ultramarine5

Investment Thesis

The Signet payment platform has been a key driver of Signature Bank (NASDAQ:SBNY, NASDAQ:SBNYP) stock’s explosive growth in 2021, but it is also the main source of bearish sentiment today. The market fears that the outflow of digital deposits could jeopardize the financial strength of the bank. However, the impact of crypto on Signature metrics is very limited because:

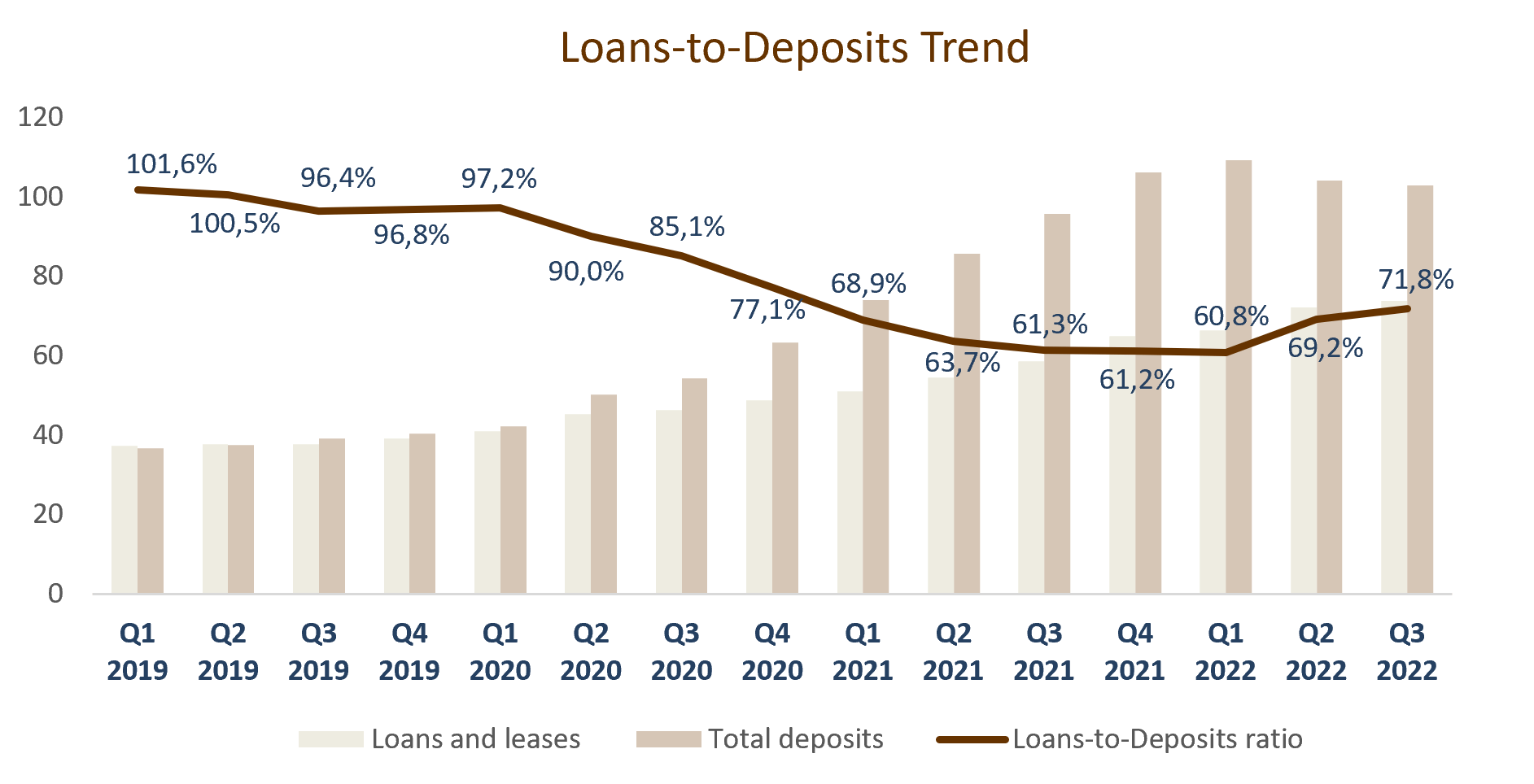

- The deposits of crypto-companies account for only 22.9% of the bank’s total deposits. Even if all digital deposits are liquidated, the Loans to Deposits ratio will be 93.1%, significantly lower than throughout 2019, when the ratio was at the level of 96.4-101.6%.

- Signature manages to partially offset the digital deposits outflow. So, in the third quarter, the volume of digital deposits decreased by $3 billion, but total deposits decreased by only $1.3 billion.

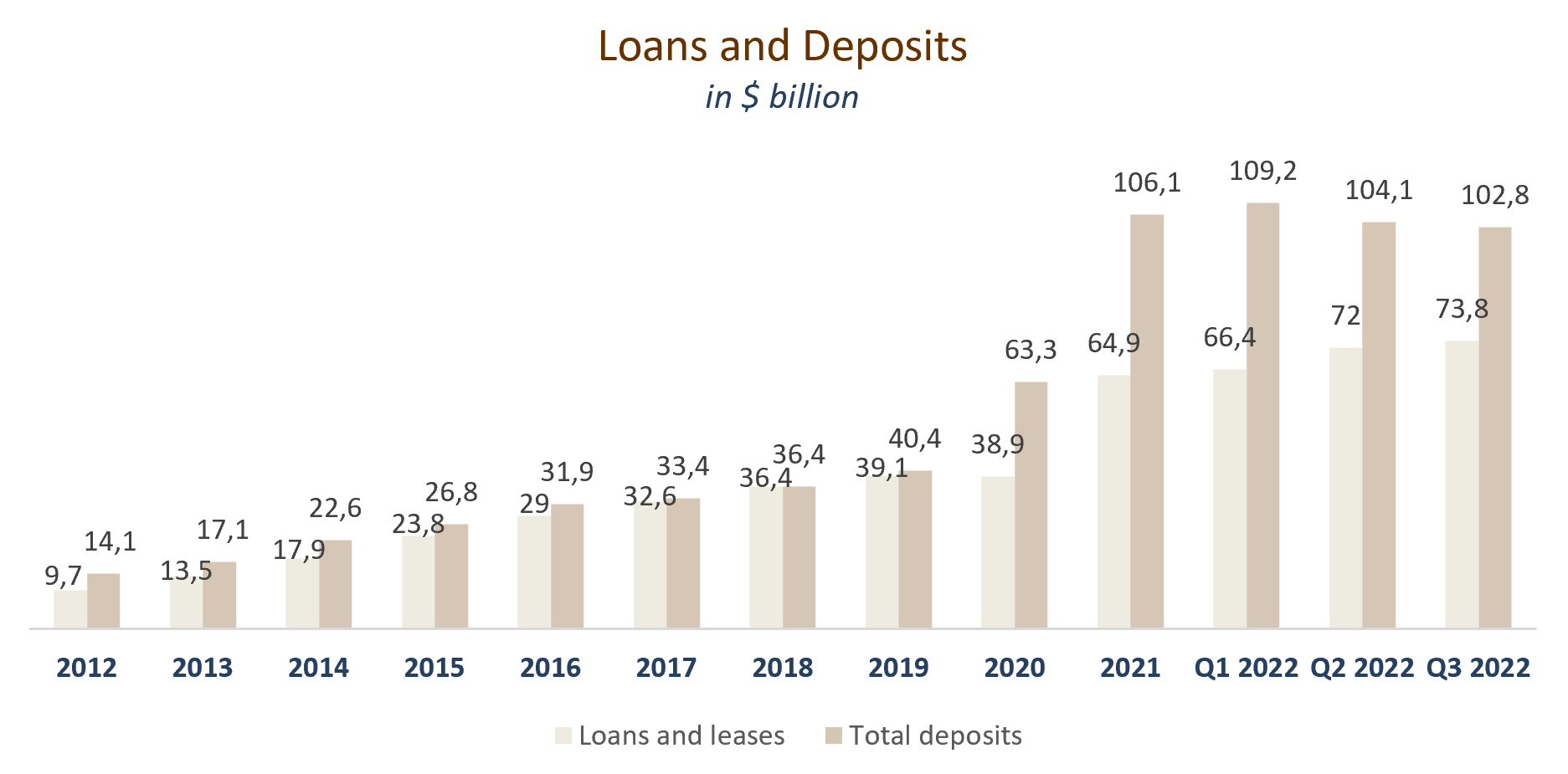

- Cryptocurrency-backed loans account for only $100 million, out of a total loan portfolio value of $73.8 billion. Signature’s loan portfolio is of high quality, with a ratio of total net charge-offs to average loans lower than that of the top 50 US banks.

The market has more than priced in all the possible risks associated with crypto. However, it ignores that Signature is a perennial compounder. Over the past 10 years, the bank’s loan portfolio has grown at a compound annual rate of 22.50% and EPS has increased at a CAGR of 17.99%. Signature demonstrates one of the best Efficiency Ratios in the industry and outperforms the largest US banks. According to our valuation, Signature Bank trades at a significant discount to its fair market value. We rate shares as a Strong Buy.

Company Profile

Signature Bank is a full-service commercial bank focused primarily on servicing businesses, enterprise owners, and top management. The bank has 37 client offices in New York, Connecticut, California, and North Carolina. Signature offers clients a full range of products and services, including insurance, specialty finance, leasing, brokerage, and asset management.

In 2019, Signature launched the Signet platform, which allows institutional crypto companies to transact with each other in real-time, 24 hours a day. The bank became the first member of the FDIC in the market for payment solutions for the crypto industry, and Signet became the first product approved by the New York State Department of Financial Services.

Limited Impact of Crypto

After the launch, Signet quickly gained popularity among institutional crypto companies. Crypto exchanges, mining companies, hedge funds, prop trading firms, and so on began to massively join the platform. Client assets used within Signet are held in non-interest-bearing deposit accounts in Signature Bank. Thus, clients get access to reliable payment infrastructure, and Signature gets access to cheap capital.

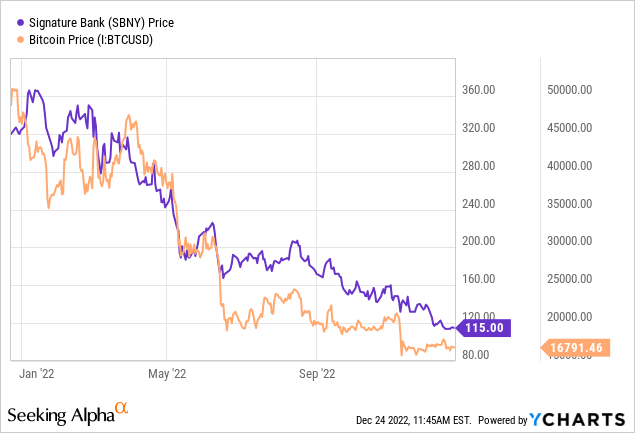

As a result of the bull cycle in the cryptocurrency market, the number of participants in the platform and their balance increased significantly. Signature received a massive influx of non-interest-bearing deposits. Signet has been a key driver of the bank’s 2021 share price rally, peaking at $366. However, it is also the main factor in bearish sentiment today. Since the beginning of the year, the capitalization of Signature has fallen by 65%, and the correlation of the bank’s shares with bitcoin has reached 0.69.

Recall that classical banks earn on the spread between the cost of capital raised, reflected in the liabilities side of the balance sheet, and the rates on loans issued. When the liability of the balance sheet decreases (for example, when customers withdraw deposits), the bank has nothing to finance its assets (its loan portfolio). At best, the bank may suffer losses by diluting capital or liquidating the loan portfolio at a discount to fair value; at worst, the bank may go bankrupt.

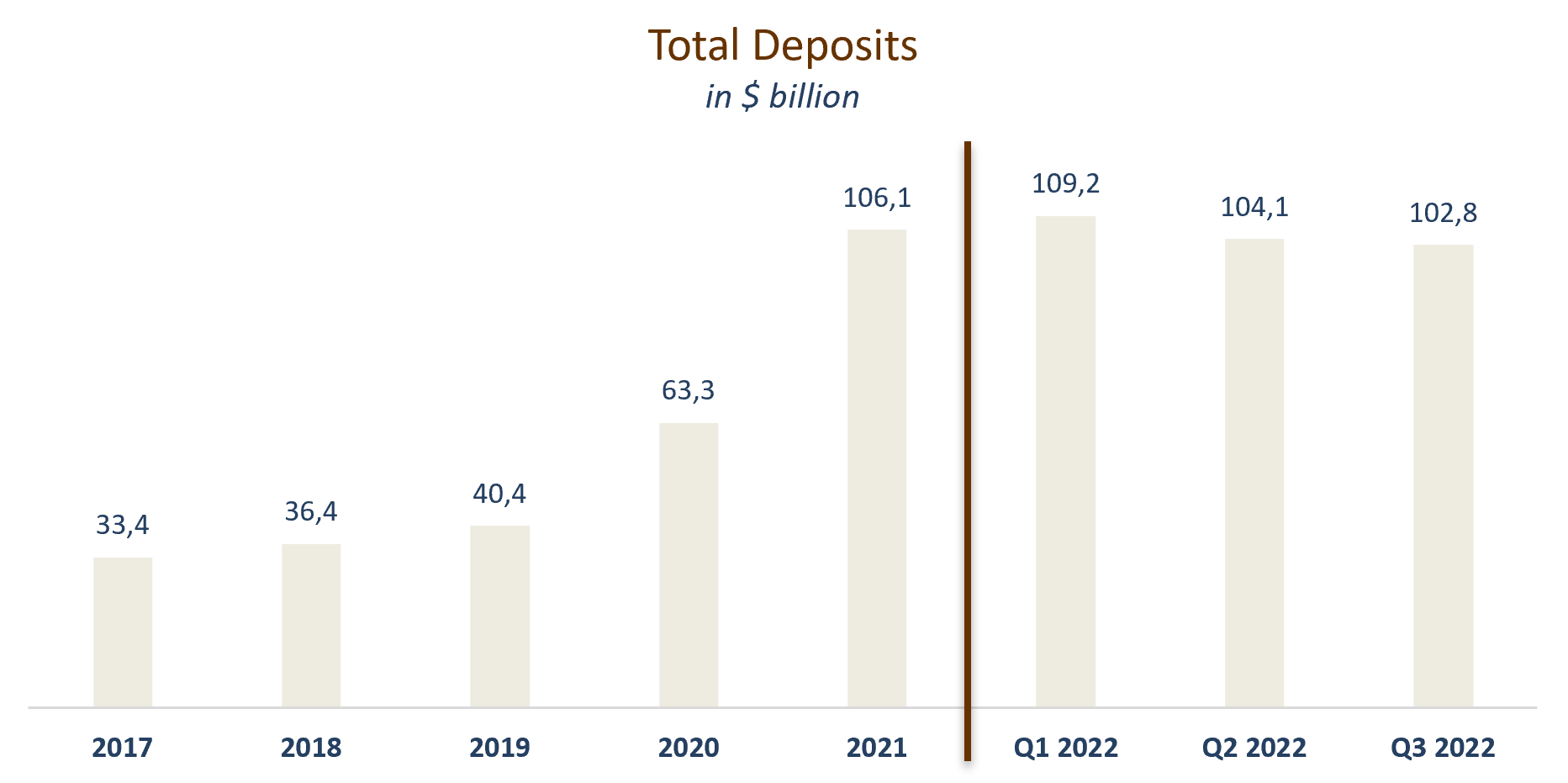

Investors fear that a prolonged decline in the crypto market will lead to a further reduction in deposits. These fears are not groundless. Signature deposits have been declining steadily over the past quarters.

Created by the author

However, the degree of influence of crypto on the stability of Signature Bank is greatly overestimated by the market.

In the third quarter, digital deposits accounted for only $23.5 billion, or 22.9% of all Signature deposits of $102.8 billion. Let’s make one extremely improbable assumption. If all crypto companies leave Signet, the bank’s deposit balance will be $79.3 billion, which still exceeds the value of Signature’s loan portfolio. As of September 30, the Loans-to-Deposits ratio was 71.8%. Excluding digital deposits, the ratio is 93.1%, which is still significantly lower than during 2019, when the indicator was at the level of 96.4-101.6%.

Created by the author

Secondly, Signature manages to partially offset the outflow of digital deposits. So, in the third quarter, the volume of digital deposits decreased by $3 billion, but total deposits decreased by only $1.3 billion, as there was an influx in other areas.

Thus, the impact of crypto on the financial position of Signature is very limited. If the crypto market does not turn around in the short/medium term, the bank’s digital deposits are likely to be crowded out by more traditional capital providers. At the same time, if a new rally starts, Signature could multiply in price, as the company has a high correlation with Bitcoin. It should be noted that the bank is actively developing Signet. In the last quarter, 116 new members joined the platform, bringing the total to 1,439. In October, Coinbase (COIN) announced that it would settle with its institutional clients through Signet.

Current Loan Portfolio

Signature is a perennial compounder. Over the past ten years, the bank has steadily expanded its geographical presence and customer base. The balance of deposits grew at a compound annual rate of 21.98%, while the loan portfolio showed a CAGR of 22.50%.

Created by the author

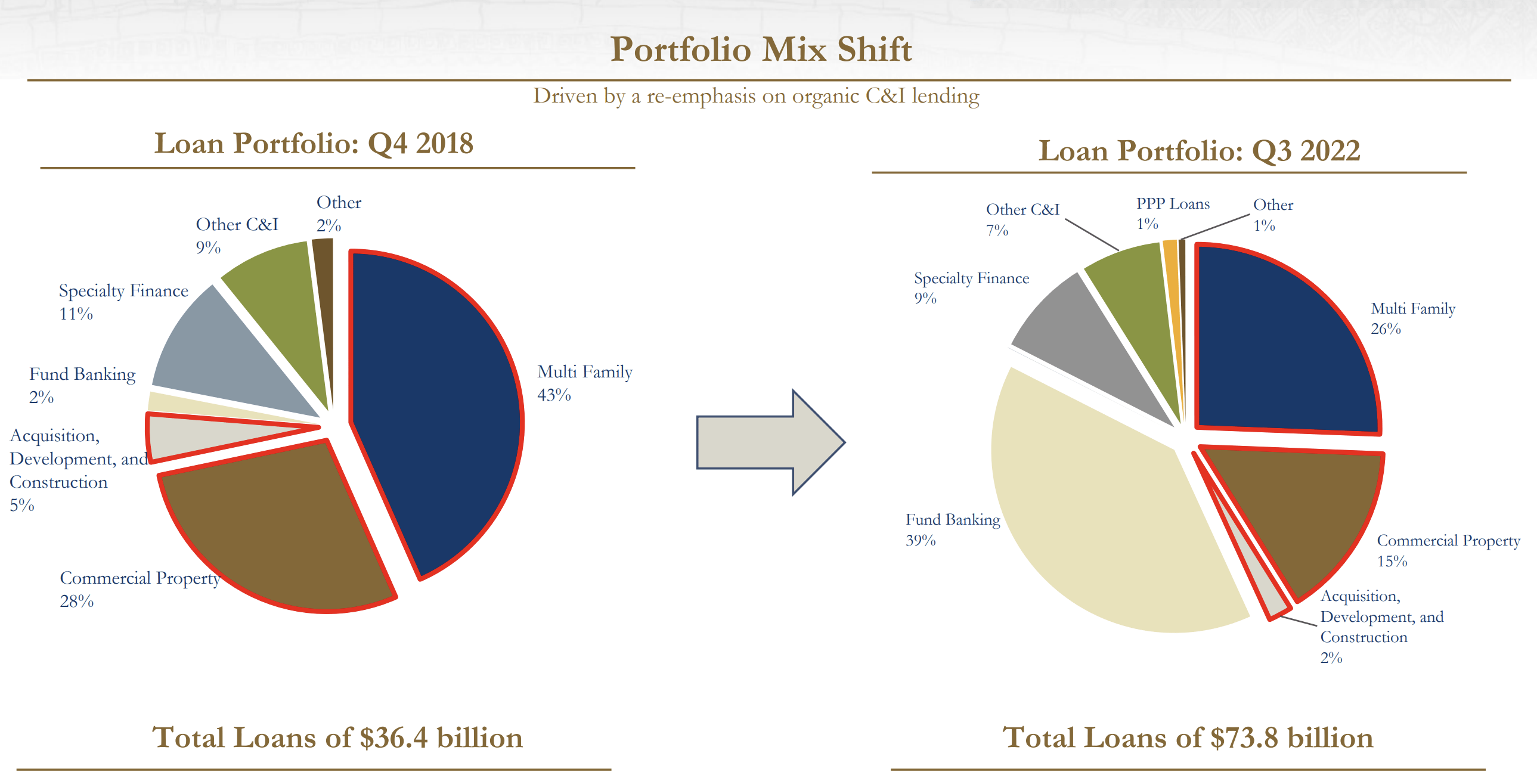

While Silvergate Capital (SI), the main competitor in the crypto infrastructure market, is actively reducing its traditional banking business and increasing its portfolio of loans secured by cryptocurrencies, Signature Bank takes a conservative approach to lending. Signet members can get a loan secured by crypto, but today such loans account for only $100 million, with a total portfolio value of $73.8 billion. Over 80% of Signature’s loan portfolio is in Fund banking, Multi-family residential property, and Commercial property.

Company Presentation

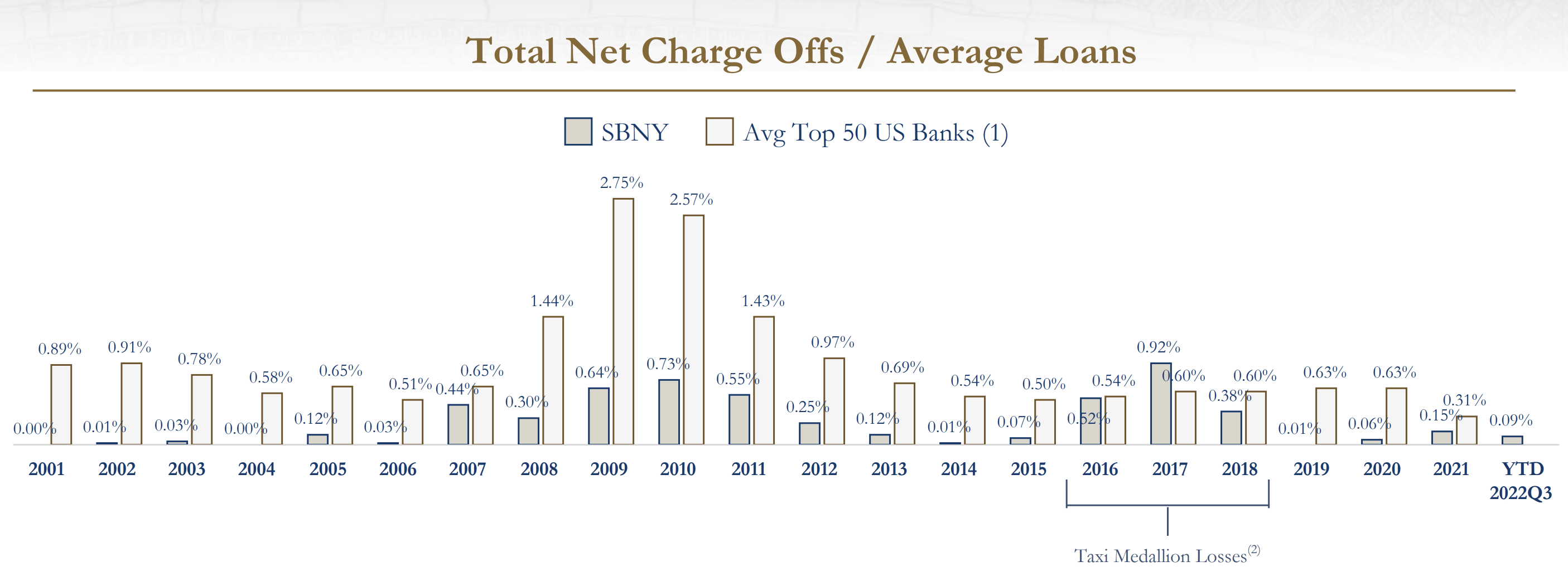

It is worth noting that the Signature portfolio has always been of high quality. Thus, since the bank was founded in 2001, its average ratio of total net charge-offs to average loans is 0.25% versus 0.91% for the 50 largest banks in the United States.

Company Presentation

The expected recession is forcing investors to be extremely selective when choosing stocks of financial institutions, especially when they are somehow related to crypto. However, as noted above, the impact of the current macroeconomic environment on deposits is limited, and the high quality of the loan portfolio allows Signature to weather any economic storm, with the possible exception of the new Great Depression.

Capital Allocation

Signature has a relatively short history of dividend payments and buybacks. In 2018, the bank’s shareholders approved a $500 million share buyback program, which was only partially implemented and suspended due to the pandemic.

Dividend payments are permanent. Signature began distributing earnings to shareholders in the third quarter of 2018 and has maintained payouts of $0.56 per quarter since then. It is worth noting that Signature has retained payments even in the pandemic of 2020.

The current dividend yield of around 1.9% is hardly an important argument to stay bullish. However, we expect the company to increase investor rewards once it overcomes crypto headwinds and resumes deposit growth.

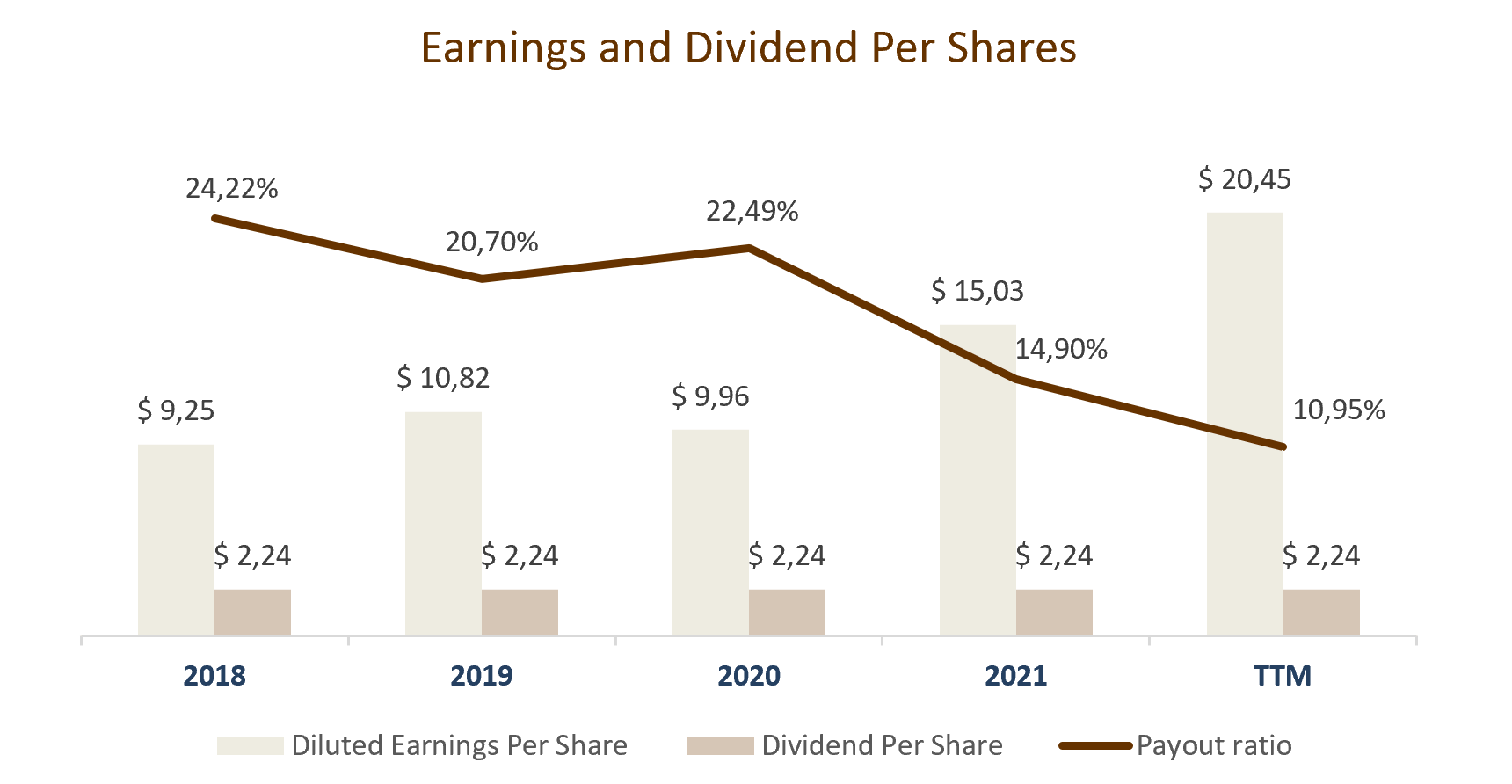

First, since the company began paying dividends, diluted earnings per share have increased from $9.25 in 2018 to $20.45 TTM, or 120%, and the book value per share has increased by 39%, from $79.65 to $110.96.

Second, even in 2018, the payout ratio was relatively low at 24.22%. However, due to strong growth in earnings per share, today the payout ratio is only 10.95% vs. 31.39% of the sector median.

Created by the author

In addition, under the previously mentioned buyback program, Signature can buy back $450 million of stock. In the third quarter of 2021, the bank has already received regulatory approval to extend the repurchase of the $170.8 million. Management is expected to seek approval for an additional $279.1 million.

Financial Performance

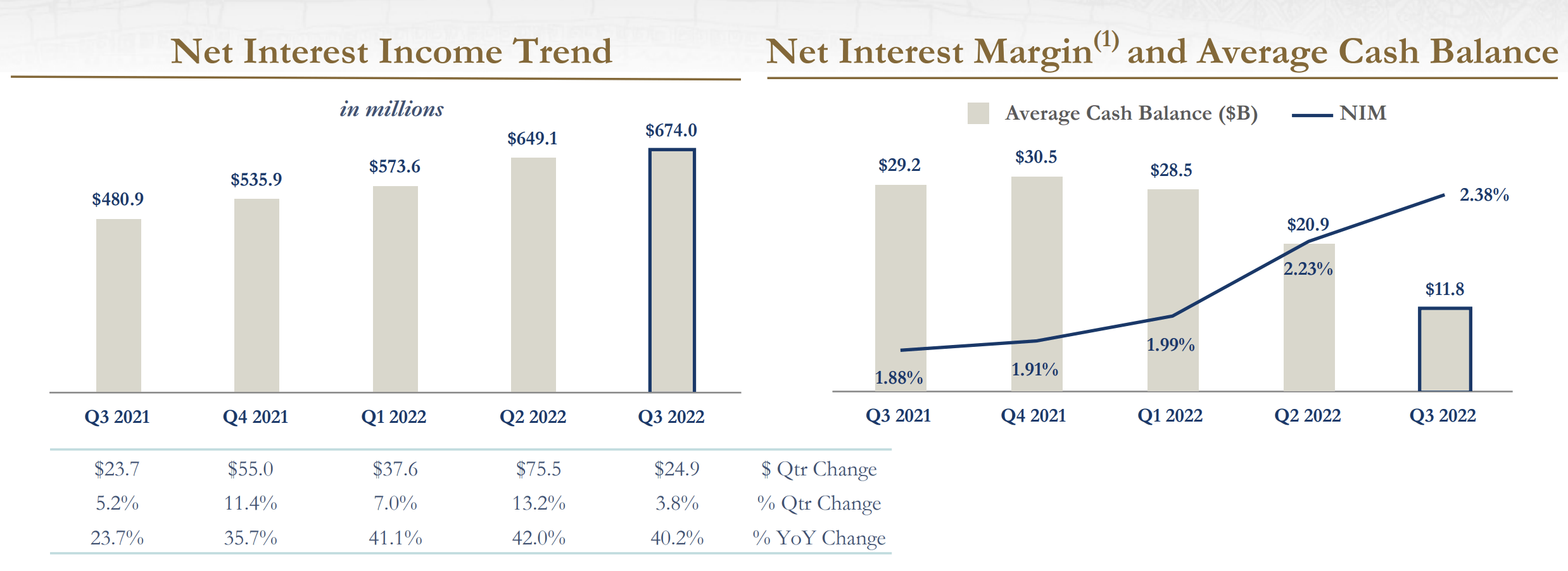

In the third quarter, Total Interest Income rose by 75.7% year-over-year to $976.4 million, driven by both loan portfolio growth and rising interest rates. Net Interest Income for the same period amounted to $674.0 million versus $480.9 million a year earlier – up 40.2% year-over-year. The Net Interest Margin has increased from 1.88% to 2.38% in the last 12 months.

Company Presentation

And although the latest quarterly results exceeded analysts’ expectations, the market took them cool. Despite the rise in NIM, there was a significant contraction in the Net Interest Spread in the third quarter. For the three months ended September 30, 2022, the figure was 69.02% against 86.53% a year earlier. The spread contraction is because the liabilities of the balance sheet turned out to be more sensitive to the interest rate growth. Signature is forced to offer higher interest rates on deposits to maintain high customer growth and cover the outflow of digital deposits. This reduces the expected net interest margin by about a quarter of a percentage point in 2023 and 2024. With the current balance of earning assets (Loans and leases + Total cash and cash equivalents), Signature could lose about $213 million a year. For comparison, over the past 12 months, Net Interest Income has amounted to $2.43 billion.

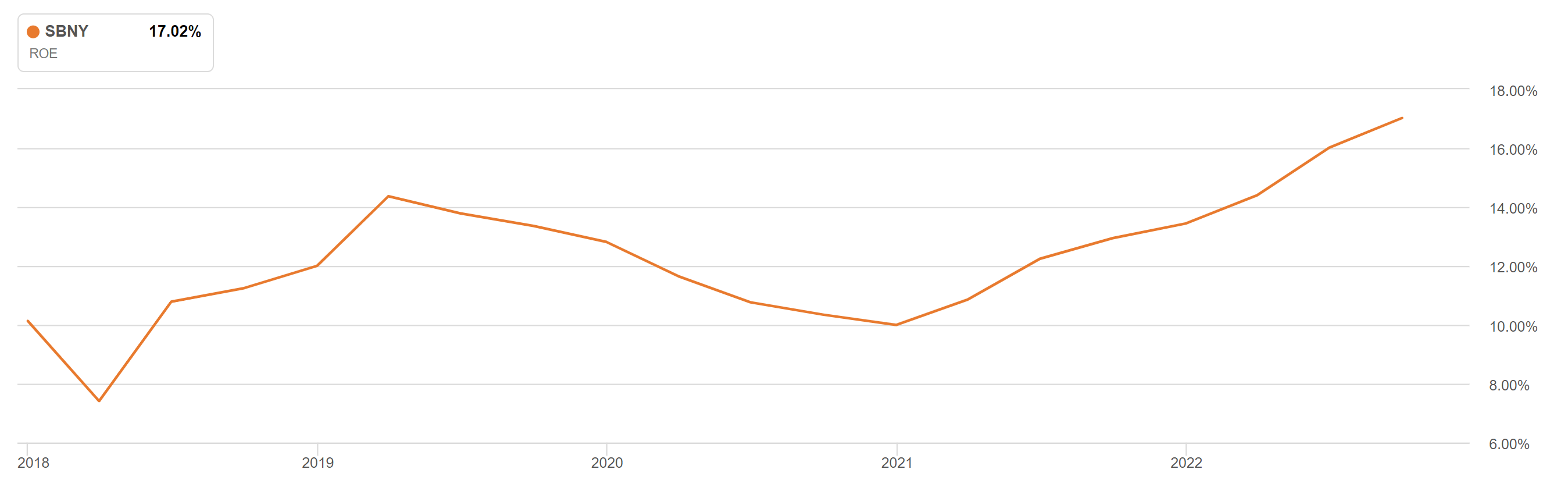

The foregone income is not critical in terms of creating shareholder value, especially given the steady growth of non-interest income. Signature is posting an impressive double-digit Return on Equity and well outperforming most US banks. At the end of the last reporting period, ROE reached 17.02% while the sector median of 11.55%. After adjusting the net income for $213 million, the ROE is 15.5%.

Seeking Alpha

It is worth noting that the bank began to gradually reduce the sensitivity of its assets to achieve an asset-liability-neutral profile. This could provide Signature with higher profitability during a period of future monetary easing. While it’s hard to pinpoint a timeline right now, it looks like the main cycle of rate hikes is behind us.

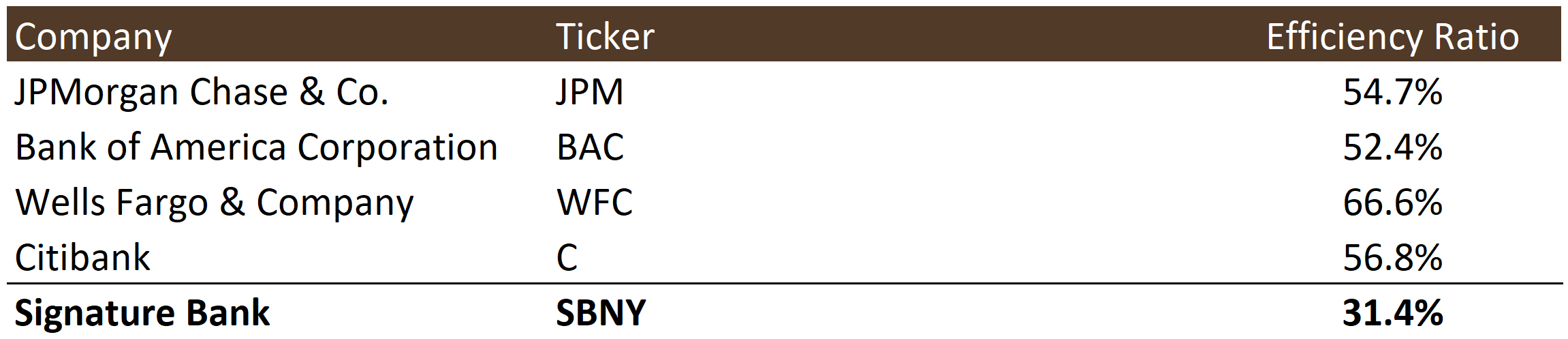

Signature demonstrates one of the best Efficiency Ratio in the banking industry – 31.4%. In this indicator, the company is surpassed only by Sallie Mae, Stifel, and Morgan Stanley, the latter two being investment banks. Efficiency Ratio = Non-Interest Expenses / Revenue, i.e. the lower the ratio, the more efficient the bank.

Created by the author

Signature has a strong balance. According to the Federal Deposit Insurance Corporation, the bank is characterized as Well Capitalized. Its capital ratios significantly exceed the regulatory requirements. Common equity Tier 1 risk-based ratio corresponds to 10.11% with an acceptable level of 6.50%, the total risk-based ratio of 11.99% with a norm of 10.00%.

SBNY Stock Valuation

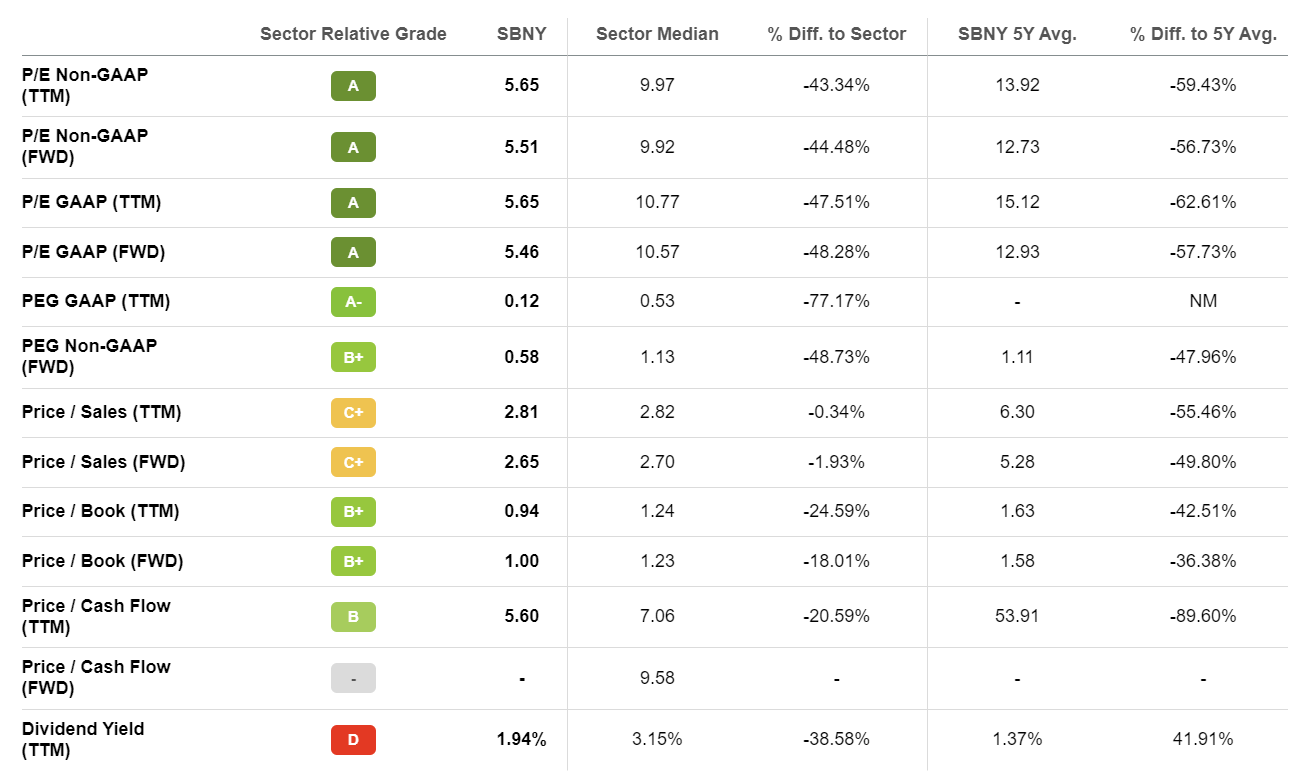

Today, Signature is trading below pre-pandemic levels and on major multiples at a discount to historical averages. Despite the impressive Return on Equity, the bank trades at a discount to its book value.

Seeking Alpha

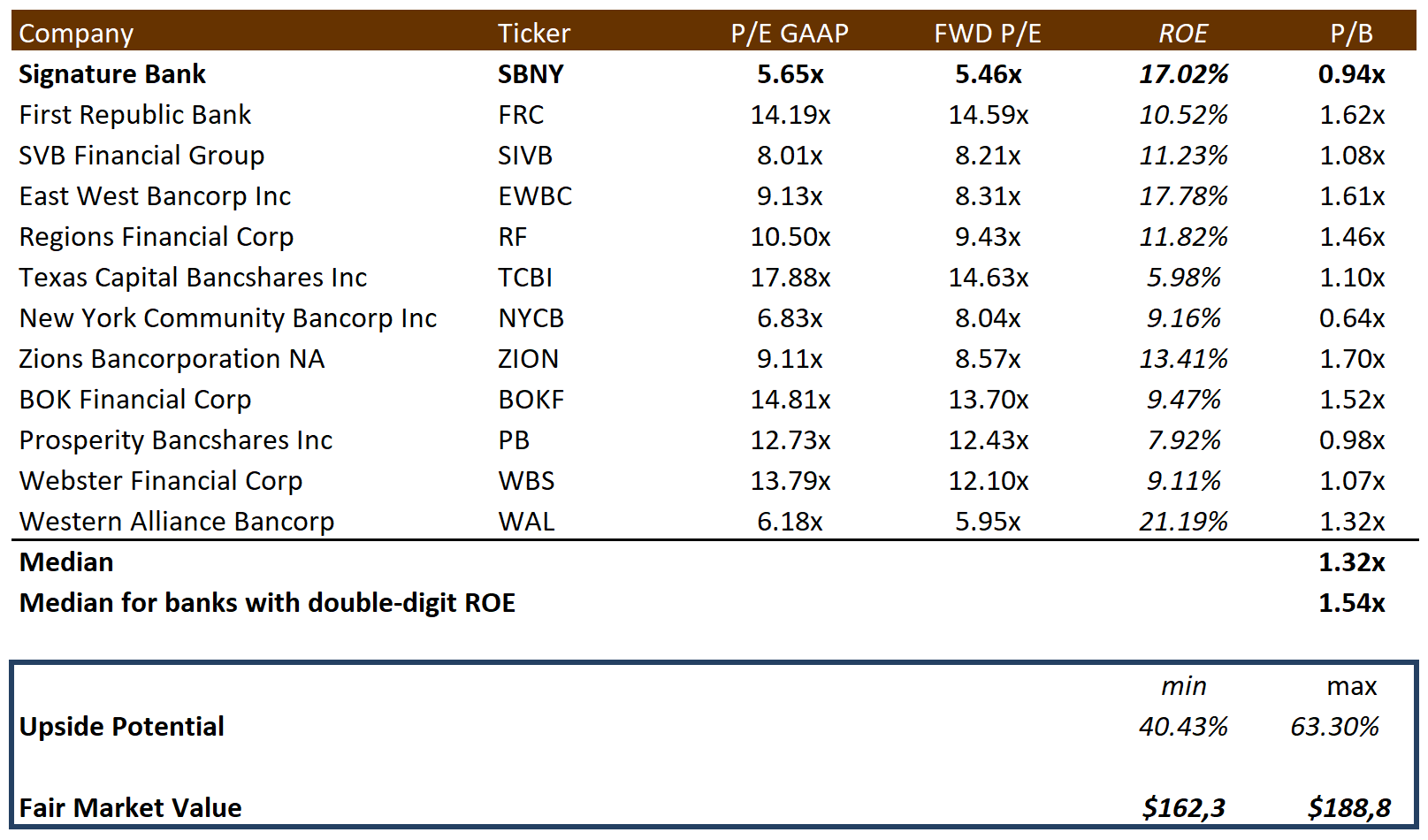

A selection of the closest peers for a comparable valuation is presented below. According to our calculations, the median P/B multiple across all banks is 1.32x. Among banks with double-digit Return on Equity, including First Republic Bank (FRC), SVB Financial Group (SIVB), East West Bancorp (EWBC), Regions Financial (RF), Zions Bancorporation (ZION) and Western Alliance Bancorp (WAL), the P/B multiple is 1.54x.

Created by the author

Thus, according to a comparable valuation, the fair market value of Signature Bank is in the range of $162-189 per share. The upside potential we see is about 40.4% at the lower end of the range.

The minimum price target from investment banks set by Morgan Stanley is $135 per share (16.77% upside potential). In turn, Maxim Group estimates SBNY at $250 (116.24% upside potential). According to the Wall Street consensus, the company’s fair market value is $172, which implies 48.9% upside potential.

Refinitiv

Key Risks

- In the event of a sharp drop in the cryptocurrency market, the bank may be forced to add short-term loans or dilute equity capital to urgently cover the outflow of digital deposits. All of these ways burn shareholder value in one way or another.

- More than half of Signature’s loan portfolio is in the commercial sector, making the company a riskier investment than traditional mortgage banks. Especially when the market expects a recession. Although we have noted that Signature has a strong portfolio, investors may demand a discount on the share price due to the wide exposure to the commercial sector.

- Signet is one of the two largest payment infrastructures for crypto companies. Due to the bankruptcy of FTX and other scandals in the crypto industry, Signature’s operations may be subject to additional regulation.

Conclusion

Signet’s prominent role in the cryptocurrency market has provided Signature Bank with a massive influx of free deposits in 2021, which has been a driver for significant growth in shares. The market fears that the outflow of digital deposits could threaten the financial stability of the bank. However, the influence of crypto on Signature is very limited, since digital deposits account for only 22.9% of all deposits of the bank. The company has a high-quality loan portfolio, Signature outperforms most US banks in terms of financial performance. According to our valuation, the company trades at a discount to its fair market value. We are bullish on SBNY.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

Be the first to comment