Justin Sullivan

Mature and Consistent

Oracle (NYSE:ORCL) is a mature technology company. The corporation was founded in 1977 and has a well-established competitive advantage built by proprietary hardware/software synergies, massive switching costs for current clients, and licensing policies that lock in profits. The question is, will the long run of success keep pace with today’s fast pace of innovation?

Oracle’s cloud infrastructure (OCI) is a unique cloud offering because of the availability of Exadata hardware, which is optimized to run massive Enterprise Resource Planning (ERP) information technology systems. The unique nature of Exadata is why Azure allows Oracle to provide a full stack OCI cloud hosting service, with Azure simply acting as the web interface. Unique value is created by Exadata and the custom software that runs it.

An ERP, as its name implies, is intended to cover the entire scope of corporate operations. It handles all data, from payroll to customer resource management and everything in between. Once a corporation transitions to an ERP, the ERP becomes the nervous system of the corporation. It becomes so ingrained in operations removing it becomes expensive and time-consuming thus most managers accept the current system despite perceived shortcomings. Customer lock-in that already exists from Exadata and custom code is strengthened by the very nature of an ERP.

Oracle is everywhere in the business-to-business world. Primarily, it provides products and services that address enterprise information technology environments worldwide. The company markets and sells its cloud, license, hardware, support, and services offerings directly to businesses in various industries, government agencies, and educational institutions, as well as through indirect channels.

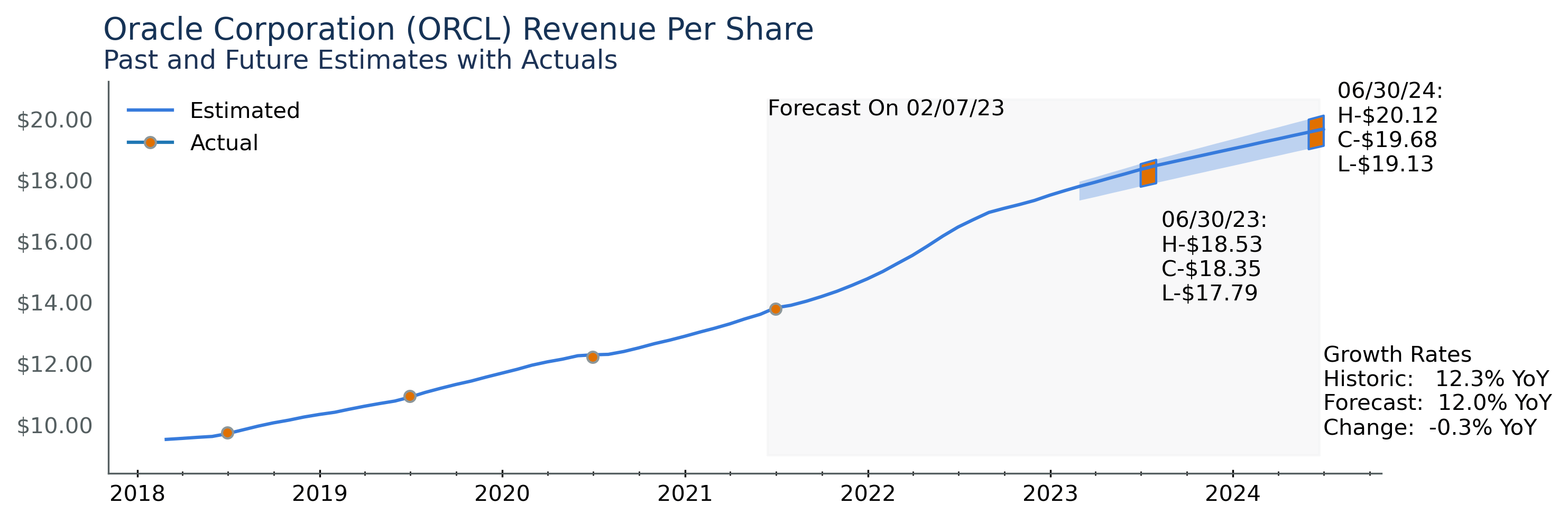

Oracle Revenue and Earnings Expectations

This chart shows the last 8 years of earnings and revenue as well as forecasts for the next 2 years from nine sell-side analysts reporting from major brokerage houses.

Author’s Image from Financial Modeling Prep Data

The revenue forecasts show that revenues are projected to grow at 12.0% over the next two years. This is in line with Oracle’s historic growth trend of 12.3%.

The revenue picture for Oracle is stable, which is to be expected. Oracle has been on the software as a service bandwagon before there was a bandwagon. Oracle’s licensing is in year or multiyear increments and therefore mostly immune to temporary changes in macroeconomic conditions.

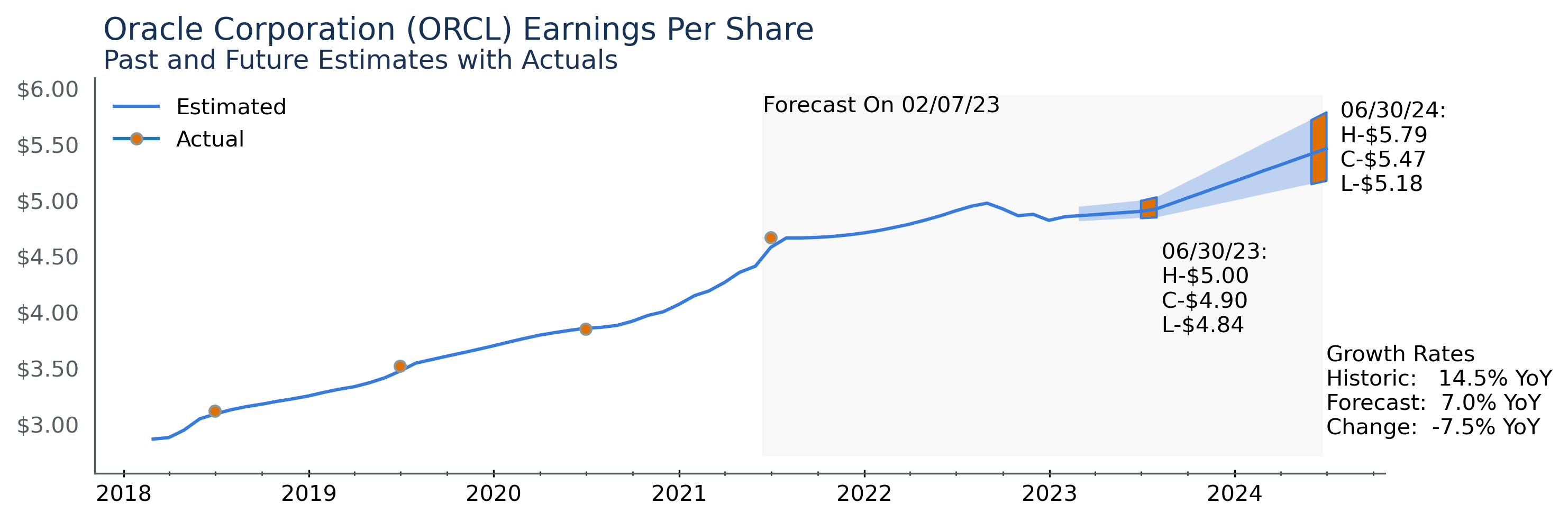

In the chart below, you can see Oracle’s earnings growth rate decreases significantly due to downward revisions seen in the second half of 2022. This decrease in margins is likely due to increased costs. Oracle, like all companies, is not immune to short-term cost increases.

Author’s Image from Financial Modeling Prep Data

Pro Forma earnings per share expectations are expected to be between$4.84 and$5.00 next year and$5.18 and$5.79 in 2024. This places Oracle on a most likely growth rate of 7.0%. We need to look at the basis of the estimate here, though. Earnings in 2021 and 2022 are well above trend. The estimates in 2023 and 2024 appear to be a return to long-term trends.

Oracle’s revenue streams are long-term, and a constant revenue picture coupled with changes in earnings is almost always caused by increased costs. This combined with Oracle’s unique offerings of Exadata, the software to run it, and customer lock-in through the nature of ERP offerings make Oracle a good long-term bet.

Growth Potential

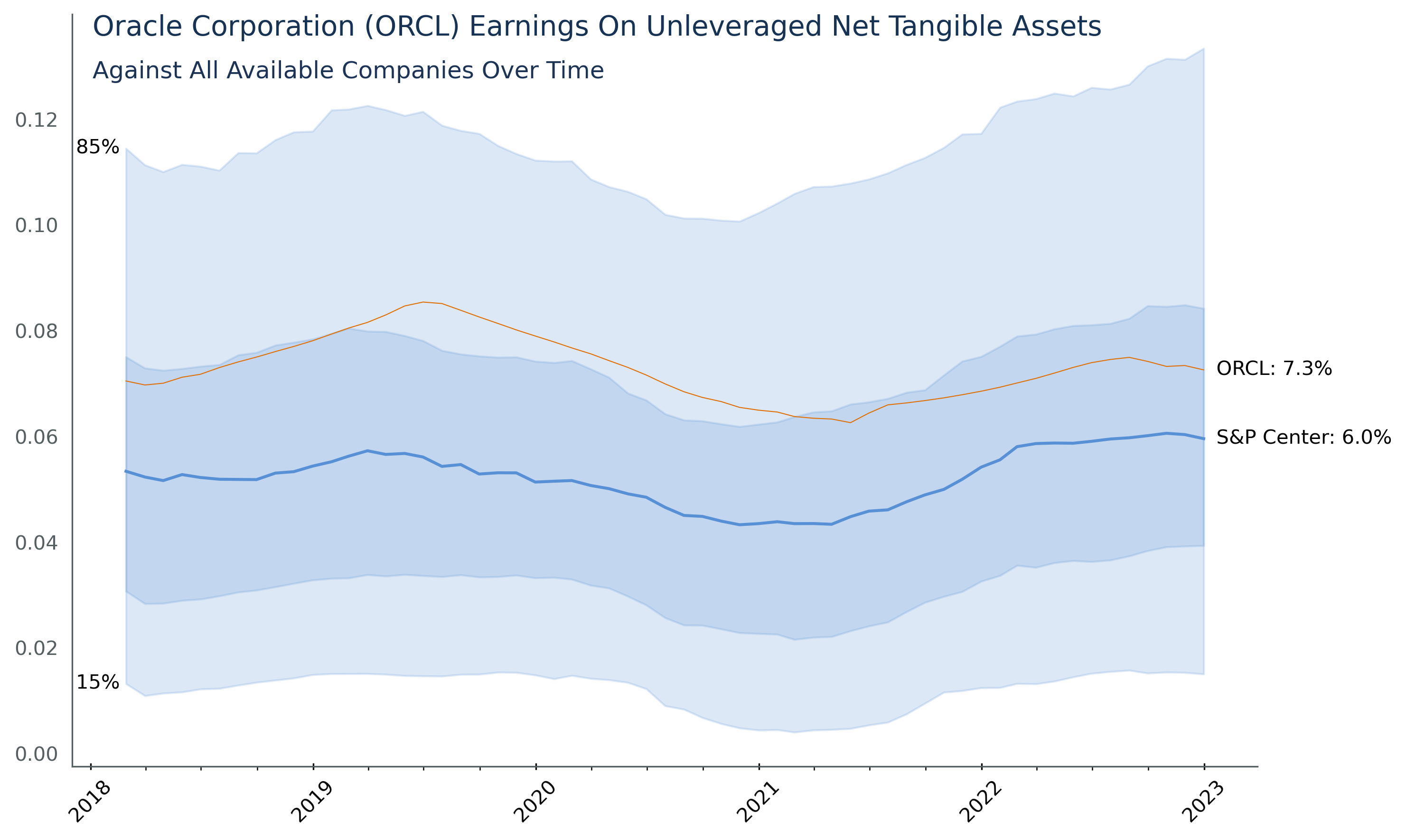

In his 2007 Letter to Shareholders, Warren Buffett provided us with clear insight into what it takes to be a great business. He put it simply: “it is far better to have an ever-increasing stream of earnings with virtually no major capital requirements.” He has spoken of this concept repeatedly and further defines it as returns on unleveraged net tangible assets. If a company needs less money to grow, it can grow faster. We unleverage the assets to compare companies on a risk-adjusted basis, this way a company with a bigger debt and risk appetite does not appear superior to a company with less debt.

Oracle’s Earnings on Unleveraged Net Tangible Assets can be seen in the chart below.

Author’s Image from Financial Modeling Prep Data

Oracle is in the middle third of companies. At 7.3% it is close to the typical company in the S&P 500. The takeaway is that Oracle will not grow as fast as other technology companies like Microsoft, which is in pulling in 13.6% on Unleveraged Net Tangible Assets.

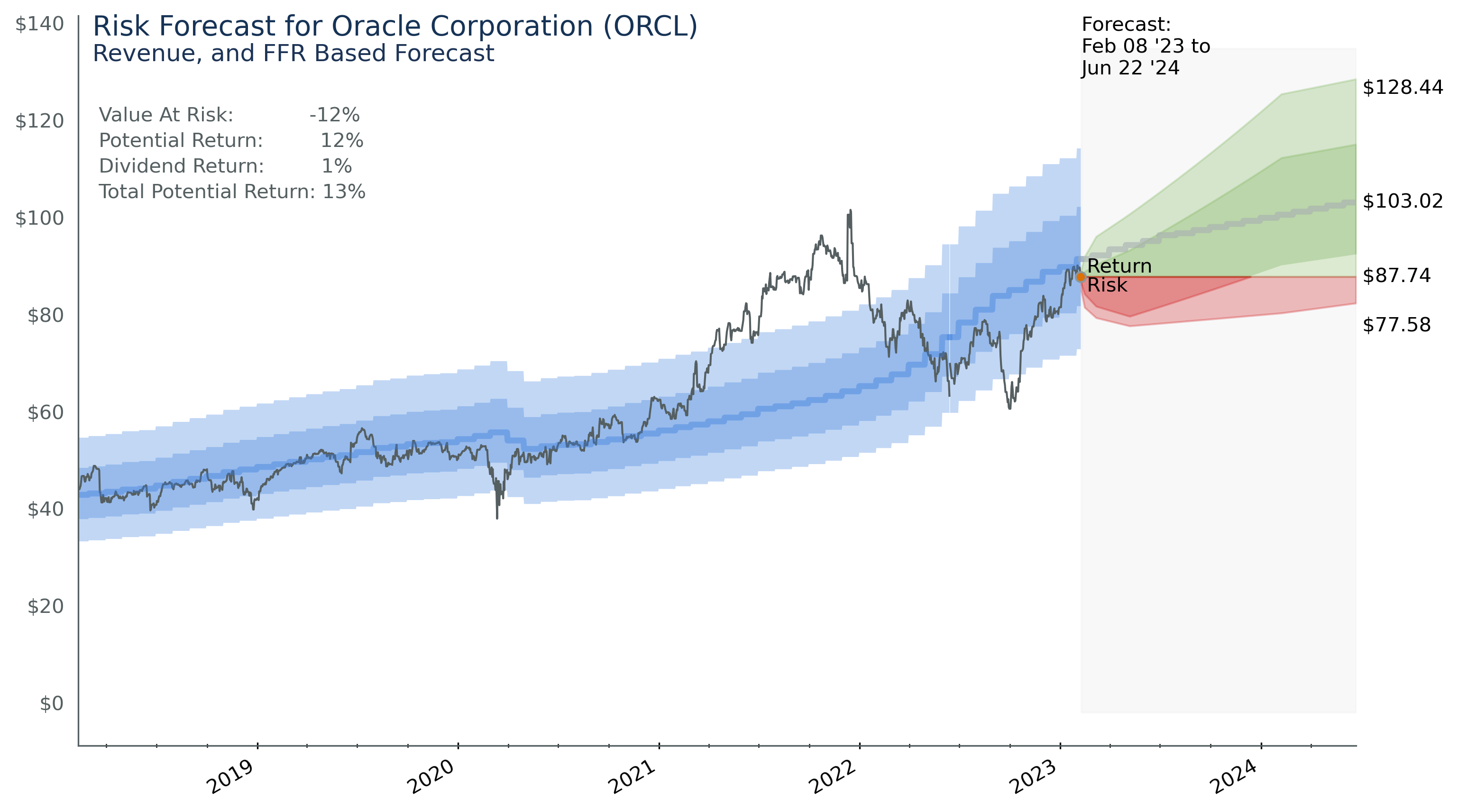

Risk Forecast

I always run my portfolio through a Risk Forecast to decide what the numbers say. My AI generates predictions based on past data and future forecasts from analysts at major brokerage houses.

As shown by the blue intrinsic value region in the chart below, Oracle is in line with its intrinsic value.

Author’s Image from Financial Modeling Prep Data

Oracle’s risk is balanced by potential returns. Oracle now has a value at risk of 12% while potential returns are 13%. This 13% is based on the long-term central value that Oracle has traded at and the long-term price prediction of $103.02.

In the case of Oracle, historic data on revenue and federal funds rate is used to train a series of machine learning algorithms to create a forecast of price risk. The chart needs some explanation. The blue bands represent the predicted intrinsic value of the company, with the actual price data shown against the prediction. The grey forecast portion shows how the price of$87.74 at the time of forecast relates to the intrinsic value of the company.

The algorithms do a pretty good job of predicting long-term price movement, but the price will go outside the blue bands. Those bands are only there to show you where the price should be 90% of the time. This forecast, and our forecasts for other stocks as well, tend to lag price when it goes down and lead when it goes up. This makes it useful to figure out risk in a stock, but it is less dependable for market timing.

Return to Shareholders/Capitol Allocation

Warren Buffett teaches us there are two ways a company can distribute capital and create value for its shareholders. First, and foremost, the company can increase long-term earnings power, thereby increasing the intrinsic value of the shares. The second way a company can create value is by returning excess cash to shareholders. Long-term earnings power can come through acquisitions or internal growth while excess cash can be returned through dividends or share repurchases.

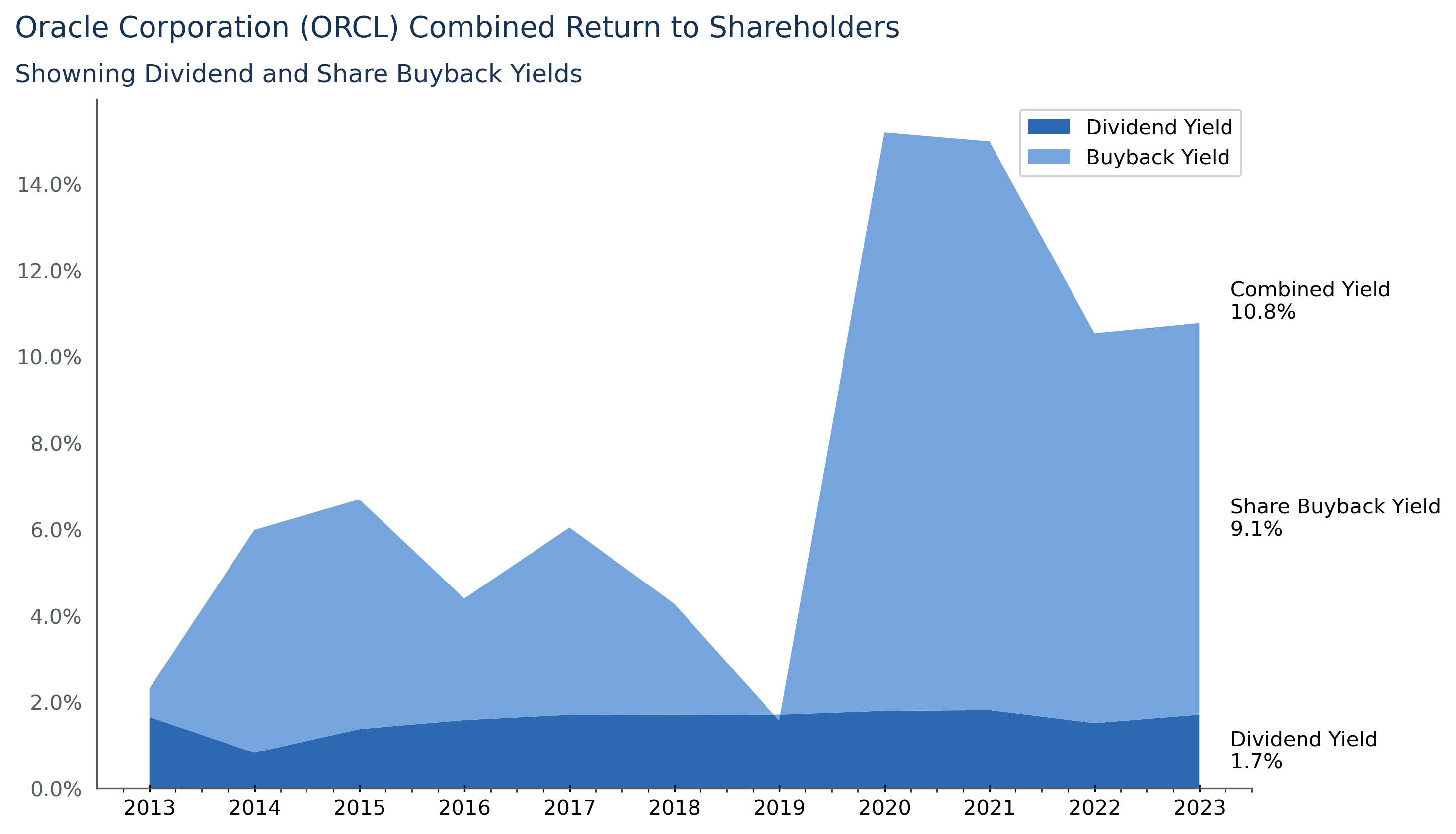

Author’s Image from Financial Modeling Prep Data

As shown above, Oracle’s dividend yield is a solid 2% and combines with a Share Buyback Yield of 9.1% resulting in a Combined Yield of 11%. This is a huge yield! However, the yield should not be calculated in future forecasts. Oracle has purchased only $2 billion shares over its first two quarters this year, which is much lower than the $16 billion over those same two quarters last year. The return forecast presented earlier is accurate and accounts for this decrease in share repurchases.

Final Word

Oracle is a juggernaut of a company. Some of its core technologies and business strategies have proven it can provide long-term value for its customers. Current analyst forecasts expect Oracle to continue to deliver revenues in line with the company’s historic performance. This stable revenue growth and current fair valuation make Oracle a buy as an underweight holding in a diversified portfolio.

Be the first to comment