stockcam

Thesis

When the market hopes/ speculates that the worst for the advertising and social media industry is over, there comes Snap Inc. (NYSE:SNAP) with another warning, again. Snap reported Q4 2022 results more or less in line with expectations, but spooked investors with a warning that revenues for the first quarter in 2023 may fall by as much as 10% as compared to the same period in 2022. Needless to say, the market did not like it: Snap stock lost as much as 15% in after market trading.

With Snap being priced as a growth company, referencing an EV/Sales of close to x4 on negative earnings, I argue a 10% YoY contraction is unacceptable to support the growth thesis. Personally, I value Snap stock with a residual earnings model and calculate a fair implied share price of $8.34. In my opinion, Snap continues to be a ‘Hold’ at best.

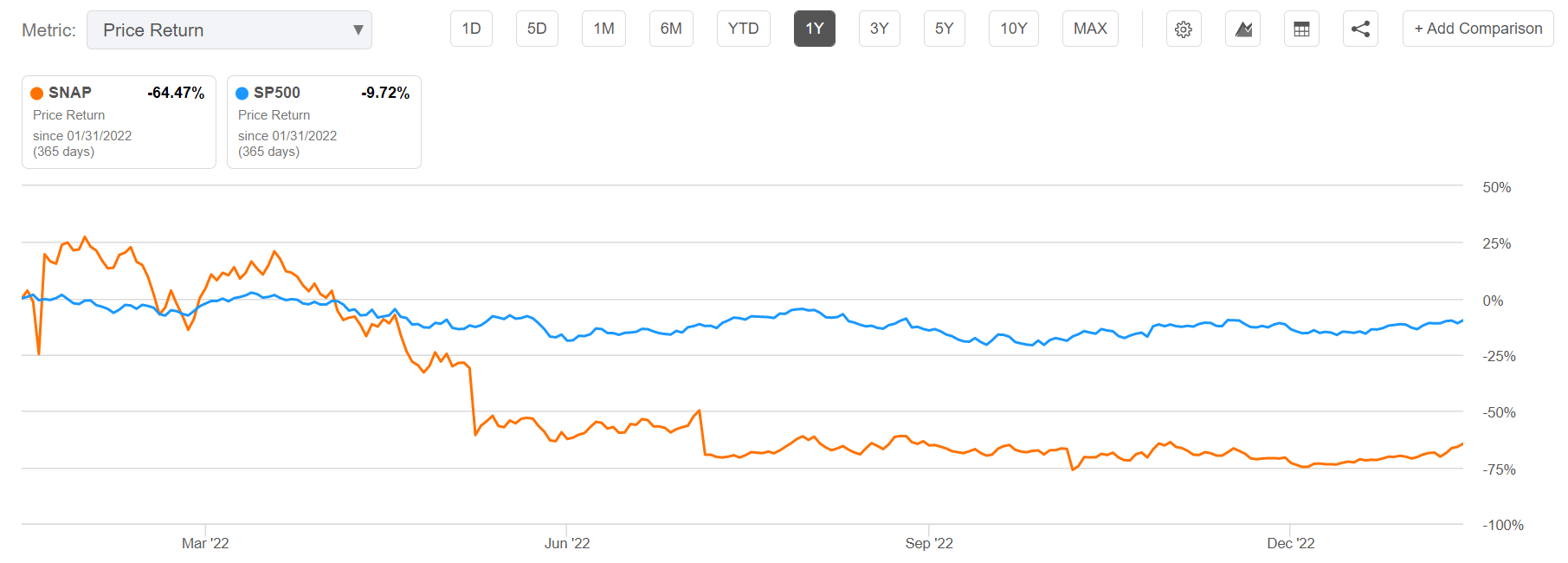

For reference, Snap stock continues to be a strong relative underperformer: shares are down approximately 64.4% for the past twelve months, as compared to a loss of about 10% for the S&P 500 (SPY).

Seeking Alpha

Snap’s Q4 2022 Quarter

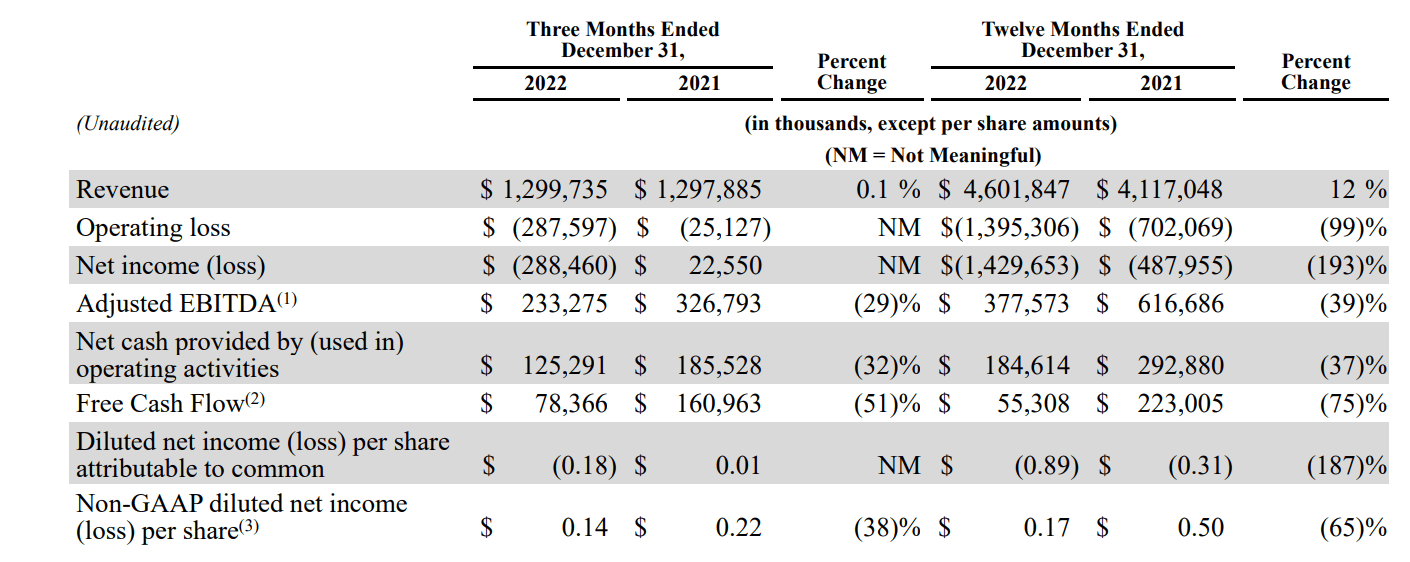

Snap reported Q4 2022 results approximately in line with analyst consensus expectations. During the period from September to end of December, the social media company generated total revenues of about $1.3 billion, as compared to $1.298 billion for the same period one year earlier (only a 0.1% year over year topline expansion). The operating loss widened significantly, about x10 to $288 million. In Q4 2021 the loss was only $25 million.

For the FY 2022 the picture is slightly better: The company’s topline increased by about 12% year over year to $4.6 billion of revenues. And the operating loss ‘only’ approximately tripled, to $1.4 billion.

Snap’s Q4 reporting

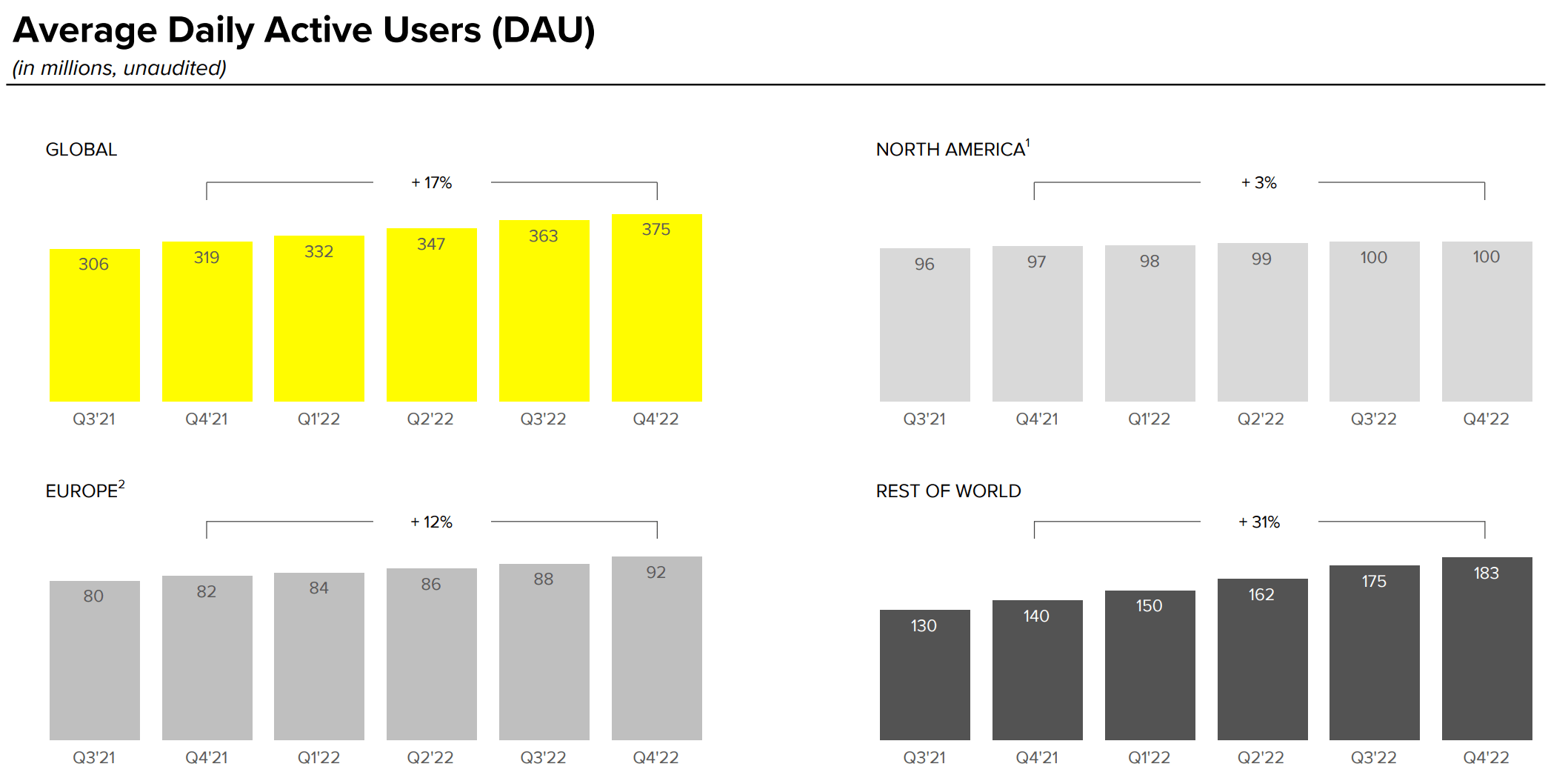

Snap’s daily active users (DAU) rose 17% YoY and about 3% QoQ to 375 million in Q4 2022, adding about 56 and 12 million new users respectively. Notably, YoY growth was observed across key regions, including North America, Europe, and the Rest of World. However, on a QoQ basis, it is quite evident that in North America Snap is getting close to market saturation.

The average revenue per user across regions was $3.47.

Snap’s Q4 reporting

A Warning That Challenges The Growth Thesis

In Q4 2022 Snap failed to surprise to the upside, but at least the social media company reported a very slight 0.1% YoY revenue expansion. And for the FY, the topline expansion has been close to 12%.

But in 2023, at least in the first quarter, the firm that posts profitability like an early stage growth company, won’t be a growth company anymore. Although Snap did not give formal guidance going into 2023, the investor letter highlights that company internal forecast model a YoY decline of between 2% and 10% for Q1 2023. This is a sharp contrast to analyst estimates, who were expecting a slight revenue expansion.

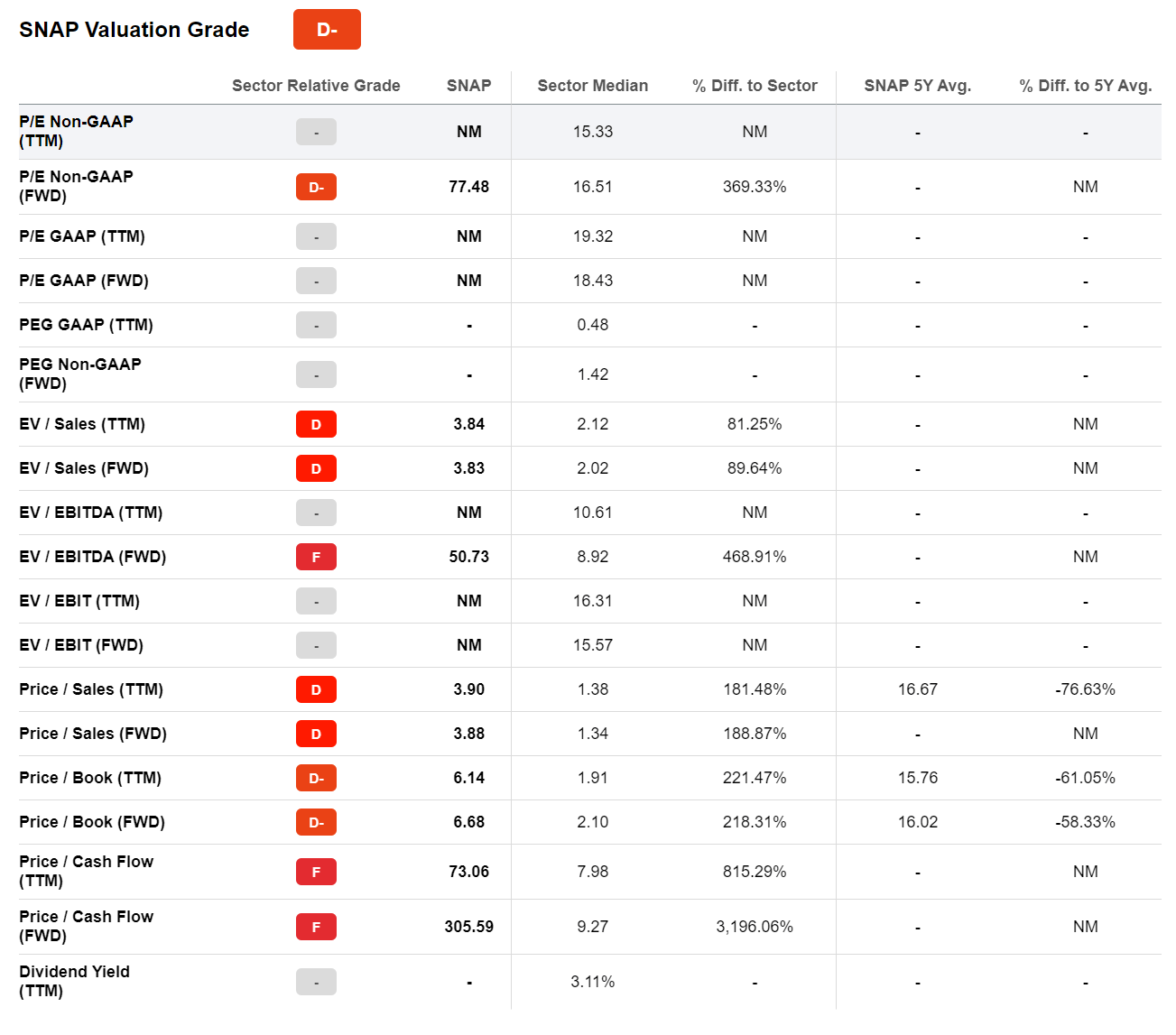

Reflecting on such a warning, it is hard to argue that Snap stock deserves to be priced like a growth company, valued at about x4 P/S, x6 P/B and x77 P/E — reflecting a premium to the industry of approximately 190%, 220% and 370% respectively.

Seeking Alpha

While there are clearly macro-economic challenges for Snap, acknowledged by management…

On the monetization side, we anticipate that the operating environment will remain challenging, as we expect the headwinds we have faced over the past year to persist throughout Q1

…some headwinds also appear structural. Notably, Apple’s updates to its privacy policies are unlikely to fade going forward, and competition with Meta (META) and TikTok will likely only accelerate.

Residual Earnings Model

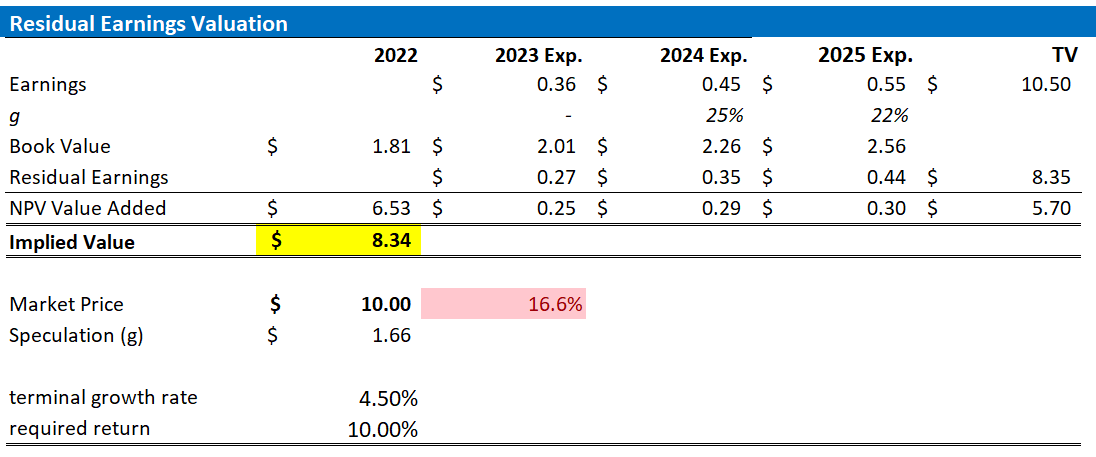

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my Snap stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor Snap’s cost of equity at 10%.

- For the terminal growth rate after 2025, I apply a proud 4.5%, which is approximately double the estimated long-term nominal GDP growth (to reflect a strong growth until at least 2030).

Given these assumptions, I calculate a base-case target price for Snap of about $8.34/share.

Analyst Consensus EPS; Author’s Calculations

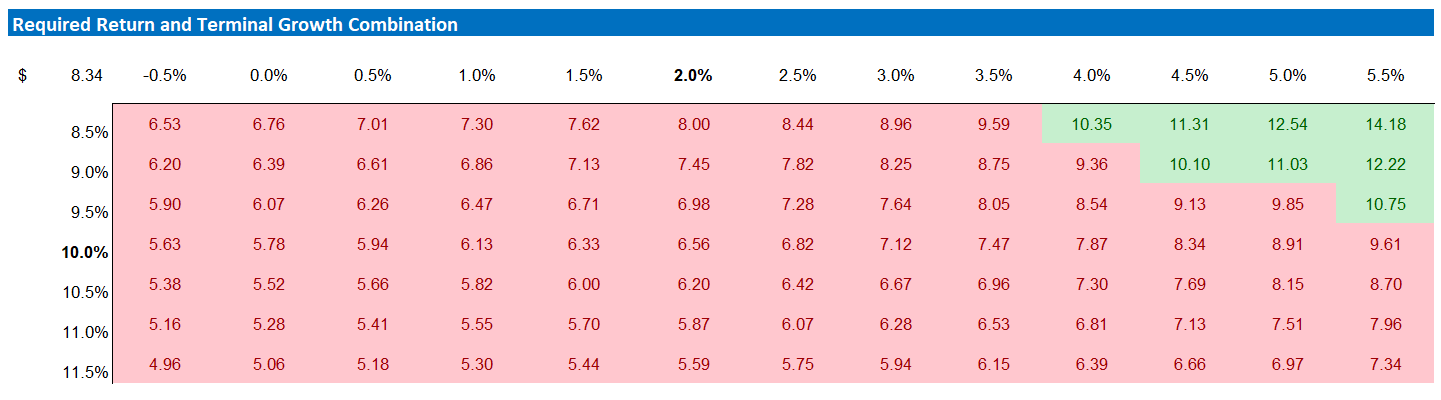

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of Snap’s cost of equity and terminal growth rate, I have constructed a sensitivity table.

Analyst Consensus EPS; Author’s Calculations

Conclusion

Shares of Snap dropped 28% the day after its Q3 earnings report in October. Shares also declined 39% in July after its Q2. And after Q4 reporting, the stock declined once again, a 15% drop in after-hours trading.

While Snap’s Q4 2022 results were mostly in line with expectations, the company’s warning of a potential 10% decrease in revenue in Q1 2023 caused concern among investors, as revenue contraction most certainly does not support the company’s growth valuation premium.

Anchored on a residual earnings model, I value Snap stock at $8.34 and consider the company a “Hold” at best.

Be the first to comment