feellife/iStock via Getty Images

Investment Thesis

SMART Global (NASDAQ:SGH) is a specialty memory, storage, and hybrid solutions company. The business is in the process of moving beyond memory solutions toward a customer engagement model focused on its Intelligent Platform Solutions (”IPS”) and LED solutions.

What I find particularly interesting is SGH’s IPS business already makes up nearly half of the total business and it grew last quarter by 78% y/y as of fiscal Q1 2023.

SGH stock’s valuation is compelling at 8x EPS. But I won’t spend any time on that consideration, because there’s a lot more to like from SGH than just its cheap valuation.

The Setup for 2023

SGH is in the process of diversifying its strategy away from being just a memory module company to a company that services the specialty, compute, LED lighting, and memory business.

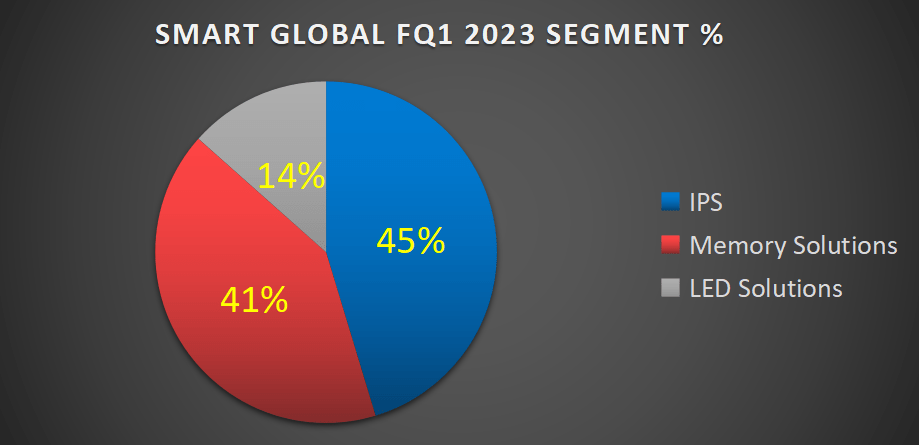

What follows is the breakdown of the business.

Author’s calculations

What you see is a business that is mostly tied to the memory business but is in the process of growing its Intelligent Platform Solutions (”IPS”) unit.

SGH’s IPS unit is responsible for specialized platform solutions. This is essentially a low-volume high-value tailored service for high-performance computing (”HPC”) and AI technology. This is the crown jewel of the investment thesis.

As more customers move away from data center to the cloud, there’s a need to understand exactly what are the best options available. This is where SHG’s customer-led designs gain traction.

With this context in mind, let’s discuss its outlook.

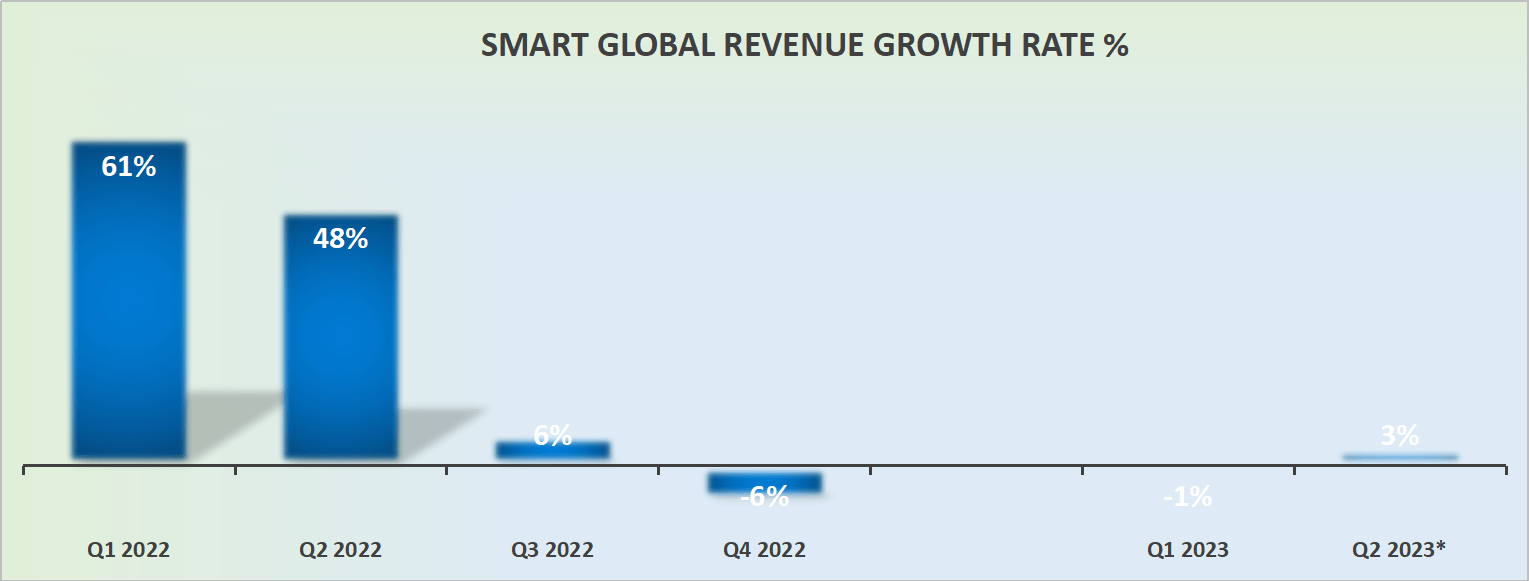

Revenue Growth Rates Set to Improve

SGH revenue growth rates

As you can see above, it’s not only that fiscal Q1 2023 posted sequential growth from fiscal Q4 2022, but that coming out of fiscal Q1 2023, the outlook for fiscal Q2 2023 points to further sequential growth.

Hence, if we take a step back, we can see that on a y/y basis, fiscal Q2 2023 is going to be more likely than not to report positive growth rates when compared with the prior year’s quarter.

In sum, not only is fiscal Q2 2023 likely to grow compared with the challenging comparable period last year, but the remainder of fiscal 2023 will have progressively easier comps as the quarters progress.

Furthermore, as touched on already, the AI-facing business, the IPS unit grew 78% y/y. That being said, keep in mind that SHG made a large acquisition of Stratus Technologies back in August 2022, which is obfuscating its near-term growth rates. Nevertheless, I suspect that on an adjusted basis, the IPS segment could continue growing at 30% CAGR over fiscal 2023.

But there’s more good news too.

Margins Continue to Improve

The way to think about SGH is as two businesses.

There’s the ”no-growth” memory solution unit. This business isn’t particularly attractive, but it does throw off positive cash flows.

And then there is the custom-designed high-performance computing platform to the cloud for customers within its IPS segment.

And even though management doesn’t provide any granularity, we can see that on a blended basis, SGH’s gross margins continue to move higher and are expected to once more repeat the record performance of fiscal Q1 2023 next quarter at 27%.

In sum, it’s not only that the business is growing but that the IPS business is reporting faster growth than the overall business.

And then, what’s even more impressive is that SGH isn’t compromising on gross margins, but actually expanding its gross margins.

The Bottom Line

No investment is without risks. Here are some risks that readers may consider.

- This business is small and cyclical.

- SGH has significant customer concentration. More specifically, 2 customers make up about 40% of the accounts receivable. If something were to happen to one of its customers, that could substantially impact its near-term prospects.

That being said, I’m very bullish on this company and I believe that paying 8x this year’s EPS while not exactly a ”no brainer”, certainly appears to be a good investment.

Be the first to comment