iantfoto

Business and Industry Outlook

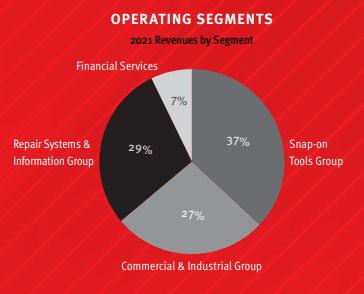

Snap-On Inc. (NYSE:SNA) is a leading provider of tools, equipment, and diagnostic software for professional users worldwide. The company has a long history of steady growth and profitability, and its high-quality products are highly regarded in the automotive, aviation, and industrial markets. Their product line breakdown is tools; diagnostics, information and management systems; and equipment. Revenue breakdown of operating segments is shown below.

SNA Operating Segments (SNA Investor Relations)

One of the things that separates SNA from competition is quality and brand name recognition. As an engineer in a manufacturing setting, I can back that Snap-On is highly regarded as the best hand tool, storage and diagnostics brand available. With that, however, is a running joke of how expensive their products are. As market downswings continue, manufacturers and consumers may opt for cheaper alternatives such as Stanley Black & Decker (SWK) or Harbor Freight. I think it’s important to reflect this situation in my valuation analysis where EBIT margins are reduced to 20% to compete for price. Another industry question that pops up is the need for hand tools as automation advances. I don’t think this will be the case as there will always be specialized equipment and tasks that can only be maintenance with a human and a tool. In fact, Hand Tool CAGR is around 4.3% through 2030 with diagnostics around 5%.

Financials

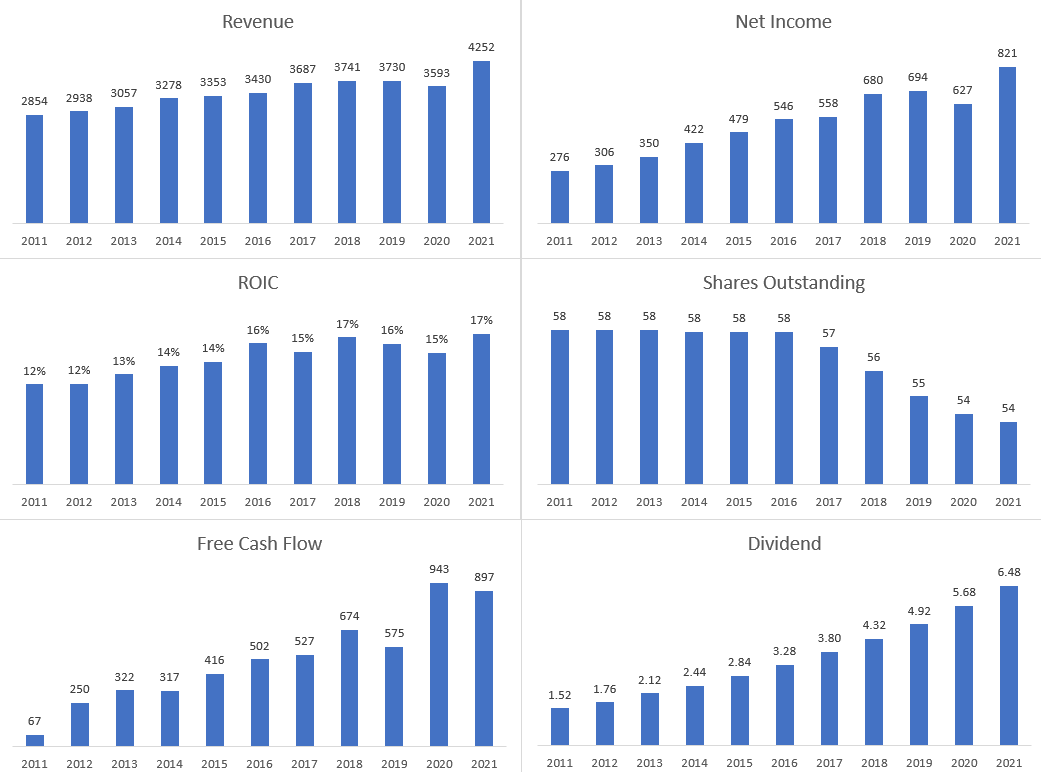

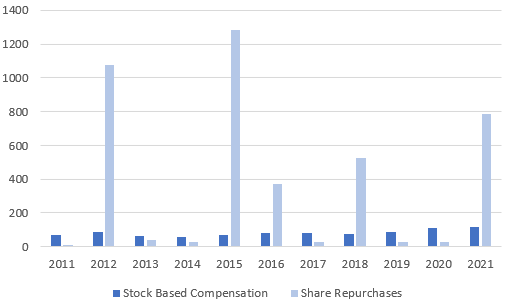

SNA has seven key things I look for when judging the performance of a company. They have top line revenue, net income, and free cash flow growth over the last ten years. They consistently repurchase shares, generating value for the shareholder, and have increased their dividend as well. They also boast a good ROIC average, which is higher than their calculated WACC. This tells me management is efficient at investing capital. Furthermore, their share repurchases generously outweigh any stock-based compensation.

SNA Financials (Author) Stock Based Compensation (Author)

Competition

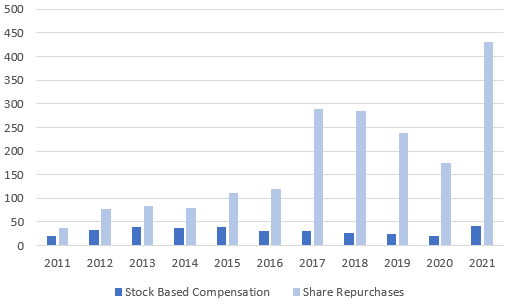

Comparing SNA’s financials to a very common competitor, SWK, reveals how strong SNA is.

SWK Financials (Author) SWK Stock Based Compensation (Author)

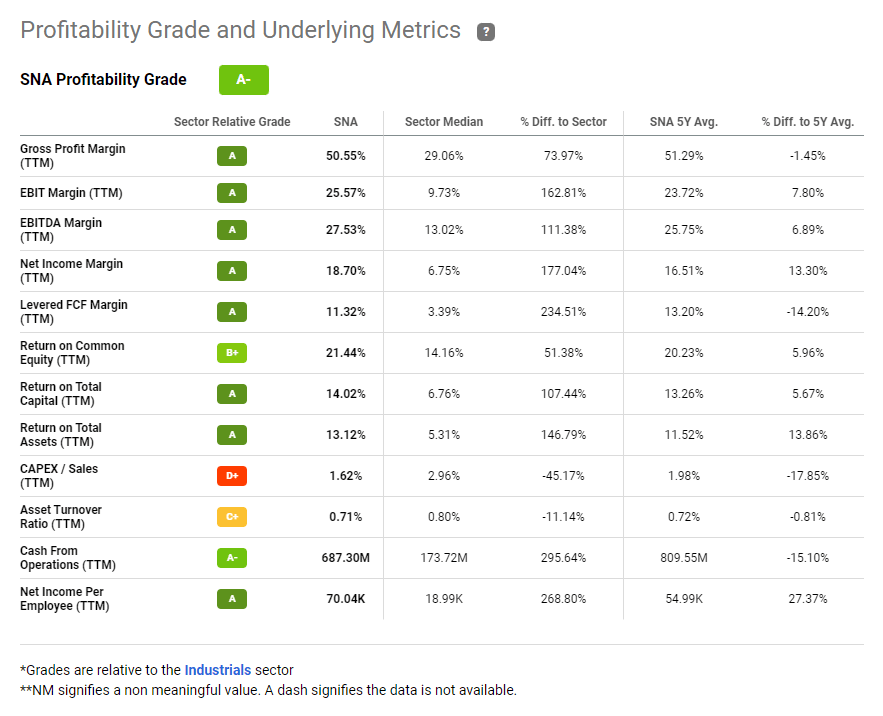

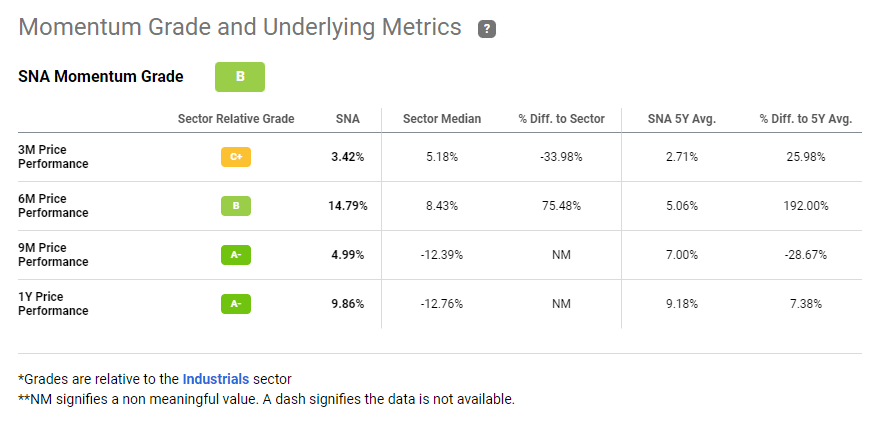

The similarities between the two companies show top line revenue, net income, and dividend growth. But that seems to be where the similarities end. When looking at ROIC, SWK boasts a mere 8% for a 5 year and 10-year average. With SWK’s WACC hovering 9%, its very hard to tell if their management is generating value. If we flip over to SNA, their ROIC is 14% and 16% for 5 year and 10-year averages. Not only is it significantly higher than SWK, but it is also growing, indicating management is becoming even better at generating value. Furthermore, SWK has really struggled with inventory issues leading to low free cash flow numbers since the pandemic, and issuing more shares, diluting the investor. Also, SWK’s share repurchases versus stock-based compensation is very dodgy during some years where they offered to compensate more to employees than the shareholder. SNA has never had these issues. We can also compare SNA to the industry and other peers and see that their profitability and momentum metrics are superior.

SNA Profitability (Author) SNA Momentum (Author)

Valuation

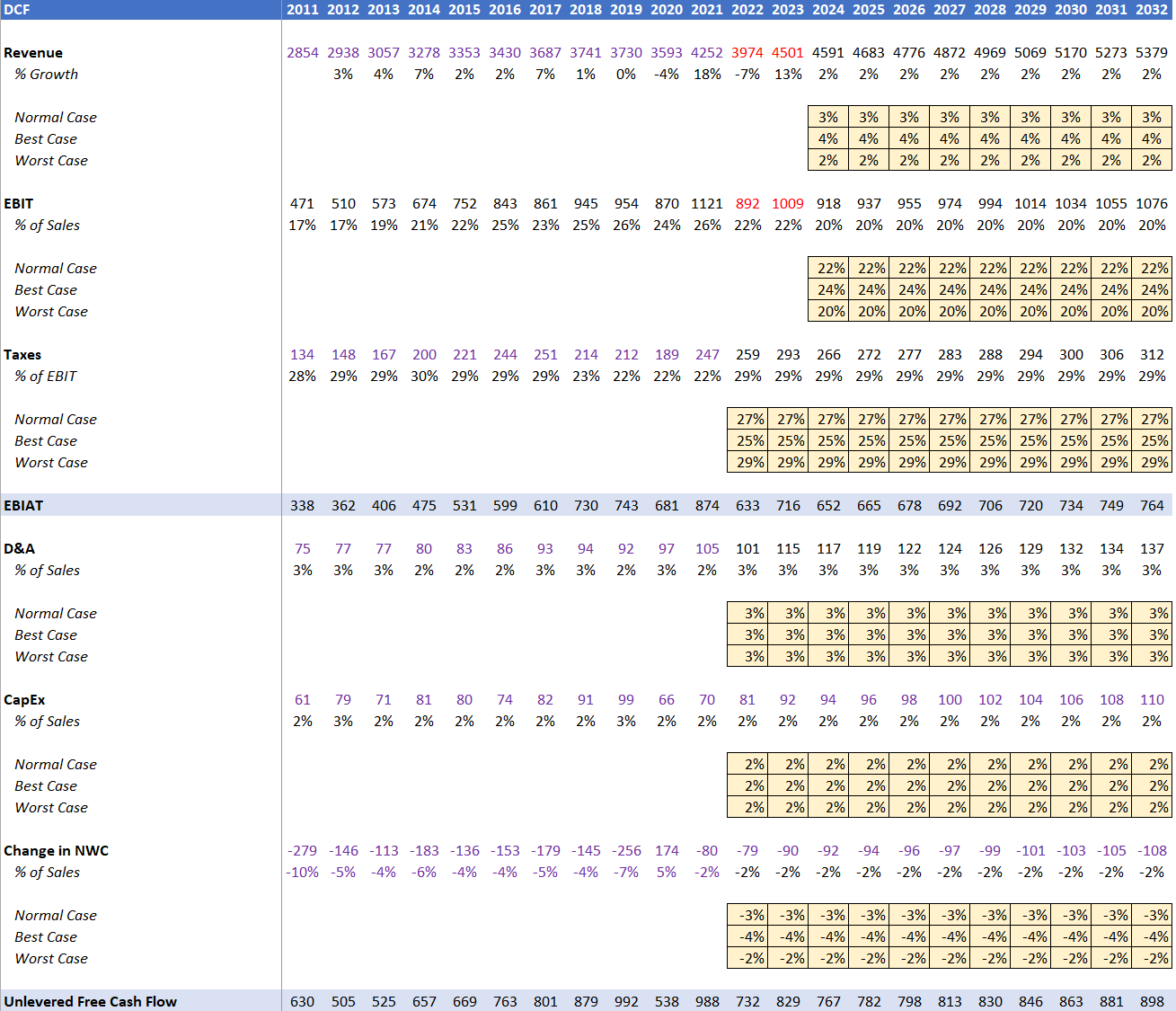

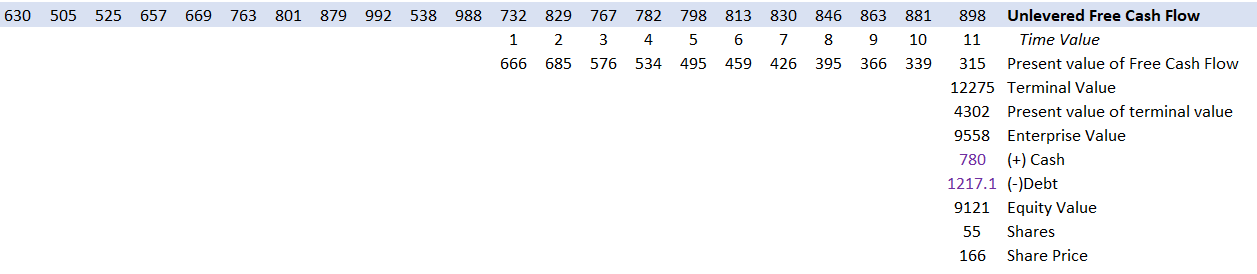

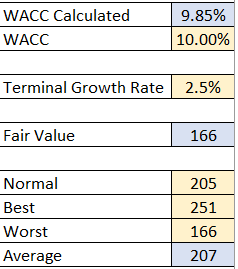

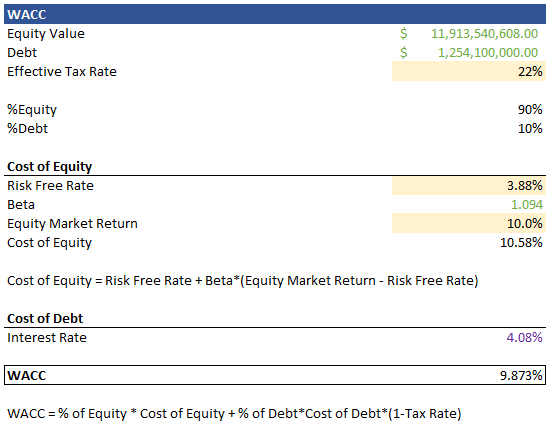

A fair value of $207 per share was calculated by a 10-year Unlevered Discounted Cash Flow (“DCF”) analysis using CAPM with a 2.5% terminal growth rate (“TGR”) and a 10% weighted average cost of capital (“WACC”) discount. Note that SNA’s WACC was actually calculated to be 9.85%, but I decided to discount by 10% to match the market. A worst-case, best-case, and normal-case scenario were averaged to arrive at the fair value. Revenue and EBIT projections were used from average results of (18) analysts for 2022 and (10) analysts for 2023 from Financial Modeling Prep (Red Text). Personal projections were used thereafter, with the following conservative assumptions in the tan boxes.

SNA Assumptions (Author) SNA Fair Value Calculation (Author) SNA Fair Value Calculation – 2 (Author) SNA WACC (Author)

Conclusion

Overall, Snap-On is a well-managed company that operates in stable and growing markets. Its strong brand, and solid financial performance make it an attractive investment for long-term growth. They look very compelling compared to competition however, at its current price, I would mark it as slightly overvalued. For these reasons, I see this as a company to hold forever, but new investors should wait for prices sub $210 to start making positions.

Be the first to comment