Sean Gallup

What a difference a year makes, as 2022 has been horrific for growth stocks. As the tailwinds disappeared, many of the most popular stocks from 2021 are down more than -50% in 2022. Shopify (NYSE:SHOP) was one of the pandemic heroes that investors couldn’t get enough of, and now it’s become one of the hardest hit growth stocks. While a $34.03 billion market cap is nothing to dismiss, SHOP has declined -80.24% YTD falling from $136.31 to $26.94 in 2022. Looking at its 52-week trend, SHOP has declined by -84.72% from its highs, declining from $176.29 to $26.94. SHOP’s share price of $26.94 may look attractive considering when it was less than 1 year ago, but it’s financials tell another story.

I want to love SHOP, as this platform drastically helps businesses of all sizes reach a larger customer base, and e-commerce is projected to take more market share from brick and mortar over the next several years, but not at this valuation. SHOP could fall by another 50%, placing its share price at $13.47, which would bring its 52-week decline to -90.12% from -80.24%, and it would still have a $17.15 billion market cap. Investors need to understand that a company and its stock are two separate things. SHOP is a great company in my opinion, but I don’t believe its stock is great or represents an opportunity today. My hesitation with investing in SHOP isn’t its business; it’s the income statement and, on a more granular level, the cost of running the business.

I want to own Shopify, but not at a $34.03 billion valuation

Millions of businesses utilize SHOP to start, grow and manage their businesses. SHOP’s platform allows someone to create and customize an online store and then sell virtually through multiple e-commerce platforms, including on the web, through social media, and through marketplaces. All of the inventory and product management, payment processing, and shipping can be taken care of through SHOP’s platform. Regardless of how big or small a company is or the technological proficiency of the end user, SHOP makes it easy to build an online store without coding and connect to customers on all of the major platforms. For me, the proof is in the numbers. Millions of merchants across 175 countries utilize SHOP for their business. From a business and capitalist standpoint, I love that SHOP supported 5 million jobs in 2021 and $444 billion in global economic activity. Hosting the entire backend and making it possible that anyone can create an online store and sell through 3rd party marketplaces such as Amazon (AMZN) and eBay (EBAY), in addition to social media platforms such as Instagram, provides tremendous opportunities for millions of businesses.

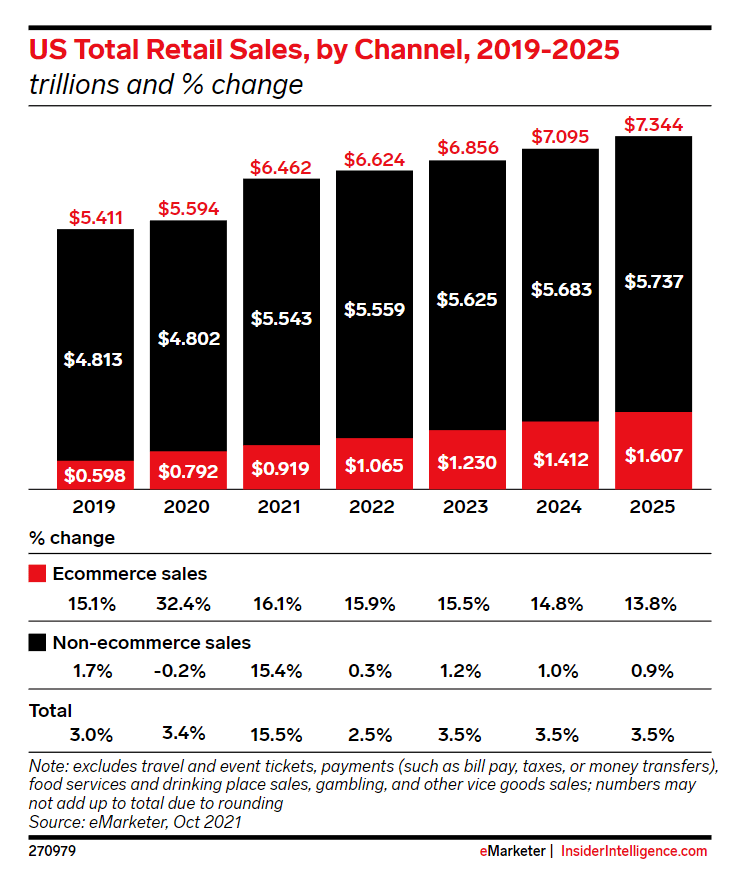

There is still a tremendous opportunity in e-commerce, and I believe more companies will utilize SHOP in the future. In the U.S, total retail sales are expected to reach $6.62 trillion in 2022. E-commerce is projected to total $1.07 trillion in sales, which is 16.08% of the retail sector. Many people, including myself, wouldn’t have guessed that e-commerce is still under 20% of retail sales in America. In 2025 e-commerce sales will grow to $1.61 trillion, which is a 50.89% increase from where they will finish in 2022. The entire retail sector is expected to grow, which means that even at $1.61 trillion, e-commerce will represent 21.88% of total retail sold in 2025 across the U.S.

Insider Intelligence

I believe SHOP has strong future growth potential as it should generate additional revenue as more commerce is conducted online over the years. I want to be invested in SHOP because its platforms enable businesses to reach a larger pool of customers and create a frictionless selling process. SHOP has created a platform that helps businesses grow by streamlining remedial tasks and simplifies many aspects of running an e-commerce business to deliver value on day 1. While I believe SHOP will ultimately appreciate in the future, I think it is still at risk of seeing further value destruction as it trades at too rich of a valuation.

Shopify’s $34.03 billion valuation is too expensive for me, and I think shares will fall further before appreciating

Just because a stock has fell -84.72% from its 52-week highs, that doesn’t mean it’s done falling. SHOP’s income and cash flow statements are concerning when it comes to the valuation. SHOP has a strong balance sheet, and there are no red flags there, in my opinion.

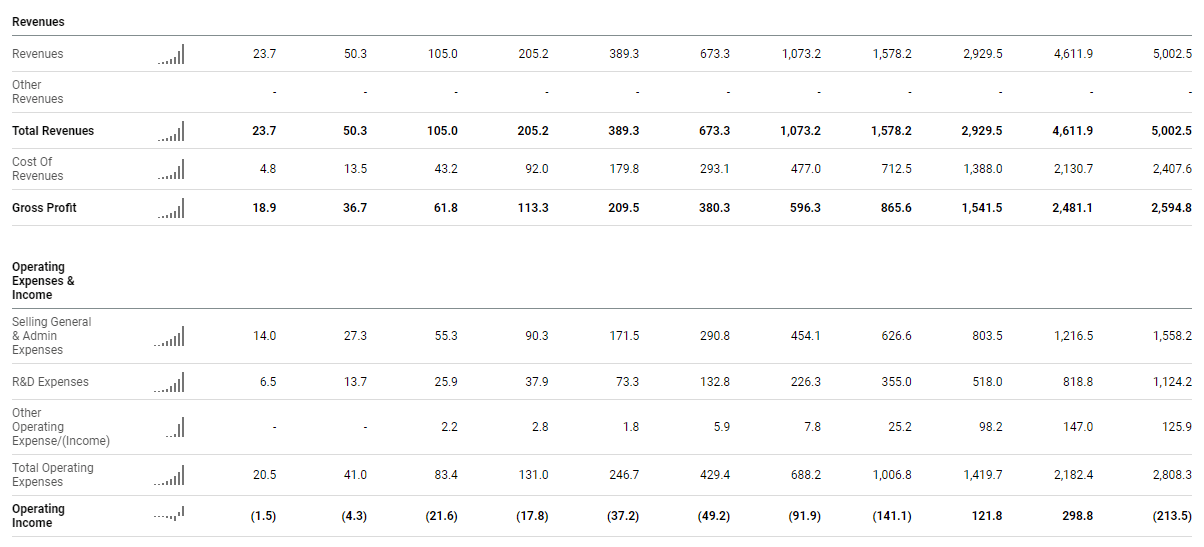

SHOP is running a capital-intensive business as its costs continue to rise. In the TTM, SHOP has generated just over $5 billion of revenue. The problem is that even with $5 billion of revenue, SHOP loses money. In the TTM, SHOP’s cost of revenue was $2.41 billion, leaving them with a gross profit of $2.6 billion or 48.13%. This is very low for a SaaS company as most SaaS companies that I have seen have a 70-85% gross margin. Next, SHOP’s total operating expenses have come in at $2.8 billion as selling, general and admin was $1.56 billion, R&D was $1.12 billion, and its other expenses were $125.9 million. SHOP’s operating income in the TTM was -$213.5 million.

Seeking Alpha

Prior to dissecting the expenses, the first problem is that growth is dramatically slowing down for SHOP. SHOP grew its revenue in 2021 by $1.68 billion or 57.43% YoY to $4.61 billion from $2.93 billion. After Q4 2019, SHOP’s quarterly revenue increased in 3 of the next 4 quarters in 2020 compared to Q4 2019. SHOP had a similar trajectory in 2021, as each quarter in 2021 represented consecutive QoQ growth since Q4 of 2020.

In 2022, SHOP has broken its trend, and this is now the first time in the past 2 consecutive years where growth is not just slowing, but reversing. SHOP had 7 quarters of consecutive QoQ revenue growth from Q1 2020 thru Q4 2021, and now the revenue growth has disappeared. In Q4 of 2021, SHOP delivered $1.38 billion in revenue. In Q1 of 2022, SHOP generated $1.2 billion of revenue which was a -12.78% decline QoQ, then $1.3 billion of revenue in Q2 2022, which was a -6.15% decline from Q4 2021. SHOP had 7 consecutive quarters of growth and now its revenue hasn’t exceeded Q4 2021’s revenue in 2 quarters, and its expenses have increased.

Seeking Alpha, Steven Fiorillo

In Q4 2021, SHOP generated its largest quarterly revenue at $1.38 billion. SHOP spent $687.4 million on its cost of revenue and $732.2 million on total operating expenses bringing its total expenses to $1.42 billion. In Q2 of 2022, SHOP generated $1.3 billion in revenue while its cost of revenue was $639.4 million, and its total expenses were $803.5 million. SHOP’s revenue declined by $84.9 million, yet its expenses increased by $23.3 million. SHOP’s margins are low for a SaaS company, and their expenses are impacting their operating income as this is now a $34 billion company with negative operating income.

Last year, SHOP generated $2.91 billion in net income, and this year it lost -$1.9 billion in net income. Their line item for EBT, INCL Unusual items, included $3.14 billion in 2021 and a loss of -$1.99 billion in 2022. This is why I like looking at free cash flow (FCF) as FCF is not as easily manipulated as net income is. In 2021 SHOP generated $453.6 million in FCF, and in the TTM for 2022, SHOP has generated $58.8 million of FCF. SHOP isn’t producing the type of FCF or cash from operations that I would like to see from a company of its size, and when I look at its price to FCF metric, it is egregious.

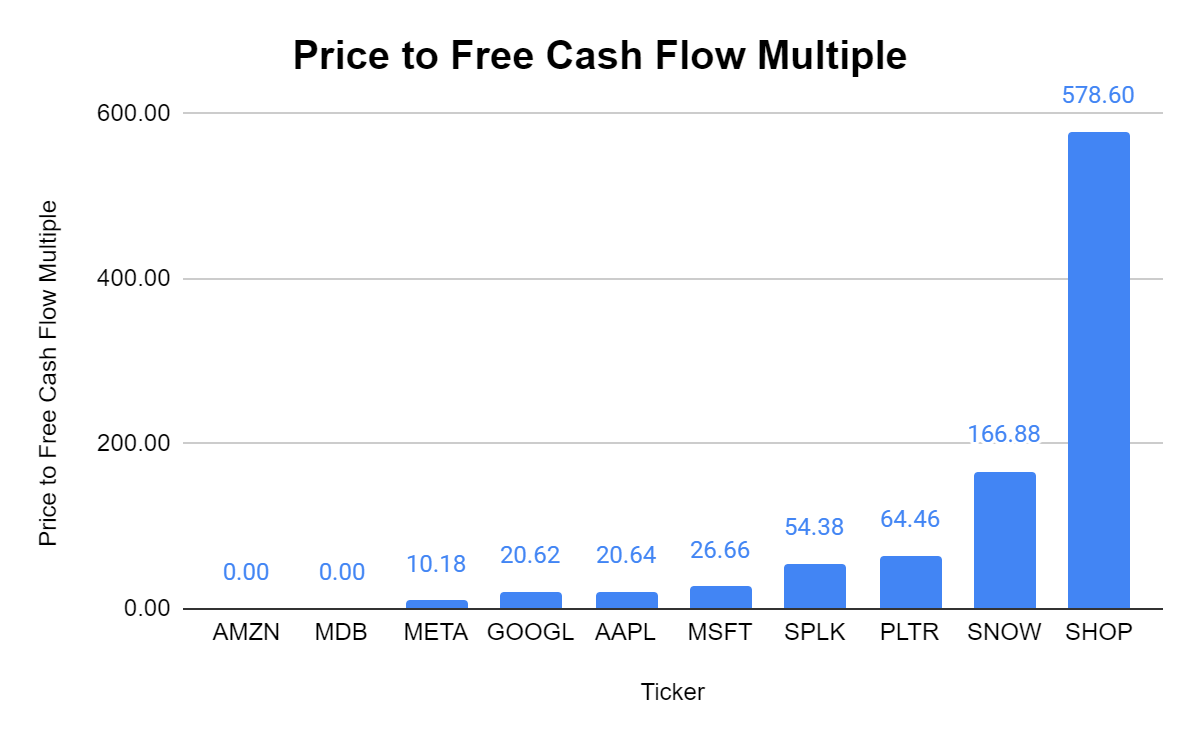

SHOP has created a great business that is critical to millions of organizations, but that doesn’t mean it’s investable. SHOP has a $34 billion market cap, and its income statement and cash flow statement look sub-par for a $34 billion market cap. I wanted to see how the market was valuing SHOP, so I compared it to the following companies:

I picked these companies because I wanted to compare SHOP to other growth companies that have been hit hard in 2022, and big tech.

Since the growth companies don’t have positive earnings yet, I am sticking to looking at the FCF metric. FCF is often looked at as one of the best measures of profitability as FCF excludes the non-cash expenses of the income statement and includes spending on equipment and assets as well as changes in working capital from the balance sheet. To some investors, FCF is more important to analyze than net income because it’s harder to manipulate as it is a true indication of the company’s cash. FCF is also the pool of capital that companies can utilize to repay debt, pay dividends, buy back shares, make acquisitions, or reinvest in the business. With every investment, you’re paying the current value for a company’s present and future cash flow.

I thought SNOW’s FCF multiple was crazy, but SHOP is trading at 578.60x its FCF. There is no way I would pay this valuation when I can buy META at 10.18x its FCF. Now, META is a more mature company, but SHOP is making SNOW look cheap. If I was to substitute the TTM FCF, for 2021’s, SHOP would trade at 75x its FCF with declining revenue. That would make it the 2nd largest valuation instead of the largest valuation among the extended peer group I created.

Steven Fiorillo, Seeking Alpha

|

Price to Free Cash Flow |

|||

|

Ticker |

Market Cap |

Total Free Cash Flow |

Price to Free Cash Flow Multiple |

|

AMZN |

$1,151,193,150,000.00 |

-$29,784,000,000.00 |

0.00 |

|

MDB |

$13,642,473,665.00 |

-$27,500,000.00 |

0.00 |

|

META |

$364,646,492,955.00 |

$35,830,000,000.00 |

10.18 |

|

GOOGL |

$1,251,723,744,968.00 |

$60,697,000,000.00 |

20.62 |

|

AAPL |

$2,220,977,600,955.00 |

$107,582,000,000.00 |

20.64 |

|

MSFT |

$1,736,942,768,380.00 |

$65,149,000,000.00 |

26.66 |

|

SPLK |

$12,235,708,783.00 |

$225,000,000.00 |

54.38 |

|

PLTR |

$16,773,466,646.00 |

$260,200,000.00 |

64.46 |

|

SNOW |

$54,387,202,148.00 |

$325,900,000.00 |

166.88 |

|

SHOP |

$34,021,556,834.00 |

$58,800,000.00 |

578.60 |

Conclusion

I want to own SHOP as a long-term investment, but the valuation is still well outside my comfort zone. SHOP has declined so much that I don’t think it’s worth abandoning if you have a long time horizon, but it’s not a buy yet, in my opinion. I am placing SHOP on my watchlist, and I think it could be very interesting around the $16 level if its cash from operations can increase in Q3. I think Q3 earnings will be critical for SHOP, and I want to see revenue increase above Q4 2021, their expenses decline, and FCF increase. Long-term, I believe SHOP will be a winner but paying 578.6x its FCF is not something I am willing to do as growth is slowing and its margins are well below typical SaaS companies.

Be the first to comment