Mark Wilson/Getty Images News

Thesis for Potential Investment

Tyson Foods (TSN) is getting hit at all angles, including their fundamentals. As shown in this fundamental analysis and technical analysis, you will need to be fully aware of how there is little momentum in this stock. I believe market entry is not possible until early 2023 at the earliest. Shrinking markets and lower margins in their premium meat input costs do not help. Therefore, looking at the bottom line of profit levels should be a higher priority than analyzing their somewhat impressive revenue.

Valuation seems inadequate to make any investment in the short term, but fundamentals may improve to alter that decision after 4-6 months. Of course, this is under perfect conditions if the American stock market improves in the next six months.

News and Catalysts

Here is some news investors need to be aware of.

Tyson appears to be getting their credit rating not raised due to dropping profitability. Also, Tyson faces a shrinking market as USDA suspends potential orders to China.

Moody’s expects Tyson Foods’ beef operating margins to decline from current levels as lower expected cattle supplies are likely to drive higher cattle costs, and softer consumer demand for premium cuts of beef results in lower average beef prices. Moody’s expects Tyson’s operating margins to decline from current levels, as limited hog supplies result in higher costs and average sales prices fall because of weaker export and consumer demand.

Tyson Foods, Inc. — Moody’s affirms Tyson Food’s Baa2 rating; outlook stable (yahoo.com)

Smaller markets with no more China access as USDA orders no exports to a large market.

USDA Suspends Exports to China from Tyson Foods’ Indiana Pork Plant

…is reporting that Tyson Foods’ Logansport, Ind. plant has been suspended from exporting products to China, effective August 29. Neither the plant nor the USDA has indicated why exports were halted.

USDA Suspends Exports to China from Tyson Foods’ Indiana Pork Plant | Food Processing

Fundamental Data Valuation Shows Long-Term Stock Price Declines

Many metrics below are highlighted to showcase the continued long-term weakness of Tyson Foods.

Free cash flow growth has been negative last year at -0.016

|

2019 |

2020 |

2021 |

2022 |

|

|

Dividend growth |

-0.621 |

-0.59 |

-0.581 |

-0.619 |

Source: Financial Modelling Prep

Dividend growth has been negative for the last few years:

Last year was the worst of the previous four years.

An optimistic forecast for revenue and dividend growth contrasts with dividend growth.

|

2022 |

2023 |

2024 |

2025 |

|

|

Revenue |

53,013 |

54,393 |

54,974 |

58,650 |

|

Dividend |

1.82 |

1.98 |

2.26 |

3.13 |

Source: 6+

Don’t be fooled by the rising EBITDA over the years:

|

2018 |

2019 |

2020 |

2022 |

|

|

EBITDA |

$4.22B |

$3.94B |

$4.8B |

$5.91B |

Source: Financial Modelling Prep

Forward P/E is 9.246 is greater than the trailing P/E is 6.380. As a result, it is expected that earnings should decline.

The current market price is far from the target price of $92.33.

The simple mean average of 20 days is -4.96%, the simple moving average of 50 days is -11.01% and the simple moving average of 200 is -18.42%. This is not a strong year for Tyson.

Other Warnings:

No consistent historical earnings per share

NOT consistently high return on equity

NOT consistently high return on assets

Forward Guiding Technical Analysis Show Major Drawdown Until Next Year

Most technical charts used here use forward guidance to not rely on past patterns except for the Hurst Cycles. To minimize volatility in these charts, it was chosen to use a weekly timeframe to smooth out the price action.

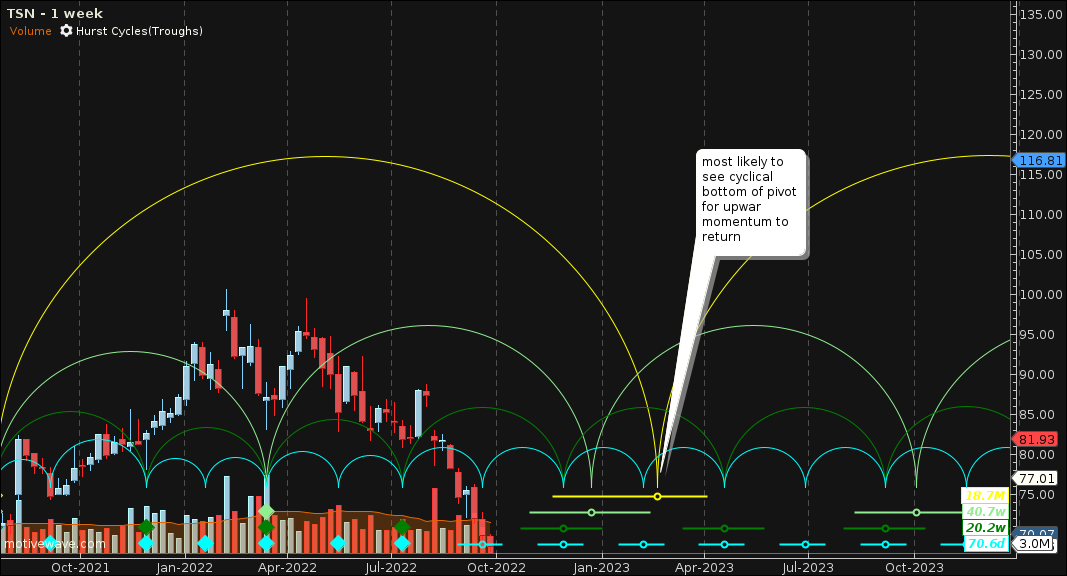

Hurst Cycles

Semi cycles in yellow show reliability for guidance on the next potential upswing based on historical Hurst Cycles. The most reliable reversal in an upswing could be in early 2023. Your investment might be flat for the next four to six months. I believe this is not wise as you could deploy your investment into an alternative instrument with higher predictable upswings in the short term.

Hurst Cycles show reversal in 2023 (MotiveWave trading platform)

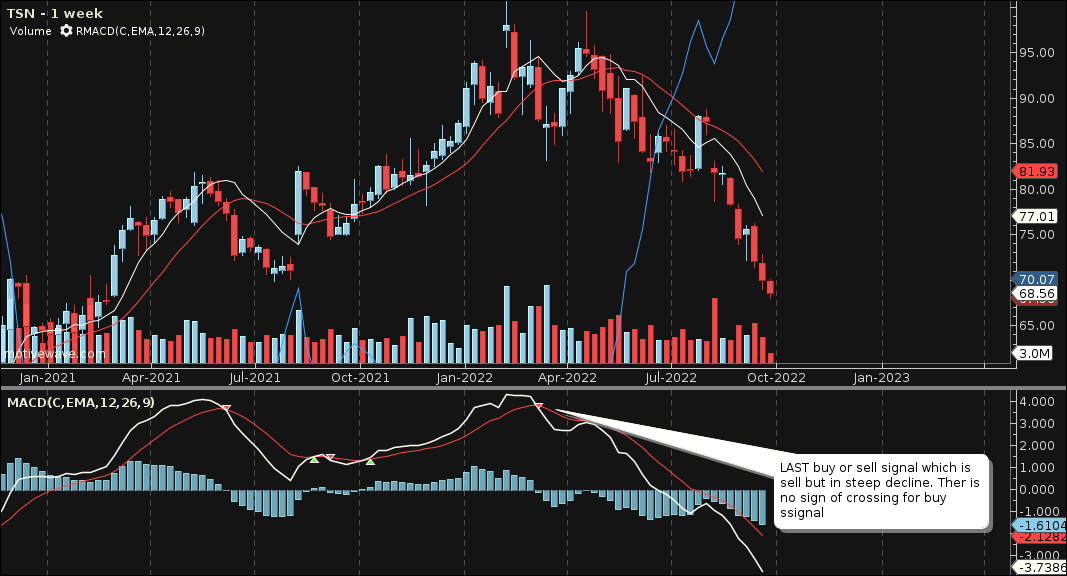

MACD RSI

This MACD RSI technical pattern combination shows that the last trading signal was a sell-back in April this year. If you are familiar with RSI guidance lines, it shows no potential for an upswing with the potential cross to signify an entry or buy signal. This combined set of indicators is pretty reliable in showing weakness in stock price. As a result, you can imagine, there could be a prolonged drop in price before the next upswing. This could be based upon relying on major USA market indices that could be correlated back to this stock of Tyson Foods.

MACD RSI sell signal last April (MotiveWave trading )

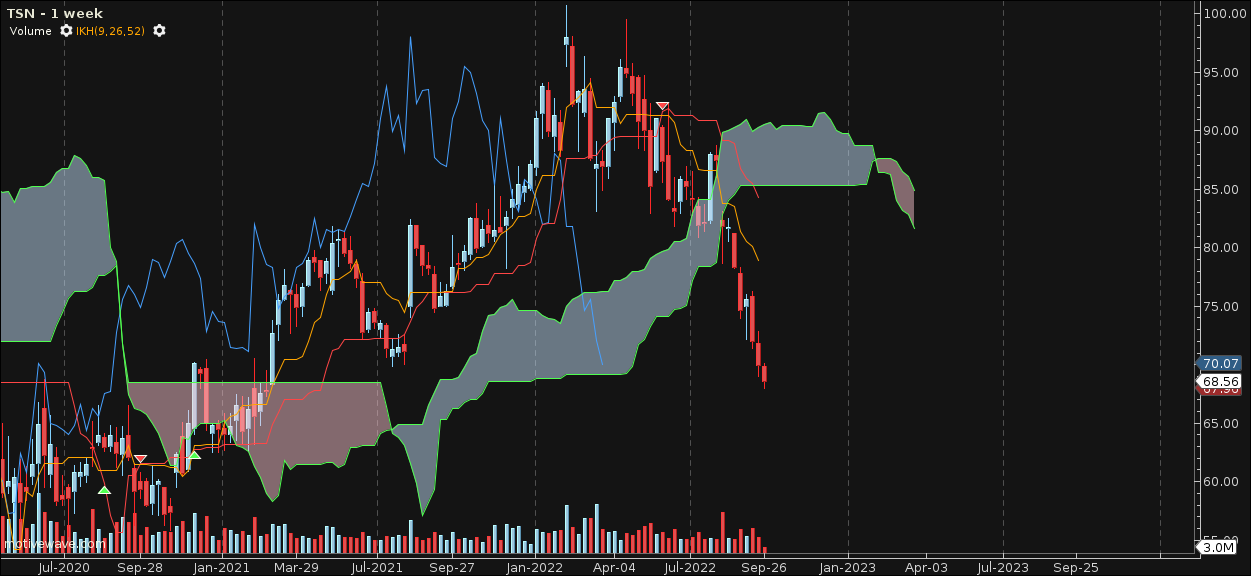

Ichimoku Cloud

Lastly, this Ichimoku Cloud shows that the stock price of Tyson Foods could be flat at best over the next few months.

flat at best (MotiveWave trading platform)

Are the Risks Worth Taking with a Weak Substandard Outlook?

As hinted at with both fundamental and technical analysis, looking at another alternative that provides better returns and higher dividend income growth is wise. There may be some small short-term income in this current quarter, but I believe it is not worth deploying capital into. Also, as hinted in this article:

Tyson Foods: A Boring, Stable Company With Consistent Results (NYSE: TSN) | Seeking Alpha

Another potential risk factor for Tyson is if they cannot attract, hire or retain key employees. They compete with other companies to hire highly skilled employees, and the inability to do so could increase costs and hamper operations.

As mentioned earlier in this article, it does not help to have the USA government limit your export markets and not get a boost in credit rating due to rising input costs.

As a result, Tyson Foods does not have a strong outlook as compared to other companies to invest in.

To change a positive outlook, Tyson will need to implement cost-cutting or reposition itself in the market. An example of repositioning is by marketing itself as a premium brand to justify any added input costs. Other changes might be needed to eliminate lower margin products to improve long-term share growth and dividend income growth. Since I would not consider TSN a top-performing stock, Tyson Foods is a company that needs to change as its stock performs on par with major stock market indices at best.

Conclusion

As you can imagine, this is not a company going into bankruptcy or losing significant market share. Tyson Foods should remain a considerable force within the food processing industry. It is wise to consider this a sell that could be considered for potential shorting in a reasonably predictable way until its subsequent market reversal. As hinted with the Hurst Cycles, this will likely not be until early next year when one might see potential market entry.

Be the first to comment