Oselote

Investment thesis: The global mined silver supply has been stagnant. It has been sliding gradually lower over the past 8 years since a 2016 production peak, while demand, including for industrial applications, has been rising steadily.

Silvercorp Metals Inc. (NYSE:SVM) is a solid miner that is able to produce silver at a profit at current price levels. Its stock is currently down significantly from its 2020 record highs, mostly due to the effects of rising interest rates on precious metals prices. Long-term fundamentals make the current stock price levels a good entry point, with far more upside potential going forward than downside risk. It is my 2023 pick for a potentially outperforming stock, based on silver market supply/demand fundamentals, as well as a potential reversal in monetary policy next year.

2022 is shaping up to be a lackluster year for Silvercorp from a financial standpoint. Silver prices have been a drag.

Silvercorp’s stock is down almost 23% YTD, with this poor performance being mostly a reflection of its financial performance. For the latest quarter, it managed to put in a net loss of $10.2 million, on revenues of $51.7 million. In other words, the profit margin was -20%. For the first nine months of the year, it is still above water, with net earnings of $3.9 million, on revenues of $115.3 million. It is a very significant deterioration in its financial performance compared with the first nine months of 2021, when it achieved net earnings of $29 million, on revenues of $117.3 million. A significant rise in mining costs of $8 million played a significant part. A foreign exchange loss of $6 million also hit the company’s profits. Some of these pressures on profitability, such as the FX loss portion of it may improve in the fourth quarter. Energy and other mining input costs may come in lower in the current quarter as well.

An ample resource base, which could get more valuable in time as silver market fundamentals move towards a potential supply shortfall.

Based on its fiscal 2022 estimates, Silvercorp is sitting on 108 million ounces of proven & probable silver reserves, with some additional gold, zinc, and lead resources. At current production rates, it seems that it has about two and a half decades worth of proven & probable silver reserves. It should be noted that currently, about 54% of its sales are coming from silver in terms of revenue, with gold, lead, and zinc making up the rest.

I followed silver and its emergence as a very valuable industrial input for a growing number of goods produced throughout the global economy for a very long time. A number of technological developments played a role in suppressing what is otherwise a very obvious trend of growing global reliance on silver inputs in industry. The industrial demand-driven bull market for silver thesis took a massive hit a very long time ago as photography moved to mostly digital, greatly reducing the need for silver. Then it took a second major, prolonged hit from a drastic reduction in silver use per solar panel, which led to a full decade of lackluster demand.

These two major events played a pivotal role in masking the otherwise obvious trend of growing silver demand in industrial applications. There are, however, signs emerging of those factors having been spent, with a resumption in industrial silver demand growth.

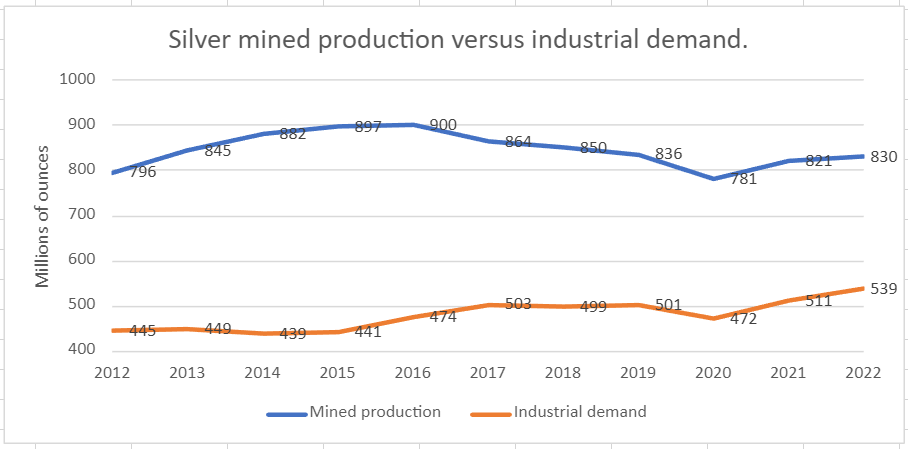

Data source (Silver Institute)

The reason why I tend to focus on mined production versus industrial demand when it comes to my assessment of the global silver market outlook is that it represents in my view the clearest picture of the true supply/demand situation. Industrial demand currently makes up about half of all silver demand. Unlike most other demand factors, it is a source of demand that often leads to non-retrievable uses. Some industrial recycling does take place, but a lot of the silver ends up being lost forever. In regards to total global supplies, the most often cited number is the number that includes recycling. In other words, it includes jewelry that is recycled, industrial retrieval, and so on, on top of the mined production volumes. These factors may serve to distort the true long-term trends to some extent.

As we can see, silver prices at current levels do not seem to be enough of an incentive for global silver miners to continue increasing production, which peaked in 2016, and it is not entirely clear at this point what it would take for producers to ramp up production. We are currently about 8% below those peak production levels. In the same timeframe, industrial demand for silver increased by about 12%, which contributes to a narrowing in the mined production, versus the industrial demand gap that is visible in the chart above.

Industrial demand will continue to be driven by solar panel manufacturing growth, as well as many emerging uses of silver in electronics, where a small amount tends to make a significant difference in terms of performance. The dramatic decline in silver volumes used per solar panel produced is proving to be a long-term blessing for the silver market. It makes it feasible to continue using silver in the panels even as silver prices are likely to increase. The cost of the silver used in a panel was around 10% of the total cost of the panel last year. In other words, if silver prices were to double, it would add about 10% to the cost of a solar panel, which the market can absorb. The quadrupling of the price of silver would lead to a 30% increase in solar panel prices, with all other factors held equal. It would become more painful to bear, but still it would not necessarily lead to the replacement of silver with copper for instance, where panel performance would suffer in the process.

A hypothetical doubling of the price of silver would in theory lead to a roughly 50% increase in Silvercorp’s revenues, while a significant increase in net earnings would also be forthcoming, with all else held equal. It remains to be seen whether a tightening of the supply/demand situation can lead to such an outcome, perhaps with other factors also playing a role, such as a possible sustained rally in gold prices, which tends to drag the price of silver along.

An interesting calculation, made in 2017, estimated that it would take about 51 billion standard solar panels to power the global electric grid, given the needs at the time. It is estimated that about 20 grams of silver, or about 2/3 of an ounce, is needed to produce one panel.

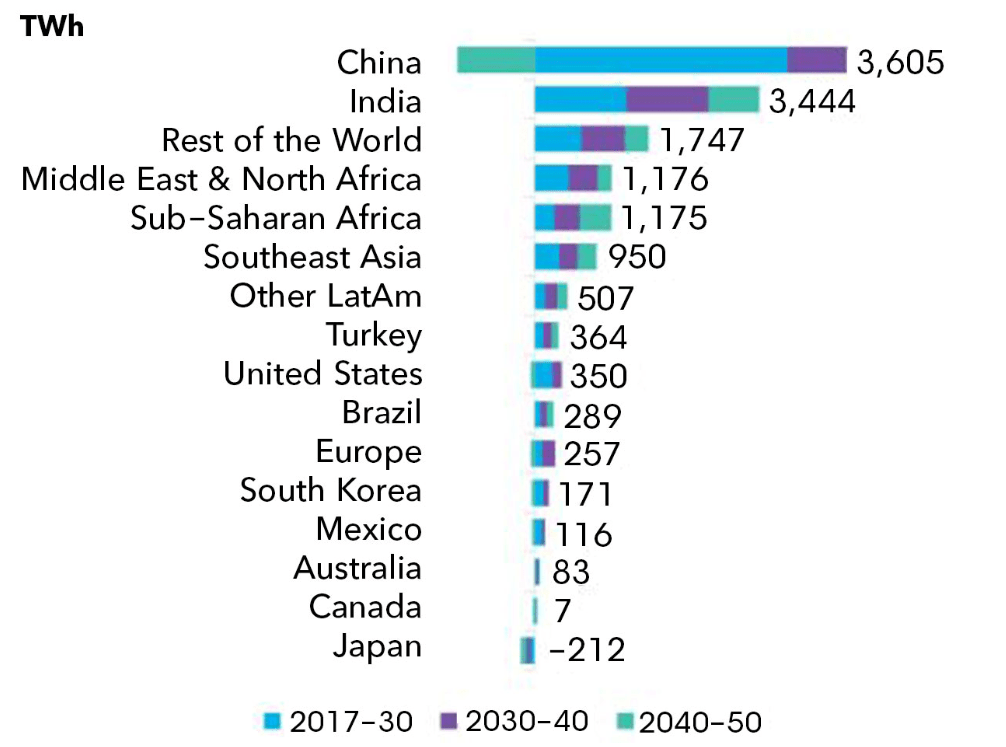

Global electricity demand growth (Bloomberg)

Relative to 2017 global electricity demand levels, it is estimated that perhaps a demand increase of about 55% will occur by 2050. With all else being held equal, it would take about 80 billion solar panels to run the global electricity grid on strictly solar panels by 2050, needing about 51 billion ounces of silver. Of course, we can also assume that solar panel efficiency will improve in time, while the amount of silver going into a solar panel should be further decreased. It also goes without saying that even in the most optimistic scenario out there, the global electrical grid will not be run exclusively by solar, ever.

Silver Institute

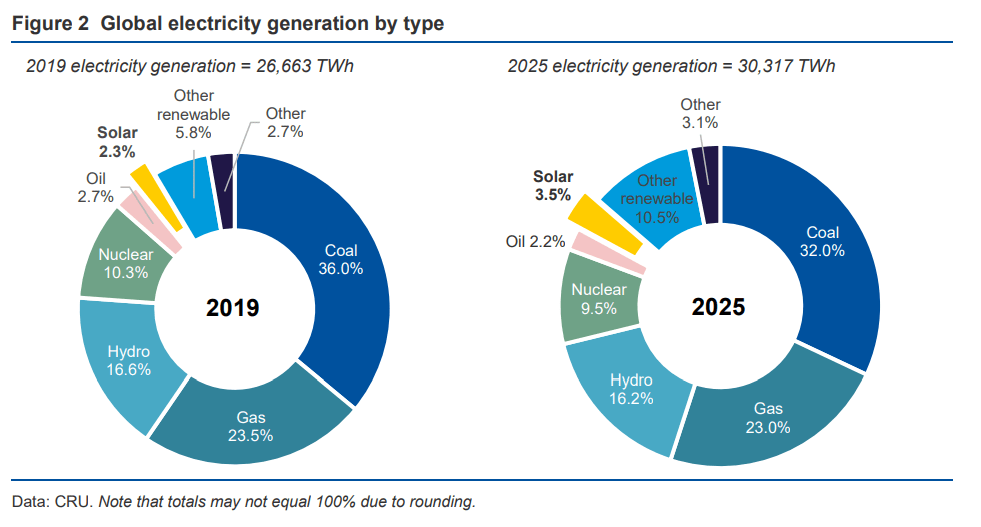

As we can see, between 2019 and 2025, solar’s share of global electricity generation is set to increase from 2.3% to 3.5%. Even though the rate of growth is exponential, the low base effect makes for a relatively minor overall change in the global energy mix. Assuming the same exponential rate of growth all the way to 2050, it would account for roughly one-quarter of all electricity produced worldwide, either directly or indirectly, as some of it may be converted to hydrogen, which would then be used to power the global grid.

Assuming the same amount of silver going into a panel as it does now, silver demand in solar panels could be about 12 billion ounces between now and 2050, which amounts to roughly 54% of all mined silver supplies between now and then, assuming mined production will remain stable at current levels. This figure might change somewhat as other factors will likely alter the outcome. Continued efficiency gains can reduce the amount of silver needed.

On the other hand, we will start to enter the window where solar panels installed right about now, as well as over the past few decades will start to expire and will need to be replaced. This need will grow exponentially, the same as the solar power generation capacity itself.

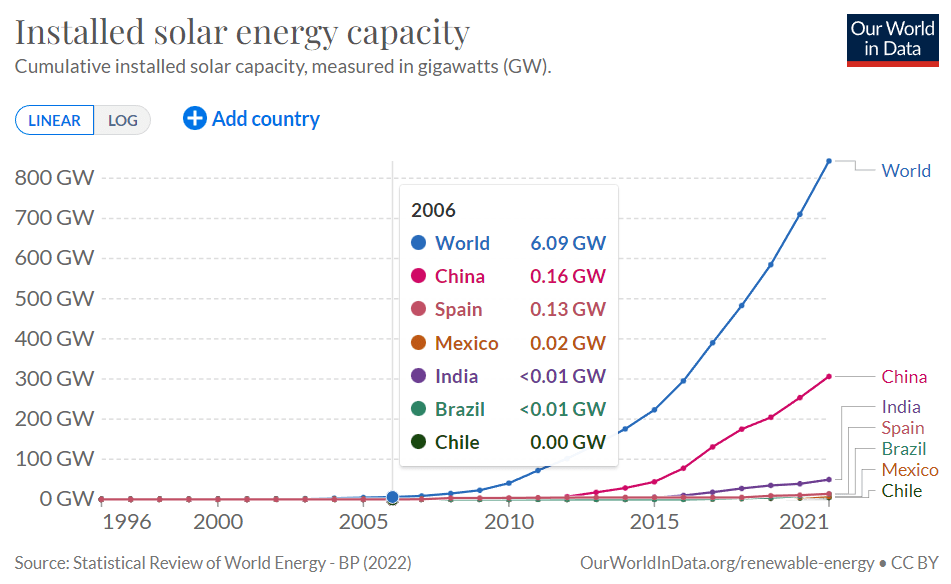

Our World In Data

We should keep in mind that there are other growing industrial uses for silver, including in ever more sophisticated electronic devices, ranging from cell phones to electric vehicles (“EVs”). It is estimated that between 25 grams and 50 grams of silver go into each EV, which could also become a significant source of demand growth in time.

Investment implications

Looking at all these factors, as well as the already-established supply/demand trend that we are seeing for some years already, it seems to me that the global mined supply, versus industrial demand gap for silver, is set to shrink and perhaps disappear altogether in the next few years, or perhaps within a decade.

If all or most of the mined supply will get used up in industrial activities, the silver that will be left for all other non-industrial needs, such as for jewelry, or as investment assets such as coins and bars will see a stagnation in volume growth, for the first time in human history. In an extreme scenario, some of the already existing silver above ground in various forms will start to flow into industrial uses as well, if mined supplies will fall short, leading to a net shrinkage in silver available for non-industrial consumer needs.

Seeking Alpha

As we can see, Silvercorp stock is down more than 30% for the past year. Rising interest rates have not been kind to the precious metals market. Markets do have a tendency to repeat prior trading patterns, with correlations being reinforced by the herd effect. We should keep in mind that the trend also works in reverse, once we will start to see monetary easing.

Even with the significant decline in its stock price, its forward P/E is not particularly attractive. At a ratio of over 13 currently, it is far above P/E levels that one might regard as ideal for a mining company, given that commodities extractors are highly cyclical, thus the risk volatility needs to be factored in. If, however, my thesis in regards to silver prices is correct and we will see a significant and sustained rally in silver prices, then Silvercorp stock makes sense, given that it, in effect, becomes a growth stock, on the back of higher revenues and profits.

Besides the tightening global silver supply/demand realities and future outlook, there is also the matter of recent signals from the U.S. Federal Reserve starting to contemplate a softening of its tightening policy, which should give precious metals prices a boost next year. The selling we saw in Silvercorp’s stock from over $8/share reached in 2020, to less than $3/share currently is a buying opportunity, given all the factors that suggest that things are looking up for most silver producers. In the short term, we have the growing odds of monetary easing, which is bullish for precious metals, while long-term investors should be looking at this as a buying opportunity, based on the silver market fundamentals that are emerging. For this reason, I consider Silvercorp Metals Inc. stock the candidate to be my best investment performer in 2023.

This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

Be the first to comment