onurdongel

With the aim of providing memorable products, Solo Brands (NYSE:DTC) operates premium authentic lifestyle brands. Due to its high-quality products, the company has enjoyed customer loyalty over the years. In the last year, the company has entered into three acquisitions, Our Kayak, Surf Ventures, and Chubbies, which are expected to strengthen the existing business model.

The company is operated by a visionary founder, who founded its core business, Solo Stove, in 2011 to bring the family together outdoors. With time, due to its profitable operations, the company has expanded its footprints in various segments.

Currently, Solo brand markets its products through its rapidly growing DTC platform and has been focused on delivering innovative and high-performance products to reach a broad community of customers.

Solo brands manufacture durable and easy-to-use products such as Signature 360º Airflow Design™ and OruPlast™, which give customers a memorable experience and drive customer loyalty.

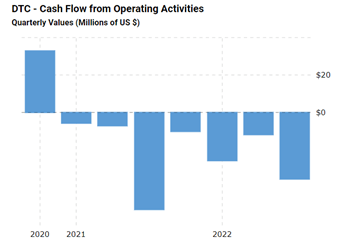

Cash flow from operations (macrotrends.net )

Although the company seems to be growing, cash flow from operations is still negative, which may bring substantial concerns about the business model. Despite posting profits, last year’s cash flow had been negative; As the company has been engaged in an expensive acquisition, it might require to depend on external sources to fund its loss-making internal operations and acquisitions; which might lead to deteriorating investment returns.

I believe it is better to wait until the company turns profitable and successfully expands its other segment; holding the stock at such a point where the company has been making huge losses can bring substantial risk. My current view on the stock is bearish.

Historical performance

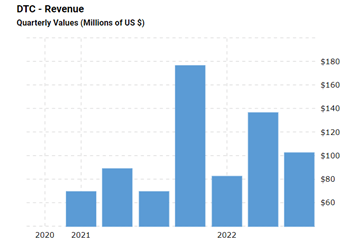

Since its IPO in 2021, the company’s sales have increased significantly, primarily attributed to increased marketing initiatives, hype in outdoor product sales, and partially due to the acquisitions. As a result of rapidly rising demand, the company became profitable after last year’s loss. In the last year, the company has seen revenue increase from $133 million in 2020 to about $403 million by 2021, resulting in a net profit of over $10 million (offset by net income attributed to controlling members prior to the reorganization transaction). But despite profitable operations, the cash flow turned significantly negative due to increased inventory levels.

Quarterly revenue (macrotrend.net )

Over the last few quarters, revenue seems to be increasing (fluctuations are partially attributed to seasonality), but such revenue growth is attributed to higher marketing spending, which is exerting significant pressure on the company’s margins; therefore, it is better to wait until the business performance turns positive.

Strength in the business model

Management’s aim to keep everything simple, sustainable, and easy has played a bigger role in the company’s success. Although the company has expanded into various segments, it has managed its product quality. Such a successful expansion might be attributed to a data-driven product development process and an innovative approach different from its competitors.

The company has been focused on bringing innovative products as per the customer requirements and needs; such a customer-centric approach might drive significant revenue in the upcoming years. Also, recently developed research and development facilities can help understand customers’ needs better, which can further strengthen the business model.

It seems that management has carefully focused on every segment of the business, from marketing initiatives to product development, showing that the management is owner-oriented and working hard to strengthen its competitive advantage.

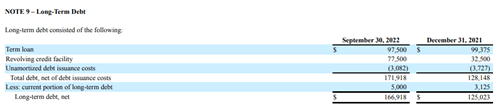

Debt (quarterly report )

It is appreciated that debt levels are moderate, which reduces the risk. Still, investors must consider that if management couldn’t turn business operations profitable, the company will have to depend on external sources such as debt and equity offering to fund its operation, which can put significant pressure on the company’s financial position.

Risk Factors

Although over time, the company has expanded through various segments, over 90% of the total revenue comes from Solo Stove; such a high concentration of sales might bring a substantial risk of competition; if the competition came up with many innovative products, the revenue might see a significant drop.

Also, the rapid growth in the last year can cause a demand surge in recreational and outdoor products; Therefore, such growth may not sustain for a longer time.

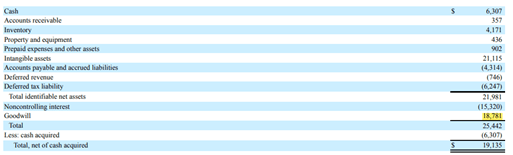

Kayak acquisition transaction (annual report )

The above mentioned picture reflects the transaction of Our Kayak acquisition; based on the significant goodwill generation, it seems that the management has entered into an expensive acquisition (when the industry was booming). Such a capital allocation decision might bring a substantial cost to the company resulting in subdued shareholder returns. Also, the company has paid such an expensive price in its other two acquisitions as well; any deterioration in the business performance of those acquired companies might bring considerable goodwill impairment charges.

Recent development

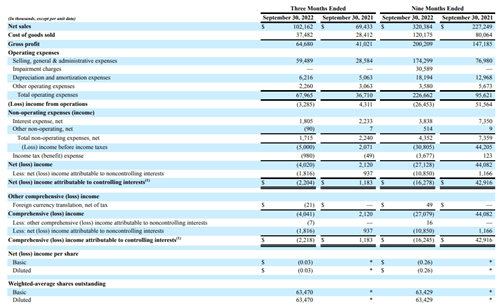

quarterly results (quarterly report )

In the recent quarter, revenue has increased substantially from $69 million in the same quarter last year to about $102 million now; but as a result of higher spending on marketing, the net profits turned negative. Also, due to increased inventory levels, the cash flow from operations became negative, and as a result, the company had to rely on debt to sustain its operations.

Inventory levels have increased significantly, reaching about $65 million, and the cash reserves have depleted; therefore, it seems that as the business has been losing money consistently, it will have to depend on external sourcing to sustain its operations which will eventually affect the business value.

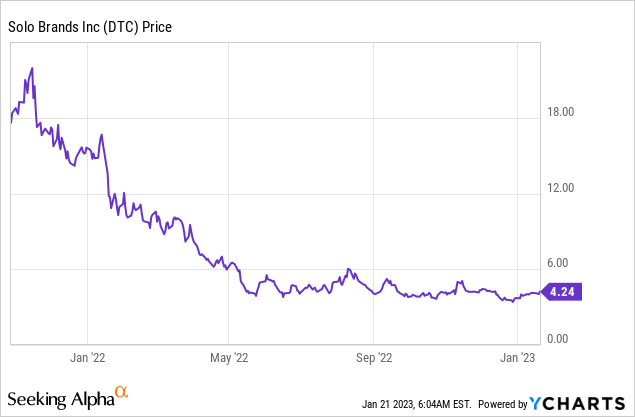

share price (YCharts )

Currently, the company has been trading for nearly $405 million. Since its IPO, the stock has lost over 76% of its value; after dropping from $18.36 per share in 2021, the stock has reached $4.24 per share now. I believe, due to its loss-making business operations, the company will have to take substantial debt, and as the market cap has contracted, the company will have to dilute its significant stake to raise capital.

Therefore, it is better to stay away from such a loss-making business which can bring substantial risk; I assign a sell rating to the stock.

Be the first to comment