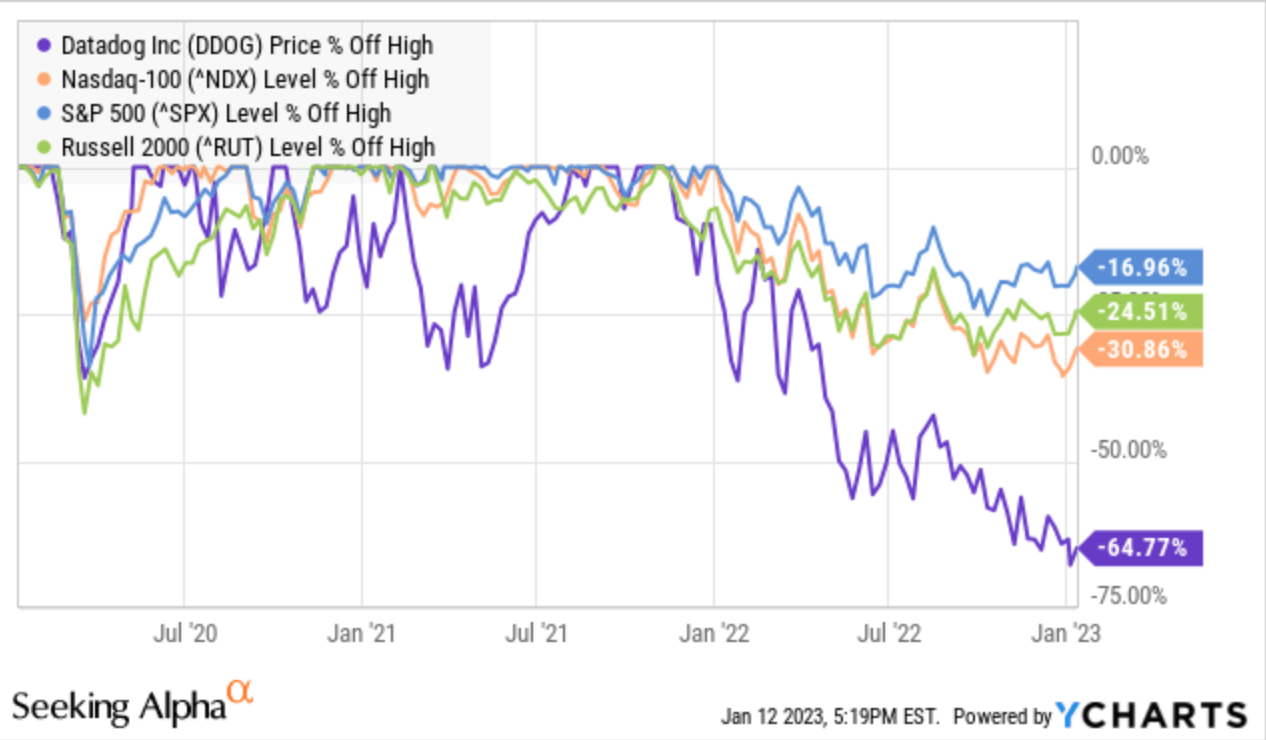

However, during the ongoing bear market, DDOG collapsed by around 65% from its all-time high. Consequently, DDOG has now underperformed all the major indices, such as the S&P 500, Nasdaq as well as the Russell 2000 (see chart).

Price % off high – DDOG vs indices (YCharts)

So, what reasons, besides the collapse in the stock price, speak for putting the stock on top of you watchlist? Moreover, is the stock cheap enough for an investment?

2. Valuation

In terms of valuation, I have chosen two valuation models:

- the enterprise value-to-sales ratio (EV/S), which adds debt and preferred shares to the market cap and subtracts cash as well as

- the rule of 40 by using the revenue growth rate and EBITDA margin.

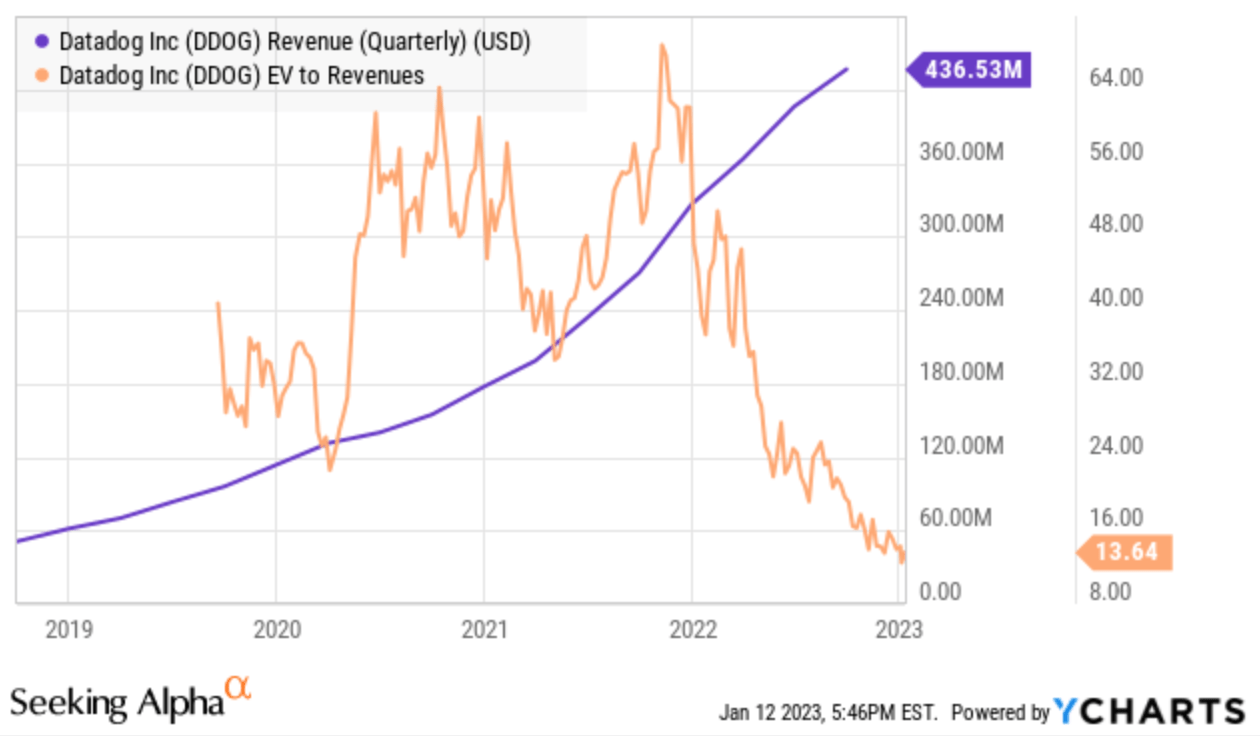

With regard to the EV/S ratio and the quarterly sales trend, it is striking that the EV/S ratio has logically fallen sharply from around 64 to currently 13.64, on a level never seen since the company’s IPO as a result of the slump in the share price. Nevertheless, sales are growing sequentially on a quarterly basis.

The lowest EV/S ratio was around 24 in 2020 as a result of the COVID selloff at the stock market. Nevertheless, the stock recovered quickly and reached an EV/S ratio of 64 as a beneficiary of the work-from-home policy as well as the ultra loose monetary policy of the Fed.

DDOG EV/S ratios and quarterly revenues (YCharts)

Consequently, the current EV/S ratio of 13.64 seems to be quite tempting despite the Fed’s current hawkish monetary policy although one could argue that a EV/S ratio is still high taking into consideration other SaaS companies (see following chart).

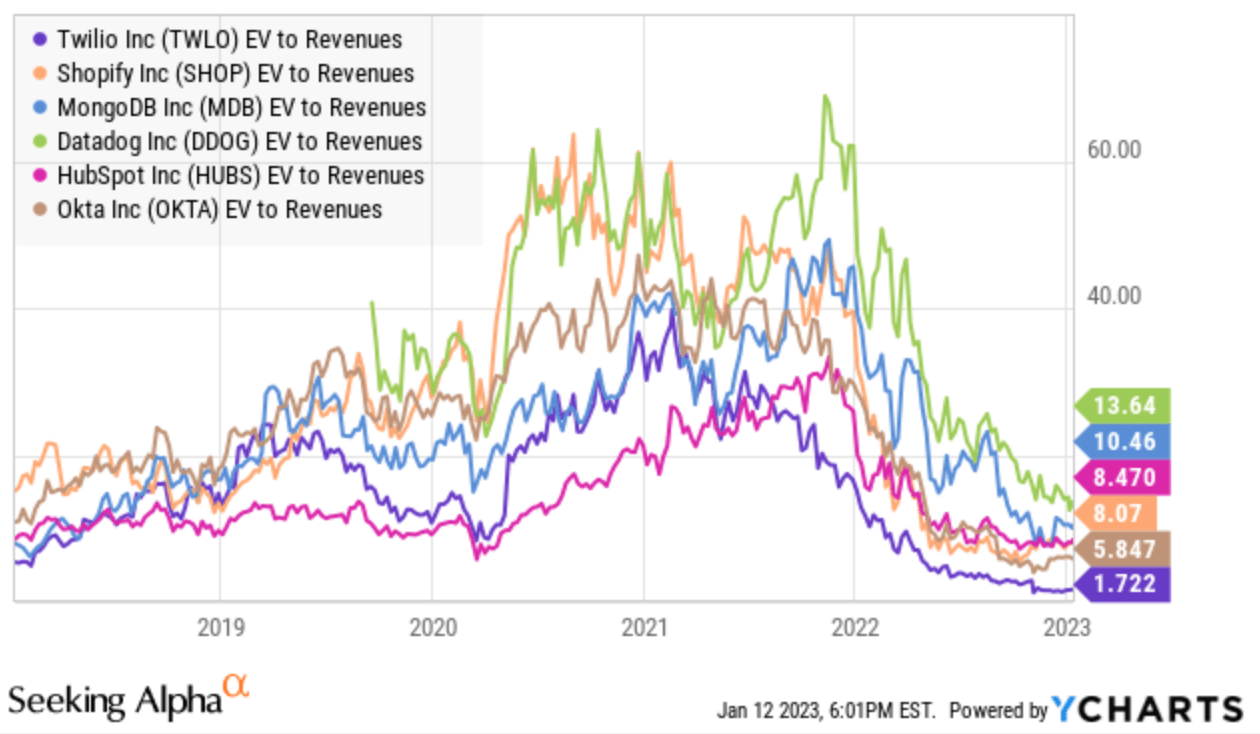

EV/S ratio – DDOG vs peer group (YCharts)

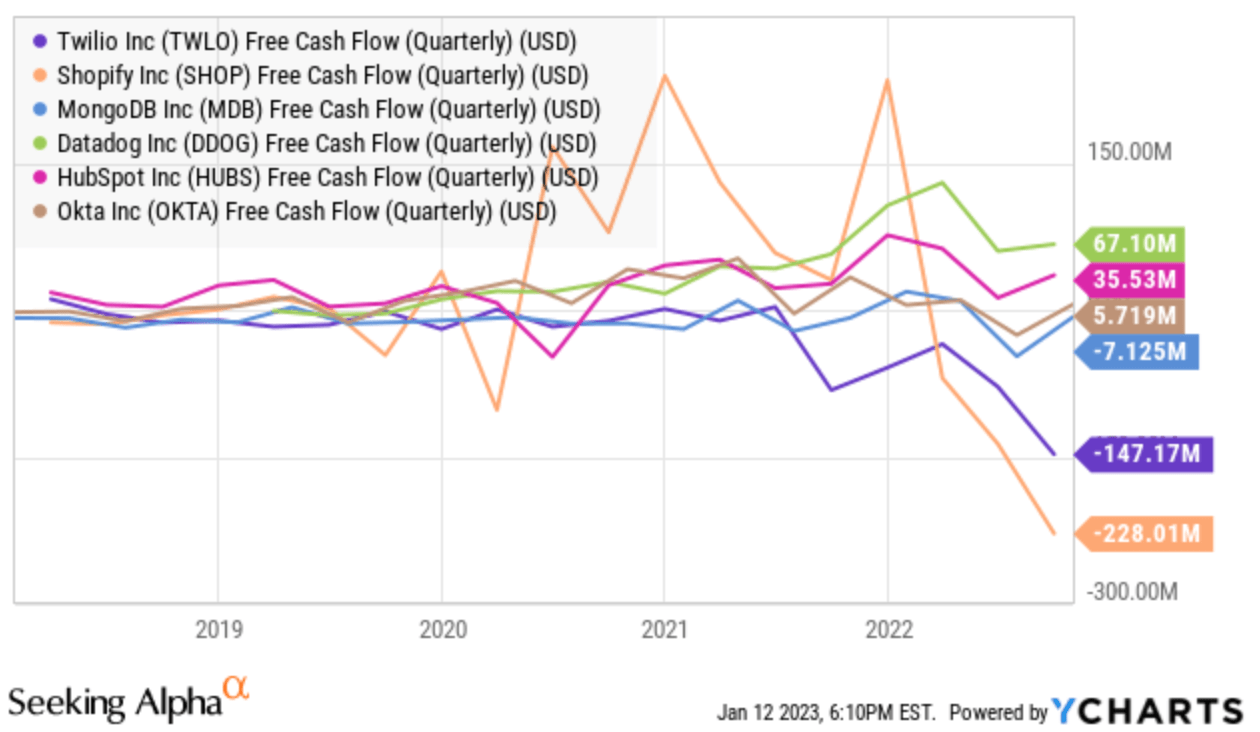

The reason for DDOG’s relatively higher valuation becomes clearer by taking into consideration the Free Cash Flow (FCF) as well as the Operating Income. DDOG, as one of a few exceptions among growth stocks, has a track record of sustainable positive FCF (see Chart).

Free Cash Flow – DDOG vs peer group (YCharts)

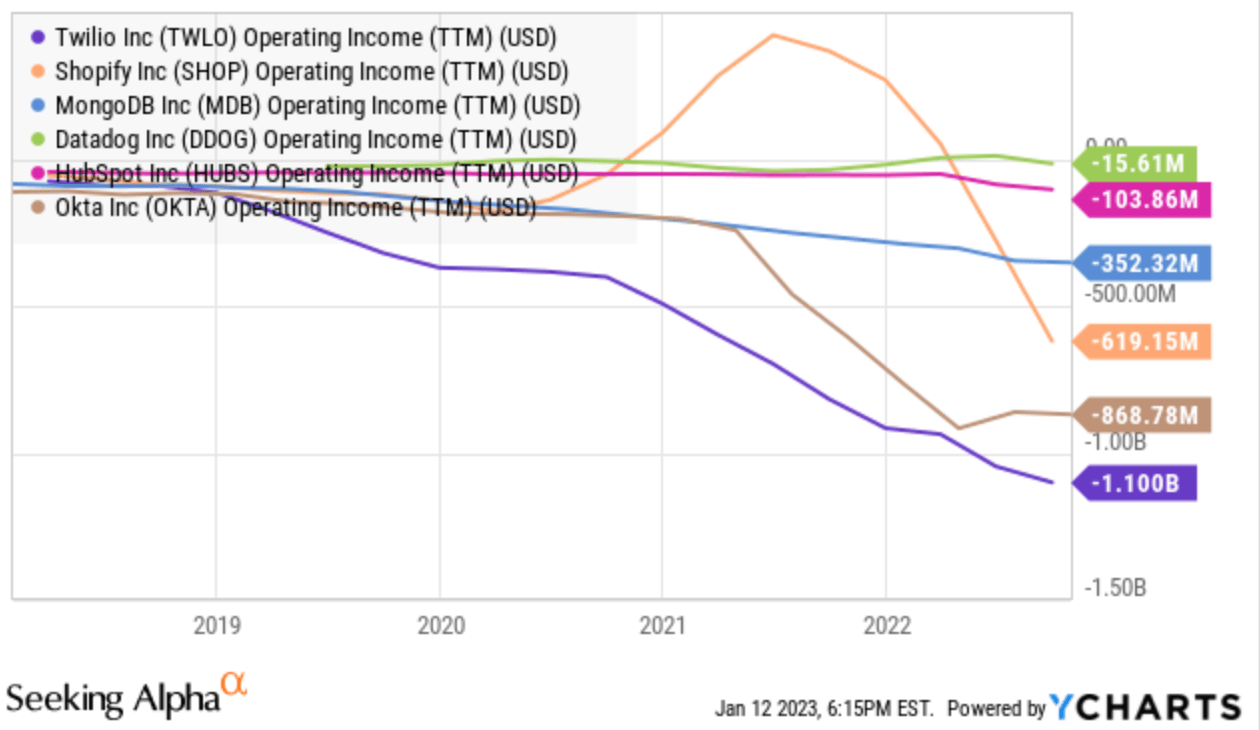

Additionally, DDOG has much lower losses from operations compared to its peers (see Chart).

Operating Income – DDOG vs peer group (YCharts)

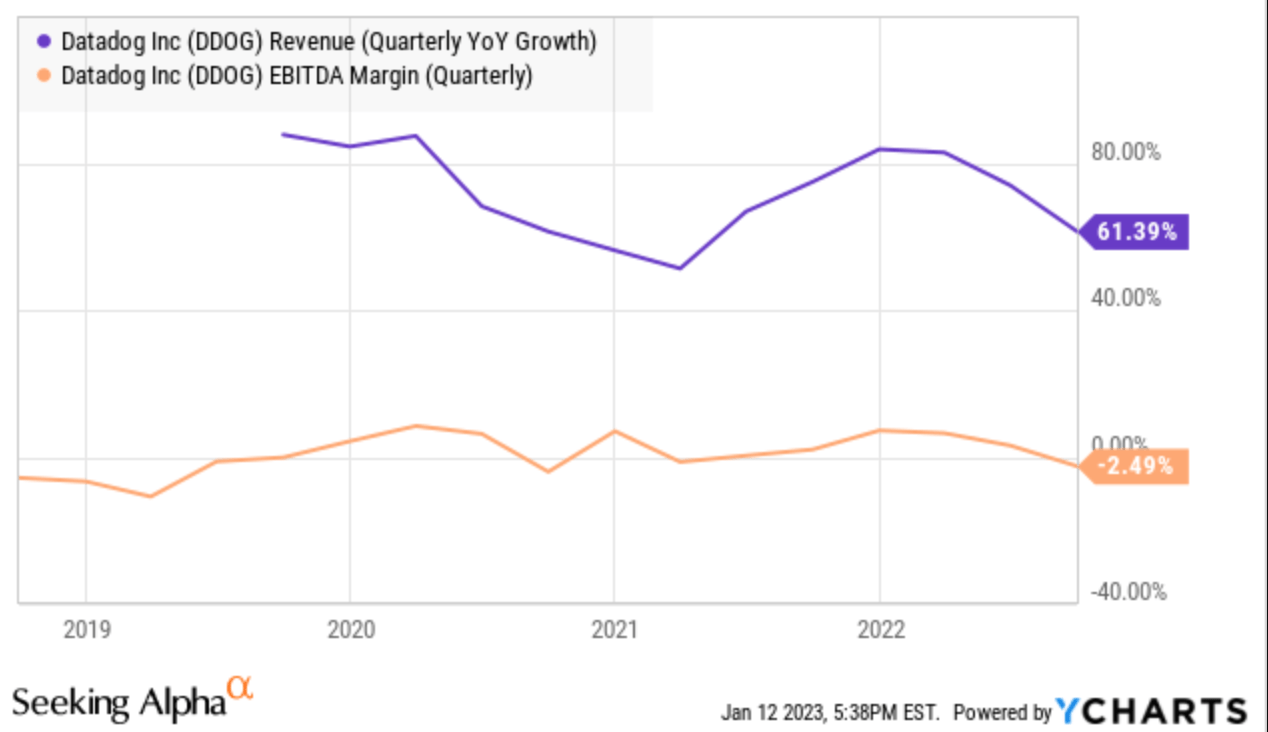

With regard to the rule of 40 and a revenue growth rate of over 60% in the most recent quarter, it can be stated that the ratio of 58.9 (61.39 minus 2.49) is very tempting to consider an investment at the current stage. According to the rule of 40, a promising investment should have a ratio of 40 or more.

Rule of 40 – DDOG’s quarterly revenue growth rates and EBIDTA margin (YCharts)

3. Technical Analysis

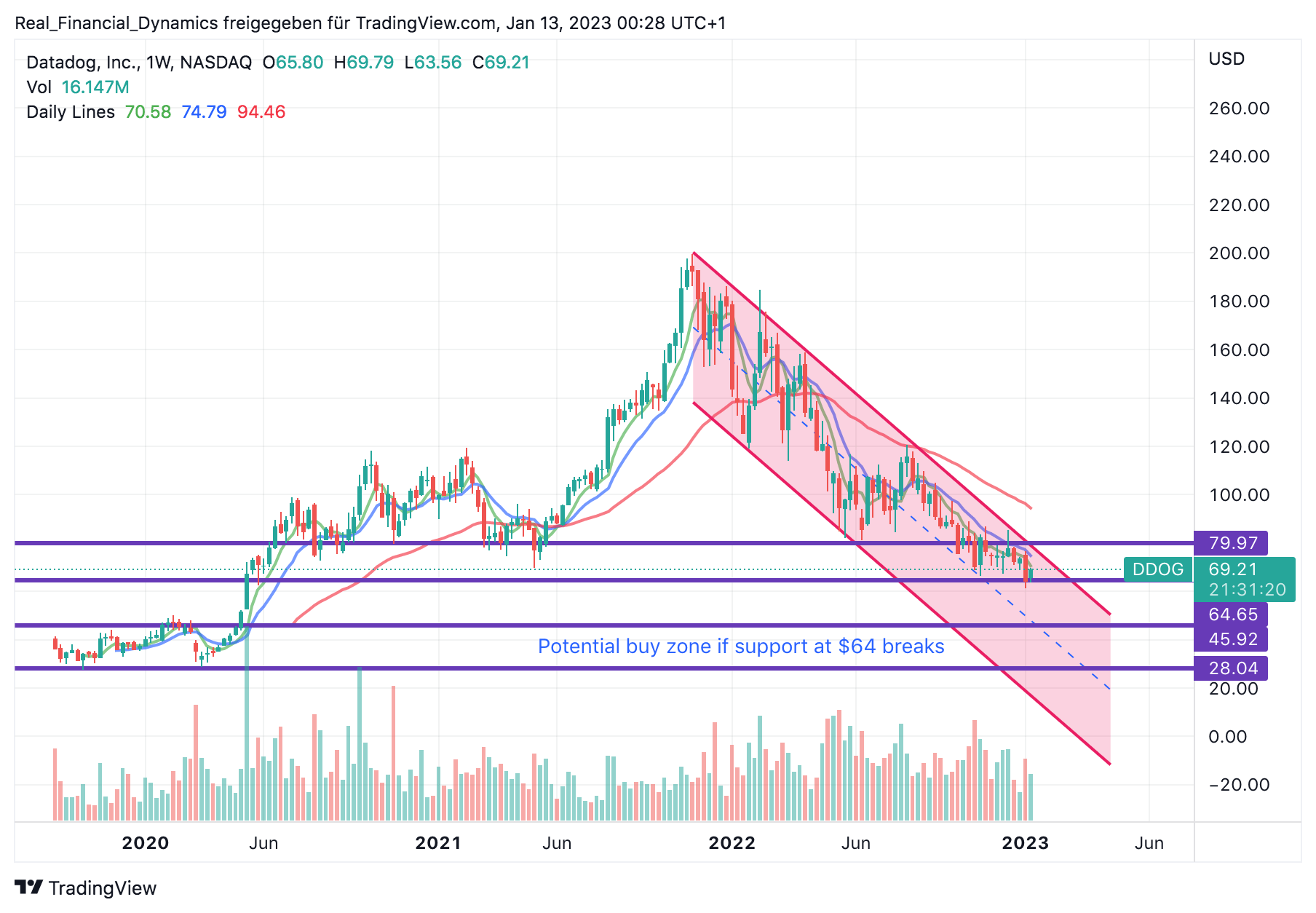

Taking into account the technical analysis, it is noticeable that the stock is caught in a downtrend, despite a couple of rebounds and breakout attempts, similar to a number of previous high-flying growth stocks (see Chart).

Based on my analysis, the stock is currently sitting close to a support level of around $64, which could break downwards if there is no improvement in the market conditions, such as inflation or the Fed’s monetary policy.

On the other hand, the stock could also make a breakout attempt to around $80 depending on the market conditions.

Overall, the trend still tends downward, signaling more selling than buying pressure.

DDOG stuck in a downtrend (TradingView)

4. Conclusion

DDOG is a hyper growth stock, which delivered triple digit returns to its investors since its IPO in 2019. Additionally, the company was still able to provide revenue growth beyond 60% in the most recent quarter.

While the EV/S ratio of 13.64 seems to be still high compared to SaaS companies, DDOG’s higher valuation is justified since the company provides positive free cash flows and only slight operating losses.

Moreover, considering the rule of 40, the company has a ratio of 58.9, which demonstrates a high quality growth stock with very promising fundamentals.

On the other hand and by taking into consideration the technical analysis, it becomes clear that DDOG is still caught in a downtrend, which tends for further share price declines in the near future unless there is a short term improvement from the inflation or monetary policy side (which seems to be unlikely at the current stage).

Overall, I would give DDOG a neutral rating. At the same time, I could imagine that investors will get more attractive prices in the near future so it would not be the worst advice to keep the powder dry for the time being. However, as soon as the tide turns and the Fed loosens its monetary policy, DDOG could be one of the growth stocks delivering once again triple digit returns.

Be the first to comment