MJ_Prototype

Inflation is like toothpaste. Once it’s out, you can hardly get it back in again.” – Karl Otto Pohl

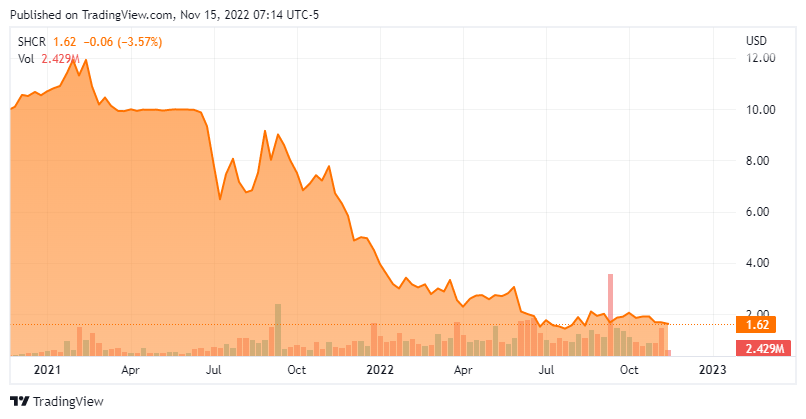

We are going to take our first look at Sharecare, Inc. (NASDAQ:SHCR) today. This SaaS concern was birthed out of a merger Falcon Capital Acquisition, a special purpose acquisition company (SPAC) in the summer of 2021. Like so many that debuted via this route during the SPAC craze of late 2020 and through most of 2021, the stock is now deeply in ‘Busted IPO‘ territory. With the stock down more than 80% from where it came public, is Sharecare a falling knife or oversold buying opportunity? An analysis follows below.

Seeking Alpha

Company Overview:

August Company Presentation

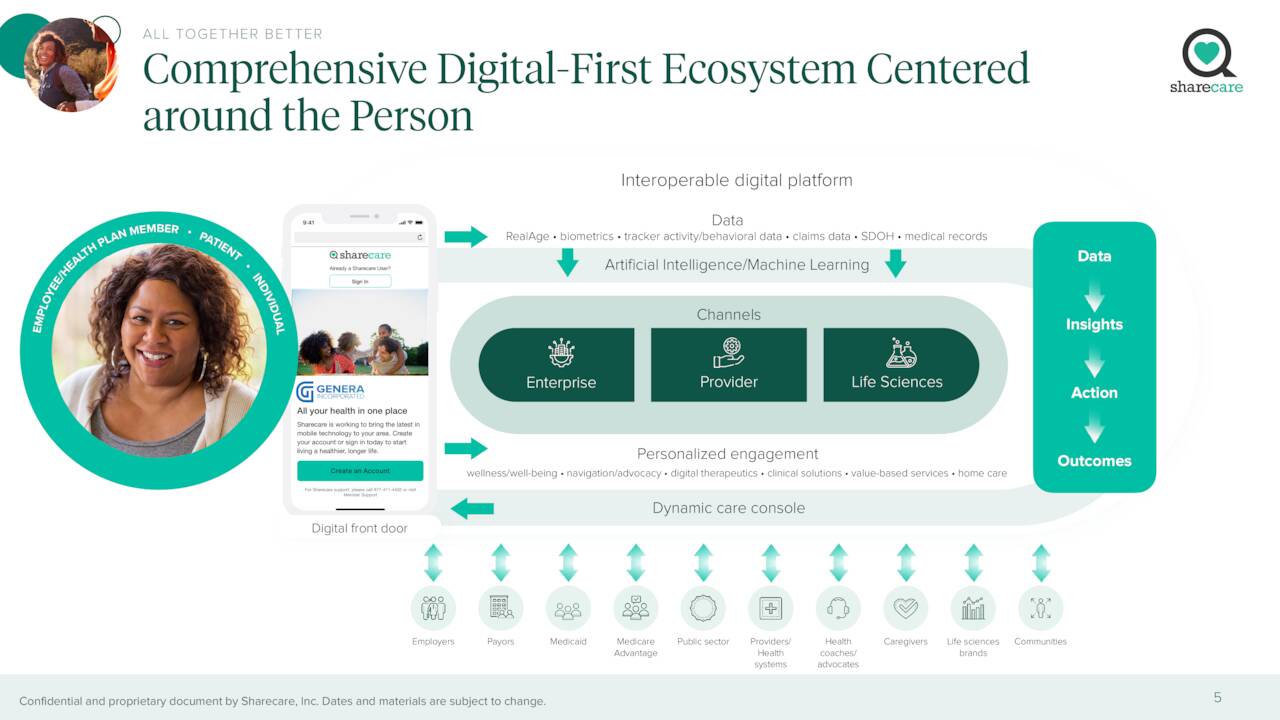

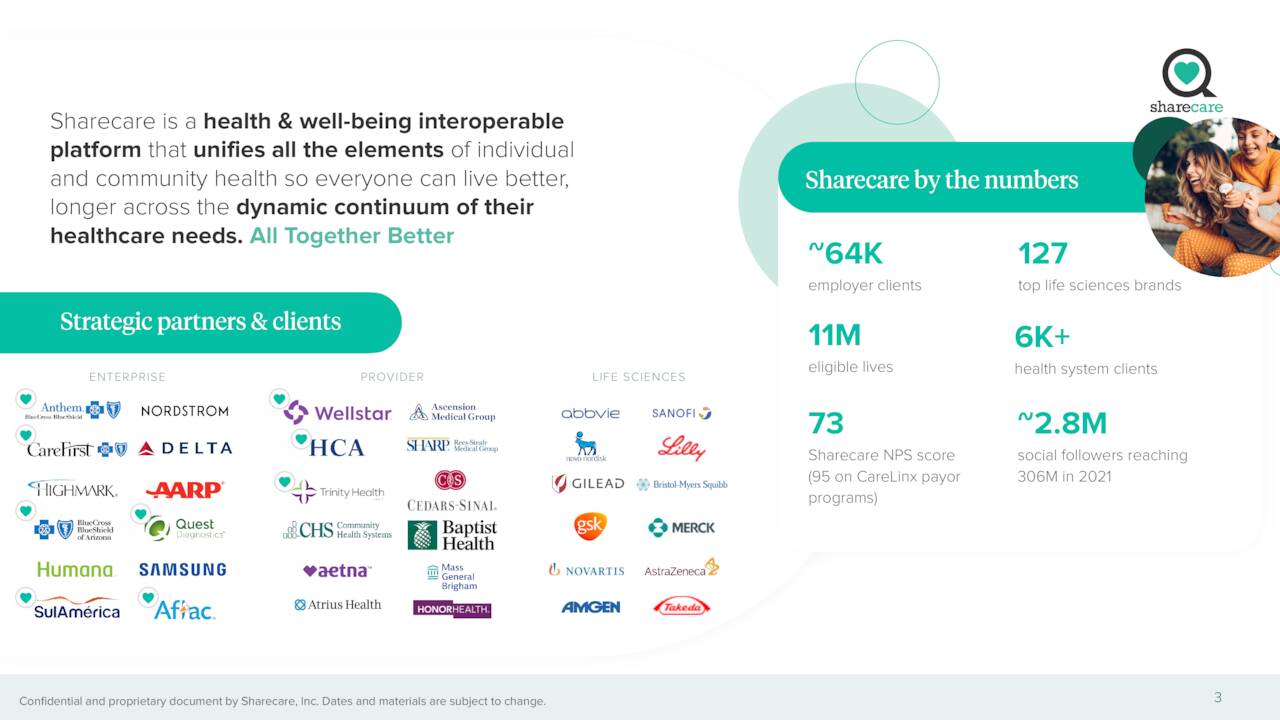

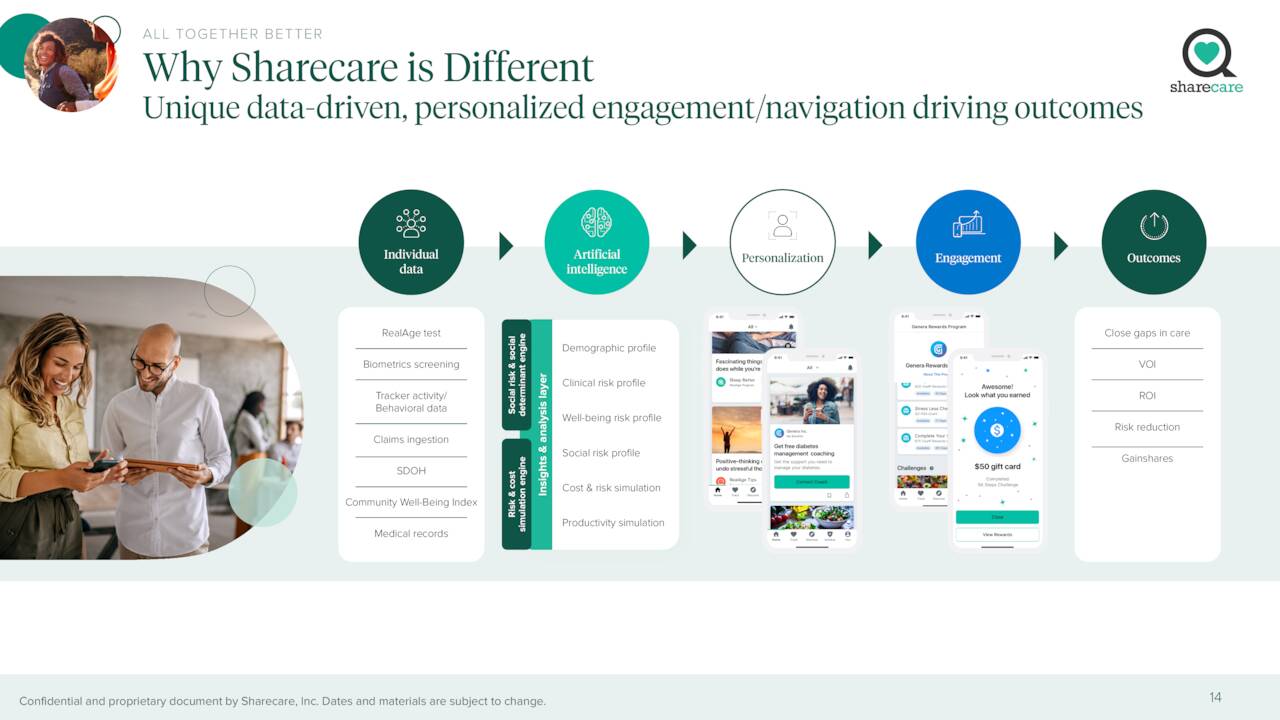

Sharecare, Inc. is based in Atlanta, GA. This digital health company helps people manage all their health in one place. The company also provides enterprise solutions based on a software-as-a-service model. This platform allows these clients to message, motivate, and manage their populations. They can also measure their population progress. Services also include a suite of data and information-driven solutions; and life sciences solutions, which provides members with personalized information, programs, and resources to enhance the health and well-being of their employees. Just over 11 million employees/customers currently use Sharecare’s platform, of which, 1.8 million are Medicare Advantage members. The stock currently trades just above $1.50 a share and sports an approximate market capitalization of $600 million.

August Company Presentation

The company breaks down its revenue streams into Consumer, Provider and Enterprise. In the second quarter, they accounted for $20.7 million, $28.7 million and $65.2 million in revenue, respectively.

Second Quarter Results:

On November 10th, the company posted third quarter numbers. Sharecare had a non-GAAP loss of one penny. Revenues rose 8.5% on a year-over-year basis to $114.6 million, which beat the consensus by some $5 million. Despite solid results for the quarter, the stock got dinged a bit in the market when numbers were released. This was due to management suspending guidance for the fourth quarter. Leadership will provide FY2023 guidance when it posts fourth quarter numbers in mid-February.

This is the second quarter in a row management chose to delay guidance. The reason given in the second quarter was the following:

A delayed start date for a large enterprise client, the initiation of the strategic review, changing macro-economic environment affecting life sciences, and certain cost initiatives being undertaken by the company, Sharecare is suspending financial guidance for 2022. “

Analyst Commentary & Balance Sheet:

Right after third quarter results were posted, Goldman Sachs (GS) reiterated its Hold rating with $2.10 a share price target. Then last week, both BTIG ($5 price target) and Canaccord Genuity (OTCPK:CCORF) ($3 price target) reissued Buy ratings on Sharecare.

Approximately four percent of the outstanding float in SHCR is currently held short. An insider bought approximately $25,000 worth of shares this June. That has been the only insider activity in this stock since it came public last year. At the end of the third quarter, the company held just over $200 million worth of cash and marketable securities on its balance sheet against no long-term debt. The company has $50 million left on a stock buyback authorization that was not active in the third quarter. This program was announced in May of this year.

The net loss attributable to Sharecare in third quarter $27.4 million compared to net loss attributable to Sharecare of $43.1 million in 3Q2021. However, the ‘adjusted‘ net loss attributable to Sharecare was only $2 million compared to adjusted net loss attributable to Sharecare of $800,000 in the prior year period. Cash burn during the quarter was $9 million.

Verdict:

The current analyst firm consensus has Sharecare losing approximately a quarter a share in FY2022 as sales rise some seven percent to some $440 million. They also project revenue growth will pick up to the mid-teens in FY2023 and losses will narrow to 18 cents a share.

At less than one and a half times sales, the stock is not that expensive from a price to sales basis. Equating for the net cash on Sharecare’s balance sheet, the equity goes for less than one times revenues. The problem is that Sharecare is likely to continue to lose money over the next couple of fiscal years. In addition, with corporations cutting back and instituting some notable layoffs of late, 2023 could be quite challenging. In addition, the withdrawal of forward guidance by management in the past two quarters should not give investors a warm and fuzzy feeling.

August Company Presentation

I have a good friend whose wife has worked in this niche for over a decade, and usually, these types of benefits are among the first to be cut or downscaled in times of economic duress at companies. That also was my experience working in Corporate America for two decades. Given all that, I am going to pass on any investment recommendations around Sharecare at this time.

Nothing so weakens a government as inflation. “- John Kenneth Galbraith

Be the first to comment