sankai

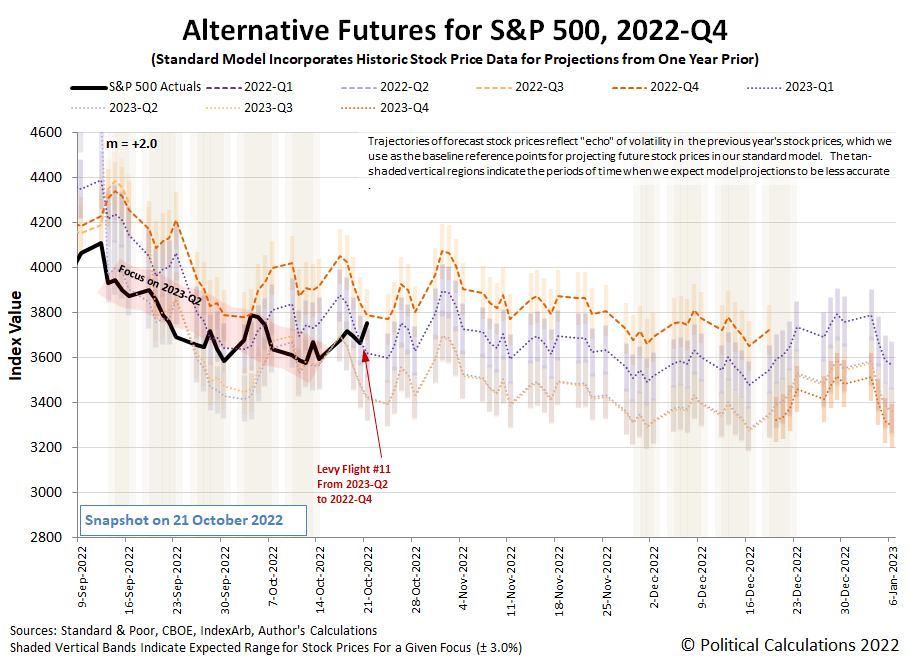

The S&P 500 (Index: SPX) underwent its eleventh Lévy flight event of 2022, jumping to close out the third week of October 2022 at 3,752.75, up 159.99 points (+4.4%) from the previous week’s close.

That’s an exciting development, because while previous swings in recent weeks have come close, they weren’t quite large enough to qualify as a full Lévy flight event where investors shift their forward-looking focus from one point of time in the future to another. For this latest event, it appears investors shifted their attention from 2023-Q3 inward to the nearer term future of the current quarter of 2022-Q4.

That change coincides with signals members of the Federal Reserve sent, mainly on Friday, 21 October 2022, that they were looking to reduce the size of their expected rate hike in December 2022.

Previously, investors were anticipating another three-quarter point rate hike in December, but were focusing on 2022-Q2 because that period coincided with when they expected the Fed’s current series of rate hikes would peak.

We don’t know how long investors might hold their attention on 2022-Q4. If investors become more concerned about the timing of when the Fed’s rate hikes will top out, it would make sense for them to shift their focus to the next future quarter of 2023-Q1.

The alternative futures chart indicates the Lévy flight that would coincide with such a change would be a low energy event. Stock prices could simply move mostly sideways to achieve that result. Meanwhile, if investors shift their term horizon back to 2023-Q2, the S&P 500 would see a noteworthy decline.

The only thing we know for sure is that investors will shift their investment horizon away from the current quarter at some point, and will absolutely do so by the end of the third Friday in December 2022.

When that happens will be subject to the random onset of new information. Speaking of which, here are the market-moving headlines we noted during the week that was.

Monday, 17 October 2022

- Signs and portents for the U.S. economy:

- China economy rebounding from summer zero-COVID lockdowns:

- Bigger trouble, stimulus developing in China:

- Bigger trouble developing in Japan:

- Wall Street ends sharply higher, dollar dips on UK U-turn, strong earnings

Tuesday, 18 October 2022

- Signs and portents for the U.S. economy:

- Some Fed members wanted bigger rate hikes this past summer; others growing concerned about U.S. labor market:

- Central bank rate-hike-o-mania:

- BOJ

- Goldman, Lockheed results buoy Wall Street

Wednesday, 19 October 2022

- Signs and portents for the U.S. economy:

- Fed members starting to be concerned about potential for bad effects from bigger rate hikes:

- BOJ more okay with falling yen than stopping never-ending stimulus:

- ECB thinking about another big rate hike:

- Wall St ends red, Treasury yields climb on dour guidance and looming recession fears

Thursday, 20 October 2022

- Signs and portents for the U.S. economy:

- Fed members want more rate hikes, worry about lockdown learning loss, and start thinking about keeping a lower profile:

- Bigger trouble developing in Canada, India, Germany:

- BOJ, JapanGov working to keep value of yen from collapsing and never-ending stimulus alive:

- Wall Street ends lower as Fed worries outweigh earnings

Friday, 21 October 2022

- Fed members start signaling they want to slow down rate hikes:

- BOJ in hot seat as bigger trouble developing in Japan:

- Wall Street ends higher as hopes for less aggressive Fed grow

The CME Group’s FedWatch Tool continues to project a three-quarter point rate hike when the FOMC next meets on 2 November 2022, but pulled back to project just a half point rate hike on 14 December (2022-Q4) following Friday’s signals from the Fed.

In 2023, the FedWatch tool now projects just a single half point rate hike in February (2023-Q1), setting the top for the Federal Funds Rate’s target range at 4.75-5.00% and holding at that level for much of the rest of the year. Looking further forward, the FedWatch tool anticipates a quarter point rate cut in December (2023-Q4).

The Atlanta Fed’s GDPNow tool‘s projection for real GDP growth in the recently ended calendar quarter of 2022-Q3 is +2.9%. The Bureau of Economic Analysis will provide its first official estimate of real GDP growth in 2022-Q3 on 27 October 2022, so the GDPNow tool should soon start forecasting real GDP for 2022-Q4.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment