bizoo_n

I have been highly bullish on Silvergate (NYSE:SI). I see the company as a regulatory play on the Bitcoin ecosystem, a way to get exposure to Bitcoin without being overtly dependent on Bitcoin’s (BTC-USD) price direction. The company takes advantage of the Bitcoin adoption trend by getting zero-cost funding from institutions using the SEN network. Silvergate then applies those funds to high-quality assets (mostly mortgage securities, 97% AA- or higher).

However, one of the biggest growth drivers is a Bitcoin collateralized lending product that allows its clients to use their Bitcoin as a guarantee for funding, the SEN leverage lending. Here is where the cracks are starting to appear. The company publicly disclosed a margin loan to MacroStrategy, an entity owned by MicroStrategy (MSTR). Let us see how this might unfold.

Crypto domino

Right now, a crypto domino of bankruptcies is unfolding as we speak. It started with Luna’s (LUNC-USD) downfall (the algo stablecoin), then spilled to 3AC (the crypto venture capital fund) that was highly leveraged, and ended with the fall of the likes of Voyager (OTCPK:VYGVQ) and BlockFi. We thought the effect had stopped when Sam Bankman-Fried appeared in a white horse, buying some of the troubled assets. However, FTX’s downfall is now raising concerns around the whole crypto space, and it reignited the domino effect.

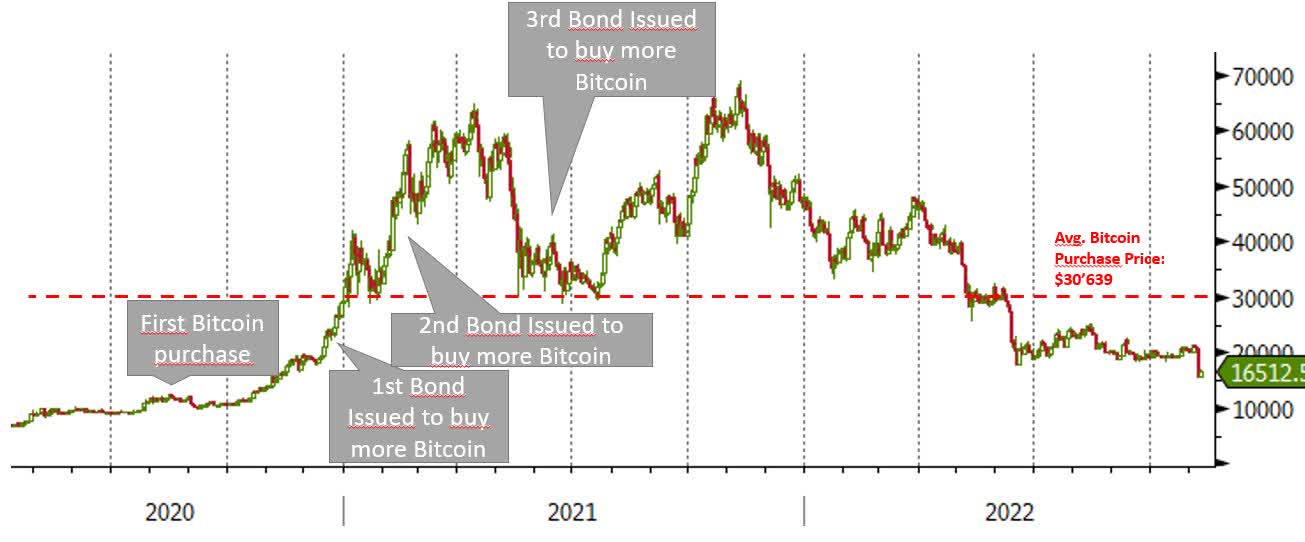

The million-dollar question is who’s next? At this point, one big contender is MicroStrategy. The company levered significantly to purchase Bitcoin during the last two years. While the first acquisition is still below the current price, the following cost more than Bitcoin is worth now.

MicroStrategy Bitcoin Buying (Twitter: @Elementcapl)

In other words, from the public info, we can estimate that the company has bought close to $4 billion in Bitcoin at an average cost of around $30,000. At the current market price of $16,000, the unrealized losses are close to 50% of the total position. The company might be able to cover the margin loan collateral and keep servicing the loans until the first maturity arises, and it might survive, but it has put itself into a tough spot.

Obviously, the current problems won’t stop with MicroStrategy. That is just one of the best-known names in the industry. Others will likely fall too. Players used credit in illiquid markets, but importantly, they used leverage in a highly volatile asset like Bitcoin. Ironically, in prior bankruptcies (like 3AC), it seems that lenders using smartcontracts in crypto platforms automatically recouped their loans. However, in those cases, the lending done through traditional financing will have to wait for the bankruptcy courts to try to get something back.

Impacts of the crypto domino on Silvergate

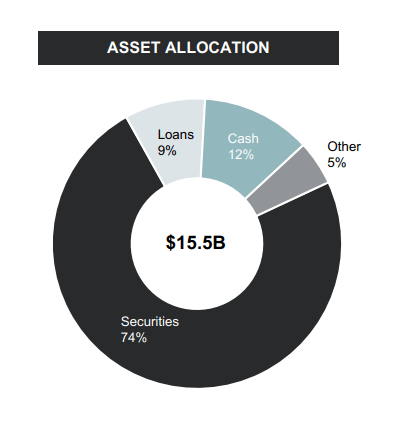

The most direct will be the ability to keep MicroStrategy’s margin loan out of losses. The loan has plenty of collateral, and it is likely to be recoverable in its entirety. However, the uncertainty is higher than ever. Not losing money in these SEN leverage loans will serve as a proof-of-concept for the whole business model. According to the company’s financial info, Silvergate has 9% of its balance sheet in direct loans:

Silvergate Asset Alocation (Silvergate)

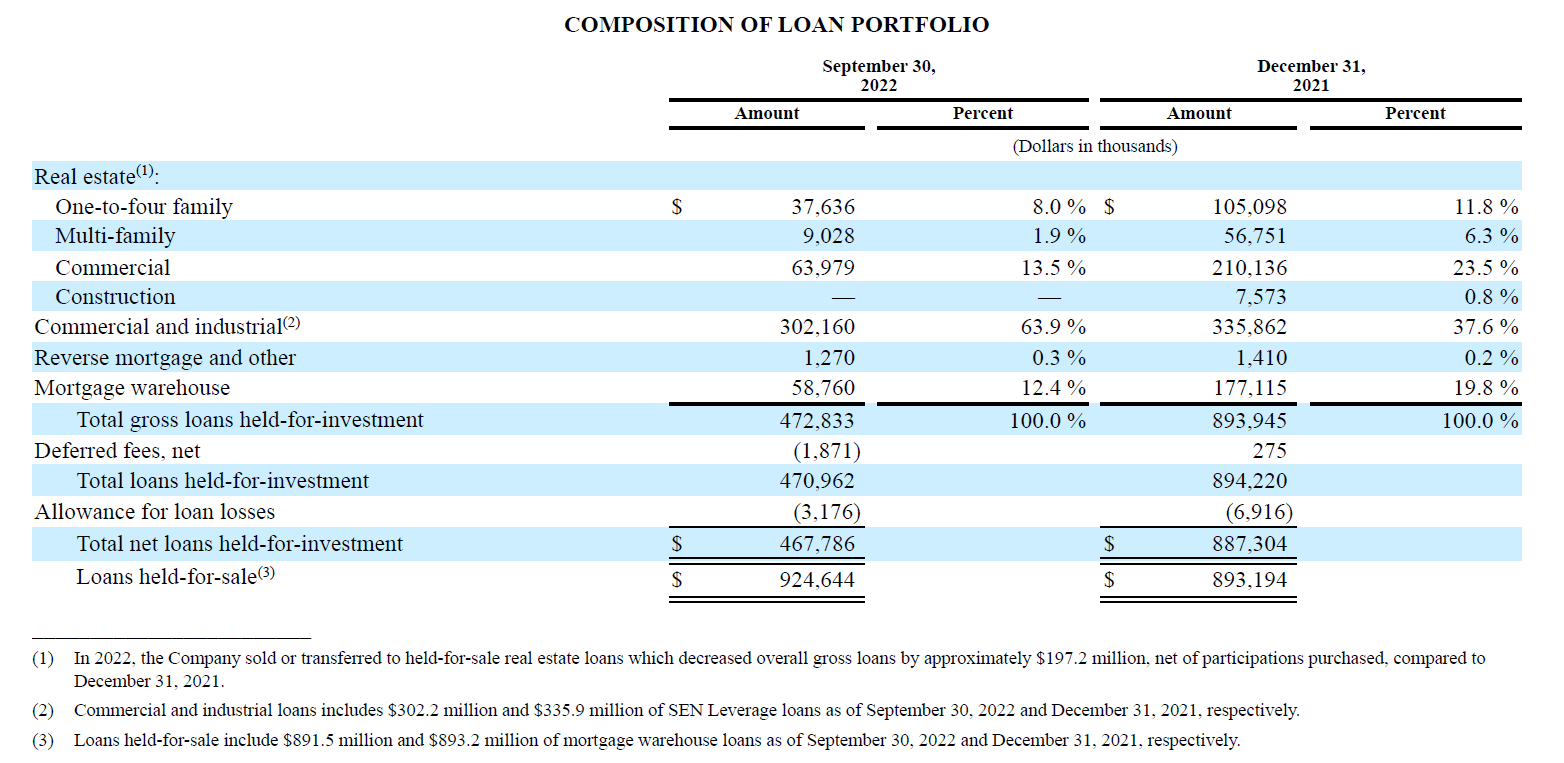

Of which around $300 million are SEN Leverage loans.

Loan Portfolio (Silvergate)

Conclusion

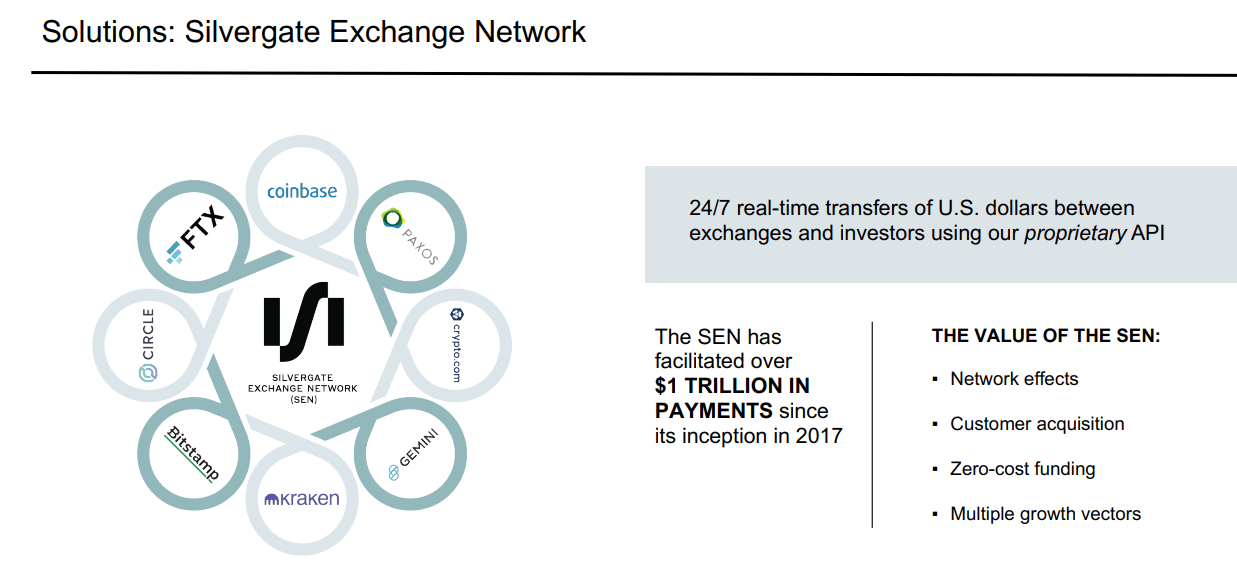

However, even if Silvergate does not lose any money in the loans, it won’t get away unscratched. They will lose customers in the SEN. FTX will be gone, and rumors are now circling about Crypto.com (CRO-USD) also facing a run. Silvergate issued a statement saying that the relation with FTX is limited to deposits, corresponding to less than 10% of 11.2 billion total deposits.

SEN (Silvergate)

Silvergate has traditionally avoided using its whole crypto deposits in its business. If this conservative approach reveals effective, that will be good for the company in the current turmoil. Nevertheless, the market is reading this as a weakness and downgrading the growth perspective for the company. The current market multiple is already recognizing lower growth and some loss recognition with a P/BV lower than one (stock price: $34.32).

If the company is able to hold ground and avoid major losses on its loans, it validates the current management strategy, and it might be an attractive entry point. However, the uncertainty has never been higher due to the multiple unforeseeable effects that the crypto downfall of several relevant companies might bring. The present context is a huge stress test for Silvergate’s management strategy and execution.

The balance sheet reveals what seems to be a somewhat contained exposure. However, the growth strategy is heavily dependent not on the Bitcoin price but on the thriving of the crypto ecosystem, and the falling domino will be a major headwind. Provided that the company avoids losses and the crypto industry can regrow, I think that Silvergate will be a good investment. But, both hypotheses will be battle-tested during the next few months.

Be the first to comment