sankai

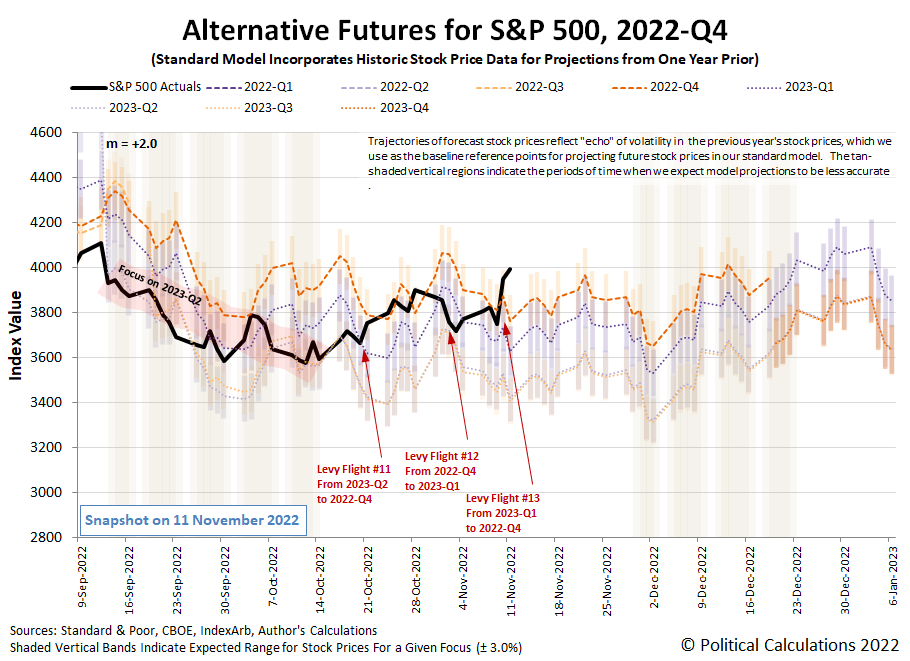

In an especially volatile year, the S&P 500 (SPX) continues to provide excitement! The index closed the trading week at 3,992.93, ending Friday, 11 November 2022 up 222.38 points (+5.9%) from the close of the previous trading week.

Getting there involved the thirteenth Lévy flight event of 2022 by our rough count, prompted by a better-than-expected Consumer Price Inflation report, and fueled by what ZeroHedge described as the “biggest short-squeeze on record, based on Goldman’s ‘Most Shorted’ basket”.

For the dividend futures-based model‘s alternative futures chart, we see the new Lévy flight event as a shift in the forward-looking time horizon for investors from 2023-Q1 back toward the current quarter of 2022-Q4.

That shift occurred because with inflation being reported lower than expected, the message the Federal Reserve’s interest rate-setting Federal Open Market Committee will send at its upcoming 13-14 December 2022 meetings will carry special weight for what investors should expect going into 2023.

Going back to the alternative futures chart, we see the level of the S&P 500 is elevated with respect to the trajectory for investors focusing their attention on 2022-Q4. It’s running at the high end of the range the model projects over the next several weeks, which may be the result of noise from the short-squeeze rally.

Given that investors are focusing on 2022-Q4, we need to point out there will be at least one more Lévy flight event before the end of 2022. If that happens during the next several weeks, that means stock prices would fall by a significant percentage. There’s also the wild card factor of the additional noise that has been injected into the market from the short squeeze event. Noise always dissipates, it’s only ever a question of when. In this case, that dissipation will also mean falling stock prices.

Here’s a recap of the week’s market-moving headlines:

Monday, 7 November 2022

- Signs and portents for the U.S. economy:

- Fed minions say they’re strangling economy even harder than data says:

- Bigger stimulus developing in China:

- Bigger trouble developing everywhere:

- Germany told to pay for Eurozone energy crisis:

- Central bank minions stuck on rate hikes:

- ECB minions thought about it, can’t stop, won’t stop rate hikes as they prep for Eurozone recession:

- U.S. stocks end higher, Meta jumps as investors eye midterms

Tuesday, 8 November 2022

- Signs and portents for the U.S. economy:

- BOJ minions briefly consider ending never-ending stimulus, JapanGov minions okay more fiscal stimulus:

- ECB minions excited about hiking rates, embrace their “dark side” as they deal with developing cracks in financial system:

- Wall Street ends higher as investors eye U.S. midterms

Wednesday, 9 November 2022

- Signs and portents for the U.S. economy:

- Fed minions admitting rate hikes will cause recession, markets betting Federal Funds Rate will top out at 5%:

- Bigger trouble developing in China:

- ECB minions say higher inflation is still coming to Eurozone despite their rate hikes:

- Wall Street drops after midterm election, CPI in focus

Thursday, 10 November 2022

- Signs and portents for the U.S. economy:

- Fed seen slowing rate hike pace as inflation eases

- Bigger trouble developing in China:

- Central banks thinking they should start backing off rate hikes:

- BOJ minions thinking about ending never-ending stimulus:

- ECB minions want more rate hikes, starting to worry about Eurozone bank’s potentially failing:

- Wall Street soars on sign of cooling inflation

Friday, 11 November 2022

- Signs and portents for the U.S. economy:

- Fed minion says more rake hikes coming despite worry about overtightening sending economy into recession:

- Bigger trouble developing in the Eurozone:

- Bigger trouble developing in China:

- BOJ, JapanGov minions thinking about ending never-ending stimulus in face of inflation:

- ECB minions thinking next rate hike may be smaller, Eurozone inflation may be higher:

- Nasdaq, S&P 500 end sharply higher, fueled by inflation optimism

With the lower-than-expected Consumer Price Inflation report, the CME Group’s FedWatch Tool still has a half-point rate hike on tap for 14 December (2022-Q4). But in 2023, the FedWatch tool now projects two quarter-point rate hikes, in February and March (2023-Q1), with the Federal Funds Rate reaching a peak target range of 4.75-5.00%. Looking further forward, the FedWatch tool anticipates two quarter point rate cuts in 2023-Q4 (November and December) as developing recessionary conditions take hold in the U.S. economy.

Meanwhile, the Atlanta Fed’s GDPNow tool‘s projection for real GDP growth in 2022-Q4 rose to +4.0% from last week’s +3.6% estimate. There continues to be a big gap between its current projection and the so-called “Blue Chip consensus” that anticipates near-zero growth in 2022-Q4.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment