Sundry Photography

SNOW Continues To Defy Gravity

Snowflake Inc. (NYSE:SNOW) stock has continued to defy gravity, as it outperformed the S&P 500 (SPX) (SP500) (SPY) since our previous update. The company went into its FQ3’23 earnings call and delivered what investors wanted to hear: improved margins.

Given the worsening macro headwinds, Snowflake’s consumption-based compute-heavy data cloud model certainly wasn’t immune. But, it still managed to deliver a quarterly net revenue retention (NRR) rate of 165% (down from Q2’s 171%).

Therefore, it demonstrated that the company’s traction in penetrating enterprise/large customers continues to be robust. Moreover, customers’ spending has also been solid, corroborating the strength of Snowflake’s data platform.

Snowflake: Gaining Traction With Enterprise Customers

Accordingly, Snowflake sees itself as a leader in its expanded CY26 or FY27 $248B cloud data platform TAM. Notably, the company estimates that its data warehouse/data lake/unistore segment accounts for $173B (about 70%) of its addressable market.

Also, the company sees the proliferation of Snowflake’s clout among general system integrators, as CFO Michael Scarpelli accentuated:

We spend a lot of time with [the GSIs] on certifying their people to be Snowflake certified. There [are] different certification levels. I will say, if you went back 3 years ago, we used to hear from customers, one of their biggest concerns was they didn’t have people who really understood Snowflake. Today, that’s not as big of an issue. You can see when we’re trying to sell into a Global 2000. And then you can see through their job postings they have people that are looking for Snowflake talent so kind of tells you we’re going to get those deals. But it’s getting better right now. We spend a lot of time training both customers, and more importantly, the GSIs. And they’re building up significant practices. (Barclays 2022 Global Technology, Media and Telecommunications Conference)

Hence, the company has continued to gain momentum with large enterprises as it looks to scale its platform toward its FY29 profitability target. Importantly, nearly 90% of its revenue is based on compute. Therefore, scalability is highly critical; thus, traction with large customers is vital.

As such, we are assured that it has continued to penetrate the Global 2000 customers (up 18% YoY), as Snowflake posted 94% YoY growth in customers with over $1M in product revenue. Therefore, the underlying growth momentum supports the strength seen in its NRR, as discussed earlier.

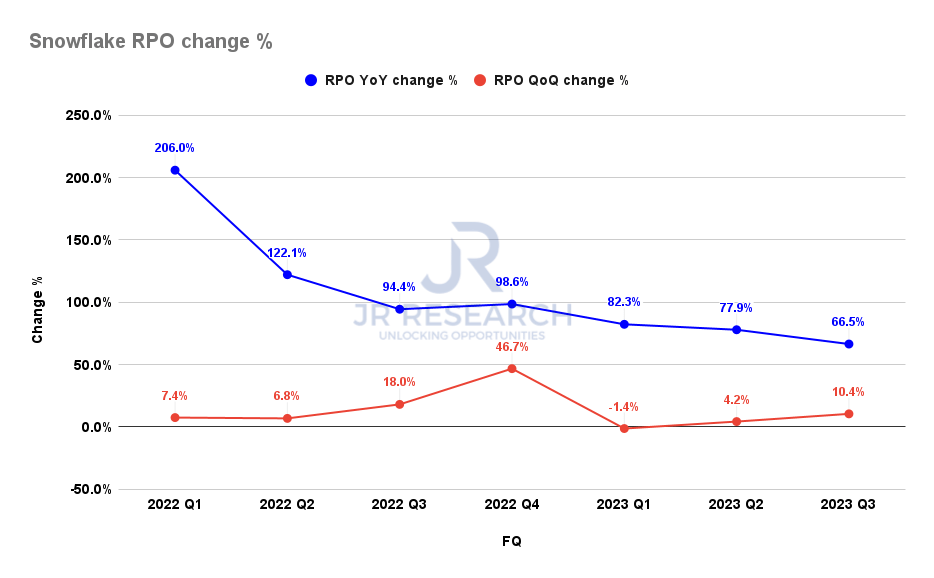

Snowflake RPO change % (Company filings)

Notably, Snowflake’s remaining purchase obligations (RPO) appeared to have bottomed out in FQ1, as the company posted a QoQ growth of 10.4%. It carried on the recovery seen in Q2’s 4.2% uptick.

Consequently, it indicated that Snowflake has been able to snag long-term contracts with its enterprise/large customers, despite the intensifying macro headwinds.

Notwithstanding, the company’s global growth drivers appeared to have stumbled as the US Dollar Index (DXY) gained significant strength in 2022.

While the DXY has fallen markedly from its September highs, we postulate that the Fed’s hawkish cadence through 2023 could likely keep the DXY at an elevated level. Hence, it could continue to impact its global growth momentum, as compute costs for its customers have risen, coupled with potentially reduced enterprise IT spending.

However, Snowflake investors need to consider whether the market remains supportive of forming a constructive consolidation at the current levels, even though we could be entering a potentially significant downturn.

Snowflake’s Stock-Based Compensation Not A Significant Concern

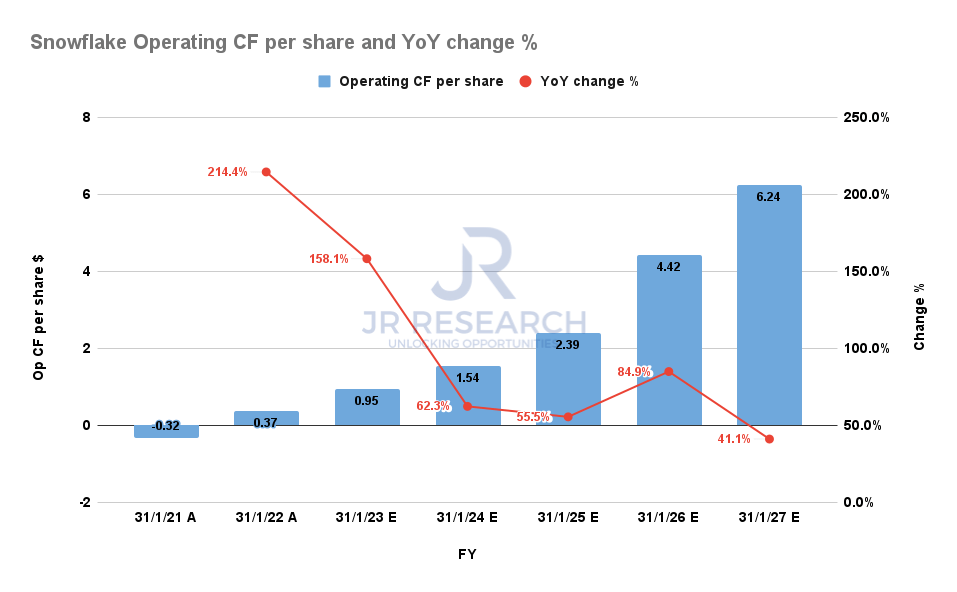

Snowflake Operating CF per share (S&P Cap IQ)

Some investors have highlighted their concerns on whether the company’s stock-based compensation policies have diluted its cash flow accretion.

It’s a valid concern. However, investors shouldn’t be unduly worried, as Snowflake has made it a priority to keep its dilution at “controlled” levels, as Scarpelli articulated:

We’ve been running at pretty low dilution given our growth. We’ve been running around 2%. I think this year, it’s going to probably be closer to 3%. But longer term, my goal is to keep it at 2%. (Barclays Conference)

Therefore, investors should assess the company’s forward operating cash flow accretion on a diluted share basis, which is still expected to expand rapidly through FY27.

Takeaway

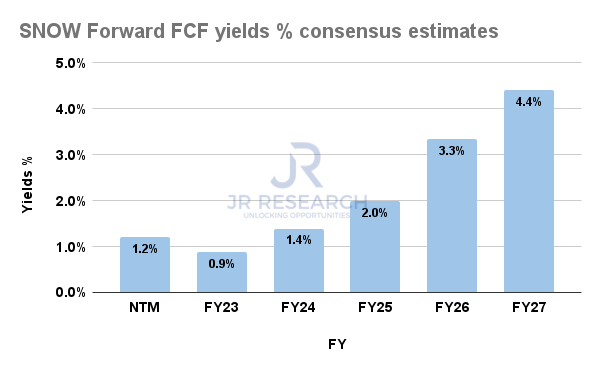

SNOW Forward FCF yields % consensus estimates (S&P Cap IQ)

SNOW is an expensive stock; make no mistake about it. While it’s free cash flow (FCF) profitable, it last traded at an NTM FCF yield of just 1.2%. Therefore, a significant growth premium is embedded in its valuation, even though SNOW is down nearly 60% YTD.

But, we believe investors considering SNOW at the current levels are buying into its future growth prospects. As seen above, SNOW last traded at an FY27 FCF yield of about 4.4%.

Therefore, the question is whether investors are confident enough that Snowflake can consistently deliver robust performances over the next five to six years, despite the macroeconomic uncertainties.

We think there’s little doubt that investors without a firm conviction or understanding of Snowflake’s data cloud model should abstain from adding exposure. Therefore, SNOW is a stock only for high-conviction investors at the current valuations.

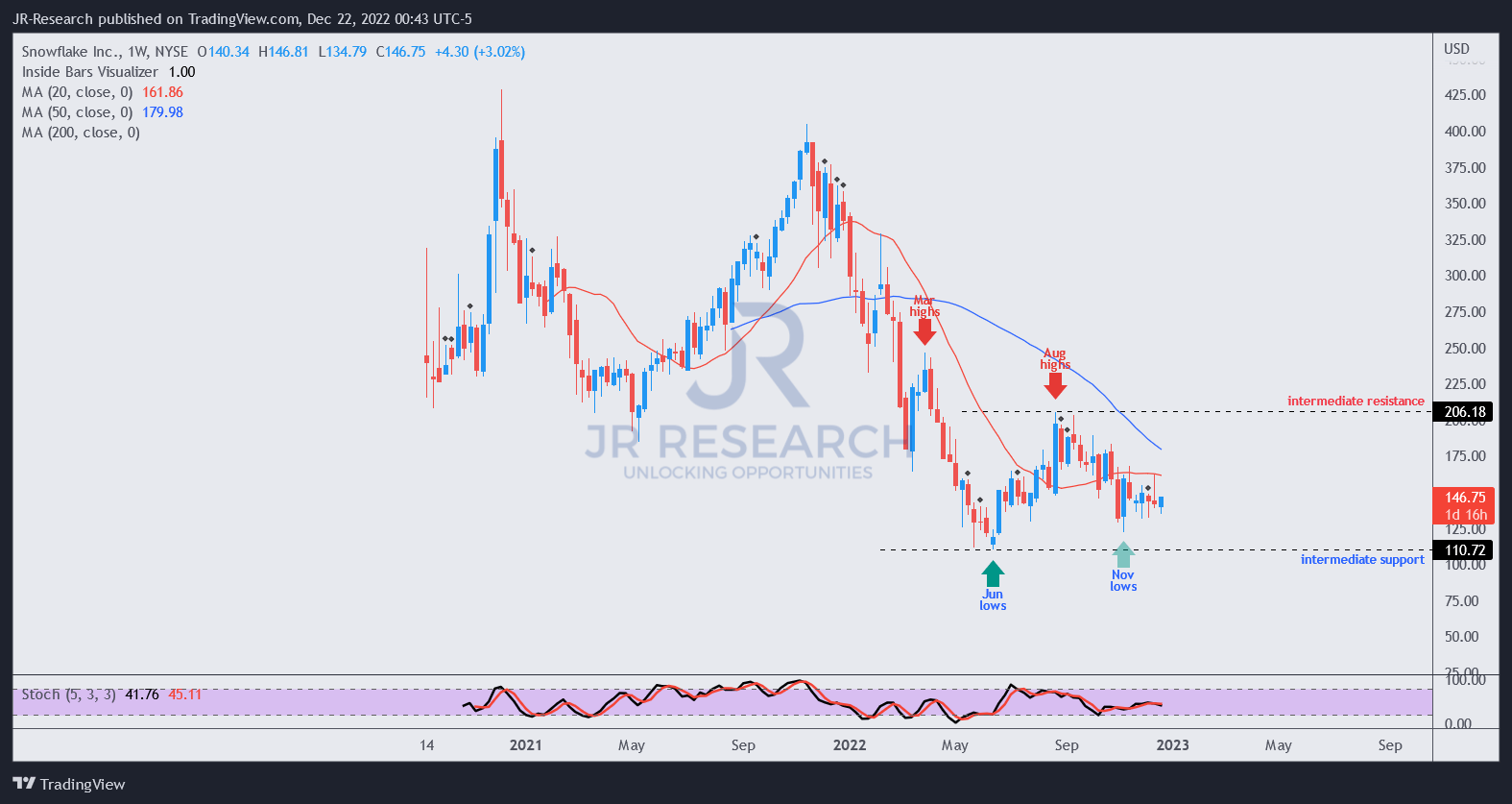

SNOW price chart (weekly) (TradingView)

However, we gleaned that SNOW appears to be bottoming out constructively, as it formed a higher low in November (against June’s lows). Also, its 20-week moving average (red line) seems to be flattening, suggesting consolidation.

However, it’s still too early to suggest that SNOW is ready to resume its medium-term uptrend. But, by the time you wait for the moving averages to align accordingly, SNOW is unlikely to be trading at the current levels.

Hence, we believe the current opportunity is constructive for investors waiting to add exposure to the leading data cloud company.

Revising from Hold to Buy, with a price target (PT) of $180, implying a potential upside of 40%.

Be the first to comment